CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–2A (FIN MAN); Prob. 4–2A (MAN)

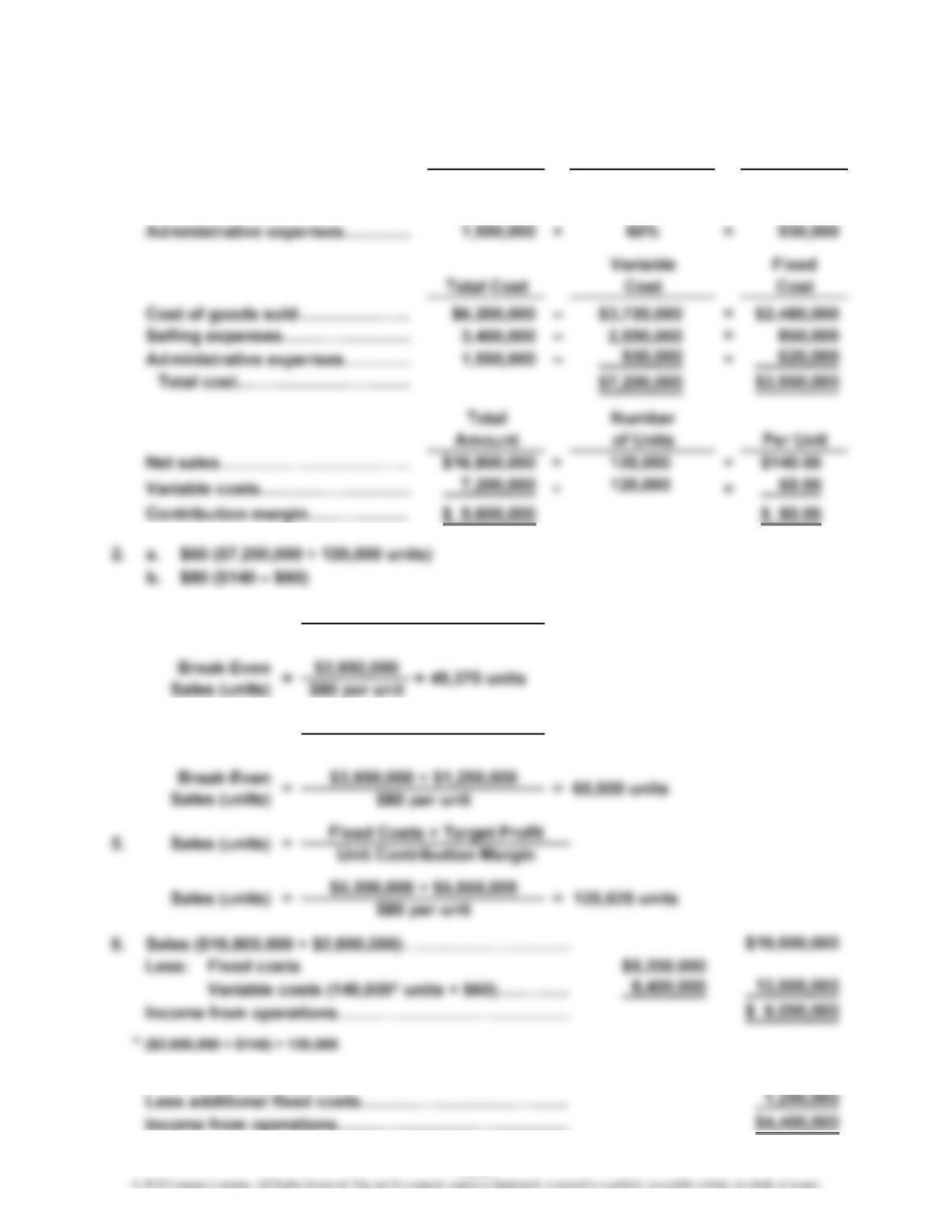

1. Variable Variable

Total Cost Cost Percentage Cost

Cost of goods sold………………

…

$6,200,000 × 60% = $3,720,000

Selling expenses…………………

…

3,400,000 ×75% = 2,550,000

7. Present operating income…………………………………

…

$5,650,000

4. Break-Even

Sales (units) =Fixed Costs

Unit Contribution Margin

3. Fixed Costs

Unit Contribution Margin

Break-Even

Sales (units) =

19-21

…

…

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–2A (FIN MAN); Prob. 4–2A (MAN) (Concluded)

8. In favor of the proposal is the possibility of increasing income from operations

from $5,650,000 to $6,000,000. However, there are many points against the

proposal, including:

19-22

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–3A (FIN MAN); Prob. 4–3A (MAN)

3.

