CHAPTER 16

SOLUTIONS TO EXERCISES—SET B

EXERCISE 16-1B

2016

1. Jan. 1 Debt Investments ……………………………….. 70,000

Cash …………………………………………… 70,000

2. Dec. 31 Interest Receivable …………………………….. 5,600

Interest Revenue

($70,000 X 8%) …………………………. 5,600

2019

EXERCISE 16-2B

January 1, 2016

Debt Investments ……………………………………………………. 50,000

Cash ………………………………………………………………… 50,000

December 31, 2016

Interest Receivable ($50,000 x 12%) …………………………. 6,000

Interest Revenue ………………………………………………. 6,000

EXERCISE 16-3B

(a) Feb. 1 Stock Investments ……………………………… 5,200

Cash …………………………………………… 5,200

July 1 Cash (500 X $1) …………………………..……… 500

Dividend Revenue ……………………….. 500

(b) Dividend revenue and the gain on sale of stock investments are reported

under other revenues and gains in the income statement.

EXERCISE 16-4B

Jan. 1 Stock Investments ……………………………………. 182,100

Cash …………………………………………………. 182,100

July 1 Cash (4,000 X $3) ……………………………………… 12,000

Dividend Revenue ……………………………… 12,000

EXERCISE 16-5B

February 1

Stock Investments ……………………………………………………. 12,400

Cash (400 X $31) ……………………………………………….. 12,400

March 20

April 25

Cash (300 X $1.00) ……………………………………………………. 300

Dividend Revenue ……………………………………………… 300

June 15

EXERCISE 16-6B

(a) Jan. 1 Stock Investments ……………………………… 240,000

Cash …………………………………………… 240,000

Dec. 31 Cash ($60,000 X 35%) …………………………. 21,000

Stock Investments ………………………. 21,000

EXERCISE 16-7B

1. 2017

Mar. 18 Stock Investments …………………………….. 280,000

Cash (200,000 X 10% X $14) …………. 280,000

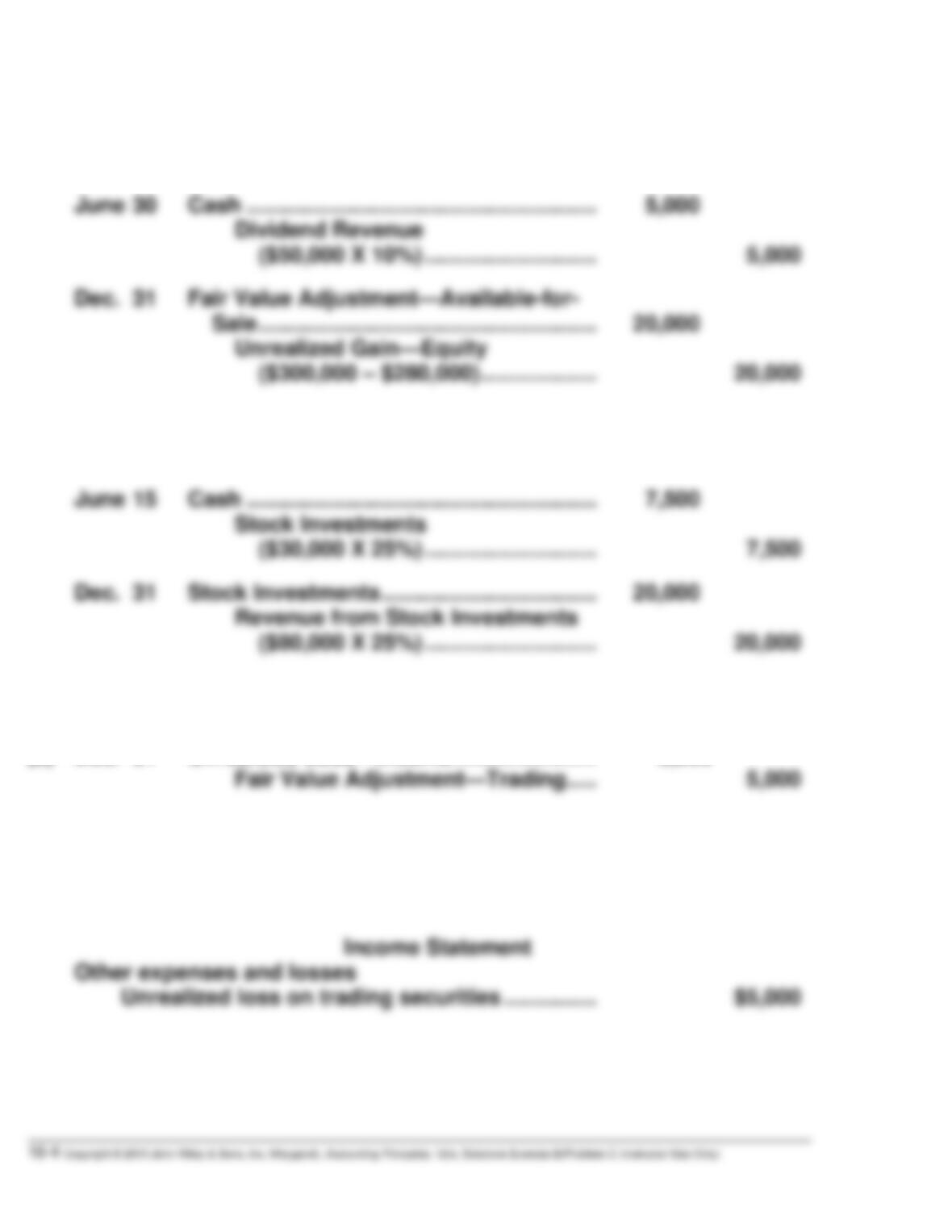

June 30 Cash …………………………..……………………. 5,000

Dividend Revenue

($50,000 X 10%) ………………………. 5,000

2. Jan. 1 Stock Investments …………………………….. 67,500

Cash (30,000 X 25% X $9) ……………. 67,500

June 15 Cash …………………………..……………………. 7,500

Stock Investments

($30,000 X 25%) ………………………. 7,500

EXERCISE 16-8B

(a) Dec. 31 Unrealized Loss—Income ………………….. 5,000

Fair Value Adjustment—Trading ….. 5,000

(b) Balance Sheet

