CHAPTER 16 Financial Statement Analysis

Ex. 16–18

a.

b.

c. Both the return on total assets and the return on stockholders’ equity have decreased

over the two-year period. The return on total assets decreased from 11.8% to 6.8%, and

the return on stockholders’ equity decreased from 17.7% to 10.4%. The return on

stockholders’ equity exceeds the return on total assets due to the positive use of

leverage.

d. During fiscal Year 3, Ralph Lauren’s results were weak compared to the industry

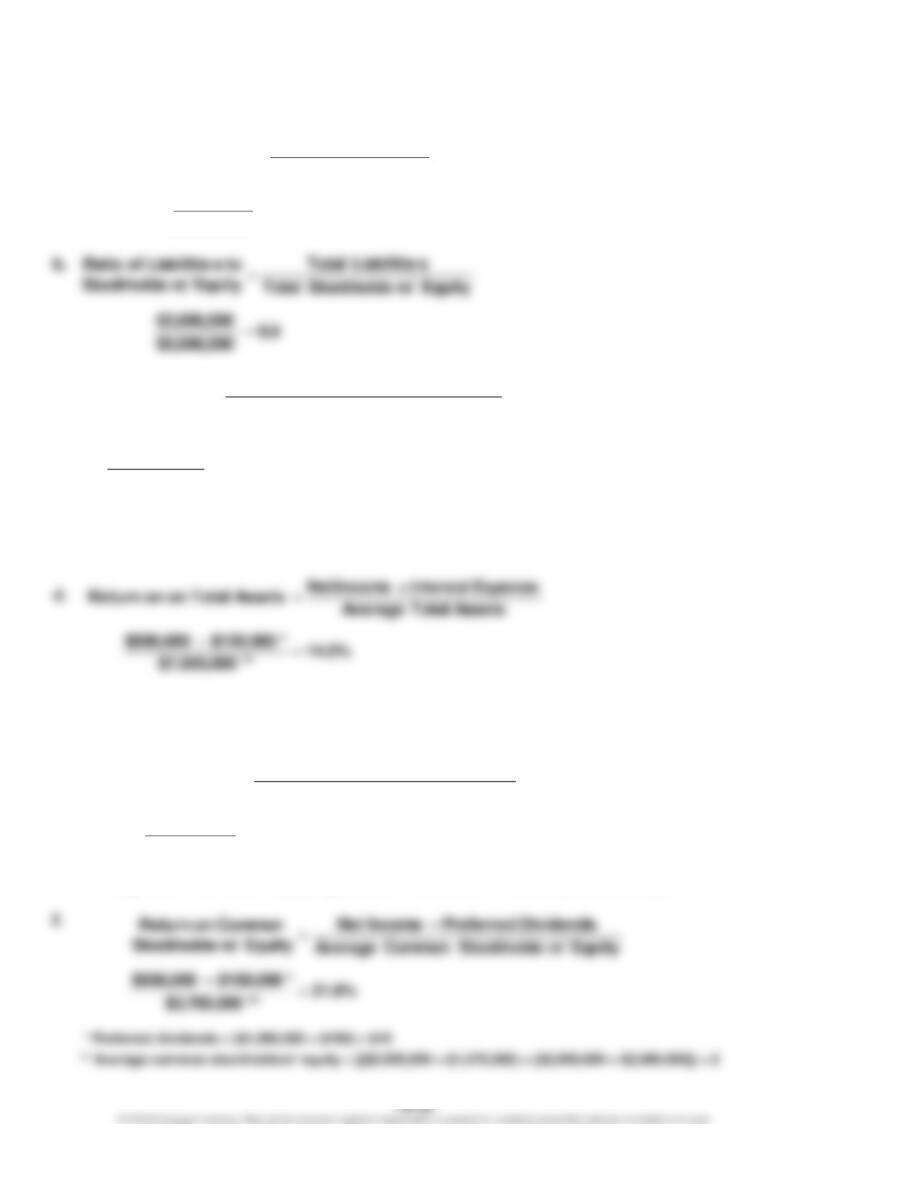

AssetsTotal Average

ExpenseInterest + IncomeNet

AssetsTotal on Return

=

Equity rs’Stockholde Total Average

IncomeNet

Equity rs’Stockholde on Return

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–19

a.

c.

* Average total assets = [($7,000,000 + $8,000,000) ÷ 2] – $3,000,000. The end-of-period total assets are equal

to the sum of total liabilities ($3,000,000) and stockholders’ equity ($5,000,000).

* Interest expense = $2,000,000 6%

** Average total assets = ($7,000,000 + $8,000,000) ÷ 2

e.

* Average total stockholders’ equity = [($1,570,000 + $2,000,000 + $1,000,000) + $5,000,000] ÷ 2

