CHAPTER 16 Managerial Accounting Concepts and Principles

Prob. 16–5A (FIN MAN); Prob. 1–5A (MAN)

1.

Work in process inventory, January 1, 2016 $ 631,800

Direct materials:

Materials inventory, January 1, 2016 $351,000

Purchases 659,800

Direct labor 670,800

Factory overhead:

Indirect labor $ 78,750

Depreciation expense—factory equipment 56,160

Heat, light, and power—factory 22,460

Property taxes—factory 18,500

Total manufacturing costs incurred during

the year 1,477,570

THE NEWQUEST CORPORATION

Statement of Cost of Goods Manufactured

For the Year Ended December 31, 2016

16-16

CHAPTER 16 Managerial Accounting Concepts and Principles

Prob. 16–5A (FIN MAN); Prob. 1–5A (MAN) (Concluded)

2.

Sales $3,010,000

Cost of goods sold:

Finished goods inventory, January 1, 2016 $ 608,400

Cost of goods manufactured 1,516,570

Gross profit $1,461,030

Operating expenses:

Administrative expenses:

Office salaries expense $185,000

THE NEWQUEST CORPORATION

Income Statement

For the Year Ended December 31, 2016

16-17

CHAPTER 16 Managerial Accounting Concepts and Principles

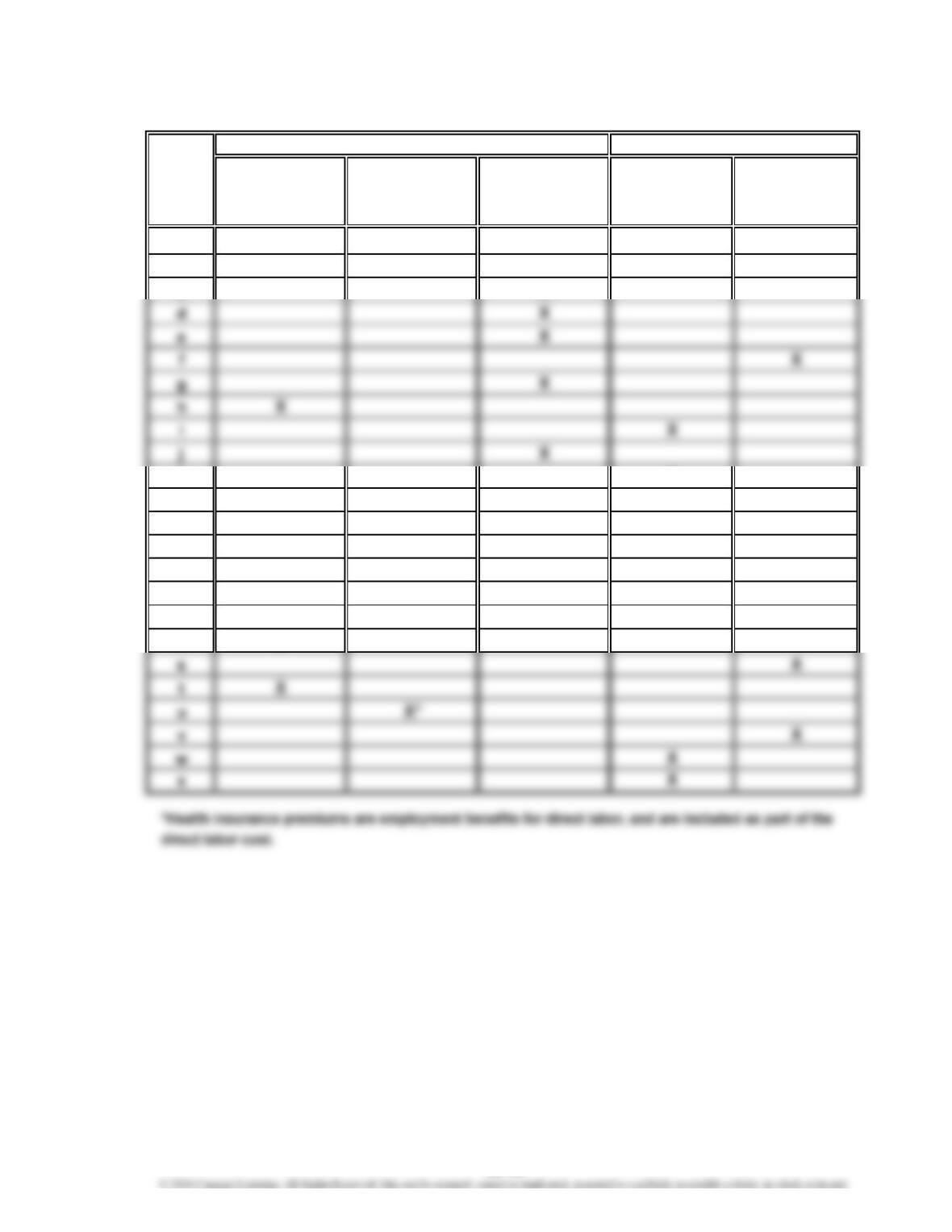

Prob. 16–1B (FIN MAN); Prob. 1–1B (MAN)

Direct Direct Factory

Materials Labor Overhead Selling Administrative

Cost Cost Cost Cost Expense Expense

aX

bX

gX

hX*

iX

jX

kX

lX

mX

nX

oX

wX

xX

yX

zX

*Item h might also be classified as direct material cost if the cost is significant because it

can be directly traced to the end product.

Product Costs Period Costs

16-18

CHAPTER 16 Managerial Accounting Concepts and Principles

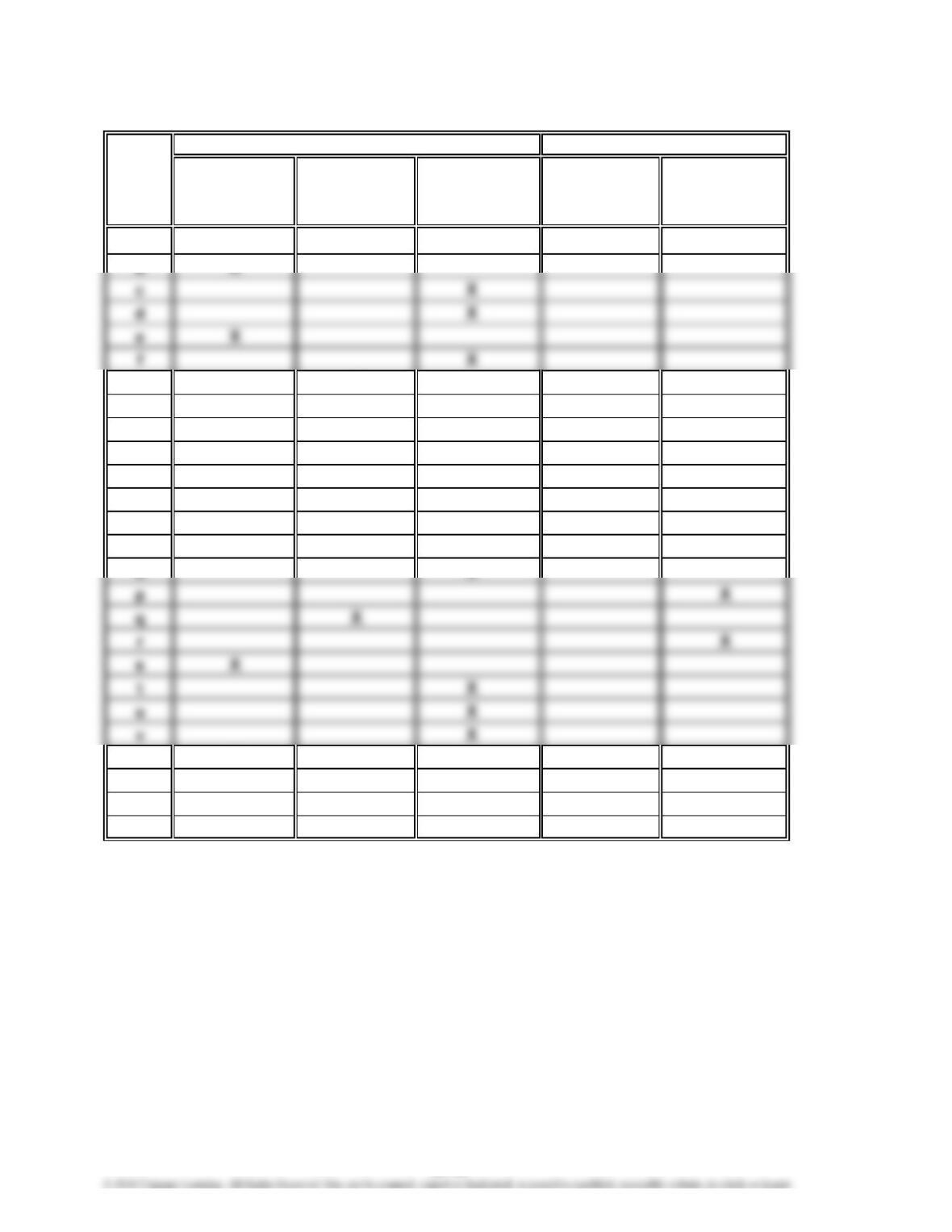

Prob. 16–2B (FIN MAN); Prob. 1–2B (MAN)