4. Sales (16,000 × $100)…………………………

…

$1,600,000

Total fixed costs………………………………

…

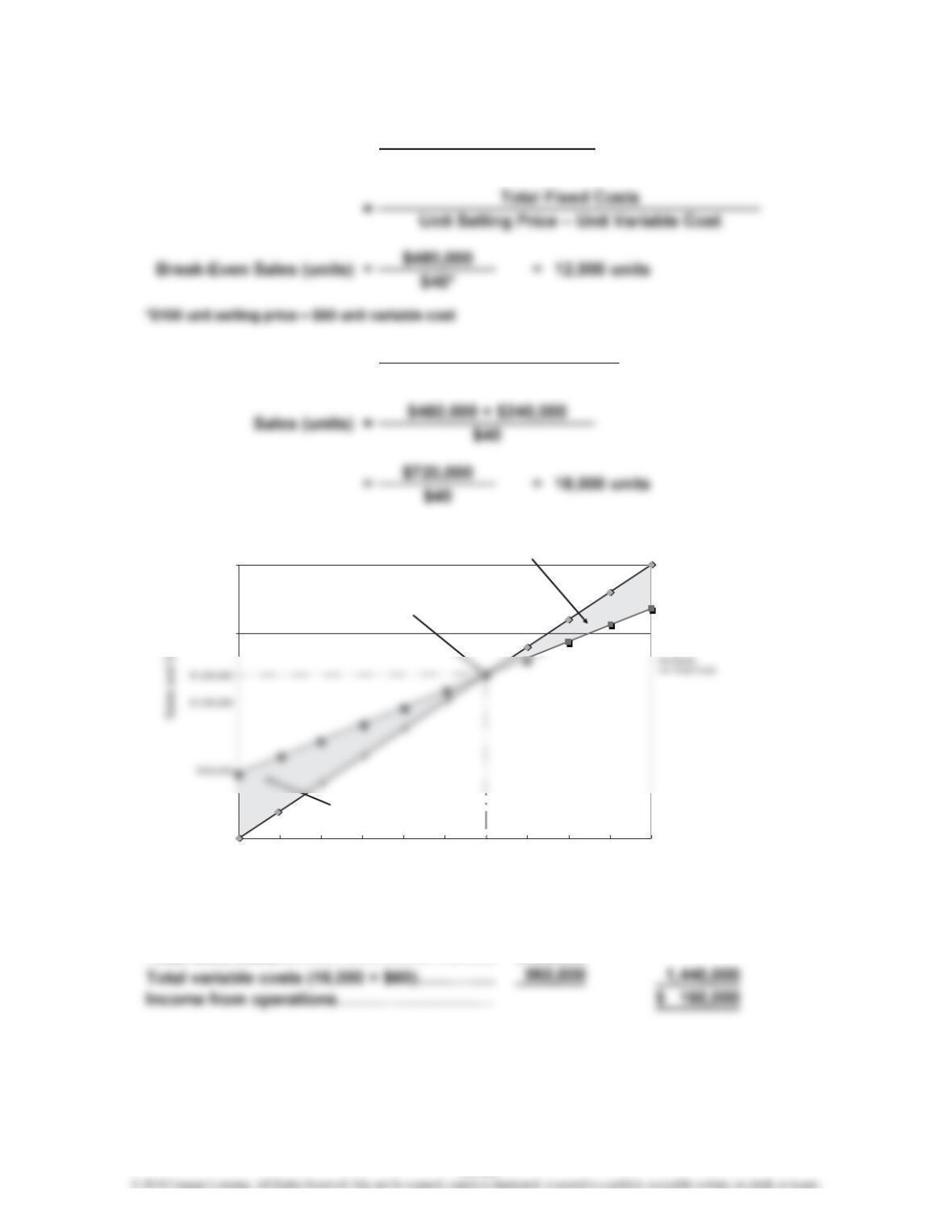

1. Break-Even Sales (units) = Total Fixed Costs

Unit Contribution Margin

2. Sales (units) = Fixed Costs + Target Profit

Unit Contribution Margin

$480,000

$0

$1,500,000

$2,000,000

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000 20,000

Units of Sales

Operating Loss

Area

Operating Profit Area

Break-Even Point

19-23

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–4A (FIN MAN); Prob. 4–4A (MAN)

1.