1.6

$2,000,000

$3,200,000

sLiabilitie Term–Long

(net) AssetsFixed

sLiabilitie Term–Long

to AssetsFixed of Ratio

=

=

4.2

*$4,500,000

0$18,900,00

s)investmentterm–long (excluding

AssetsTotalAverage

Sales

TurnoverAsset

=

=

19.4%

*$4,785,000

$930,000

Equity rs’Stockholde Total Average

IncomeNet

Equity rs’Stockholde

on Return

=

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–20

*Interest expense = $5,000,000 bonds payable 8%

ExpenseInterest

ExpenseInterest Expense Tax Income Before Income

EarnedInterest Times a. +

=

times 8.5

$400,000

*$400,000 $3,000,000 =

+

10.0

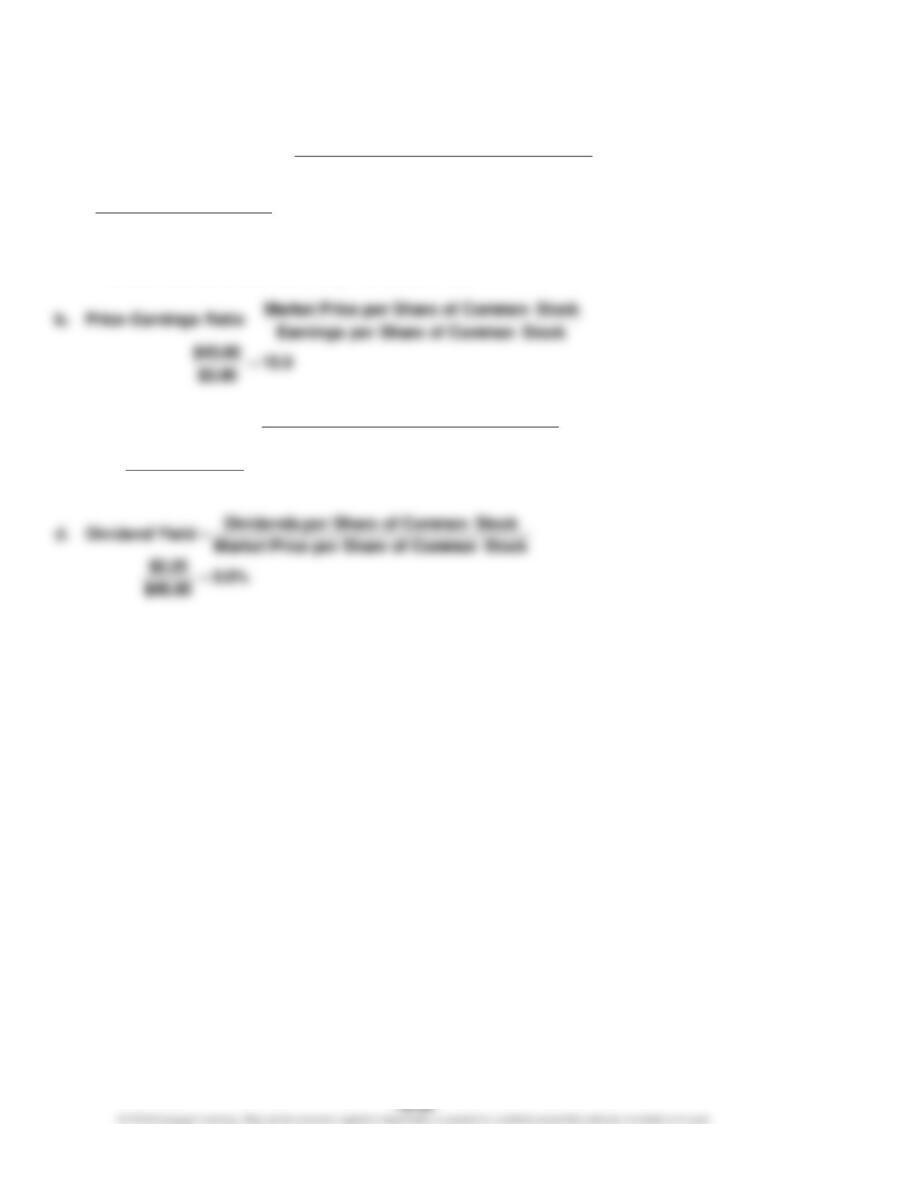

$3.20

$32.00

Share per Earnings

Stock Common of Share per PriceMarket

Ratio Earnings–Price c.

=

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–21

* Preferred dividends = ($2,500,000 ÷ $40) × $4

** Shares of common stock outstanding = $10,000,000 ÷ $20

$3.00

**shares 500,000

*$250,000 – $1,750,000

gOutstandin Stock Common of Shares

Dividends Preferred – IncomeNet

Share per Earnings a.

=

=

$2.25

shares 500,000

$1,125,000

gOutstandin Stock Common of Shares

Dividends Common

Share per Dividends c.

=

=

CHAPTER 16 Financial Statement Analysis

Ex. 16–22

a.

b. Coca-Cola has a small dividend yield and the highest price-earnings ratio of the three

companies. Stock market participants value Coca-Cola common stock on the basis of

both its dividend and its potential share price appreciation. Alphabet pays no dividend

118.4

$1.51

$178.85

:Company Cola–Coca The

37.9

$20.91

$792.45

:Alphabet

21.3

$4.83

$103.04

:Company & Deere

Share per Earnings

Stock Common of Share per PriceMarket

Ratio Earnings–Price

=

=

=

=

CHAPTER 16 Financial Statement Analysis

Appendix 1 Ex. 16–23

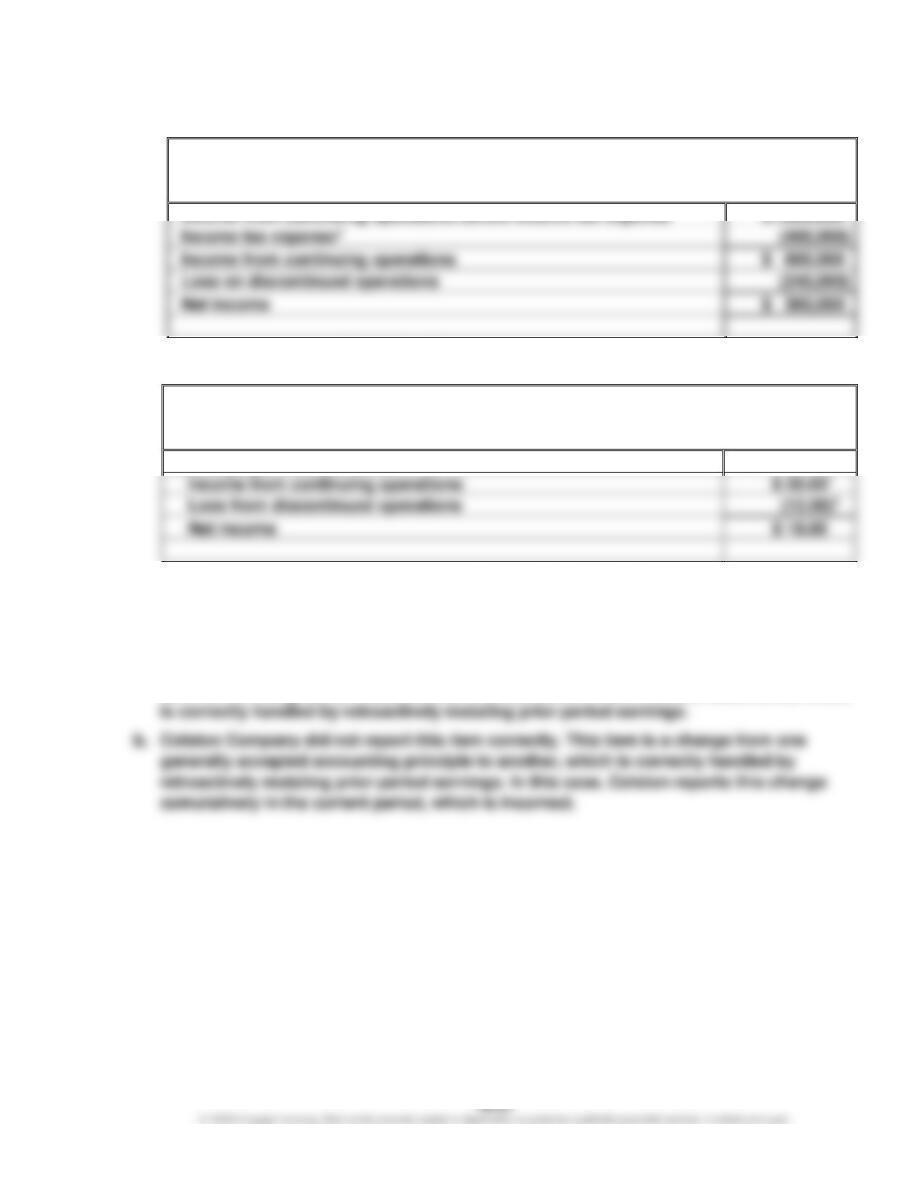

a. Earnings per share on income before discontinued operations:

Net income …………………………………………………………………………… $4,000,000

Gain on discontinued operations …………………………………………… (400,000)

Income before discontinued operations …………………………………. $3,600,000

gOutstandin

Stock Common of Shares

Dividends Preferred–

Operations edDiscontinu Before Income

Stock Common on Share per

Operations Disc. Before Earnings

=

CHAPTER 16 Financial Statement Analysis

Appendix 1 Ex. 16–24

a.

Apex Inc.

Partial Income Statement

For the Year Ended December 31

* Income tax expense = $1,000,000 40%

b.

Apex Inc.

Partial Income Statement

For the Year Ended December 31

Earnings per common share:

1EPS on Income from continuing operations = $30.00 = $600,000 ÷ 20,000

2EPS on Loss from discontinued operations = –$12.00 = –$240,000 ÷ 20,000

Appendix 1 Ex. 16–25

a. Colston Company reported this item correctly in the financial statements. This item is an

error in the recognition, measurement, or presentation in the financial statements, which

CHAPTER 16 Financial Statement Analysis

Appendix 2 Ex. 16–26

a.

