Prob. 18–2A (FINMAN); Prob. 3–2A (MAN)

1.

Whole Direct

UNITS Units Materials Conversion

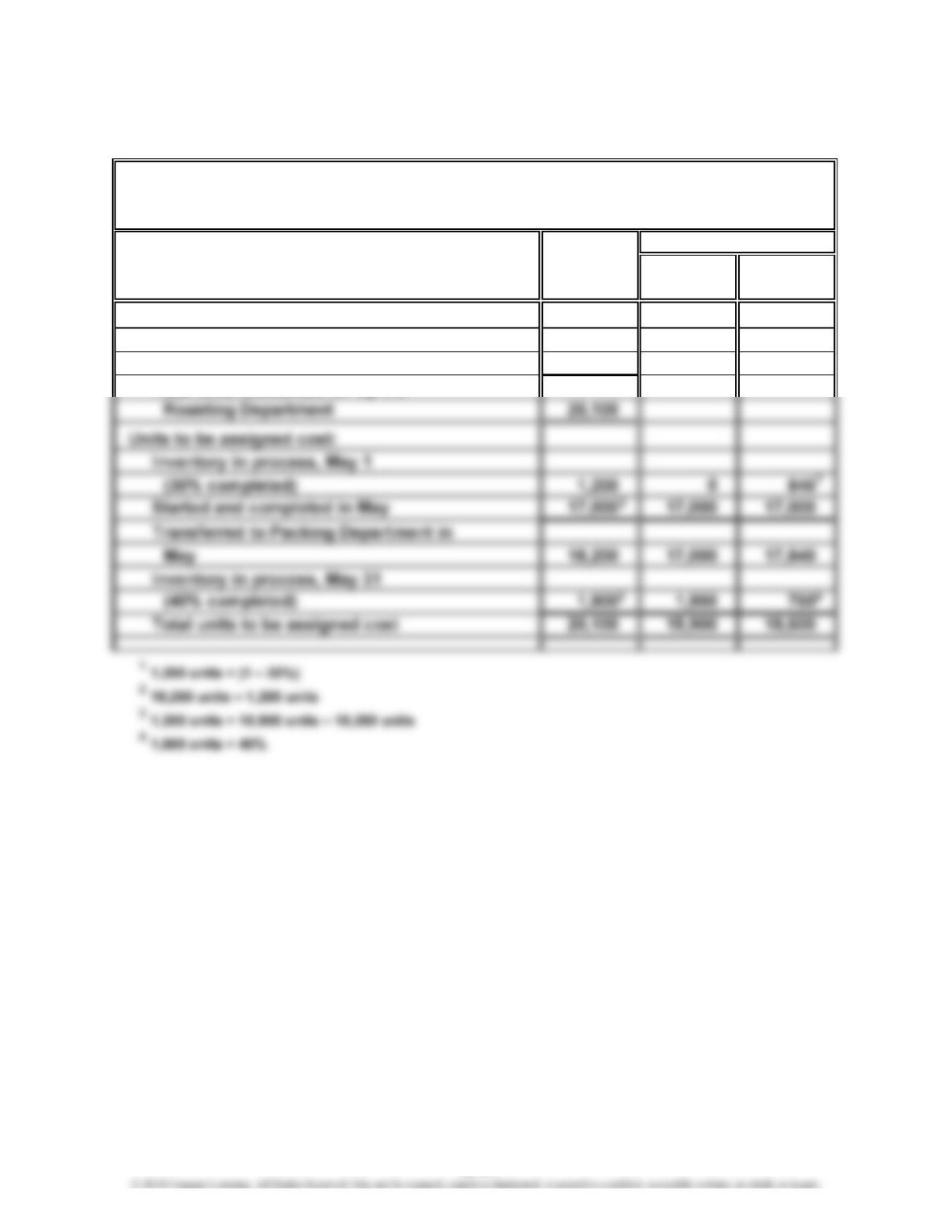

Units charged to production:

Inventory in process, May 1 1,200

Received from materials storeroom 18,900

Total units accounted for by the

ABICA COFFEE COMPANY

Cost of Production Report—Roasting Department

For the Month Ended May 31, 2014

Equivalent Units

18-41

Prob. 18–2A (FINMAN); Prob. 3–2A (MAN) (Continued)