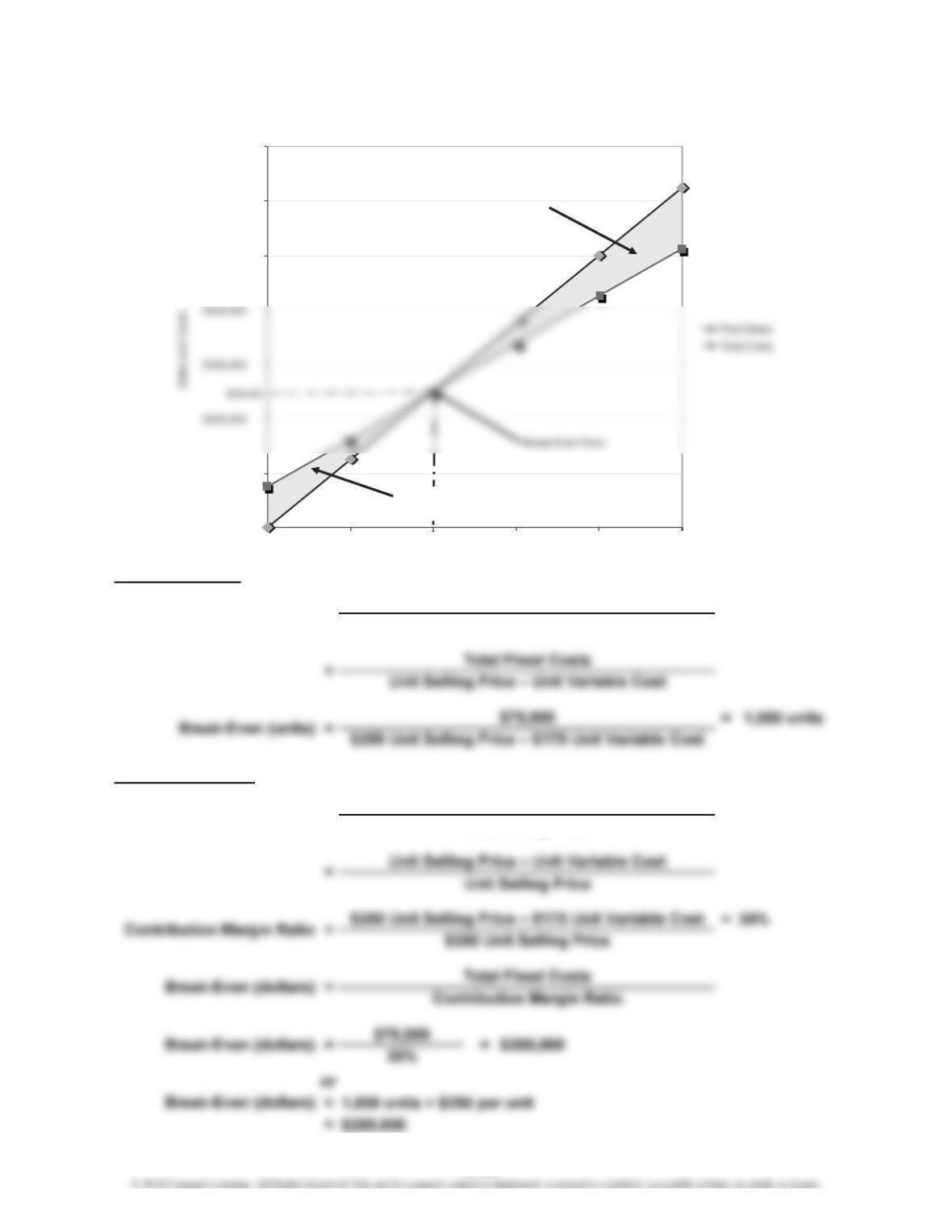

Contribution Margin Ratio

Unit Selling Price

Total Fixed Costs

Unit Contribution Margin

=Unit Contribution Margin

=

Break-Even Units:

Break-Even Dollars:

Break-Even Sales (units)

$0

$100,000

$500,000

$600,000

$700,000

0 500 1,000 1,500 2,000 2,500

Units of Sales

Operating

Profit Area

Operating

Loss Area

$75,000

19-24

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–4A (FIN MAN); Prob. 4–4A (MAN) (Continued)

2.

$0

$100,000

$300,000

$600,000

0 500 1,000 1,500 2,000 2,500

Units of Sales

Tot a l Sale s

Total Costs

Operating

Profit Area

Operating Loss

Area

$625,000

$75,000

19-25

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–4A (FIN MAN); Prob. 4–4A (MAN) (Continued)

3.

Break-Even Units:

Break-Even Dollars:

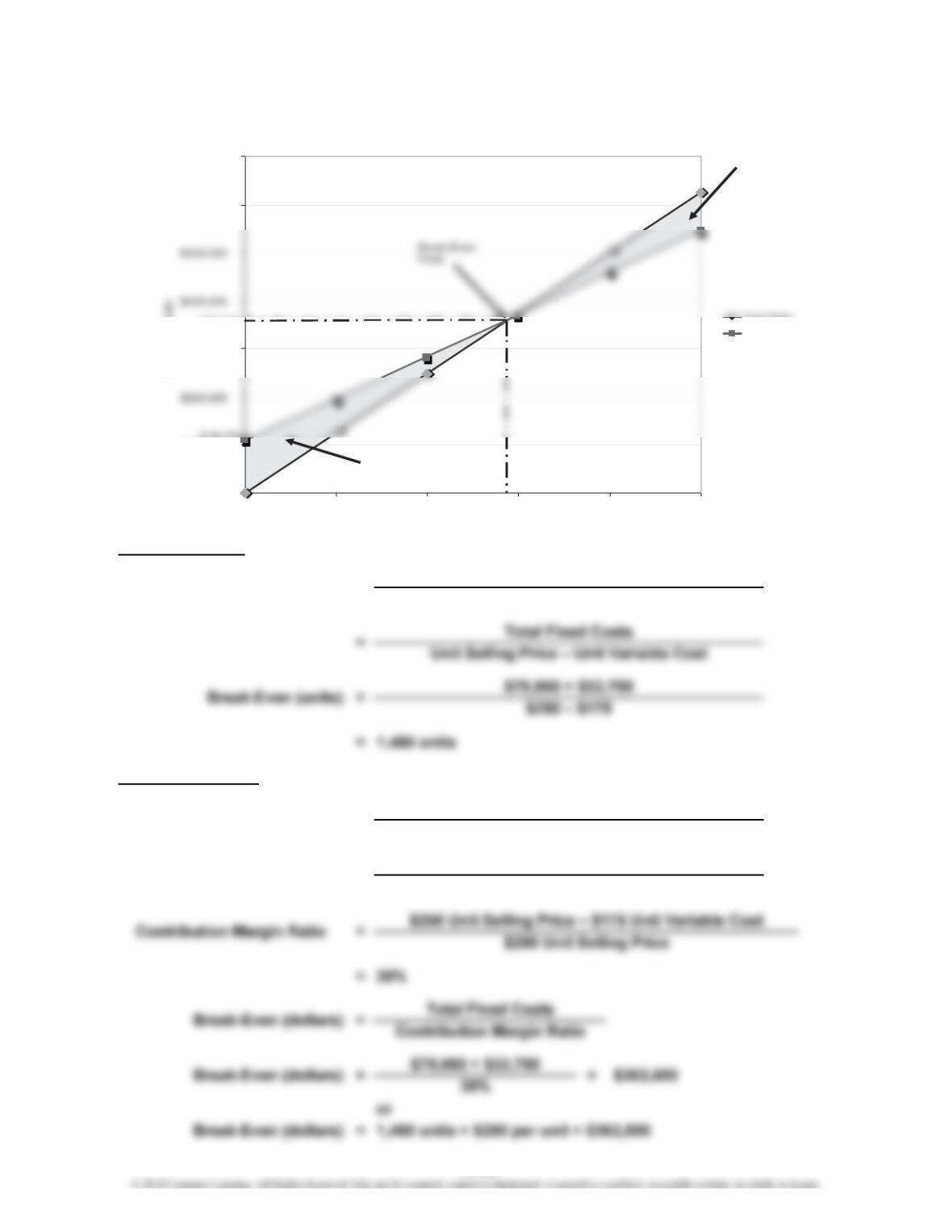

Unit Contribution Margin

Break-Even Sales (units) = Total Fixed Costs

=

=

Contribution Margin Ratio Unit Contribution Margin

Unit Selling Price

Unit Selling Price – Unit Variable Cost

Unit Selling Price

$0

$100,000

$300,000

$600,000

$700,000

0 500 1,000 1,500 2,000 2,500

Sales and Costs

Units of Sales

Total Sales

Total Costs

Operating

Profit Area

Operating Loss

Area

$362,500

1,450

$108,750

19-26

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–4A (FIN MAN); Prob. 4–4A (MAN) (Concluded)