Anson Industries, Inc.

Income Statement

For the Year Ended December 31, 20Y1

Sales

$ 4,000,000

Cost of goods sold

(2,300,000)

Gross profit

Operating expenses

Operating income

Income tax expense

Net income

Other comprehensive income

Comprehensive income

b.

Anson Industries, Inc.

Income Statement

For the Year Ended December 31, 20Y1

Sales

$ 4,000,000

Cost of goods sold

(2,300,000)

Gross profit

Operating expenses

Operating income

$ 700,000

Income tax expense

Net income

Anson Industries, Inc.

Statement of Comprehensive Income

For the Year Ended December 31, 20Y1

Net income

$420,000

Comprehensive income

$870,000

CHAPTER 16 Financial Statement Analysis

PROBLEMS

Prob. 16–1A

1.

McDade Company

Comparative Income Statement

For the Years Ended December 31, 20Y2 and 20Y1

20Y2

20Y1

Increase/(Decrease)

Amount

Percent

Sales

$ 16,800,000

$ 15,000,000

$1,800,000

12.0%

Cost of goods sold

(11,500,000)

(10,000,000)

1,500,000

15.0%

Gross profit

$ 5,300,000

$ 5,000,000

$ 300,000

6.0%

Selling expenses

$ (1,770,000)

$ (1,500,000)

$ 270,000

18.0%

Administrative expenses

(1,000,000)

22.0%

Total operating expenses

$ (2,500,000)

$ 490,000

19.6%

Operating income

$ 2,310,000

$ 2,500,000

$ (190,000)

Other revenue

31,950

14.2%

Income before income

tax expense

$ 2,566,950

$ (158,050)

Income tax expense

(1,500,000)

(87,000)

