CHAPTER 26 Cost Allocation and Activity-Based Costing

Prob. 26–6A (FIN MAN); Prob. 11–6A (MAN) (Concluded)

3. Procedure A Procedure B Procedure C

Reimbursement (patient days ×

reimbursement rate)* $ 682,080 $1,319,500 $1,948,800

4. Procedure A requires more activity cost than is being reimbursed by the insurance

company. As a result, the hospital may wish to determine if the costs of providing

Procedure A are too high. Hospital management may wish to investigate the

CHAPTER 26 Cost Allocation and Activity-Based Costing

Prob. 26–1B (FIN MAN); Prob. 11–1B (MAN)

1. a. Direct labor overhead rate:

b. Machine hour overhead rate:

2.

a. Direct labor hours:

Blending Department…………

…

260 dlh 245 dlh 215 dlh

Packing Department……………

…

470 300 130

Total direct labor hours………

…

730 dlh 545 dlh 345 dlh

Skim Milk Cream

Whole Milk

…

…

CHAPTER 26 Cost Allocation and Activity-Based Costing

Prob. 26–2B (FIN MAN); Prob. 11–2B (MAN)

1.

Production department factory

overhead totals…………………………………………………

…

$178,200 $121,500

2. Whole milk

Blending Department…………………

…

=$ 71,500

Skim milk

Blending Department…………………

…

=$78,100

…

650 dir. mach. hrs. × $110/dmh

Dept. Dept.