Direct

COSTS Materials Conversion Total

Costs per equivalent unit:

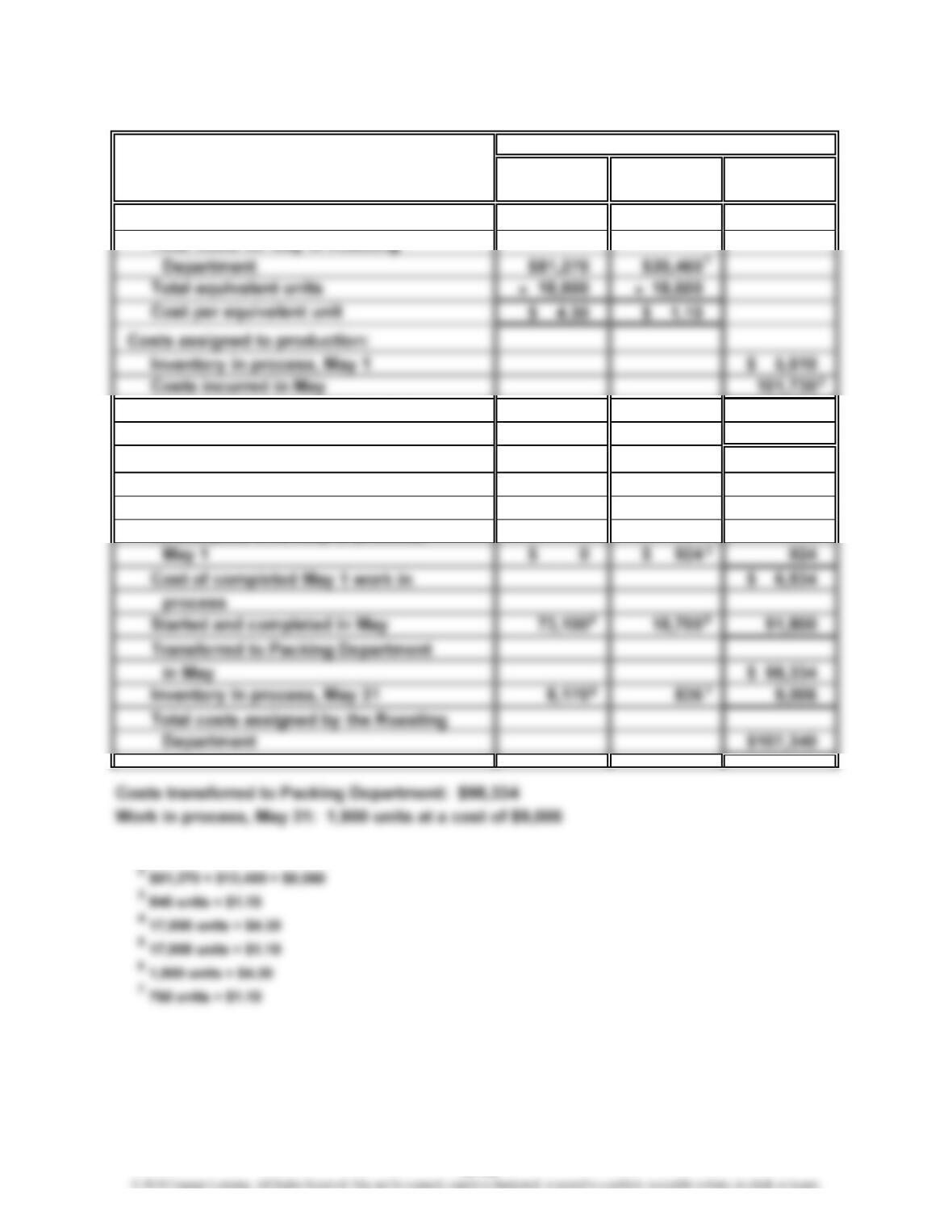

Total costs for May in Roasting

Total costs accounted for by the

Roasting Department $107,340

Cost allocated to completed and

partially completed units:

Inventory in process, May 1 balance $ 5,610

To complete inventory in process,

1$12,400 + $8,060

Costs

18-42

Prob. 18–2A (FINMAN); Prob. 3–2A (MAN) (Concluded)

Computations:

18-43

Prob. 18–3A (FINMAN); Prob. 3–3A (MAN)

1.

