Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

2. A single plantwide overhead rate will provide accurate product costing if products use

p

roduction department activity-base quantities in nearly the same ratio across departments.

For example, if Product X used 2 hours of Department A and 4 hours of Department B

3. Under the multiple production department rate method, factory overhead rates are determined

for each production department. Factory overhead is allocated to products depending on the

4. When there are significant differences in the factory overhead rates across different production

5. Under activity-based costing, factory overhead costs are assigned to activity cost pools rather

6. These activities are part of selling and administrative expenses, which must be treated as

7. If the costs listed in Discussion Question 6 were included as product costs, then they would be

8. Calculating product costs using activity rates may result in greater accuracy than using

9. Activity-based costing would be preferred over the relative sales value method when the

10. Service companies can use activity-based costing to determine the cost of service offerings.

CHAPTER 26 (FIN MAN); CHAPTER 11 (MAN)

COST ALLOCATION AND ACTIVITY-BASED COSTING

DISCUSSION QUESTIONS

CHAPTER 26 Cost Allocation and Activity-Based Costing

PE 26–1A (FIN MAN); PE 11–1A (MAN)

a. Jeans: 15,000 units × 0.15 direct labor hour = 2,250 direct labor hours

b. Single plantwide factory overhead rate:

PE 26–1B (FIN MAN); PE 11–1B (MAN)

a. Speedboat: 250 units × 12 direct labor hours = 3,000 direct labor hours

PE 26–2A (FIN MAN); PE 11–2A (MAN)

a. Cutting: (15,000 jeans × 0.05 dlh) + (15,000 khakis × 0.10 dlh)

b. Cutting Department rate: $72,000 ÷ 2,250 dlh = $32 per dlh

PRACTICE EXERCISES

CHAPTER 26 Cost Allocation and Activity-Based Costing

PE 26–2B (FIN MAN); PE 11–2B (MAN)

a. Fabrication: (250 speedboats × 8 dlh) + (250 bass boats × 4 dlh)

CHAPTER 26 Cost Allocation and Activity-Based Costing

PE 26–3A (FIN MAN); PE 11–3A (MAN)

a. Cutting: $22,500 ÷ 2,250 direct labor hours = $10 per dlh

b.

Activity Activity

Activity Cost Cost

Cutting 750 dlh /dlh 1,500 dlh /dlh

$10 $15,000

$10

$ 7,500

Khakis

×= ×=Rate

Activity

Rate

Activity-

Jeans

Activity-

Base

Usage

Activity Base

Usage

CHAPTER 26 Cost Allocation and Activity-Based Costing

PE 26–3B (FIN MAN); PE 11–3B (MAN)

a. Fabrication: $204,000 ÷ 3,000 direct labor hours = $68 per dlh

b.

Activity Activity

Activity Cost Cost

Fabrication 2,000 dlh /dlh 1,000 dlh /dlh

Speed Boat

Activity-

Base

Usage

Activity Base

Usage

Bass Boat

×= ×=Rate

Activity

Rate

Activity-

$68

$136,000

$68 $ 68,000

PE 26–4A (FIN MAN); PE 11–4A (MAN)

PE 26–4B (FIN MAN); PE 11–4B (MAN)

a. Sales order processing activity: 750 orders × $20 per order = $15,000

PE 26–5A (FIN MAN); PE 11–5A (MAN)

PE 26–5B (FIN MAN); PE 11–5B (MAN)

Guest check-in…………………………………………… $ 8.00 (1 check-in × $8.00)

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–1 (FIN MAN); Ex. 11–1 (MAN)

Ex. 26–2 (FIN MAN); Ex. 11–2 (MAN)

*Total direct labor hours:

×=

b.

Direct

Labor

Hours ×=

Trumpets…

…

960 ×= $48,000 ÷ 1,600 units = $30

Single Plant-

wide Rate

per Direct

Labor Hour

$50

Overhead

$ 48,000

Budgeted

Production

Volume

Factory

Budgeted Production Volume)

(Factory Overhead ÷

Factory Overhead per Unit

Direct Labor

Hours

Direct Labor

Hours per Unit

EXERCISES

Single Plantwide Factory Overhead Rate = a. $145,500

2,910 direct labor hours*

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–3 (FIN MAN); Ex. 11–3 (MAN)

** Total processing hours:

×=

Tortilla chips………………

…

×=

b.