Blending Packing

710 dir. mach. hrs. × $110/dmh

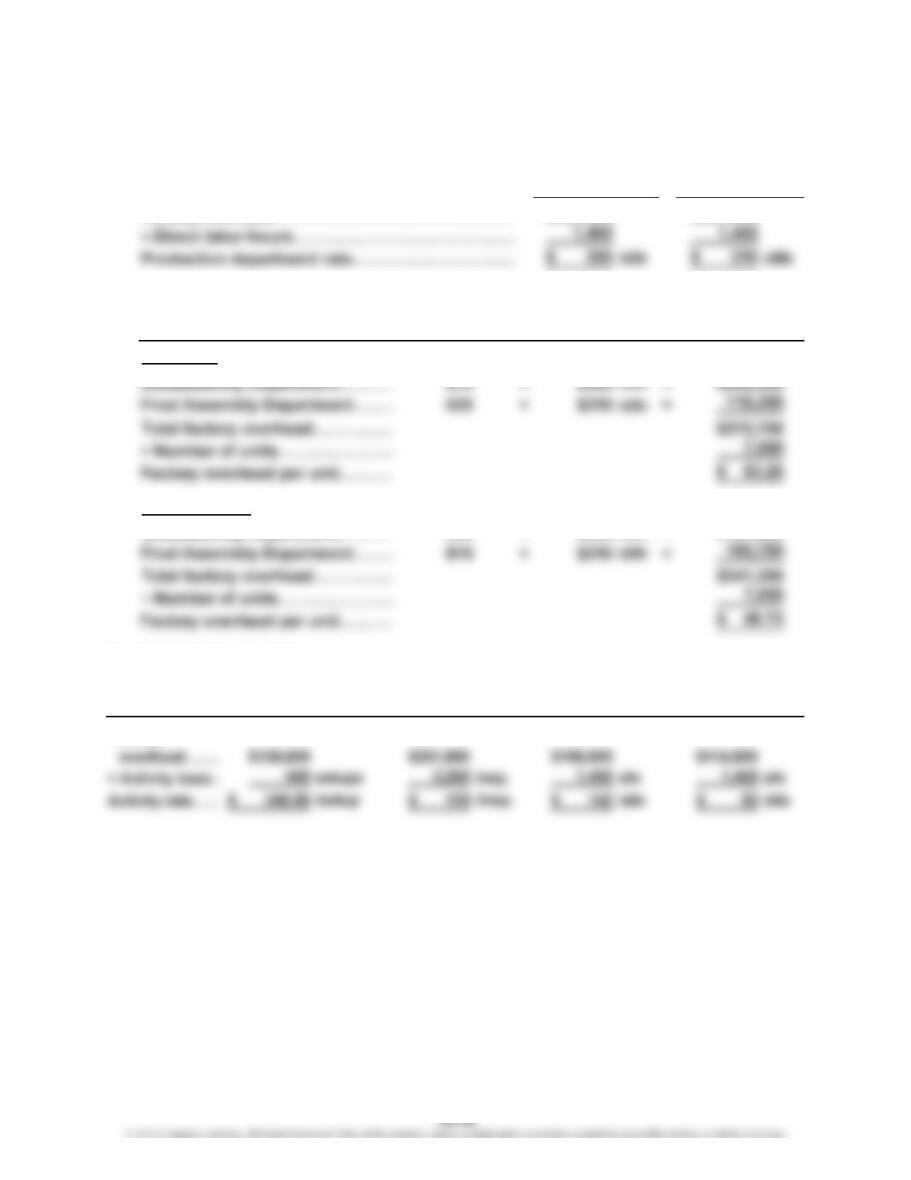

CHAPTER 26 Cost Allocation and Activity-Based Costing

Prob. 26–3B (FIN MAN); Prob. 11–3B (MAN)

1. Production department rates:

Factory overhead……………………………………

…

2.

× =

Receivers:

…

…

Loudspeakers:

Subassembly Department………

…

× $300 /dlh =

…

3. Activity-based rates:

Factory

$294,000

Production

Overhead

Factory

Rate

Department

Subassembly Final Assembly

Department

$420,000

Final Assembly

Department

Department

Department

$157,500

Subassembly

Direct

Labor Hours

525

Setup

Quality

Control

CHAPTER 26 Cost Allocation and Activity-Based Costing

Prob. 26–3B (FIN MAN); Prob. 11–3B (MAN) (Concluded)

4.

Activity Activity

Activity Cost Cost

Setup 80 setups /setup 320 setups /setup

Quality control 450 insp. /insp. 1,750 insp. /insp.

5. The activity-based overhead allocation reveals that loudspeakers are more costly on a per-unit basis than are the receivers. The multiple

production department rate method determines that the per-unit factory overhead is nearly the same for the two products. The multiple