Current assets

Short-term investments, at fair value……………. $50,000

EXERCISE 16-9B

(a) Dec. 31 Unrealized Gain or Loss—Equity …………….. 5,000

Fair Value Adjustment—Available-

for-Sale ……………………………………….. 5,000

(b) Balance Sheet

Investments

(c) Dear Mr. Wyman:

Investments which are classified as trading (held for sale in the near

term) are reported at fair value in the balance sheet, with unrealized

gains or losses reported in net income. Investments which are classified as

available-for-sale (held longer than trading but not to maturity) are also

reported at fair value, but unrealized gains or losses are reported in the

stockholders’ equity section.

EXERCISE 16-10B

(a) Fair Value Adjustment—Trading

($125,000 – $120,000) ………………………………………… 7,000

Unrealized Gain—Income ………………………………. 7,000

(b) Balance Sheet

Current assets

Short-term investments, at fair value………………. $127,000

Investments

Investment in stock of less than 20% owned

companies, at fair value ……………………………… 95,000

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 16-1C

(a) 2016

Jan. 1 Debt Investments …………………………... 800,000

Cash ………………………………………. 800,000

Dec. 31 Interest Receivable ($800,000 X .09) .. 72,000

Interest Revenue …………………….. 72,000

Dec. 31 Interest Receivable ($400,000 X .09) .. 36,000

Interest Revenue …………………….. 36,000

(b) 2016

PROBLEM 16-1C (Continued)

(c) Balance Sheet

Current assets

Interest receivable ……………………………………………… $ 72,000

Investments

PROBLEM 16-2C

(a) Feb. 1 Stock Investments ………………………………. 40,800

Cash ……………………………………………. 40,800

Mar. 1 Stock Investments ………………………………. 15,300

Cash ……………………………………………. 15,300

Aug. 1 Cash ………………………………………………….. 21,600

Gain on Sale of Stock Investments… 1,200

Stock Investments

[($40,800 ÷ 600) X 300] ………………. 20,400

Sept. 1 Cash ($1 X 500) …………………………………… 500

Dividend Revenue ………………………… 500

Oct. 1 Cash ($60,000 X 9% X 1/2) ……………………. 2,700

Interest Revenue ………………………….. 2,700

PROBLEM 16-2C (Continued)