Net income

$ 1,153,950

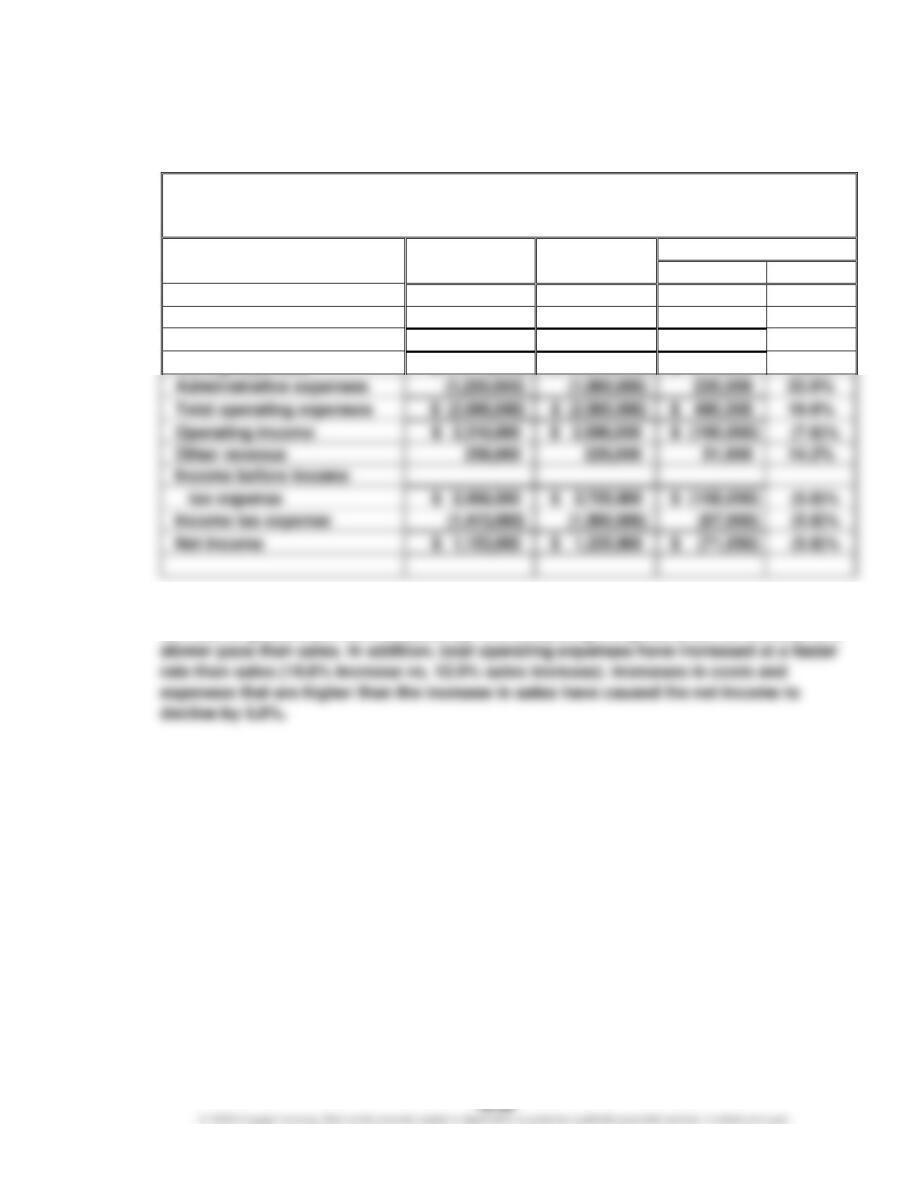

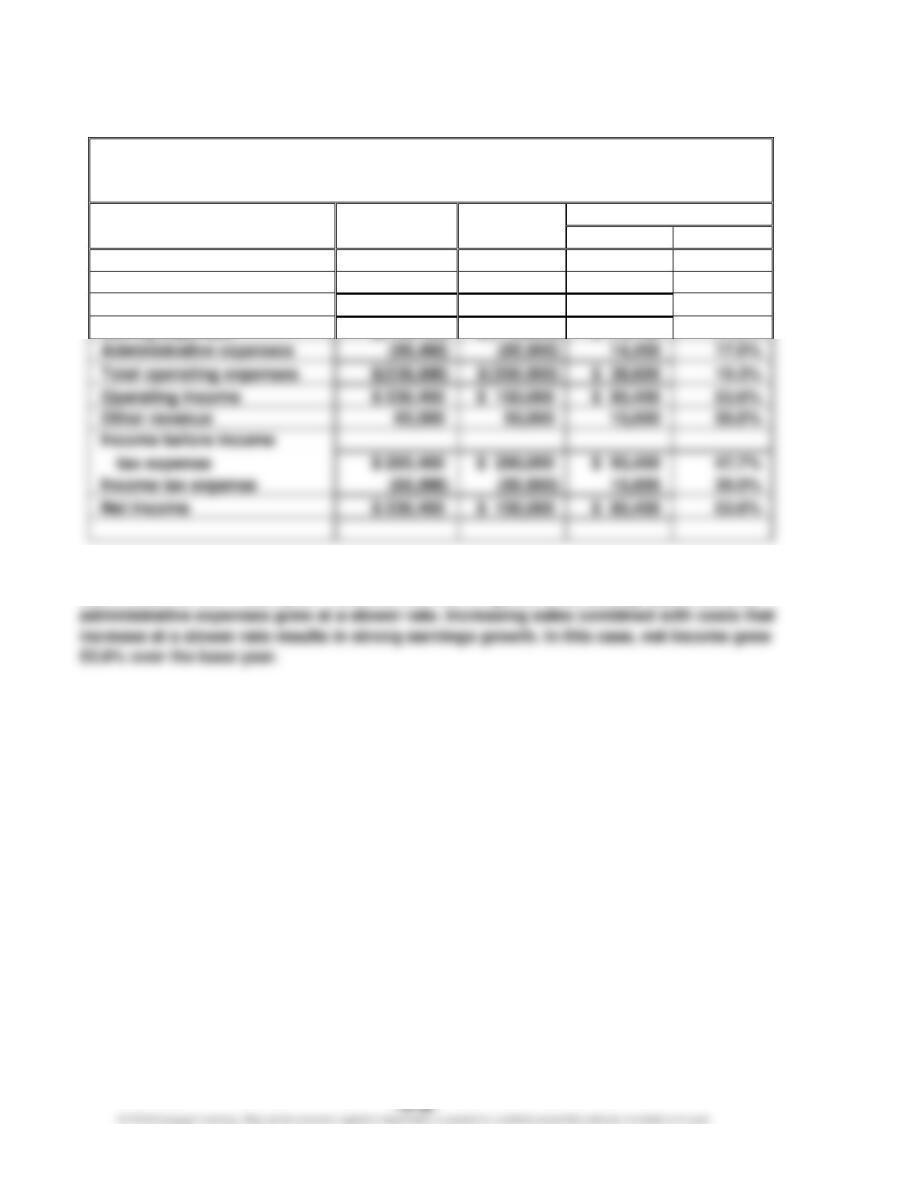

2. Net income has declined from 20Y1 to 20Y2. Sales have increased by 12.0%; however,

the cost of goods sold has increased by 15.0%, causing the gross profit to increase at a

CHAPTER 16 Financial Statement Analysis

Prob. 16–2A

1.

Tri-Comic Company

Comparative Income Statement

For the Years Ended December 31, 20Y2 and 20Y1

20Y2

20Y1

Amount

Percent

Amount

Percent

Sales

$1,500,000

100.0%

$1,250,000

100.0%

Cost of goods sold

(510,000)

(34.0)%

(475,000)

(38.0)%

Gross profit

$ 990,000

66.0%

$ 775,000

62.0%

Selling expenses

$ (270,000)

(18.0)%

$ (200,000)

(16.0)%

Administrative expenses

(180,000)

(156,250)

(12.5)%

Total operating expenses

$ (450,000)

(30.0)%

$ (356,250)

(28.5)%

Operating income

$ 540,000

$ 418,750

33.5%

Other revenue

4.0%

Income before income

$ 600,000

$ 468,750

37.5%

Income tax expense

(450,000)

(30.0)%

(375,000)

(30.0)%

Net income

10.0%

$ 93,750

7.5%

2. The vertical analysis indicates that the costs other than selling expenses (cost of goods