Whole Direct

UNITS Units Materials Conversion

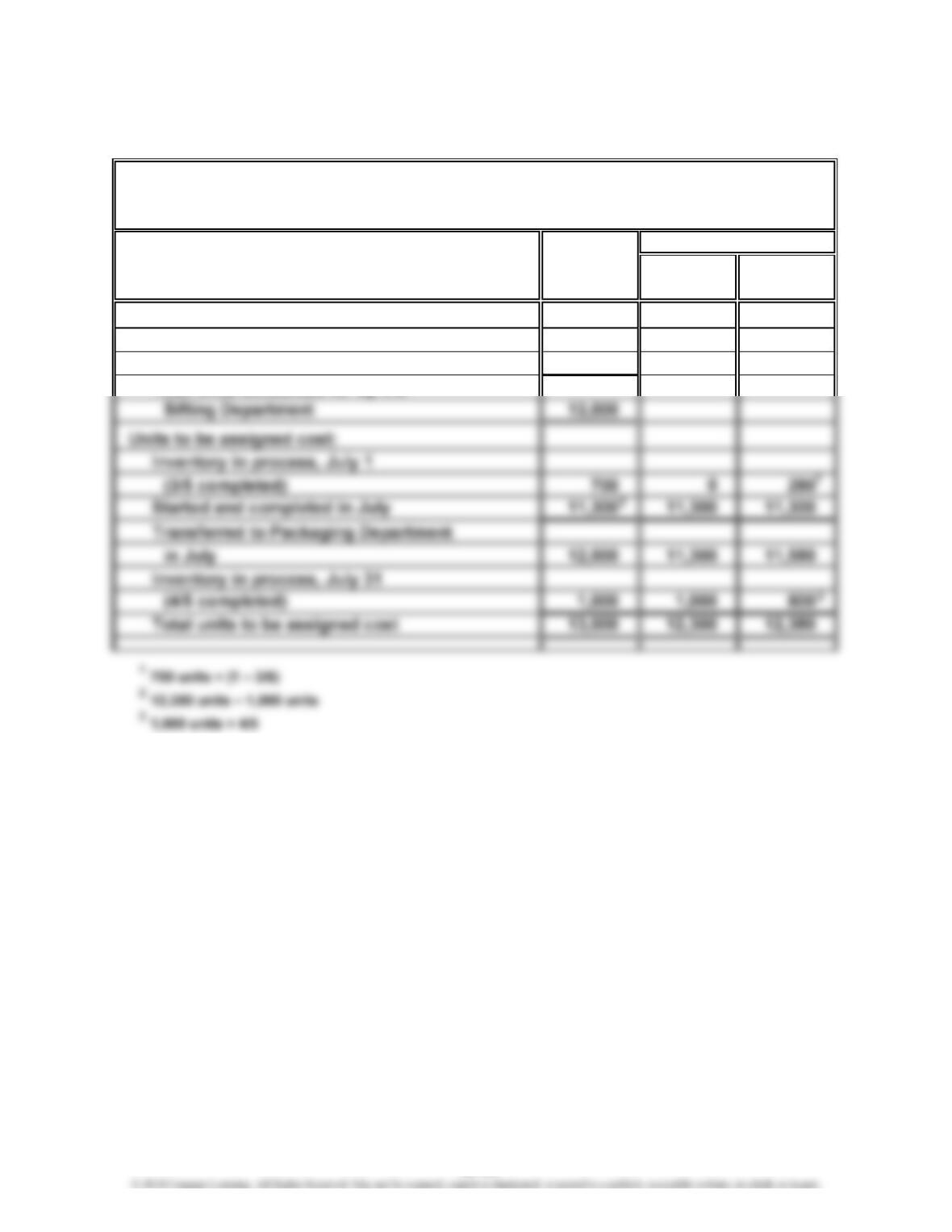

Units charged to production:

Inventory in process, July 1 700

Received from Milling Department 12,300

Total units accounted for by the

LILY FLOUR COMPANY

Cost of Production Report—Sifting Department

For the Month Ended July 31, 2014

Equivalent Units

18-44

Prob. 18–3A (FINMAN); Prob. 3–3A (MAN) (Continued)

Direct

COSTS Materials Conversion Total

Costs per equivalent unit:

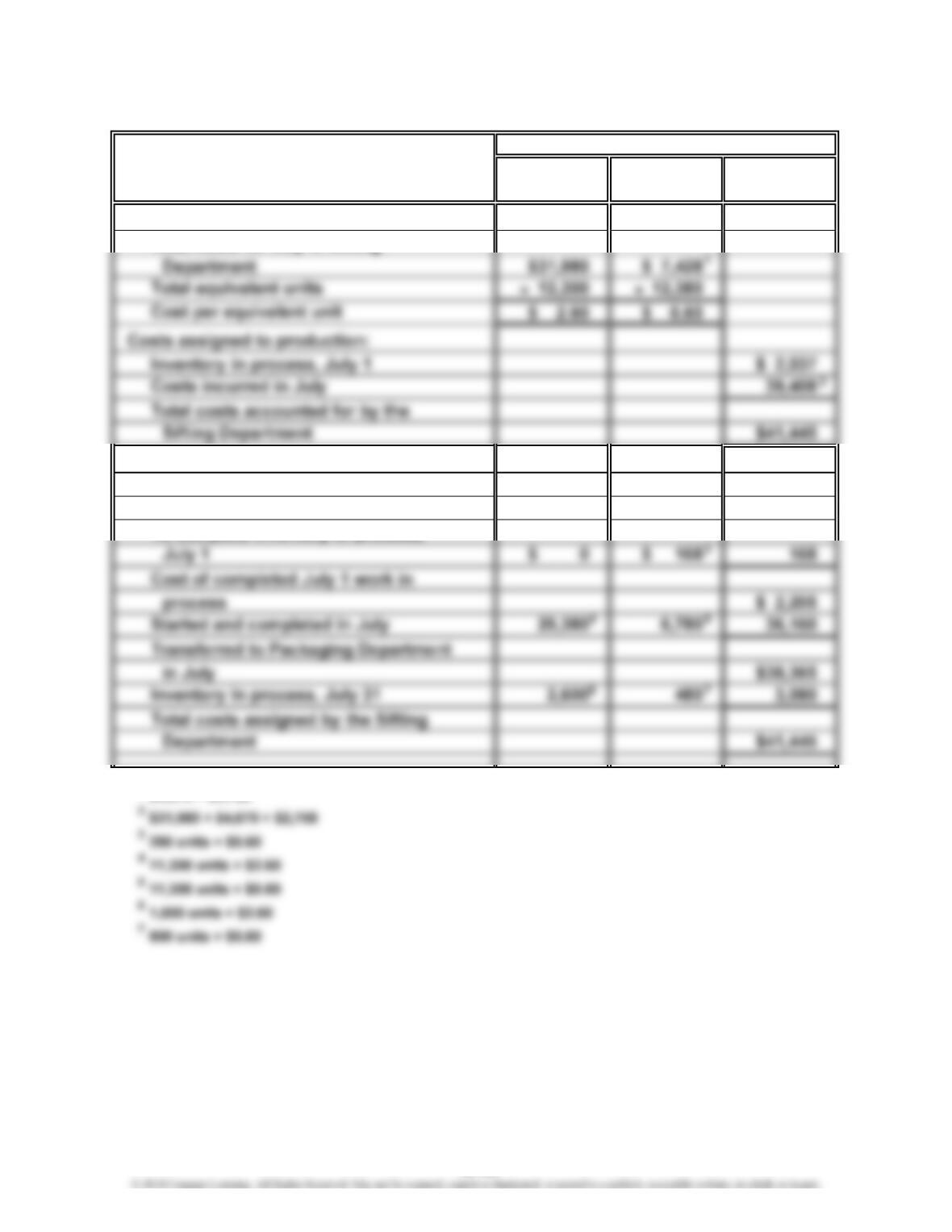

Total costs for July in Sifting

Cost allocated to completed and

partially completed units:

Inventory in process, July 1 balance $ 2,037

To complete inventory in process,

1$4,670 + $2,758

Costs

18-45

Prob. 18–3A (FINMAN); Prob. 3–3A (MAN) (Concluded)

2. Work in Process—Sifting Department 31,980

4. The cost of production report may be used as the basis for allocating product

costs between Work in Process and Transferred-Out (or Finished) Goods. The

18-46

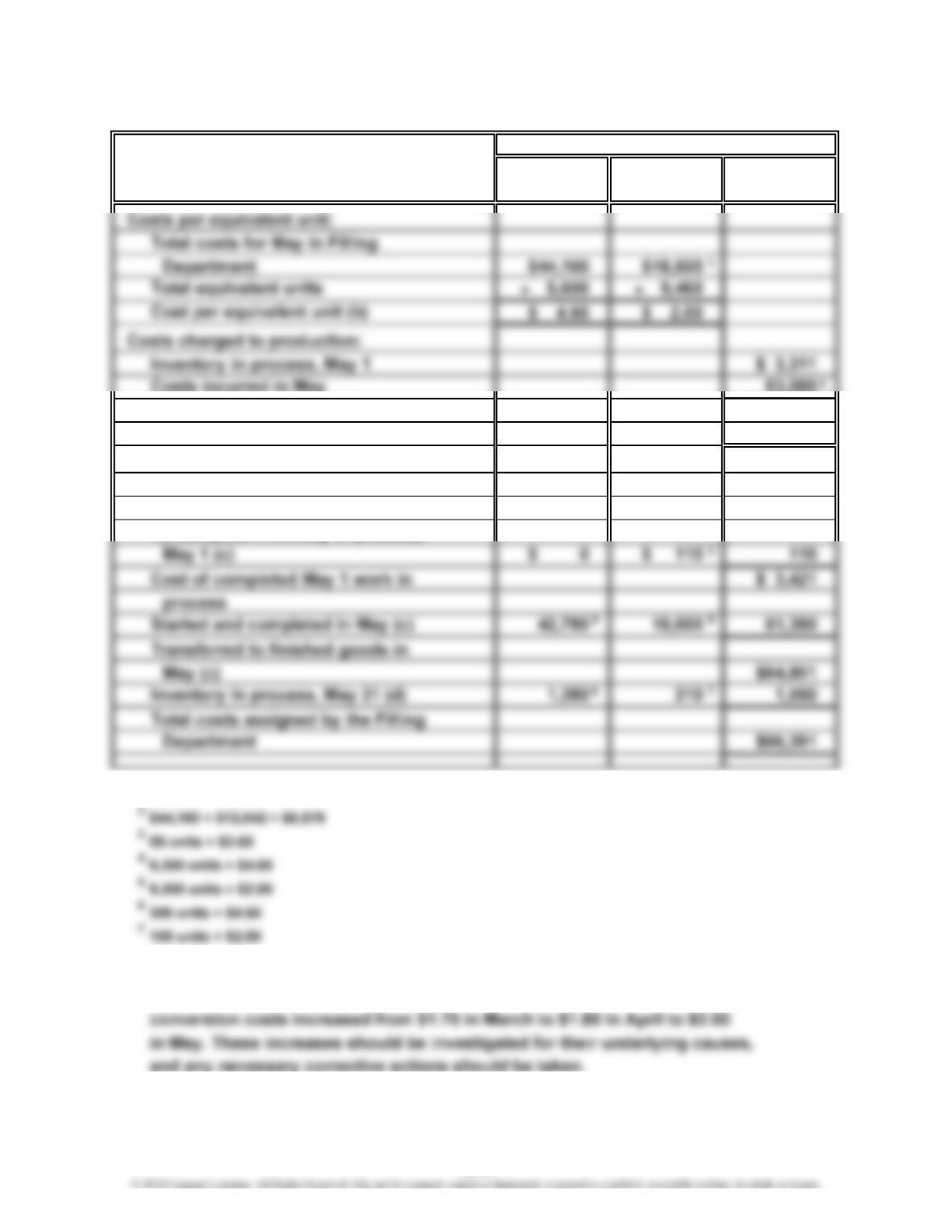

Prob. 18–4A (FINMAN); Prob. 3–4A (MAN)

1. and 2.