(b) Dec. 31 Unrealized Loss—Income ………………….. 1,400

Fair Value Adjustment—Trading ….. 1,400

Security

Cost

Fair Value

RNA common

$20,400

$19,800

(300 X $66)

(c) Current assets

Trading securities, at fair value …………………………………. $34,300

PROBLEM 16-3C

(a) 2017

July 1 Cash (6,000 X $1) ……………………………….. 6,000

Dividend Revenue ……………………….. 6,000

Aug. 1 Cash (3,000 X $.50) …………………………….. 1,500

Dividend Revenue ……………………….. 1,500

Oct. 1 Cash (600 X $27) ………………………………… 16,200

Stock Investments (600 X $20) ……… 12,000

Gain on Sale of Stock

Investments

[$16,200 – ($12,000)] ………………… 4,200

Nov. 1 Cash (1,200 X $1) ……………………………….. 1,200

Dividend Revenue ……………………….. 1,200

Dec. 15 Cash (2,400 X $.50) …………………………….. 1,200

Dividend Revenue ……………………….. 1,200

PROBLEM 16-3C (Continued)

(b) Dec. 31 Unrealized Gain or Loss—Equity

($96,000 – $90,000) …………………………….. 6,000

Fair Value Adjustment—Available-

for-Sale ……………………………………….. 6,000

Security

Cost

Fair Value

Apel Co. common

$48,000

$43,200

(2,400 X $18)

(c) Investments

Investment in stock of less than

20% owned companies, at fair

value …………………………………………. $ 90,000

Stockholders’ equity

Common stock ……………………………… $2,000,000

Retained earnings …………………………. 1,200,000

PROBLEM 16-4C

(a) 2017

Jan. 1 Stock Investments ………………………….. 1,350,000

Cash ……………………………………….. 1,350,000

31 Fair Value Adjustment—

Available-for-Sale ……………………….. 150,000

Unrealized Gain or Loss—Equity

[$1,350,000 – ($30 X 50,000)] …. 150,000

(b) 2017

Jan. 1 Stock Investments ………………………….. 1,350,000

Cash ……………………………………….. 1,350,000

PROBLEM 16-4C (Continued)

(c)