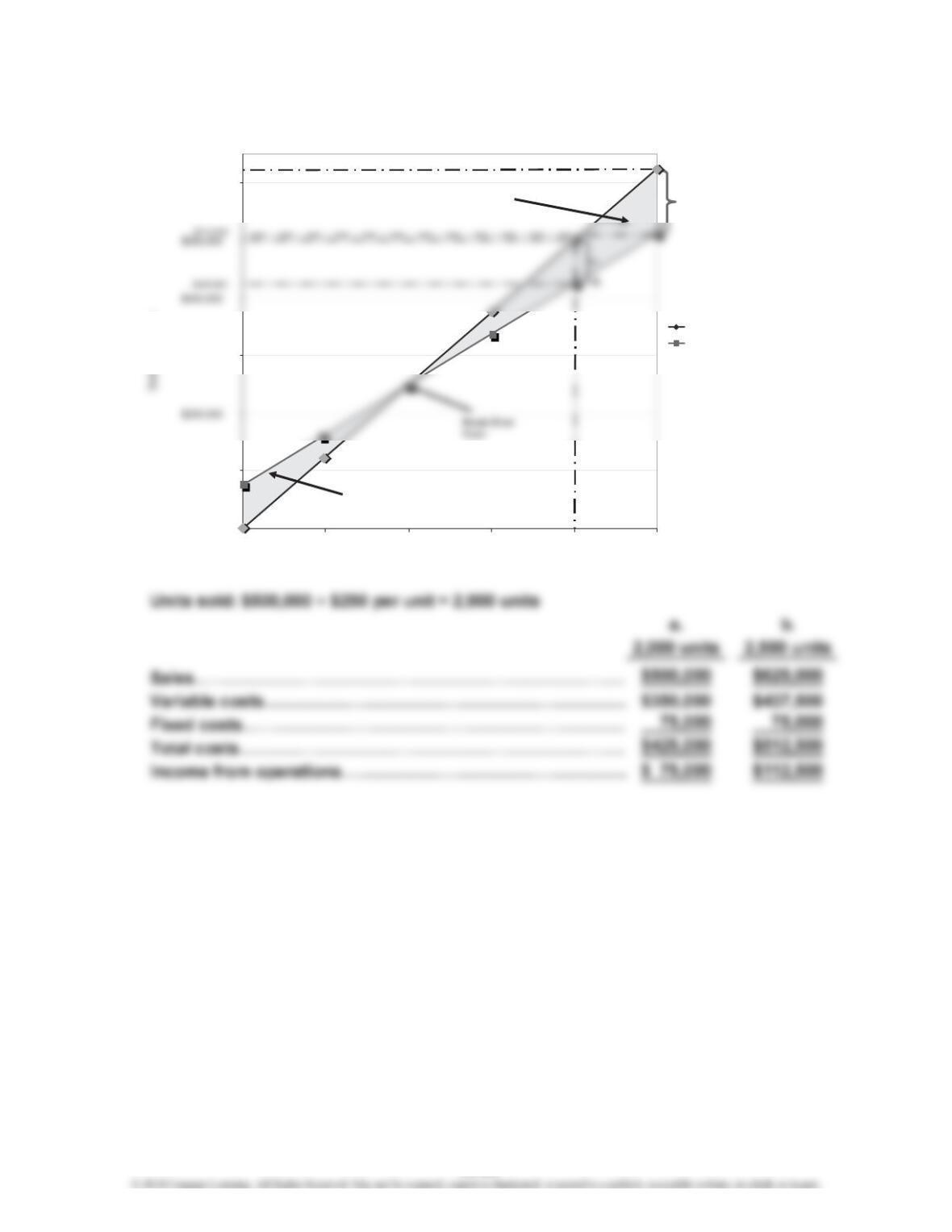

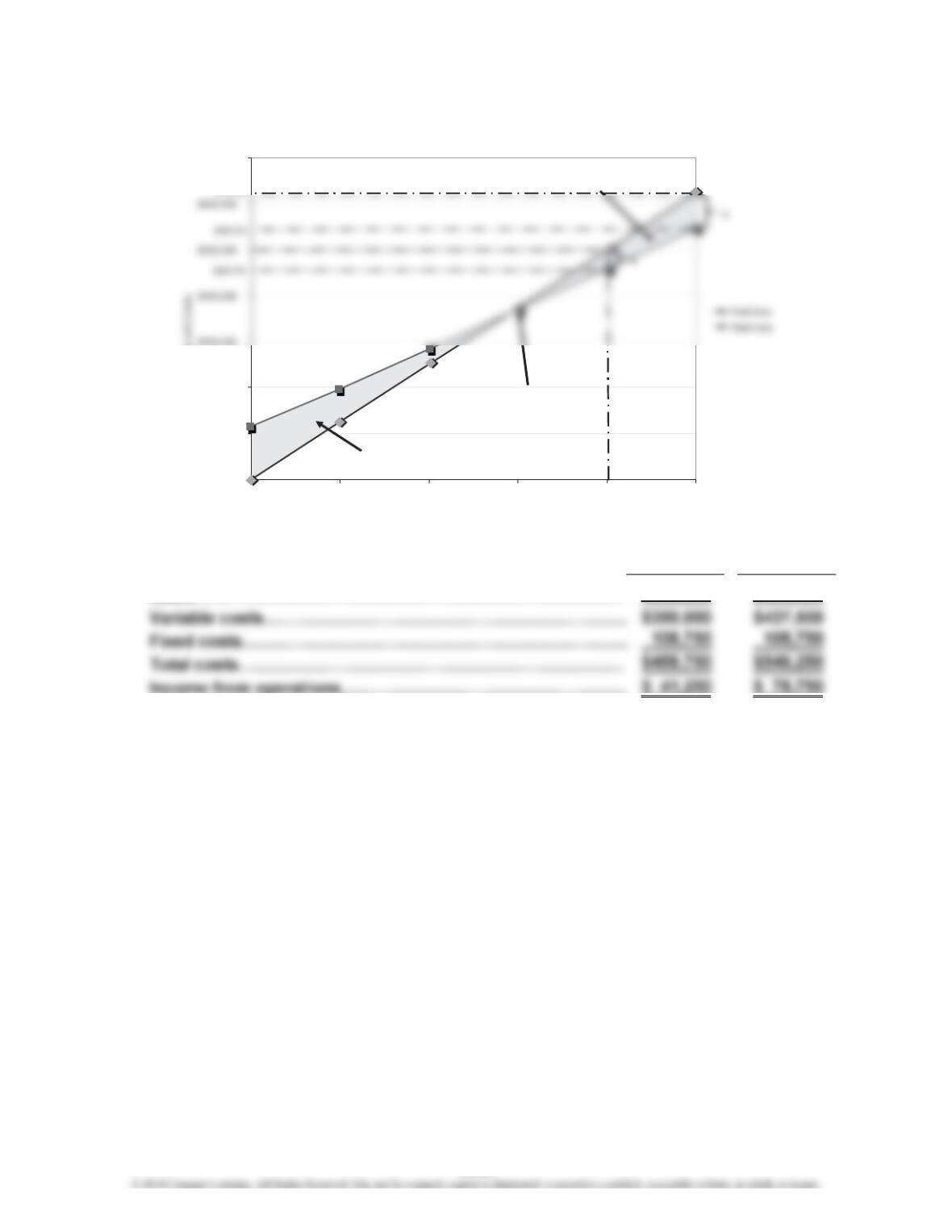

4.

a. b.

2,000 units 2,500 units

Sales…………………………………………………………………

…

$500,000 $625,000

Income from operations…………………………………………… $ 41,250 $ 78,750

$0

$100,000

$200,000

$700,000

0 500 1,000 1,500 2,000 2,500

Sales and Costs

Units of Sales

Operating

Profit Area

Break-Even

Point

Operating

Loss Area

$625,000

$108,750

19-27

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–5A (FIN MAN); Prob. 4–5A (MAN)

(Overall product is labeled E.)

1. Unit Selling Price of E [($1,600 × 40%) + ($850 × 60%)]……………………………

…

$1,150

3. Unit selling price of E [($1,600 × 50%) + ($850 × 50%)]……………………………

…

$1,225

19-28

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–6A (FIN MAN); Prob. 4–6A (MAN)