Item Dr. Cr. Dr. Cr.

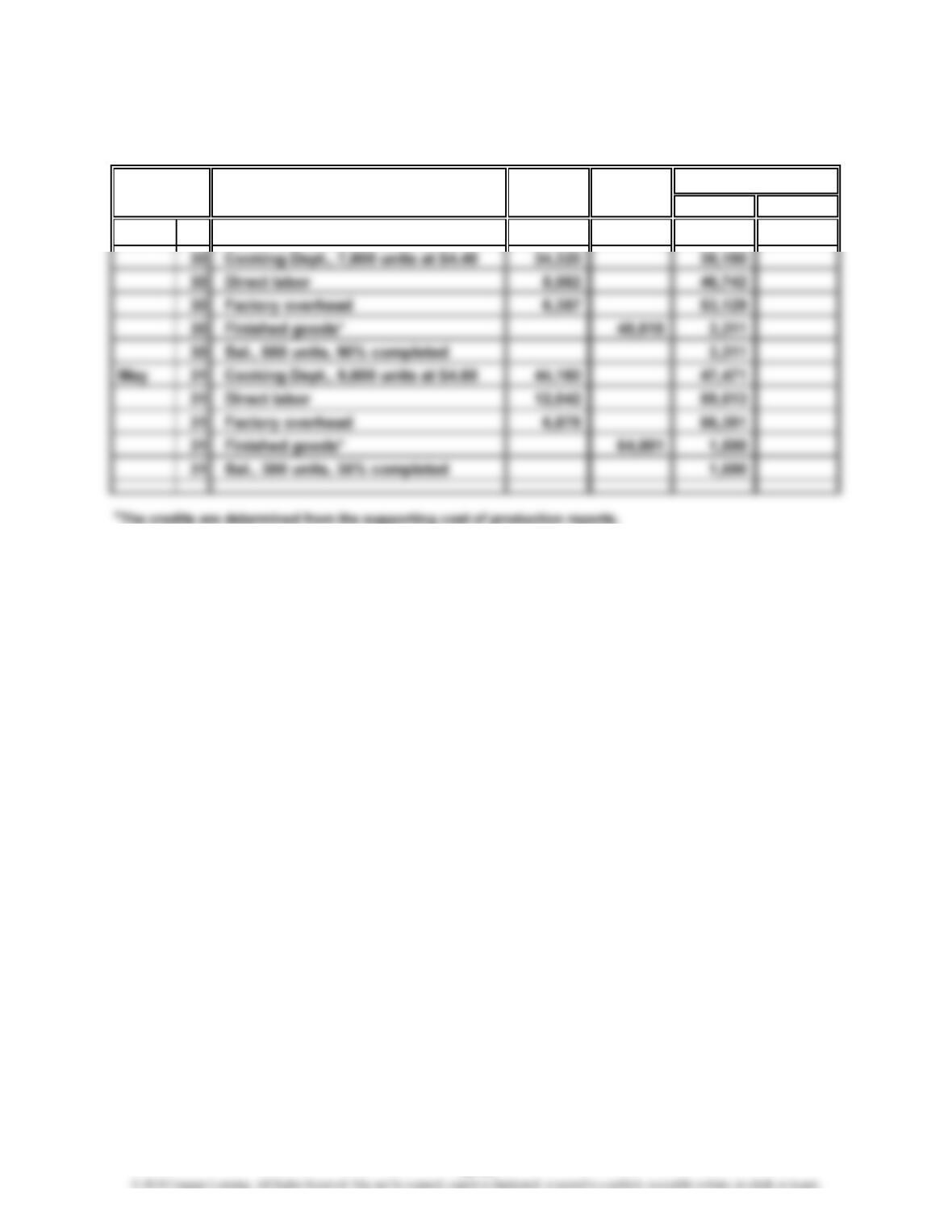

Apr. 1 Bal., 800 units, 30% completed 3,860

Date

Balance

Work in Process—Filling

18-47

Prob. 18–4A (FINMAN); Prob. 3–4A (MAN) (Continued)