sold and administrative expenses) improved as a percentage of sales. As a result, net

CHAPTER 16 Financial Statement Analysis

Prob. 16–3A

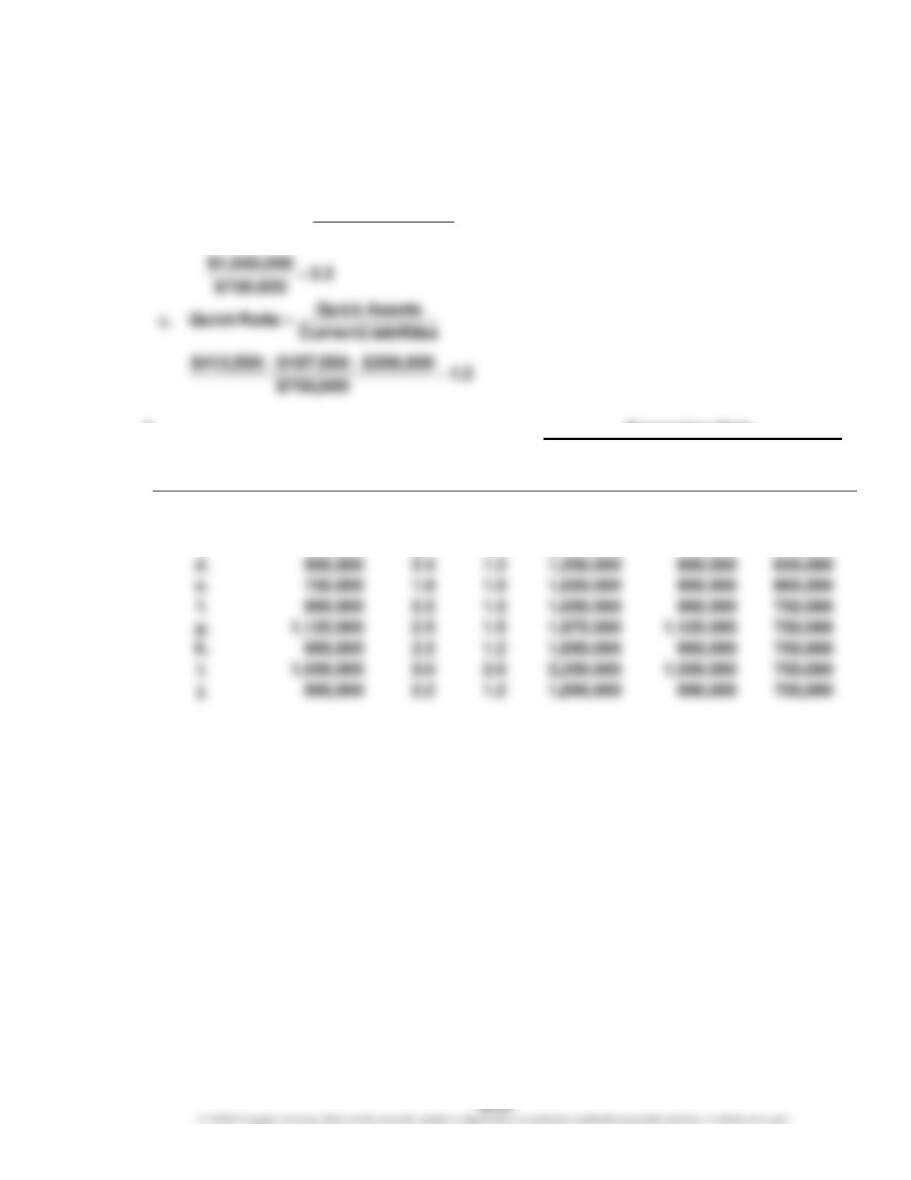

1. a. Working Capital = Current Assets – Current Liabilities

$1,650,000 – $750,000 = $900,000

b.

2. Supporting Data

Transaction

Working

Capital

Current

Ratio

Quick

Ratio

Current

Assets

Quick

Assets

Current

Liabilities

a.

$ 900,000

2.2

1.2

$1,650,000

$ 900,000

$750,000

b.

900,000

2.4

1.2

1,525,000

775,000

625,000

c.

900,000

2.0

1.0

1,760,000

900,000

860,000

d.

900,000

2.4

1.2

1,550,000

800,000

650,000

e.

750,000

1.8

1.0

1,650,000

900,000

900,000

g.

1,125,000

2.5

1.5

1,875,000

750,000

h.

900,000

2.2

1.2

1,650,000

900,000

750,000

1,500,000

3.0

2.0

2,250,000

750,000

900,000

2.2

1.2

1,650,000

890,000

750,000

sLiabilitieCurrent

setsCurrent As

RatioCurrent

=

CHAPTER 16 Financial Statement Analysis

Prob.16–4A

1. Working Capital: $2,464,000 – $880,000 = $1,584,000

Ratio

Numerator

Denominator

Calculated

Value

2.