Usage

$119

$346.50 $110,880

53,550 $119 208,250

Loudspeakers

×= ×=Rate

Activity

Rate

Receivers

Activity

Activity

Usage

Activity

$346.50 $ 27,720

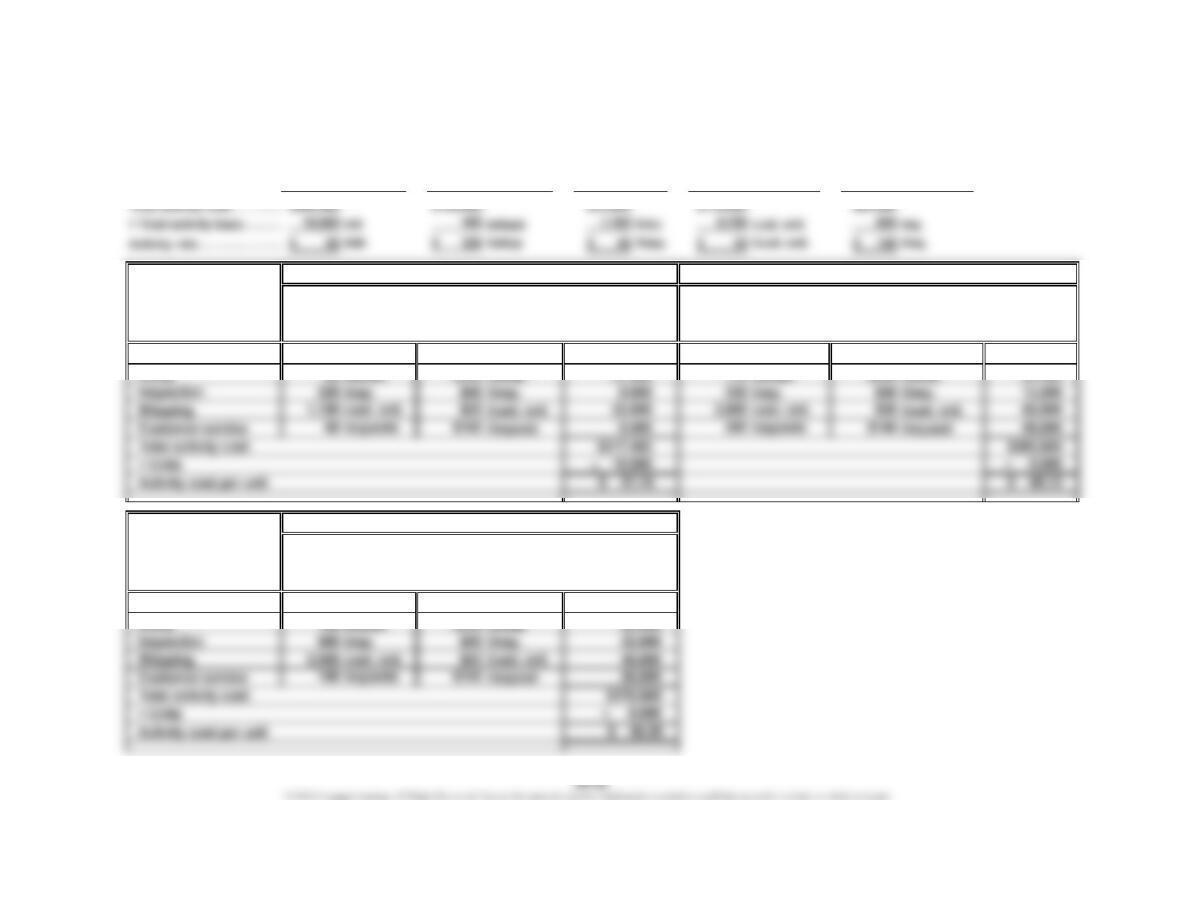

CHAPTER 26 Cost Allocation and Activity-Based Costing

Prob. 26–4B (FIN MAN); Prob. 11–4B (MAN)

1.

2.

Activity

Production 5,000 mh /mh 2,500 mh /mh

Setup 85 setups /setup 170 setups /setup

Activity

Production 2,500 mh /mh

Setup 195 setups /setup

Powdered Sugar

Activity-

White Sugar

Activity-

$125,000

$320 62,400

Base Activity Activity

Usage × Rate = Cost

Cost

Activity

Brown Sugar

Usage × Rate =

Activity-

Base Activity

Customer ServiceProduction Setup ShippingInspection

Activity

54,400

$50 $250,000 $50 $125,000

$320

Usage × Rate =

Base Activity

Cost

$320 27,200

$50

CHAPTER 26 Cost Allocation and Activity-Based Costing

Prob. 26–4B (FIN MAN); Prob. 11–4B (MAN) (Concluded)

3. The unit costs are different even though each product requires 0.5 machine

hour because the products consume many activities in ratios different from the

CHAPTER 26 Cost Allocation and Activity-Based Costing

Prob. 26–5B (FIN MAN); Prob. 11–5B (MAN)

1.

Activity cost pool……………………… $76,860 $25,920 $311,250

2. The Warehouse

Customer service……………………… × $180/sr = $ 11,160

Sales order processing………………

…

× $24/so = 7,200

…

…

Processing Support

Sales Order Advertising

Customer

Service

300 sos

62 srs

…

CHAPTER 26 Cost Allocation and Activity-Based Costing

Prob. 26–5B (FIN MAN); Prob. 11–5B (MAN) (Concluded)

3.

The Supply

Warehouse Kosmo Co. Universe

Revenues $899,100 $899,100 $899,100

4. Kosmo Co. has low profitability, while the other two customers have acceptable

margins. This is because Kosmo Co. requires many customer services, sales

order processing, and advertising support activities. For example, Kosmo Co.

orders frequently in small order sizes, which increases the sales order processing

costs; it requests a large amount of service; and it requires extensive promotional

SHRUTE INC.