Direct Direct Factory

Materials Labor Overhead Selling Administrative

Cost Cost Cost Cost Expense Expense

aX

bX

cX

kX

lX

mX

nX

oX

pX

qX

rX

Product Costs Period Costs

16-19

CHAPTER 16 Managerial Accounting Concepts and Principles

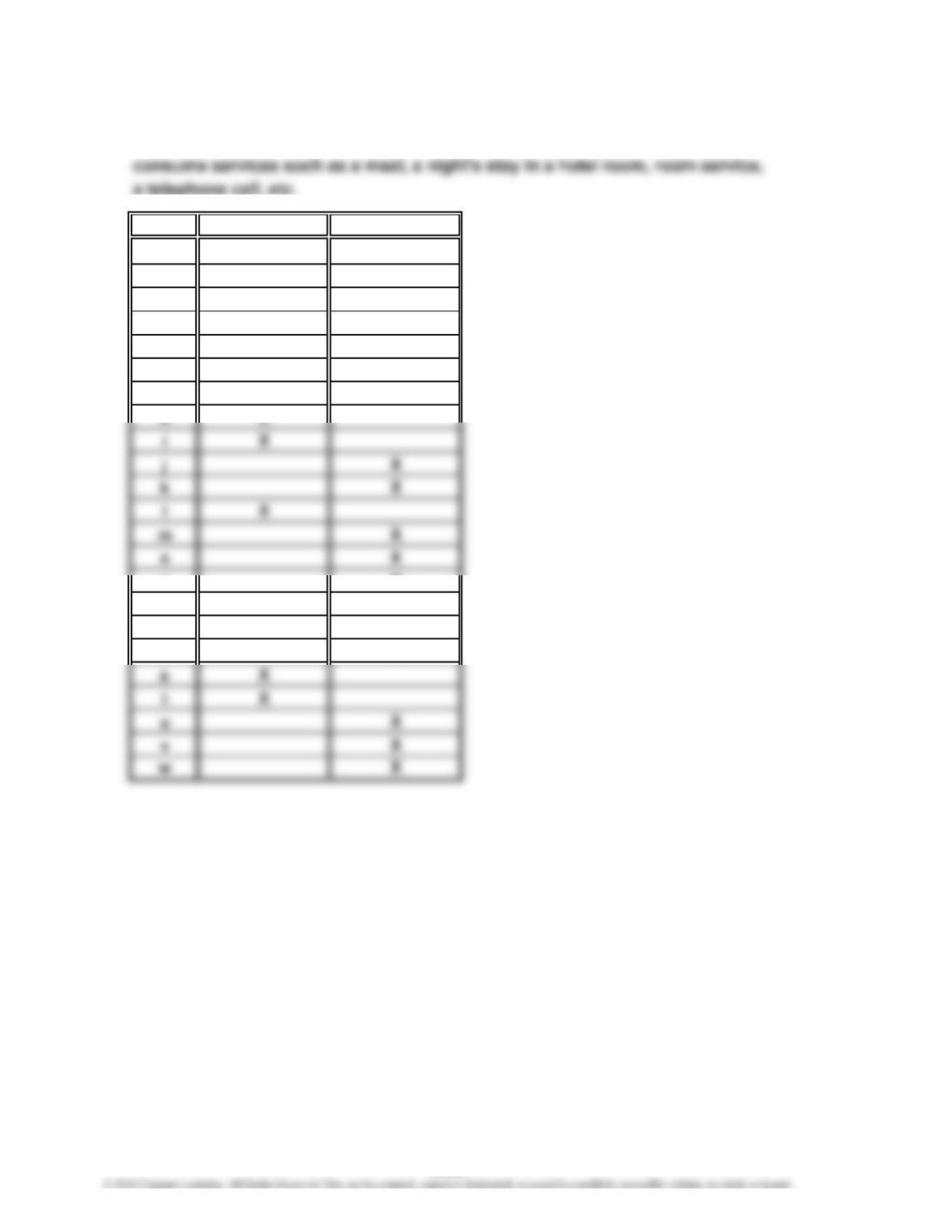

Prob. 16–3B (FIN MAN); Prob. 1–3B (MAN)