Current ratio

$2,464,000

$880,000

2.8

3.

Quick ratio

$1,936,000

$880,000

2.2

4.

Accounts receivable turnover

$10,850,000

($585,000 + $500,000) ÷ 2

20.0

5.

Number of days’ sales in receivables

($585,000 + $500,000) ÷ 2

$10,850,000 ÷ 365

18.3

6.

Inventory turnover

$6,000,000

($420,000 + $380,000) ÷ 2

15.0

7.

Number of days’ sales in inventory

($420,000 + $380,000) ÷ 2

$6,000,000 ÷ 365

24.3

8.

Ratio of fixed assets to long-term liabilities

$5,760,000

$3,200,000

1.8

9.

Ratio of liabilities to stockholders’ equity

$4,080,000

$4,944,000

0.8

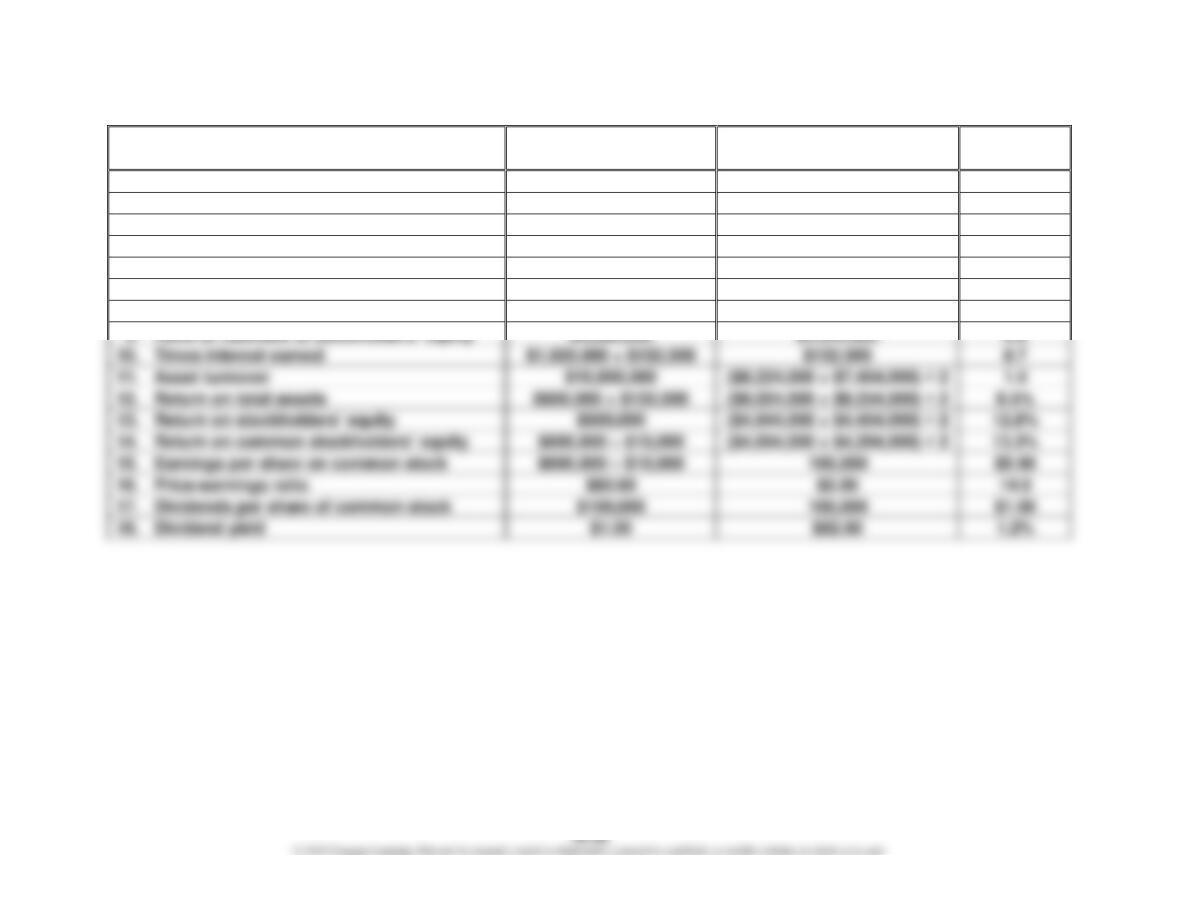

Times interest earned

$132,000

8.7

Asset turnover

$10,850,000

1.4

Return on total assets

Return on stockholders’ equity

$600,000

Return on common stockholders’ equity

Earnings per share on common stock

$82.60

14.0

Dividends per share of common stock

$100,000

Dividend yield

CHAPTER 16 Financial Statement Analysis

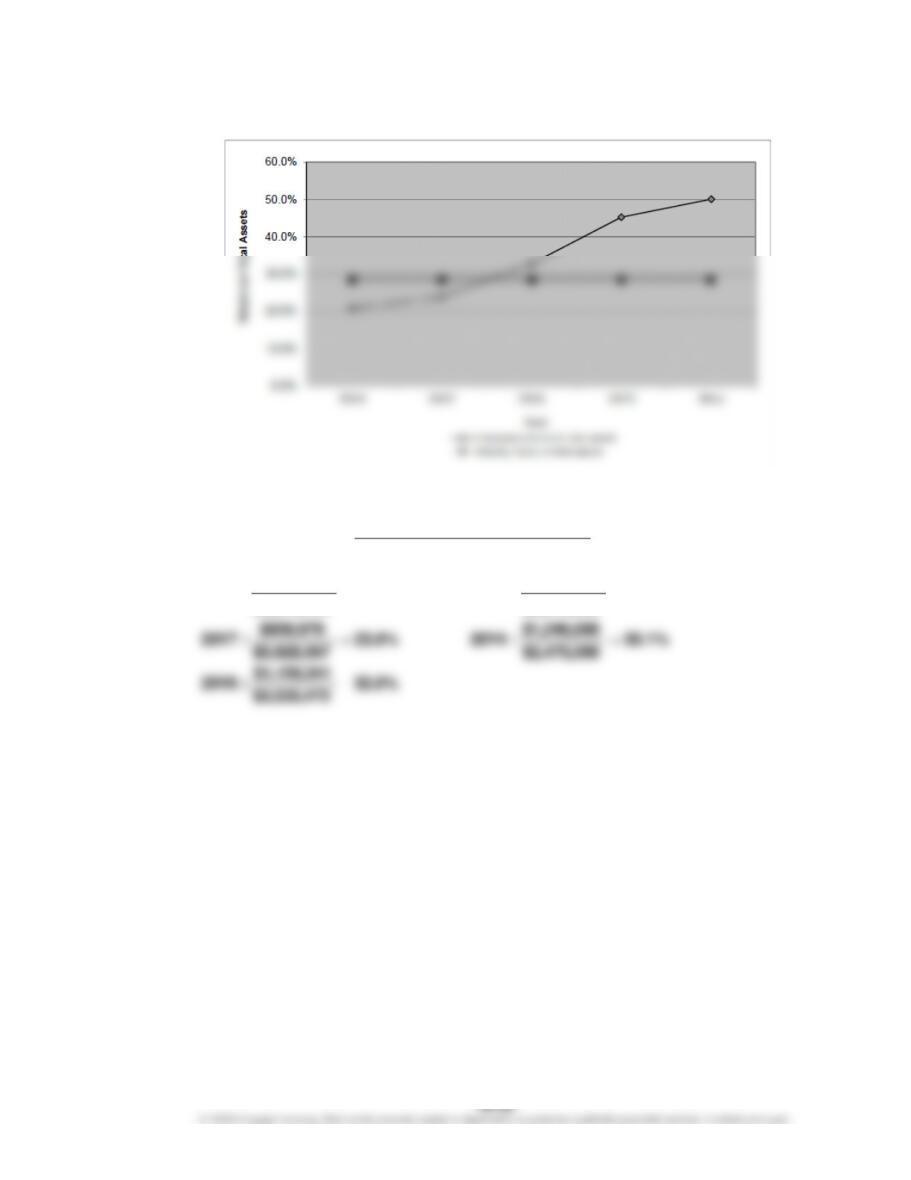

Prob. 16–5A

1.

a.