Customer Profitability Report

For the Year Ended December 31, 2014

1

CHAPTER 26 Cost Allocation and Activity-Based Costing

Prob. 26–6B (FIN MAN); Prob. 11–6B (MAN)

1. The depreciation and maintenance cost per mile is calculated as follows:

2. Monthly

Ground

Personnel

Terminal City Cost per City ÷ =

Charlotte……………

…

$256,000 ÷ =

…

3.

Passenger revenue

Flight Profitability Report

Arrivals/Departures

Number of

320

Arrival/Departure

$800

Rate per City

BLUE STAR AIRLINE

For Three Representative Flights

Flight 103Flight 102Flight 101

CHAPTER 26 Cost Allocation and Activity-Based Costing

Prob. 26–6B (FIN MAN); Prob. 11–6B (MAN) (Concluded)

4. The break-even formula is:

None of the costs in a flight are variable to the number of seats. Essentially, the

costs will be incurred regardless of the number of passengers on the flight.

Thus, the costs of the flight are all fixed. Given this assumption, the break-even

number of passengers is a straightforward division of the costs by the fare. The

results are (rounded to the nearest whole number):

Break-Even Number of

Passengers per Flight

Fixed Costs of a Flight

Ticket Price – Variable Cost per Seat

=

Flight

101

Approximate Break-Even

$41,700 ÷ $695 = 60 passengers

CHAPTER 26 Cost Allocation and Activity-Based Costing

CP 26–1 (FIN MAN); CP 11–1 (MAN)

The net income is larger because the controller took period costs and treated them

as product costs for financial reporting purposes. All of the post-manufacturing

costs should be treated as an expense in the period incurred according to generally

accepted accounting principles (GAAP). If treated as product costs for financial

CP 26–2 (FIN MAN); CP 11–2 (MAN)

The product profitability report indicates that the two products are equal in terms of

profitability (on a per-case basis). However, the additional information indicates that

CASES & PROJECTS

CHAPTER 26 Cost Allocation and Activity-Based Costing

CP 26–3 (FIN MAN); CP 11–3 (MAN)

Wells Fargo Insurance Service’s (WFIS) activity-based costing model provides more

accurate product costs than does the revenue-based allocation scheme. This is

because WFIS has a large amount of processing and service expenses that are

CHAPTER 26 Cost Allocation and Activity-Based Costing

CP 26–4 (FIN MAN); CP 11–4 (MAN)

1. Floor Bookshelf Ribbon

Loudspeakers Loudspeakers Loudspeakers

2. To: Management of Boom Box Sounds Inc.

From: Controller

The enclosed product profitability report indicates that our product lines provide

varying degrees of profitability. By far, our most profitable product line is the

bookshelf loudspeakers. The floor loudspeakers provide a healthy gross profit.

However, our marketing costs associated with this product line exceed our

gross profit. As a result, the product line is unprofitable as a whole. The ribbon

loudspeakers, on the other hand, have a very weak gross profit. As a result, the

product line is just barely profitable. As a result of this analysis, I offer the

following recommendations:

Bookshelf Loudspeakers

Floor Loudspeakers

We should retain the floor loudspeakers in our product portfolio. The product

provides us a healthy gross profit. Unfortunately, we spend too much on

Ribbon Loudspeakers

Ribbon loudspeakers are one of our “up and comers.” No other competitor has

a similar product. Thus, we have the market to ourselves. Yet, this product does

not meet our profitability objectives. We are unable to spend much on marketing

CHAPTER 26 Cost Allocation and Activity-Based Costing

CP 26–5 (FIN MAN); CP 11–5 (MAN)

Adlin’s concern appears valid. Teldar Tech Inc. is presently using direct labor as an

allocation base. This method, either as a single plantwide factory overhead rate or

as multiple production department factory overhead rates, will distort the product

costs when activities are consumed by products in different proportions than their

CP 26–6 (FIN MAN); CP 11–6 (MAN)

Students may arrive at a variety of possible activities and activity bases. Below is a

representative list.

Activity Activity Base

Opening an account Number of accounts opened

Teller deposit transaction Number of teller deposits