1. The most logical definition for the final cost object would be a hotel guest. Guests

2. Cost Direct Indirect

aX

bX

cX

dX

eX

fX

gX

oX

pX

qX

rX

16-20

CHAPTER 16 Managerial Accounting Concepts and Principles

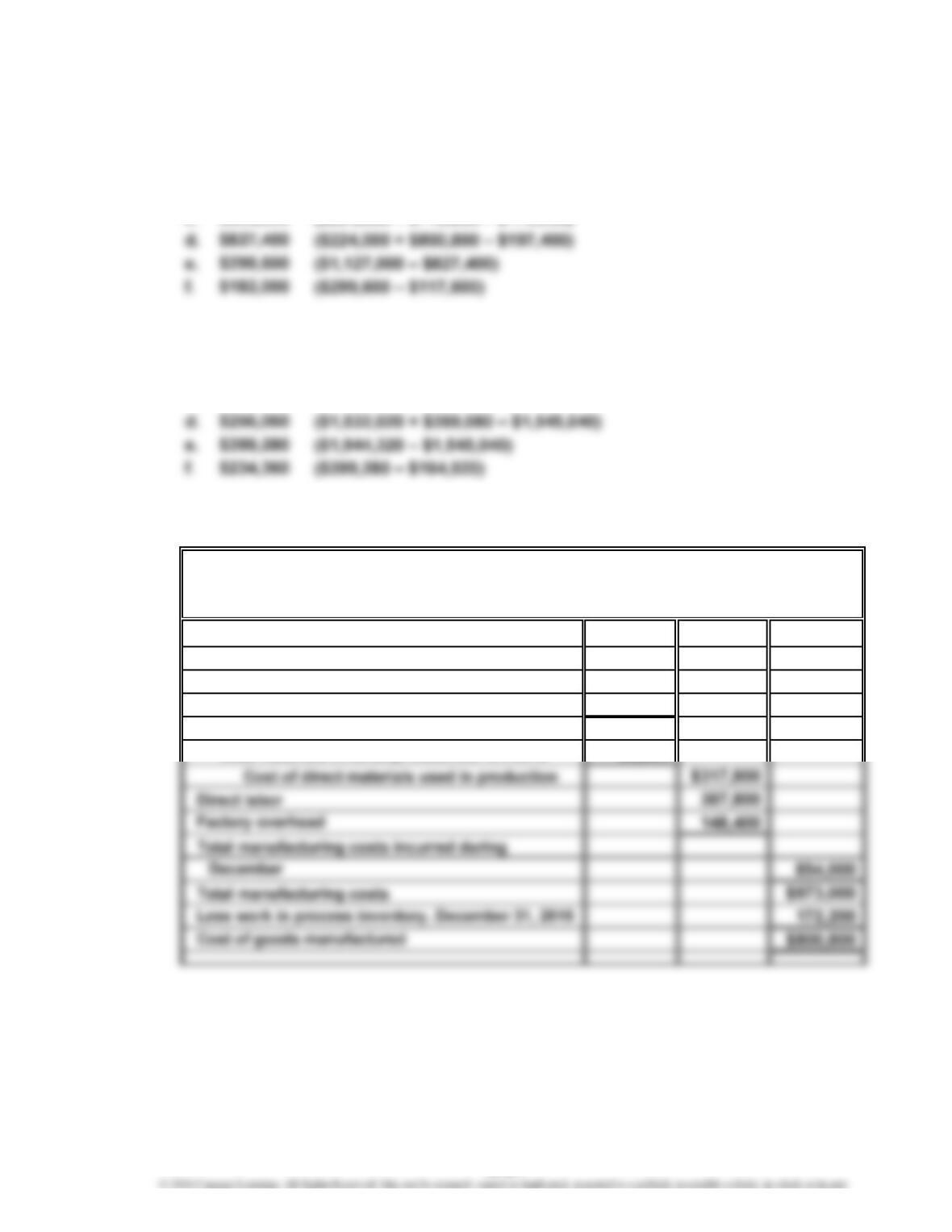

Prob. 16–4B (FIN MAN); Prob. 1–4B (MAN)

1. On Company

a. $30,800 ($282,800 + $65,800 – $317,800)

b. $854,000 ($317,800 + $387,800 + $148,400)

c. $800,800 ($854,000 + $119,000 – $172,200)

Off Company

a. $581,560 ($685,720* + $91,140 – $195,300)

b. $685,720 ($1,519,000 – $256,060 – $577,220)

c. $195,300 ($1,727,320 – $1,532,020)

*Note: The student must calculate part (b) prior to calculating part (a) because

the solution to part (b) is needed as an input to part (a).