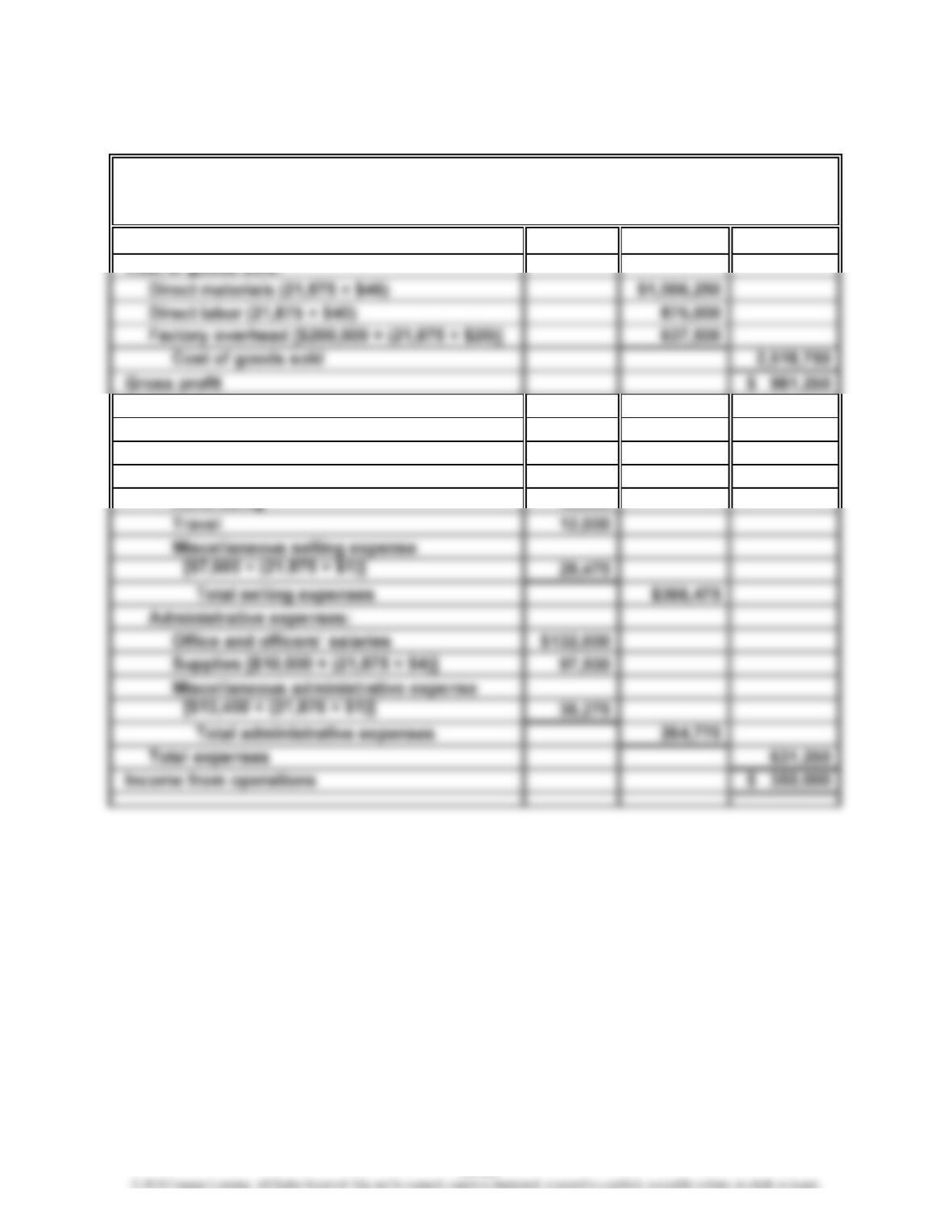

1.

Sales (21,875 × $160) $3,500,000

Cost of goods sold:

Expenses:

Selling expenses:

Sales salaries and commissions

[$110,000 + (21,875 × $8)] $285,000

Advertising 40,000

WOLSEY INDUSTRIES INC.

Estimated Income Statement

For the Year Ended December 31, 2014

19-29

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–6A (FIN MAN); Prob. 4–6A (MAN) (Continued)