Cost

Method

Equity

Method

Stock Investments

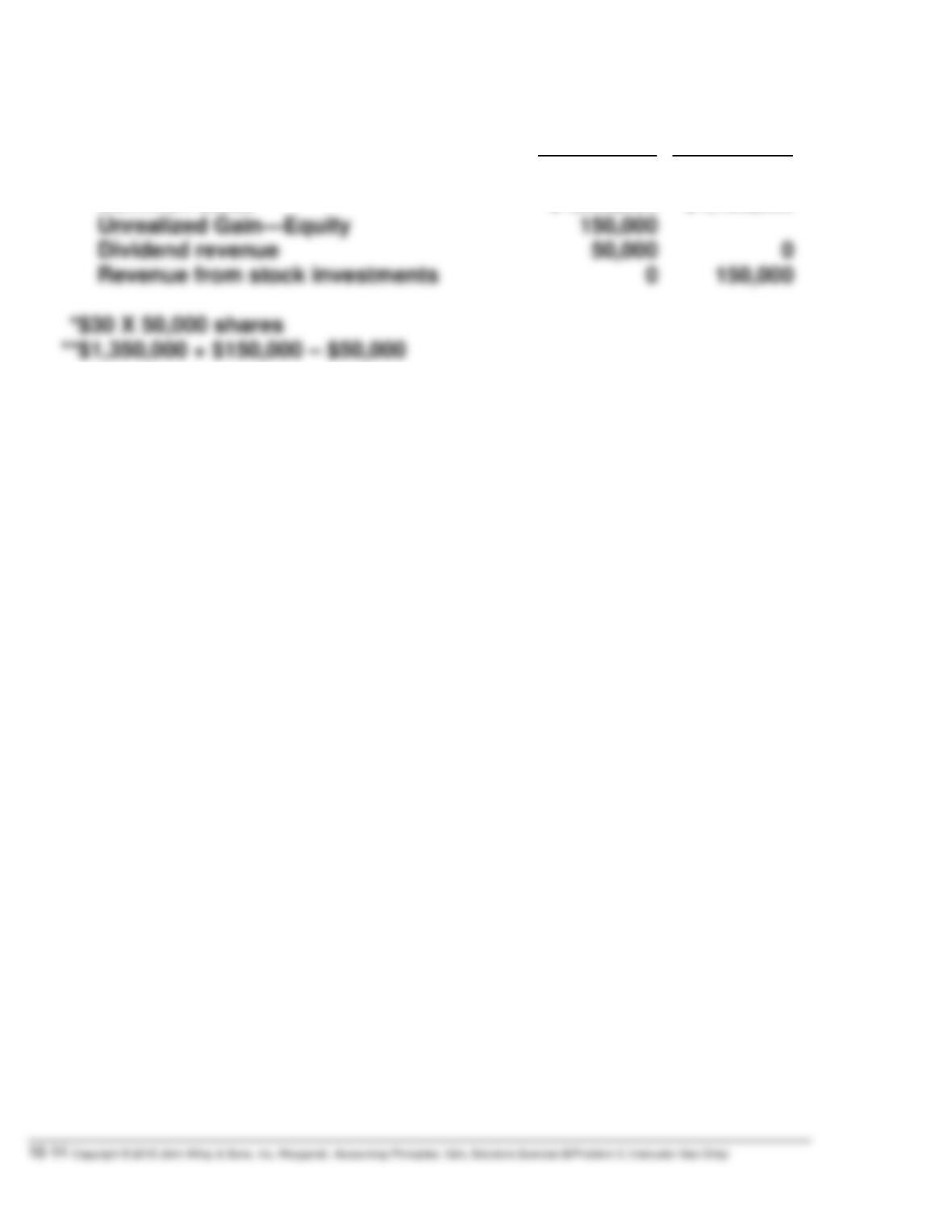

Common stock

Unrealized Gain—Equity

$1,500,000

150,000

*

$1,450,000

**

PROBLEM 16-5C

(a) Jan. 7 Cash ………………………………………………….. 28,000

Stock Investments ………………………… 26,000

Gain on Sale of Stock

Investments ………………………………. 2,000

10 Stock Investments ……………………………….. 15,600

Cash (200 X $78) …………………………... 15,600

10 Cash ($26 X 600) ………………………………….. 15,600

Loss on Sale of Stock Investments ……….. 1,200

Stock Investments ………………………… 16,800

July 1 Cash …………………………………………………… 700

Dividend Revenue

($1.00 X 700) ……………………………… 700

(b)

Stock Investments

1/1 Bal. 84,800

1/7 26,000

1/10 15,600

2/10 16,800

PROBLEM 16-5C (Continued)

(c) Dec. 31 Unrealized Gain or Loss—Equity ………………. 900

Fair Value Adjustment—Available-

Security

Cost

Fair Value

Penn Corporation common

$ 42,000

$ 44,100

(700 X $63)