2.

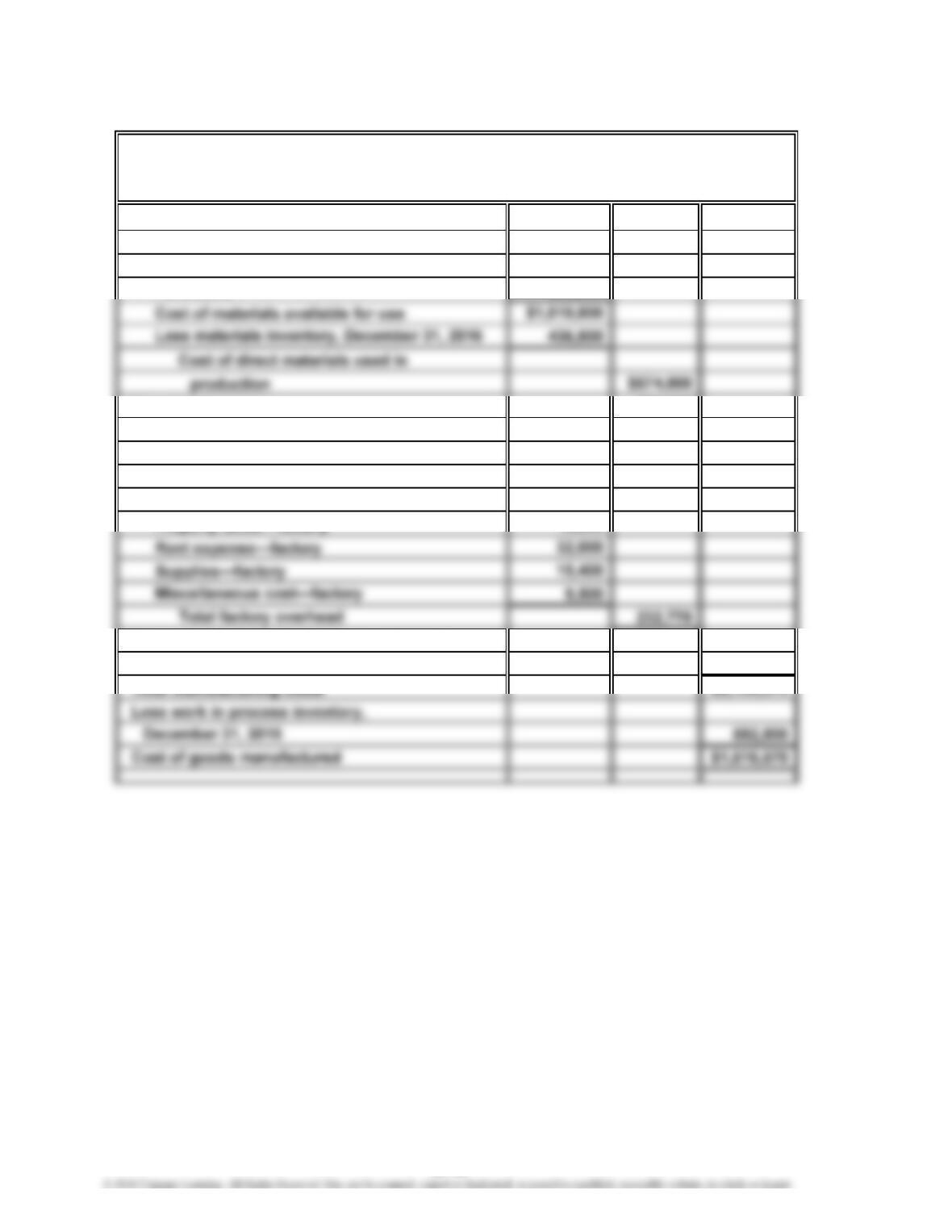

Work in process inventory, December 1, 2016 $119,000

Direct materials:

Materials inventory, December 1, 2016 $ 65,800

Purchases 282,800

Cost of materials available for use $348,600

Less materials inventory, December 31, 2016 30,800

ON COMPANY

Statement of Cost of Goods Manufactured

For the Month Ended December 31, 2016

16-21

CHAPTER 16 Managerial Accounting Concepts and Principles

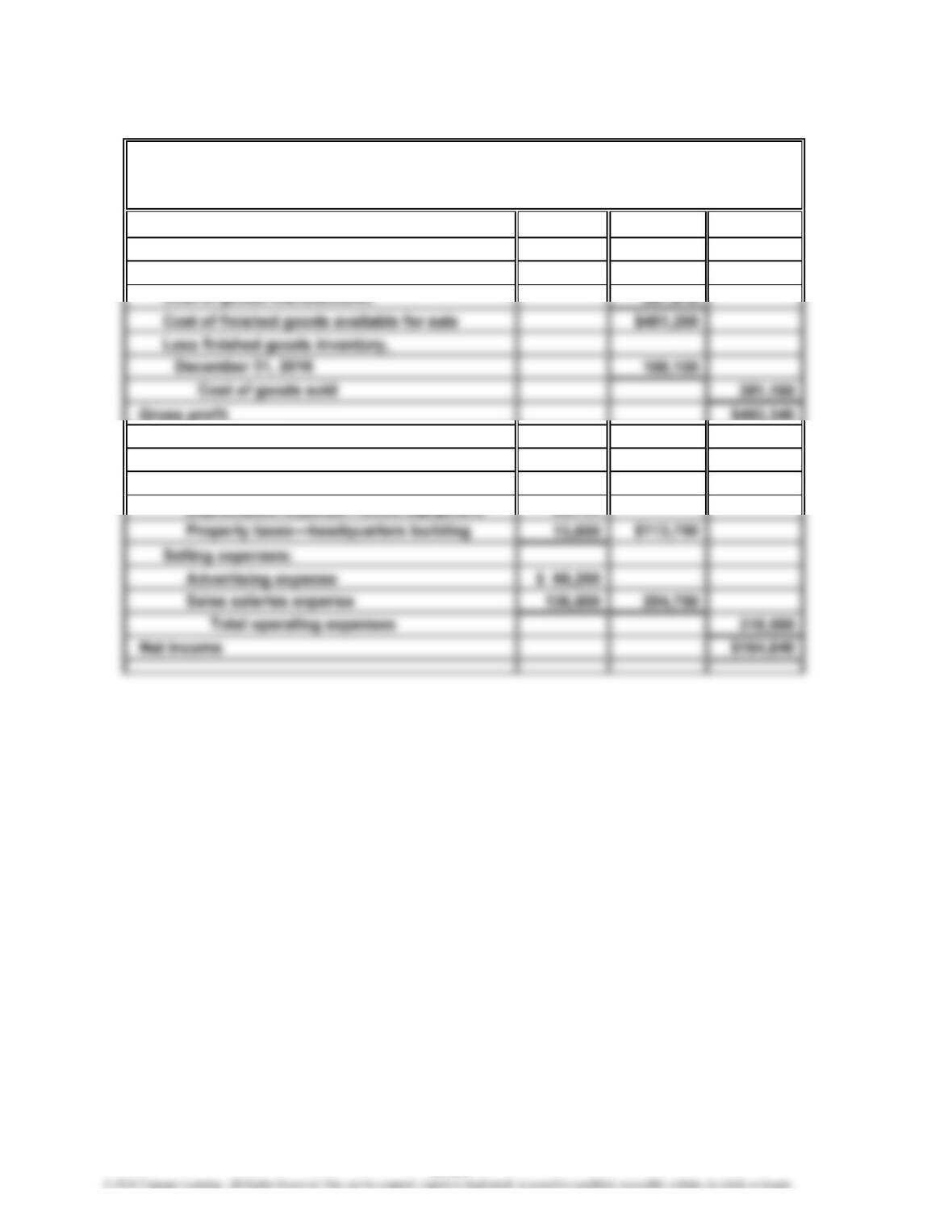

Prob. 16–4B (FIN MAN); Prob. 1–4B (MAN) (Concluded)

3.

Sales $1,127,000

Cost of goods sold:

Finished goods inventory, December 1, 2016 $ 224,000

Cost of goods manufactured 800,800

ON COMPANY

Income Statement

For the Month Ended December 31, 2016

16-22

CHAPTER 16 Managerial Accounting Concepts and Principles

Prob. 16–5B (FIN MAN); Prob. 1–5B (MAN)

1.