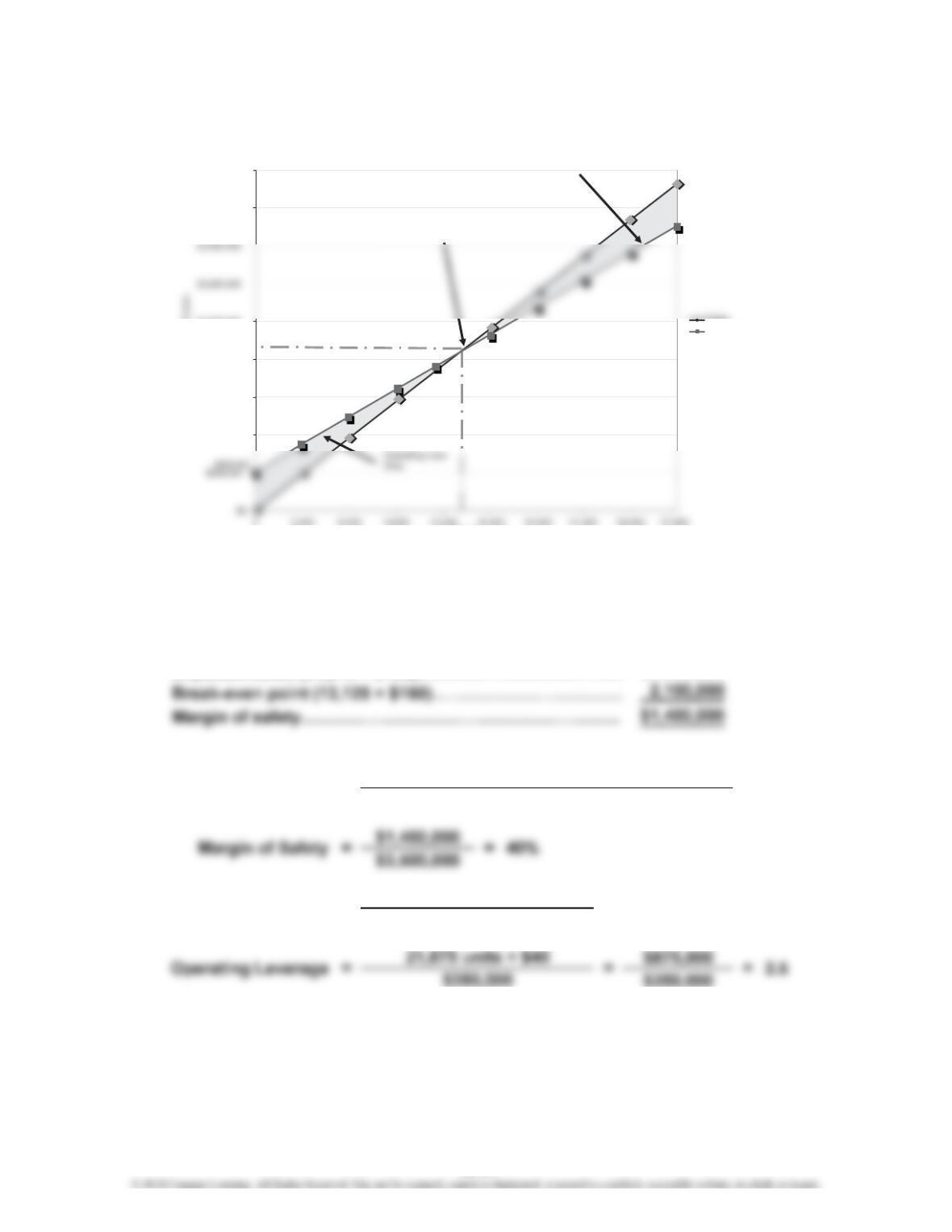

2. Contribution Margin Ratio = Sales – Variable Costs

Sales

3. Break-Even Sales (units) = Fixed Costs

Unit Contribution Margin

19-30

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–6A (FIN MAN); Prob. 4–6A (MAN) (Concluded)

4.

5. Margin of safety:

In dollars:

Expected sales (21,875 × $160)………………………………

…

$3,500,000

As a percentage of sales:

Contribution Margin

=Margin of Safety Sales – Sales at Break-Even Point

Sales

Income from Operations

6. Operating Leverage =

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$4,000,000

$4,500,000

0 3,000 6,000 9,000 12,000 15,000 18,000 21,000 24,000 27,000

Sales and Costs

Units

Sales

Total Costs

Operating Profit

Area

Break-Even Point

$2,100,000

13,125

19-31

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

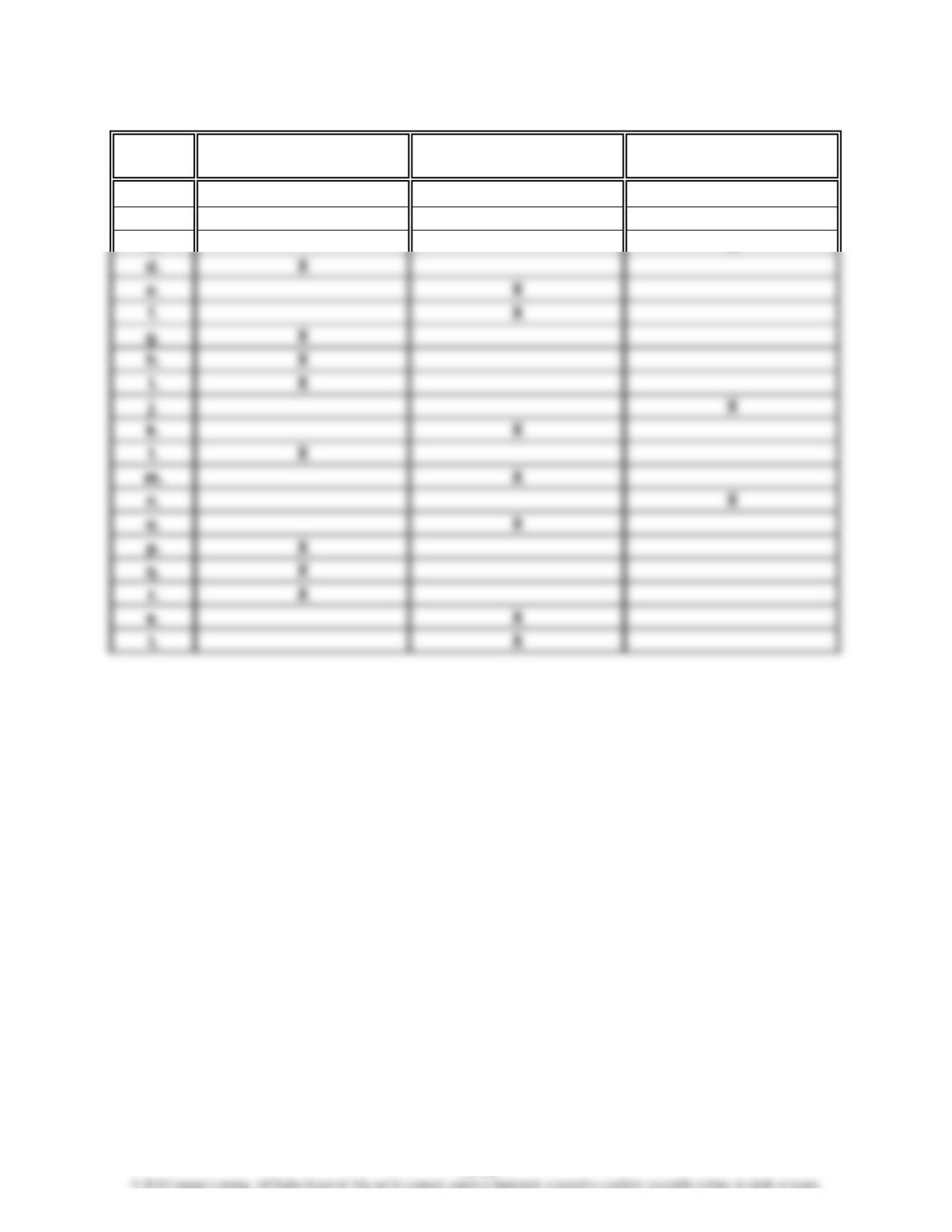

Prob. 19–1B (FIN MAN); Prob. 4–1B (MAN)