Processing

Hours ×=

Tortilla chips…

…

480 ×= $33,600 ÷ 3,000 cases = $11.20

head Rate per

Single Plantwide

Factory Over-

Production

(Cases)

3,000

Budgeted

Single Plantwide Factory Overhead Rate =

0.16

Hours per Case

Volume Processing

480

a. $98,000*

1,400 processing hours**

Hours

Processing

Budgeted Production Volume)

(Factory Overhead ÷

Factory Overhead per Case

$33,600

Processing

Hour

$70

Overhead

Factory

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–4 (FIN MAN); Ex. 11–4 (MAN)

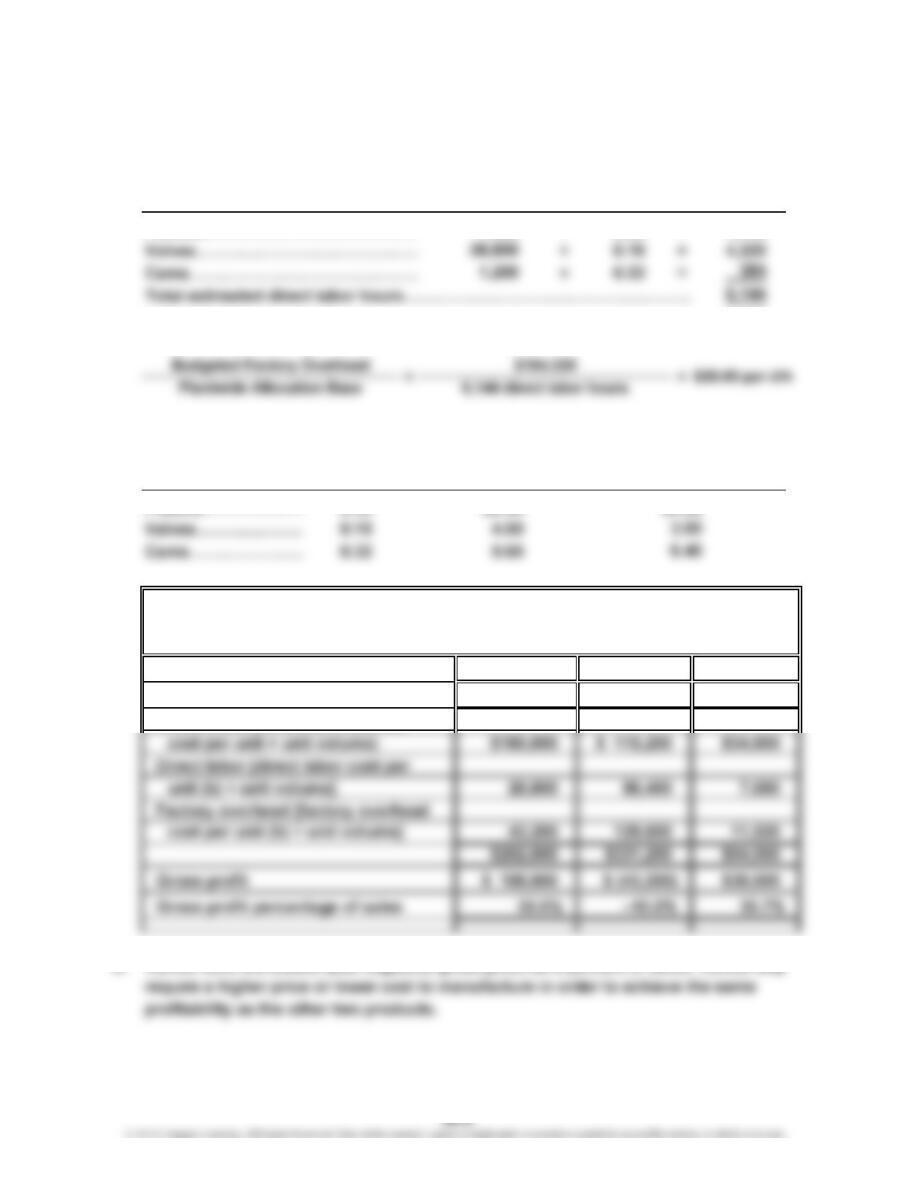

a. First, determine the total estimated labor hours consumed by the three products:

Direct Labor Total

Hours per Labor

×Unit =Hours

Pistons…………………………………

…

× 0.20 = 1,440

Next, determine the plantwide overhead rate:

b. Factory Overhead

Direct Labor Cost per Unit

Hours per ($30.00 × Direct

Unit Labor Hours per Unit

)

Pistons………………

…

0.20 $6.00

c.

Revenues (price × unit volume)

Direct materials (direct materials

d. Valves have the lowest (and negative) gross profit as a percent of sales. Valves may

$84,000

$288,000

Pistons Valves Cams

$360,000

For the Year Ended December 31, 2014

Volume

7,200

ORANGE COUNTY ENGINE PARTS INC.

Product Line Budgeted Gross Profit Reports

Cost per Unit

Labor Hours per Unit)

Direct Labor

$4.00

($20.00 × Direct

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–5 (FIN MAN); Ex. 11–5 (MAN)

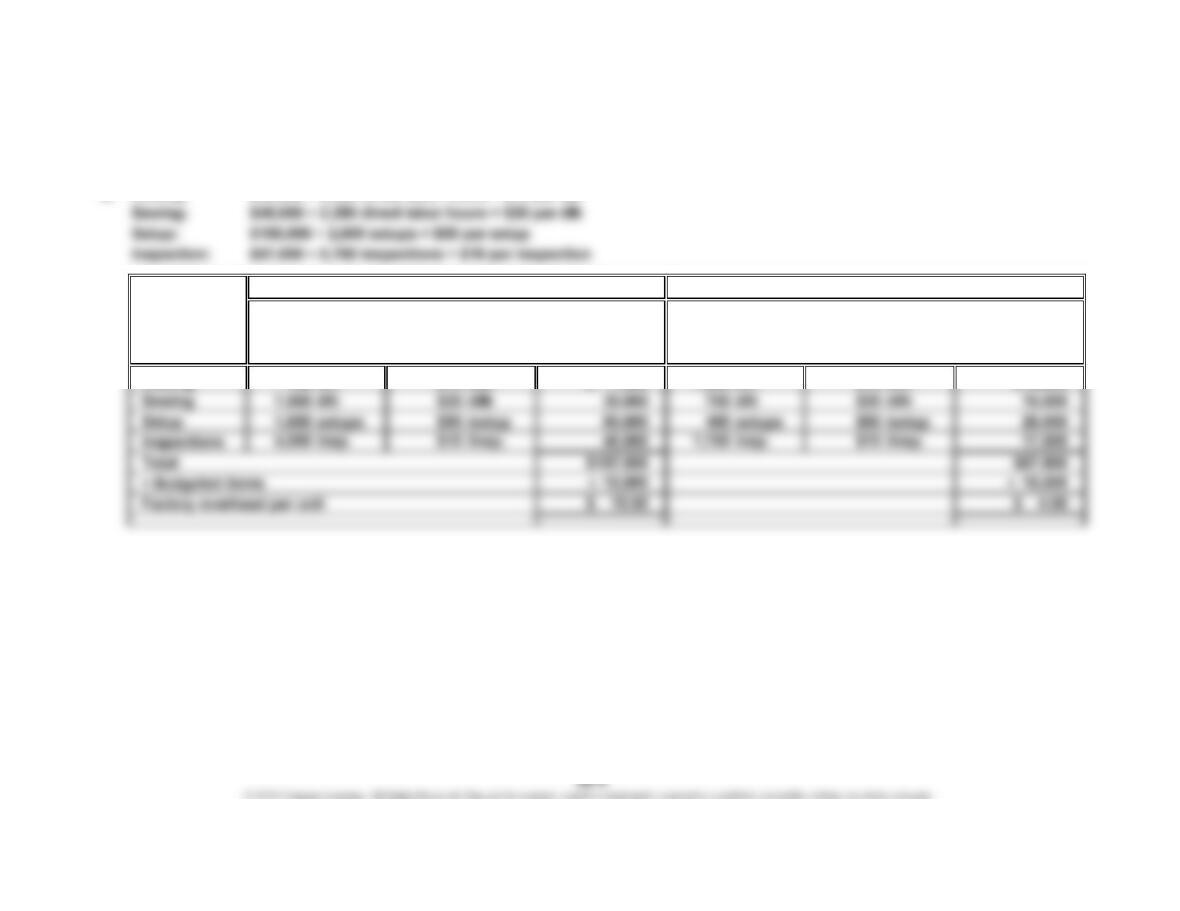

a. Production department factory overhead rates:

Total factory overhead………………………

…

$204,000 $303,600

b. Product cost allocation:

Small Glove

Pattern Department………………………

…

0.08 dir. labor hr. × $85/dlh = $ 6.80

Pattern Cut and Sew

DepartmentDepartment

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–6 (FIN MAN); Ex. 11–6 (MAN)

a. Plantwide overhead rate:

Product costs:

b. Department factory overhead rates:

Production department overhead………………

…

$187,500 $600,000

Product cost allocation:

Desktop

Assembly Department………

…

$75

c. The factory overhead determined under the single plantwide factory overhead

Assembly Testing

Department Department

1.0 dir. mach. hr. × $75/dmh =

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–7 (FIN MAN); Ex. 11–7 (MAN)

a. Plantwide factory overhead rate:

Product costs:

b. Department factory overhead rates:

Total production department

Product cost allocation:

Gasoline engine

Fabrication Department……… $150

c. Management should select the multiple department factory overhead rate method

of allocating overhead costs. The single plantwide factory overhead rate method

Fabrication Assembly

Department Department

8,400 direct labor hours

$882,000 $105 per dlh

Budgeted Factory Overhead

Plantwide Allocation Base =

1.0 dir. labor hr. × $150/dlh =

=

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–8 (FIN MAN); Ex. 11–8 (MAN)

Accounting reports Number of accounting reports

Customer return processing Number of customer returns

Ex. 26–9 (FIN MAN); Ex. 11–9 (MAN)