(d) Investments

Investment in stock of less than 20% owned

companies, at fair value ……………………………………… $101,700

Stockholders’ equity

Total paid-in capital and retained earnings ……………… xxxxx

PROBLEM 16-6C

NIETO CORPORATION

Balance Sheet

December 31, 2017

Assets

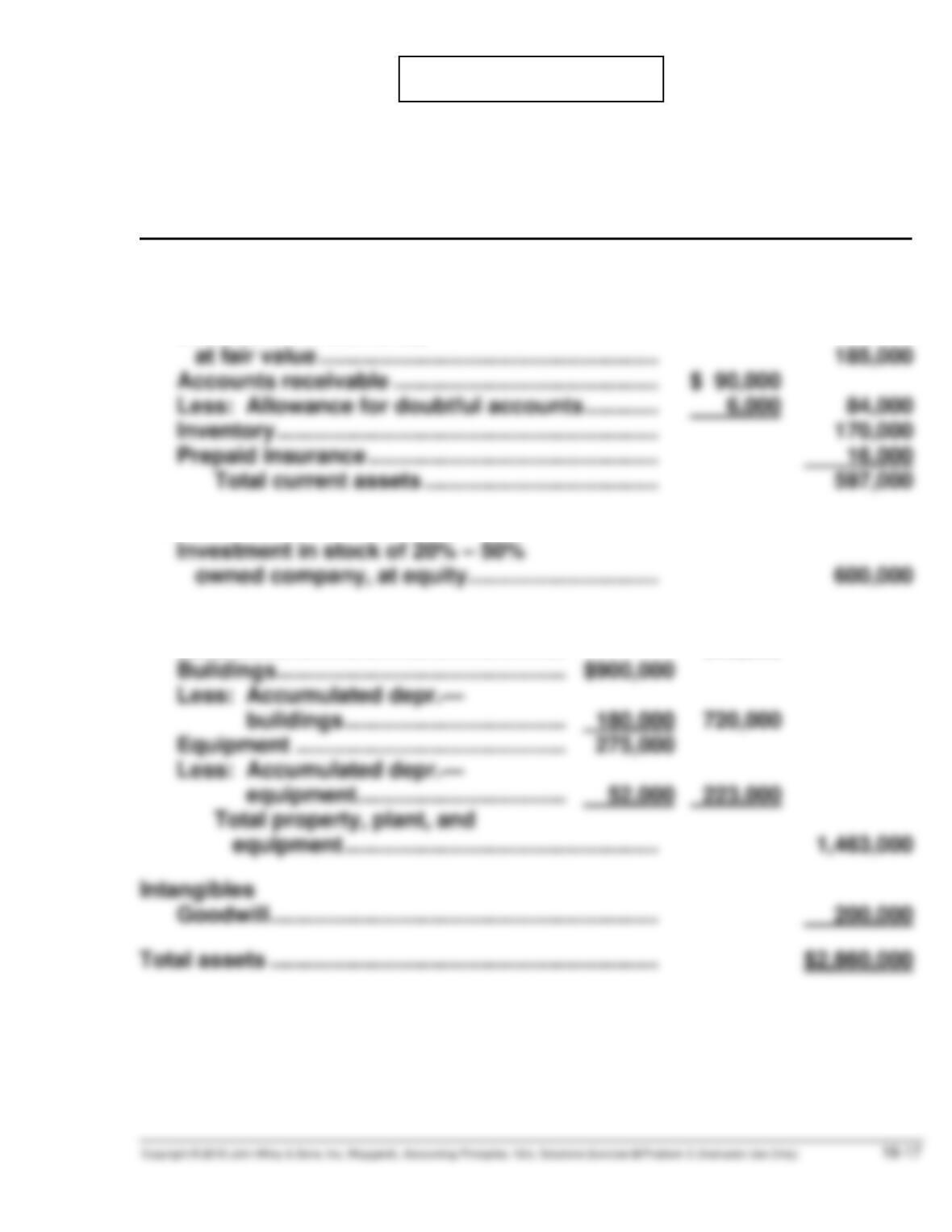

Current assets

Cash …………………………………………………………… $ 142,000

Short-term investments,

at fair value …………………………..………………….. 185,000

Accounts receivable ……………………………………. $ 90,000

Investments

Investment in stock of 20% – 50%

owned company, at equity …………………………. 600,000

Property, plant, and equipment

Land ……………………………………………… 520,000

Buildings …………………………..…………… $900,000

Less: Accumulated depr.—

Intangibles

Goodwill ……………………………………………………… 200,000

Total assets …………………………..…………………………. $2,860,000

PROBLEM 16-6C (Continued)

NIETO CORPORATION

Balance Sheet (Continued)

December 31, 2017

Liabilities and Stockholders’ Equity

Current liabilities

Notes payable …………………………………………. $ 70,000

Accounts payable ……………………………………. 250,000

Long-term liabilities

Bonds payable, 10%, due 2025 …………………. $ 400,000

Less: Discount on bonds payable ……………. 20,000

Stockholders’ equity

Paid-in capital

Common stock, $5 par value,

500,000 shares authorized,

300,000 shares issued and

outstanding …………………………………… 1,500,000

In excess of par—common stock ……….. 200,000