Work in process inventory, January 1, 2016 $109,200

Direct materials:

Materials inventory, January 1, 2016 $ 77,350

Purchases 123,500

Cost of materials available for use $200,850

Heat, light, and power—factory 5,850

Property taxes—factory 4,095

Rent expense—factory 6,825

Supplies—factory 3,250

Miscellaneous cost—factory 4,420

SHANIKA COMPANY

Statement of Cost of Goods Manufactured

For the Year Ended December 31, 2016

16-23

CHAPTER 16 Managerial Accounting Concepts and Principles

Prob. 16–5B (FIN MAN); Prob. 1–5B (MAN) (Concluded)

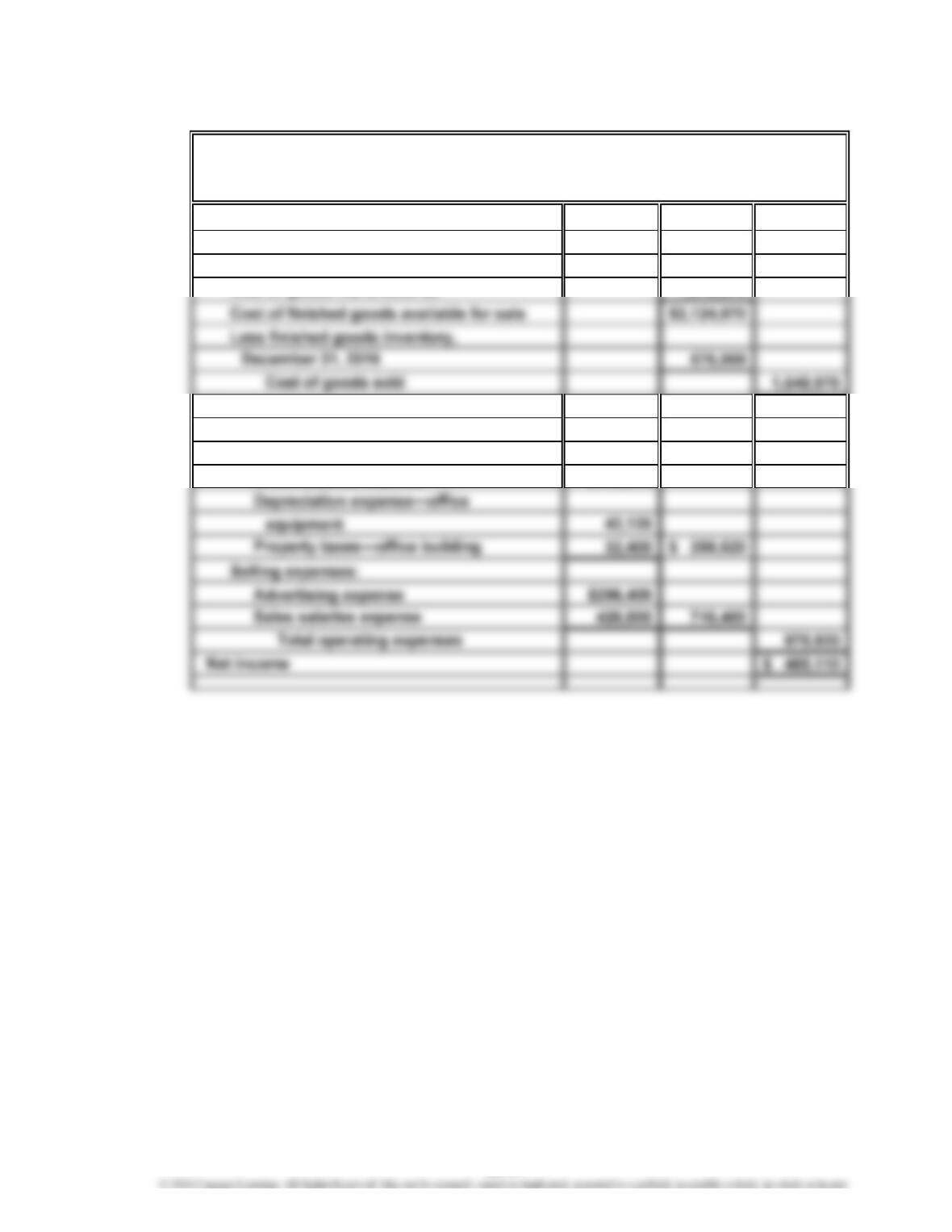

2.