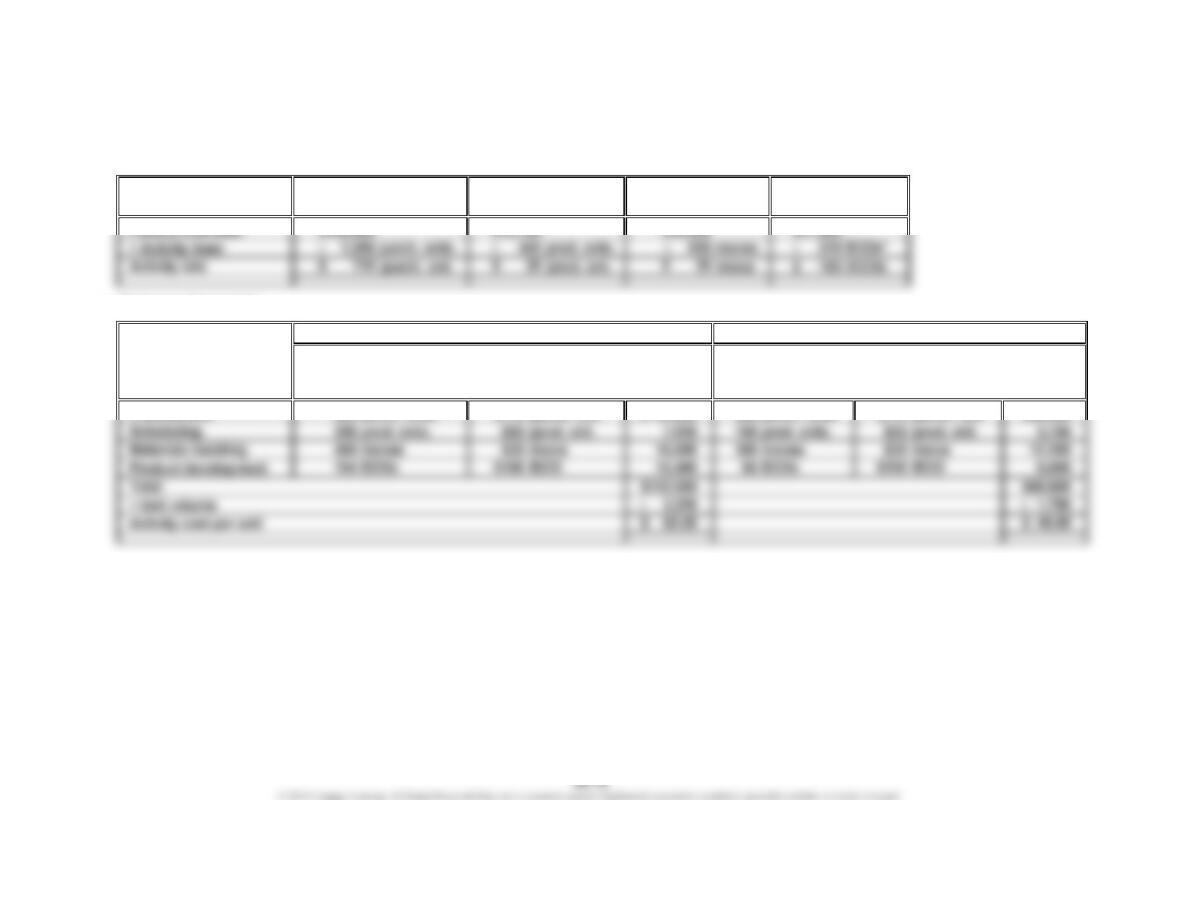

a. Sales order processing activity rate:

Activity Activity Base

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–10 (FIN MAN); Ex. 11–10 (MAN)

Activity Activity

Activity Cost Cost

Fabrication 1,600 mh /mh 1,000 mh /mh

Assembly 420 dlh /dlh 134 dlh /dlh

$32,000

$12

$12 1,608

5,040

$32$32

Usage×Rate

$51,200

Treadmill

=×=

Activity

Stationary Bicycle

Rate

Activity-

Base

Activity-

Base

Usage

Activity

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–11 (FIN MAN); Ex. 11–11 (MAN)

a.

Activity

Casting mh /mh

Assembly dlh /dlh

b.

Activity

Activity Cost

Casting 3,120 mh /mh 1,440 mh /mh

4,560

3,950

Base

Activity

=

$30

$18

Rate

Budgeted

Activity

Cost

Total

Activity

÷

$30 $ 43,200

Base Activity

Usage ×Rate =

Entry Lighting Fixtures Dining Room Lighting Fixtures

Activity- Activity-

$30 $ 93,600

Usage ×Rate =

71,100

$136,800

Cost

ActivityBase Activity

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–12 (FIN MAN); Ex. 11–12 (MAN)

a.

Factory overhead $21,900

*Engineering Change Order

b.

Activity Activity

Activity Cost Cost

Procurement 800 purch. ords. $116 /purch. ord. 500 purch. ords. /purch. ord.

Procurement

Base Activity

Activity-

Base

Activity-

Materials Handling

$29,050

Usage

Refrigerators

Activity

Ovens

Usage ×

Product

=× Rate

DevelopmentScheduling

$116 $58,000$ 92,800

$150,800

$10,750

Rate =

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–13 (FIN MAN); Ex. 11–13 (MAN)

a. Single plantwide rate:

b. Activit

y

-based rates:

3,750 direct labor hours

$375,000

Setup

Production

Support

Plantwide Allocation Base

Indirect Labor =

CHAPTER 26 Cost Allocation and Activity-Based Costing

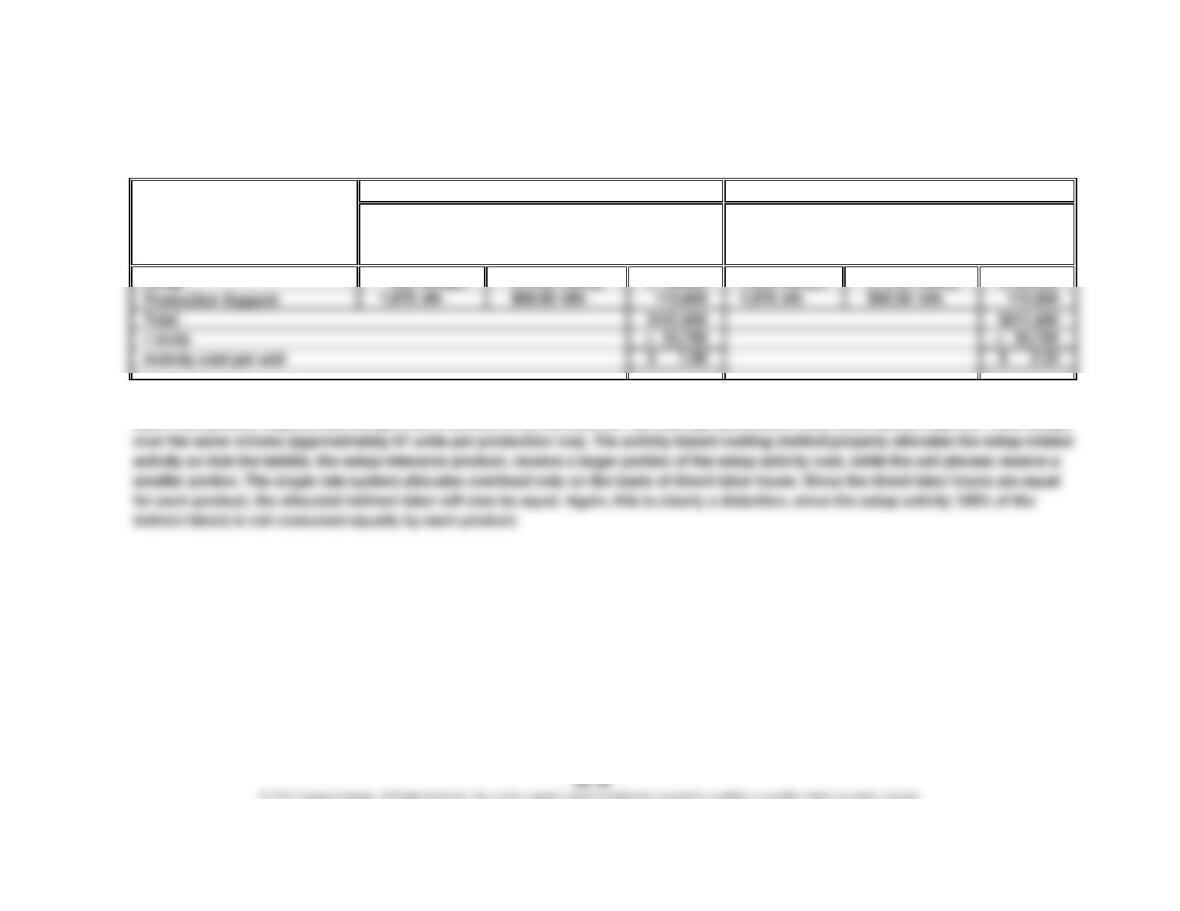

Ex. 26–13 (FIN MAN); Ex. 11–13 (MAN) (Concluded)

c.

Activity Activity

Activity Cost Cost

Setup 600 setups /setup 1,400 setups /setup

d. The per-unit indirect labor costs in (a) are distorted because setup activity is consumed by the products in a different ratio from the direct

labor. Cell phones required 600 setups over a volume of 93,750 units (or 156 units per production run), while tablets required 1,400 setups

$105,000

$75.00

$ 45,000

Base

Usage

$75.00

Activity

RateUsage

Activity

Tablets

×= ×=

Cell Phones

Activity-Activity-

Base

Rate

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–14 (FIN MAN); Ex. 11–14 (MAN)