AssetsTotal Average

ExpenseInterest IncomeNet

AssetsTotal on Return +

=

45.3%

$1,379,000

:20Y520.8%

$889,453

:20Y8

==

CHAPTER 16 Financial Statement Analysis

Prob. 16–5A (Continued)

1.

b.

Equity rs’Stockholde Total Average

IncomeNet

Equity rs’Stockholde on Return =

44.4%

$1,992,000

$884,000

:20Y57.7%

$3,569,855

$273,406

:20Y8

==

CHAPTER 16 Financial Statement Analysis

Prob. 16–5A (Continued)

1.

c.

ExpenseInterest

ExpenseInterest Expense Tax Income IncomeNet

EarnedInterest Times ++

=

3.1

$1,539,000

:20Y51.5

$921,202

:20Y8

==

CHAPTER 16 Financial Statement Analysis

Prob. 16–5A (Continued)

1.

d.

Note: The total liabilities are the difference between the total assets and total

stockholders’ equity ending balances.

Equity rs’Stockholde Total

sLiabilitie Total

Equity rs’Stockholde

to sLiabilitie of Ratio =

0.4

$904,500

:20Y50.2

$710,621

:20Y8

==

CHAPTER 16 Financial Statement Analysis

Prob. 16–5A (Concluded)

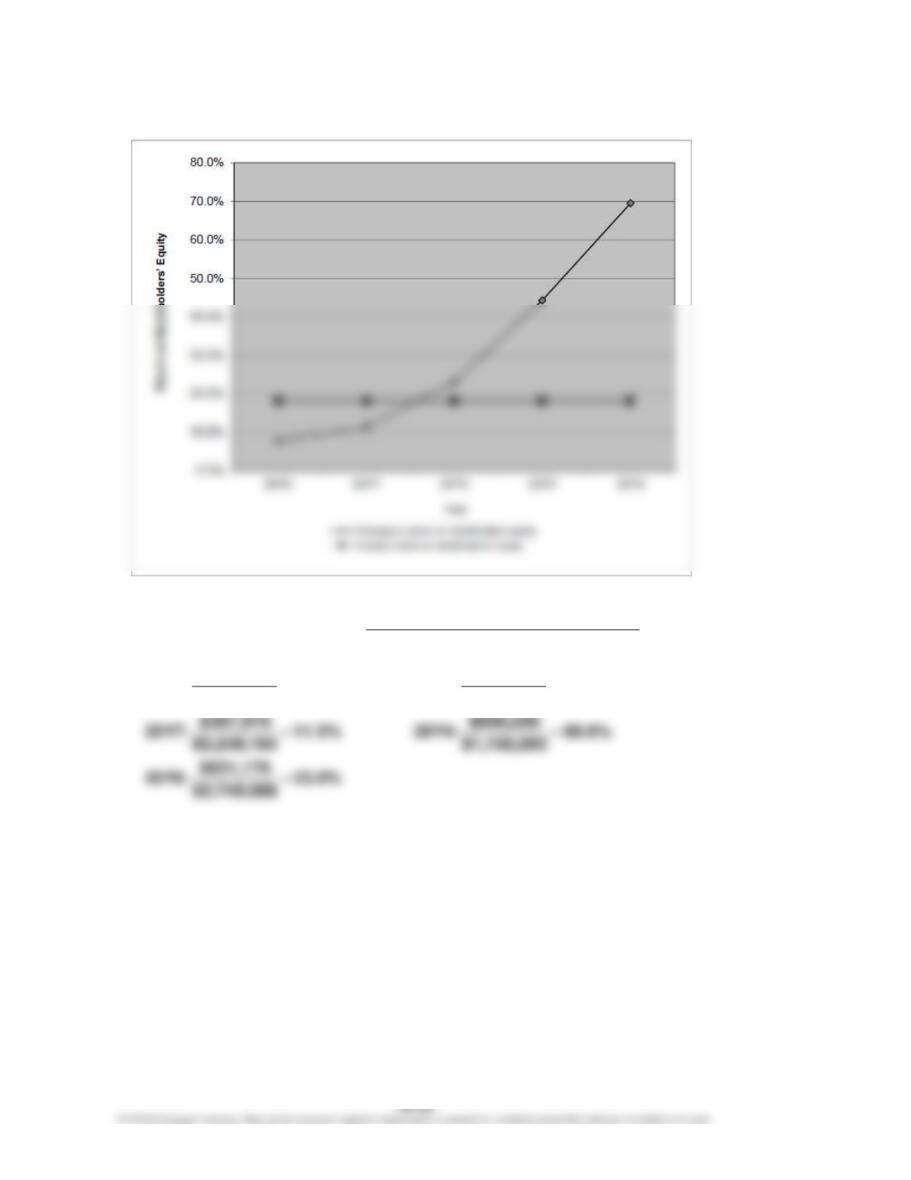

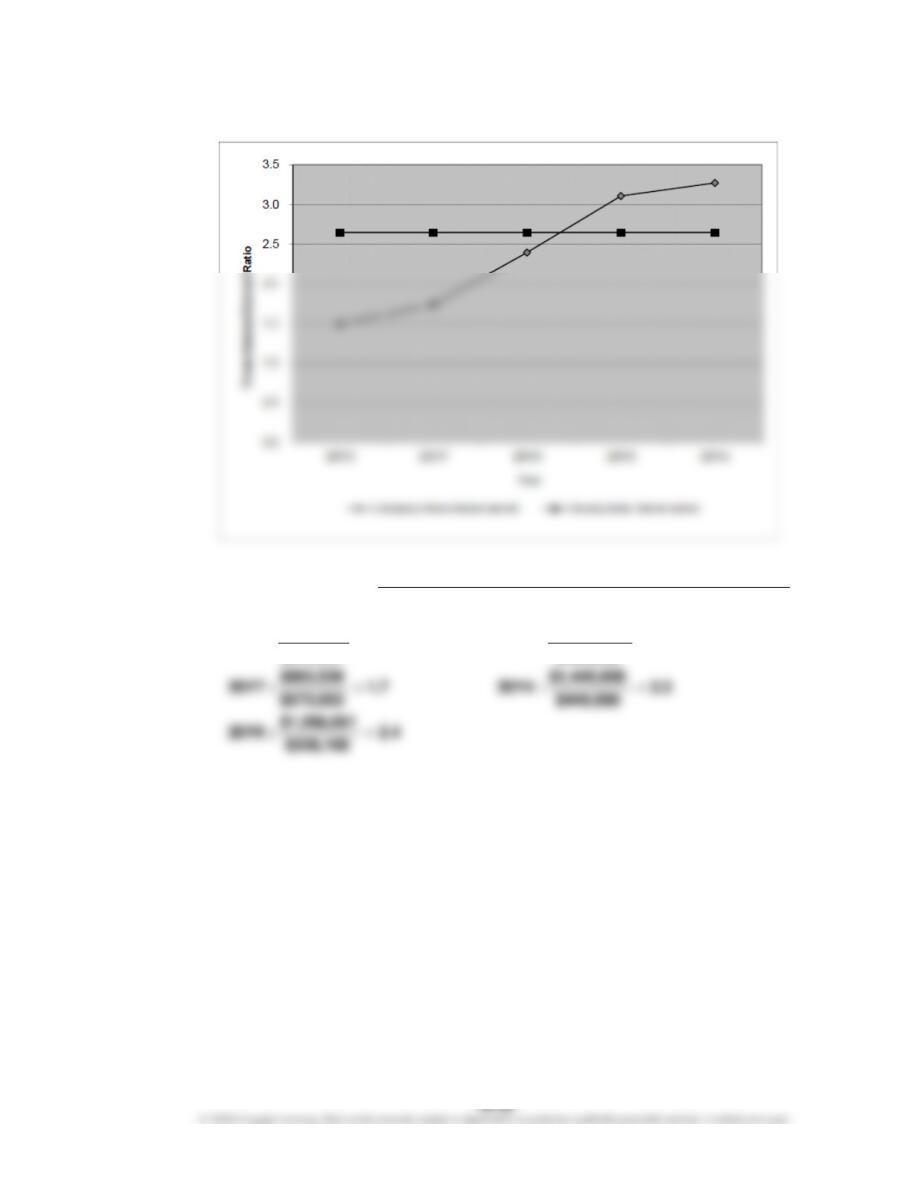

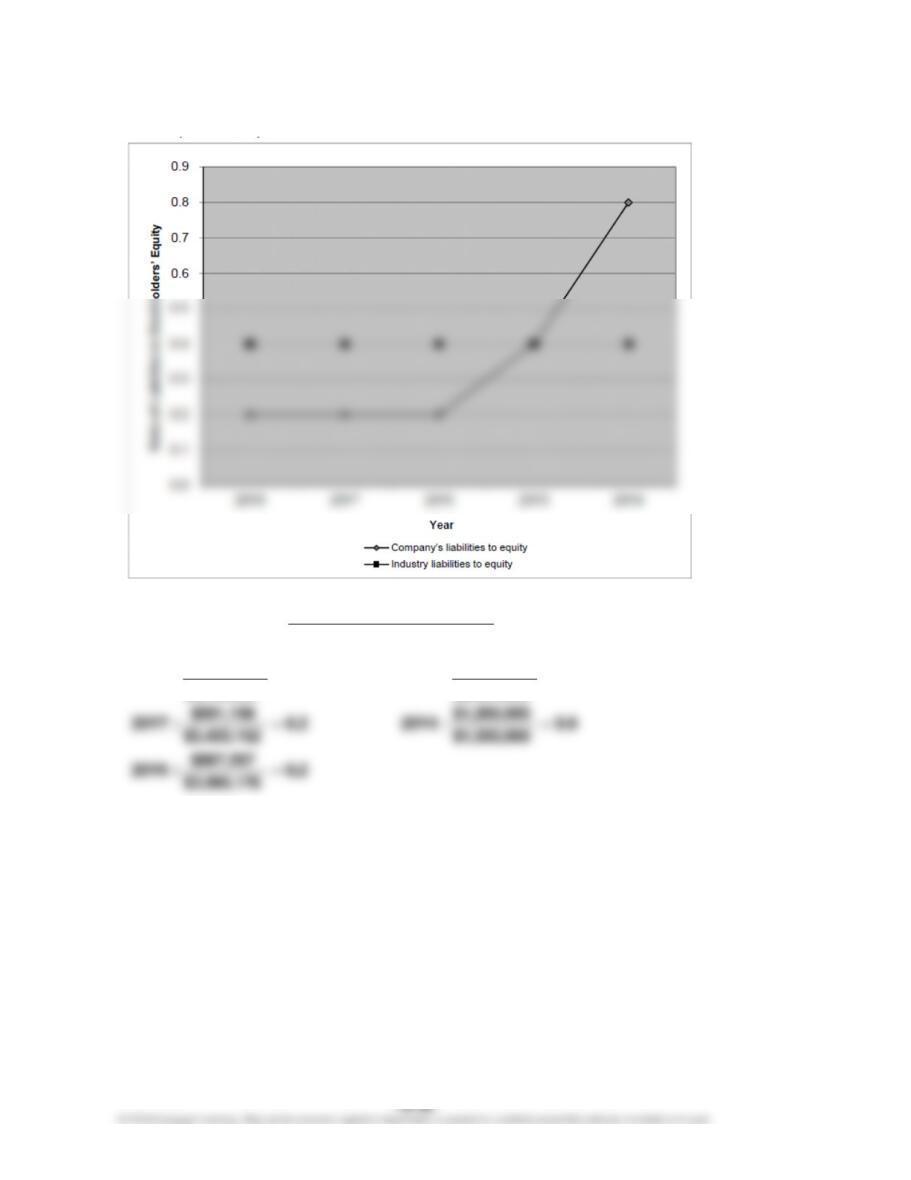

2. Both the return on total assets and the return on stockholders’ equity have been moving

in a negative direction in the last five years. Both measures have moved below the

industry average over the last two years. The cause of this decline is driven by a rapid

CHAPTER 16 Financial Statement Analysis

Prob. 16–1B

1.

Macklin Inc.

Comparative Income Statement

For the Years Ended December 31, 20Y2 and 20Y1

Increase/(Decrease)

20Y2

20Y1

Amount

Percent

Sales

$ 910,000

$ 700,000

$210,000

30.0%

Cost of goods sold

(441,000)

(350,000)

91,000

26.0%

Gross profit

$ 469,000

$ 350,000

$119,000

34.0%

Selling expenses

$(139,150)

$ 24,150

Administrative expenses

14,450

17.0%

Total operating expenses

$(238,600)

19.3%

Operating income

$ 230,400

$ 150,000

53.6%

Other revenue

15,000

30.0%

Income before income

$ 295,400

$ 200,000

47.7%

Income tax expense

15,000

30.0%

Net income

$ 230,400

$ 80,400

53.6%

2. The profitability has significantly improved from 20Y1 to 20Y2. Sales have increased by

30.0% over the 20Y1 base year. However, the cost of goods sold, selling expenses, and

CHAPTER 16 Financial Statement Analysis

Prob. 16–2B

1.

Fielder Industries Inc.