Sales $864,500

Cost of goods sold:

Finished goods inventory, January 1, 2016 $113,750

Operating expenses:

Administrative expenses:

Office salaries expense $ 77,350

Depreciation expense—office equipment 22,750

SHANIKA COMPANY

Income Statement

For the Year Ended December 31, 2016

16-24

CHAPTER 16 Managerial Accounting Concepts and Principles

CP 16–1 (FIN MAN); CP 1–1 (MAN)

Although Fred may appear to have technically complied with company policy, his

CP 16–2 (FIN MAN); CP 1–2 (MAN)

The objectives of managerial accounting and financial accounting are different;

therefore, the vice president’s statement is very incomplete. In one sense, the

statement may be true at only very high levels in the organization. For example,

the division manager may be evaluated on the basis of financial accounting profit.

CASES & PROJECTS

CHAPTER 16 Managerial Accounting Concepts and Principles

CP 16–3 (FIN MAN); CP 1–3 (MAN)

1. The vice president of the Information Systems Division can use managerial

accounting information in a number of different ways. For example, the vice

president might use these data to determine resources that will be required

2. The hospital administrator can use managerial accounting information in a

number of different ways. One way is for cost planning and control. The

administrator could use managerial information to keep costs commensurate

with services provided and to plan for staffing and nursing levels. This

information can be used to determine the cost of various services and, thereby,

3. The CEO of the food company will use managerial accounting information

to support the control of the three divisions. Each of the three divisions will

4. The copy shop manager needs fairly simple managerial accounting information.

At the most basic level, the copy shop manager needs to know the costs of

performing various copy tasks, such as one-sided copy, two-sided copy,

CHAPTER 16 Managerial Accounting Concepts and Principles

CP 16–4 (FIN MAN); CP 1–4 (MAN)

1. Obie’s bill has a number of points that should be considered. Some of the

points, with the appropriate argument, are identified below.

a. The trip back to the shop resulted in an $80 labor charge. Obie should

argue that the whole hour should not be billed. The hour is the result of

b. The overtime premium should not have been charged to Obie. What if

Obie was the first appointment in the morning? If so, then there would be

no overtime premium. It’s only random misfortune that Obie was the last

client of the day and therefore received the overtime premium. Add to

Thus, the labor portion of the bill should only be $70 + $60 + $60 = $190.

There are other parts of the bill that should not be in dispute.

●The materials storage and handling charge is a normal charge of

maintaining a parts inventory for the benefit of clients that need parts.

●The fringe benefits and overhead added to the hourly rate are both

CHAPTER 16 Managerial Accounting Concepts and Principles

CP 16–4 (FIN MAN); CP 1–4 (MAN) (Concluded)

Direct Direct

2. Cost Materials Labor Overhead

Circuit board………………………………

…

X

Storage and handling……………………

…

X

Straight-time labor…………………………

…

X

CP 16–5 (FIN MAN); CP 1–5 (MAN)

1. The High Times manager will use managerial accounting information

2. The plant manager is going to use cost information on scrap and rework to

identify the amount of waste occurring in the plant. This measure of waste is

3. The cost of ending inventory must be determined as financial statements

are prepared. The division controller will likely require inventory valuation

4. The Maintenance Department manager needs to be able to plan the resources

to be used by his department. The planning process involves identifying the

required resources to fulfill the department’s objective. For example, the

16-28

CHAPTER 16 Managerial Accounting Concepts and Principles

CP 16–6 (FIN MAN); CP 1–6 (MAN)

Note to Instructors: Consider having the teams compete for the most examples.

Have half the class do the pizza restaurant and the other the copy shop, and

compare results.

Some examples that may be offered by the students are the following:

Copy and Graphics Shop

Direct Direct Selling

Cost Materials Labor Overhead Expenses

Paper………………………………………

…

X

Graphic designer wages………………… X

Manager salary……………………………

…

X

Lease cost of copy machine……………

…

X

Coupon costs……………………………

…

X

…

CHAPTER 16 Managerial Accounting Concepts and Principles

CP 16–6 (FIN MAN); CP 1–6 (MAN) (Concluded)

Pizza Restaurant

Direct Direct Selling

Cost Materials Labor Overhead Expenses

Ingredients……………………………………

…

X

Cook wages…………………………………

…

X

Manager salary………………………………

…

X

Depreciation on equipment

and fixtures…………………………………

…

X

Coupon costs………………………………… X

Advertising……………………………………

…

X

16-30

…

…

…