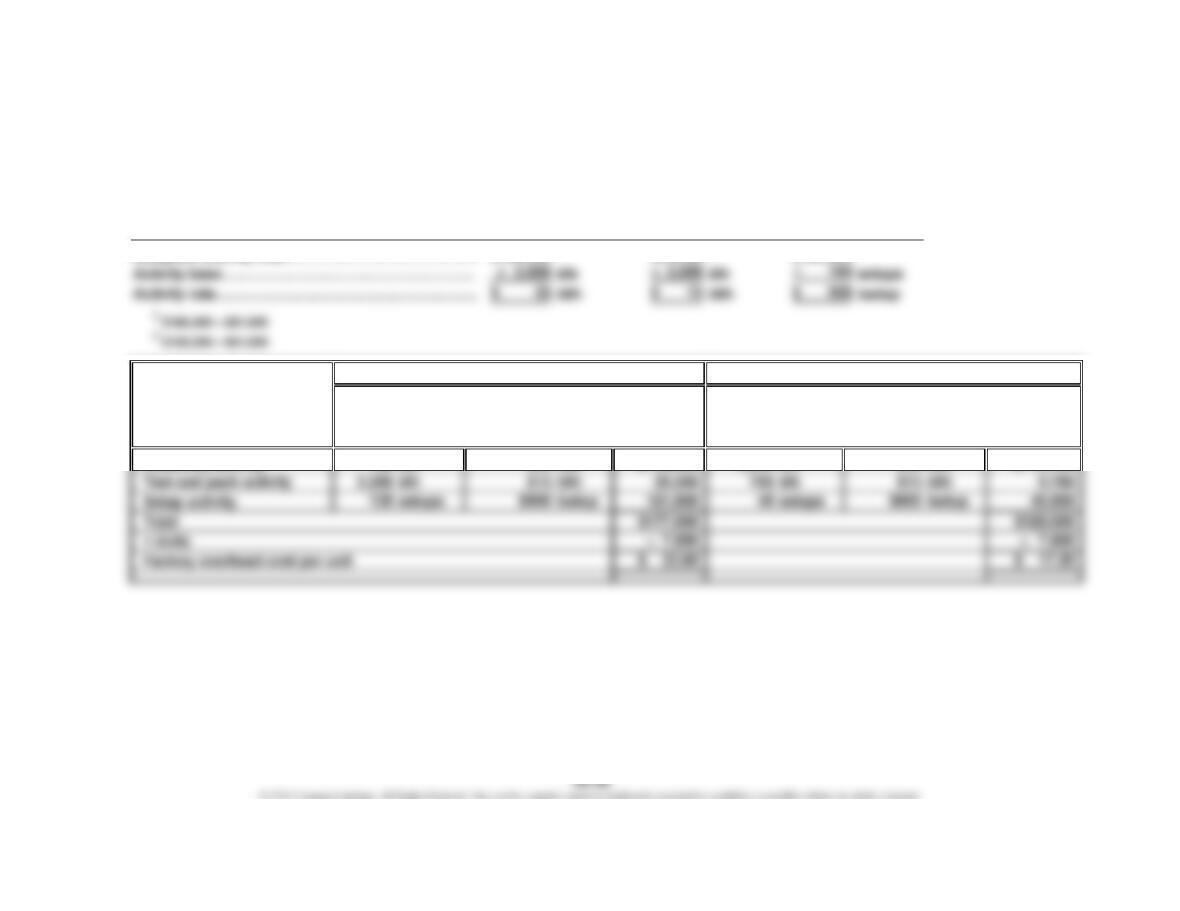

a. Production department factory overhead rates:

Factory overhead………………………………………

…

$120,000

b.

Activity Activity

Activity Cost Cost

Assembly

Department

Blender

Allocation-

Base

Usage

Activity Base

=

=Rate

×

$186,000

Activity

Toaster Oven

×

RateUsage

Test and Pack

Department

Allocation-

CHAPTER 26 Cost Allocation and Activity-Based Costing

Ex. 26–15 (FIN MAN); Ex. 11–15 (MAN)

a. Activity rates:

Budgeted activity cost…………………………………

…

$105,000 $39,000

b.

Activity Activity

Cost Cost

Assembly activity 750 dlh /dlh $ 26,250 dlh /dlh $ 78,750

Activity

Assembly Test and Pack

Activity

$35

2,250

Activity-

$35

Toaster Oven

×= ×=Rate

Activity

Rate

Setup

Activity

Blender

Activity-

Base

Usage

Activity Base

Activity Usage

$162,000

12