Comparative Income Statement

For the Years Ended December 31, 20Y2 and 20Y1

20Y2

20Y1

Amount

Percent

Amount

Percent

Sales

$1,300,000

100.0%

$ 1,180,000

100.0%

Cost of goods sold

(682,500)

(52.5)%

(613,600)

(52.0)%

Gross profit

$ 617,500

47.5%

$ 566,400

48.0%

Selling expenses

$ (260,000)

(20.0)%

$ (188,800)

(16.0)%

Administrative expenses

(169,000)

(13.0)%

(177,000)

(15.0)%

Total operating expenses

$ (429,000)

(33.0)%

(31.0)%

Operating income

$ 188,500

17.0%

Other revenue

Income before income

$ 266,500

23.0%

Income tax expense

(117,000)

(106,200)

Net income

$ 149,500

14.0%

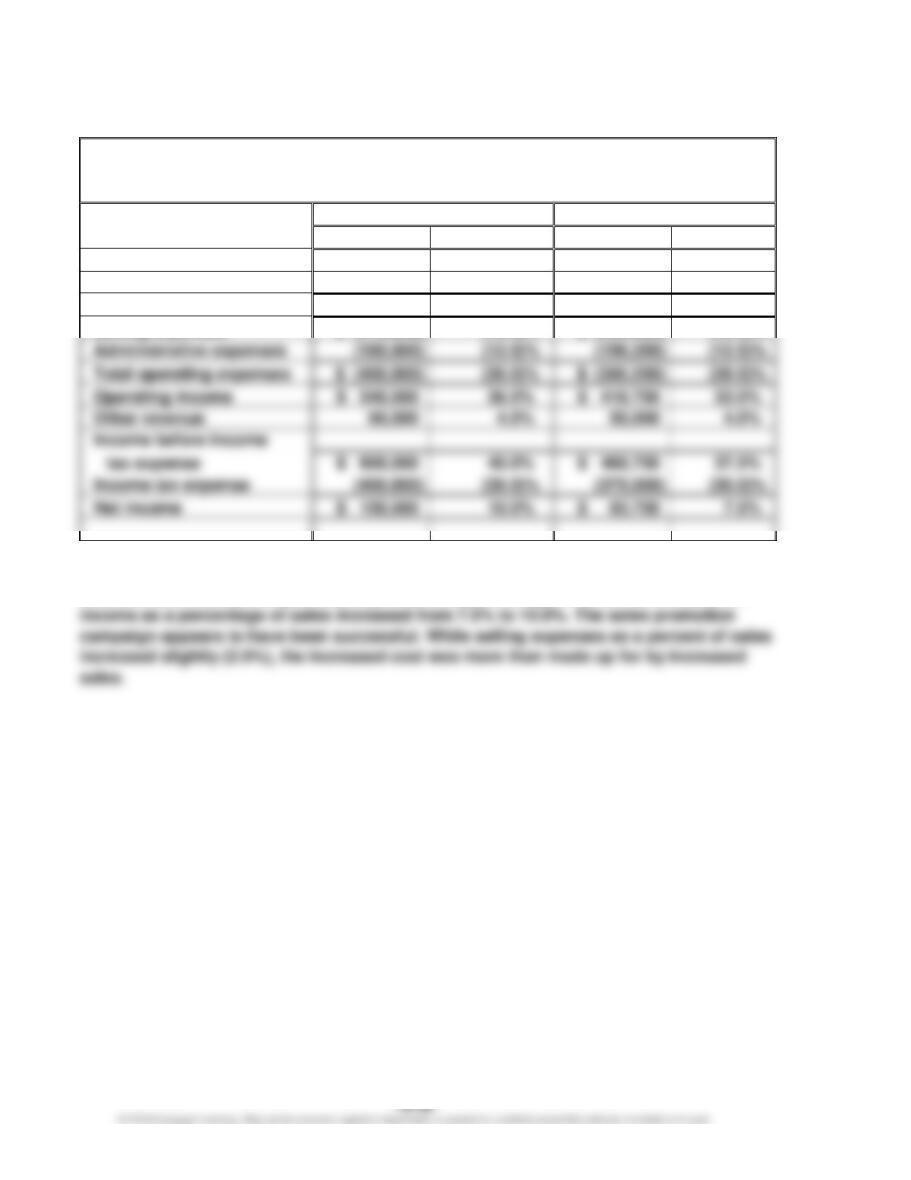

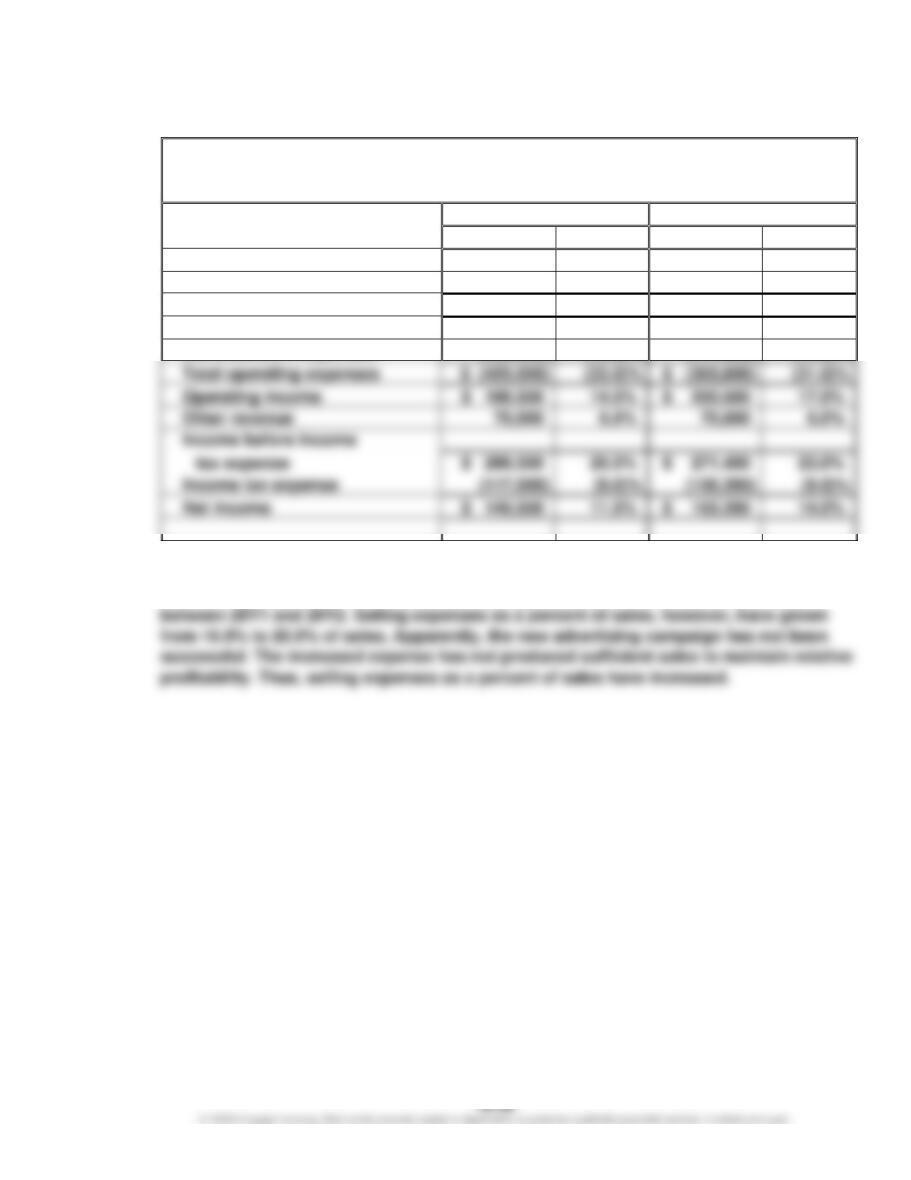

2. The net income as a percent of sales has declined. All the costs and expenses, other

than selling expenses, have maintained their approximate cost as a percent of sales