Fixed Variable Mixed

Cost Cost Cost Cost

a. X

b. X

c. X

19-32

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

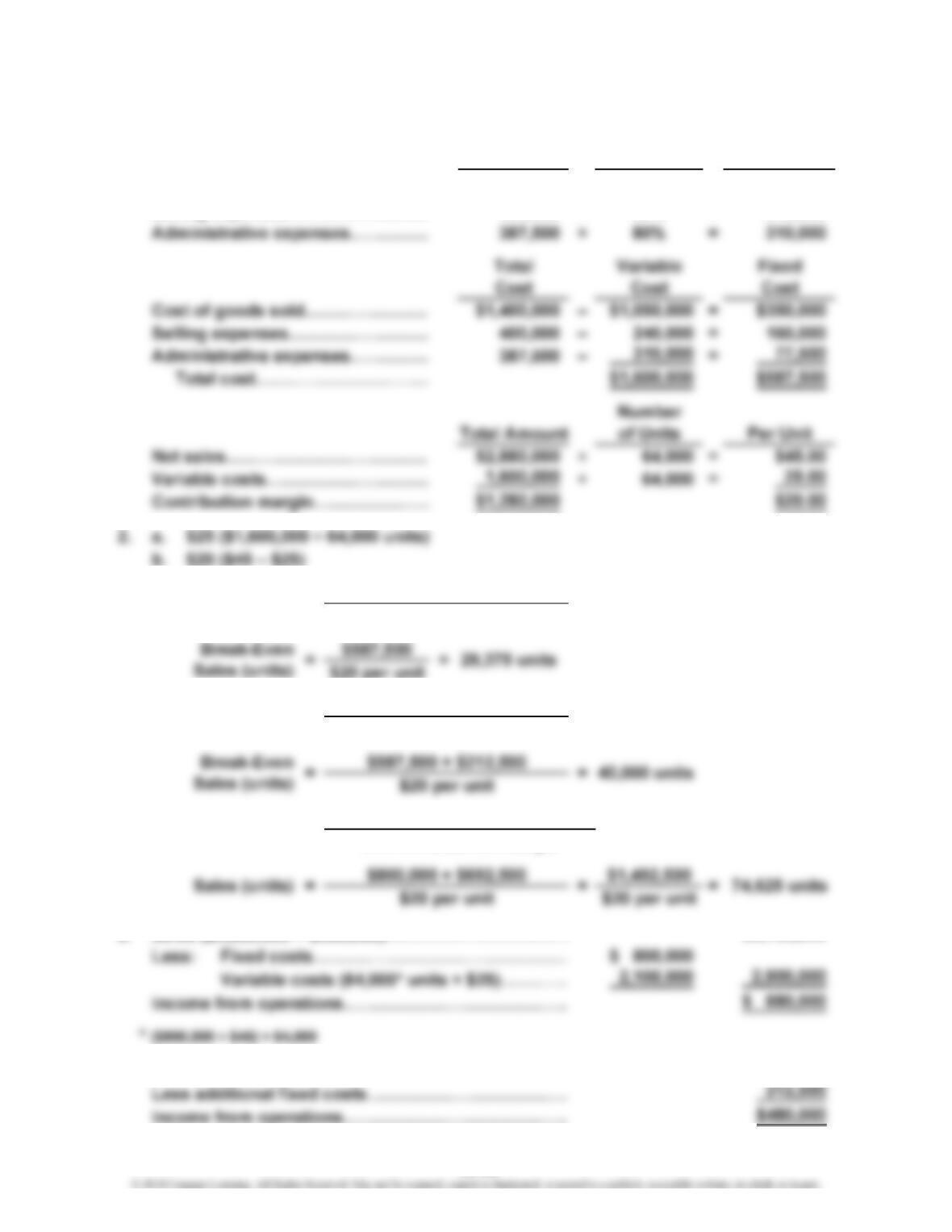

Prob. 19–2B (FIN MAN); Prob. 4–2B (MAN)

1. Total Variable Cost Variable

Cost Percentage Cost

Cost of goods sold…………………

…

$1,400,000 × 75% = $1,050,000

Selling expenses……………………

…

400,000 × 60% = 240,000

6. Sales ($2,880,000 + $900,000)…………………………

…

7. Present operating income………………………………

…

…

$692,500

5.

Break-Even

Sales (units)

Unit Contribution Margin

4. Break-Even

Sales (units) =

3. Fixed Costs

Unit Contribution Margin

$3,780,000

Fixed Costs + Target Profit

Sales (units)

=

=

Fixed Costs

Unit Contribution Margin

19-33

…

…

CHAPTER 19 Cost Behavior and Cost-Volume-Profit Analysis

Prob. 19–2B (FIN MAN); Prob. 4–2B (MAN) (Concluded)

8. In favor of the proposal is the possibility of increasing income from operations

from $692,500 to $880,000. However, there are many points against the

proposal, including:

19-34