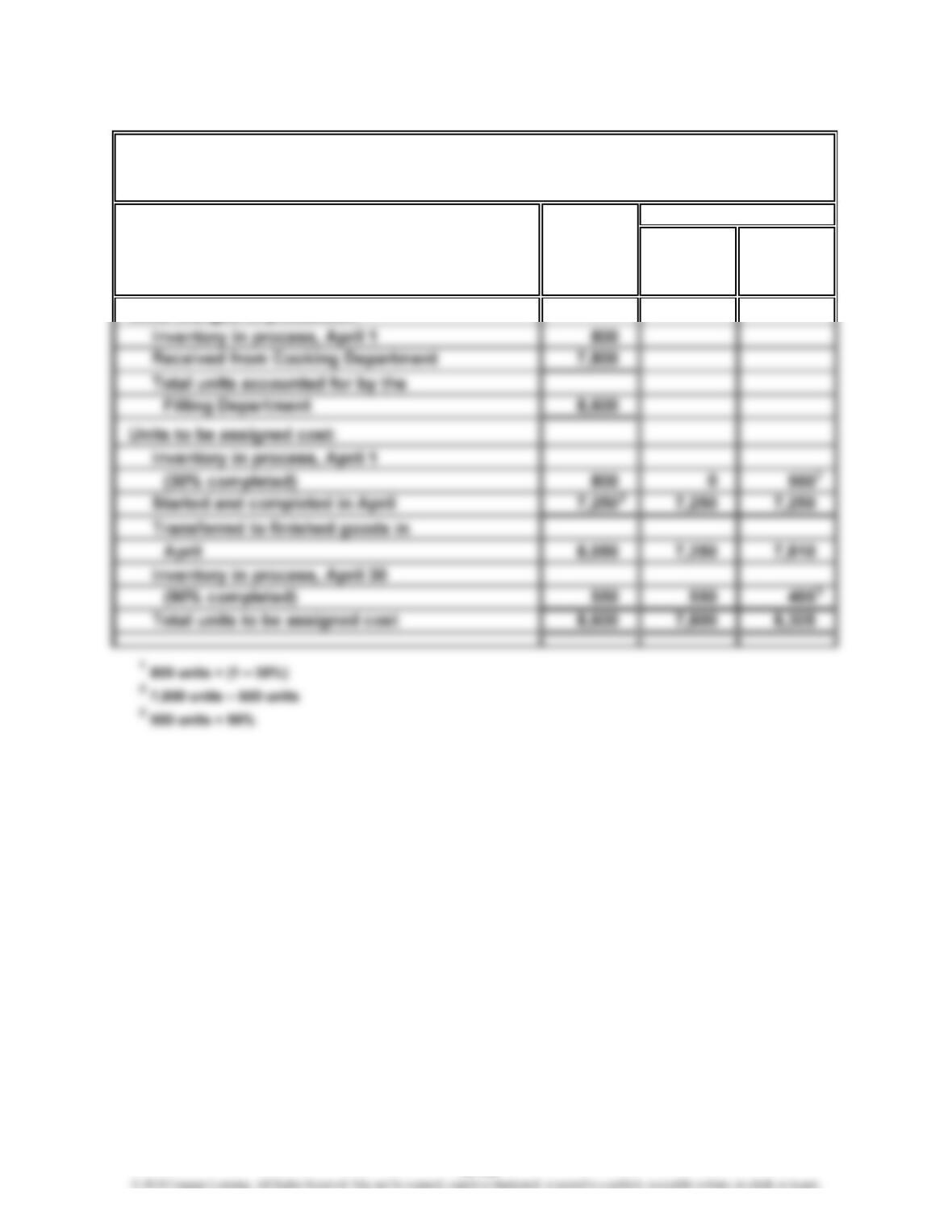

Whole Direct

UNITS Units Materials Conversion

(a) (a)

Units charged to production:

HEARTY SOUP CO.

Cost of Production Report—Filling Department

For the Month Ended April 30, 2014

Equivalent Units

18-48

Prob. 18–4A (FINMAN); Prob. 3–4A (MAN) (Continued)

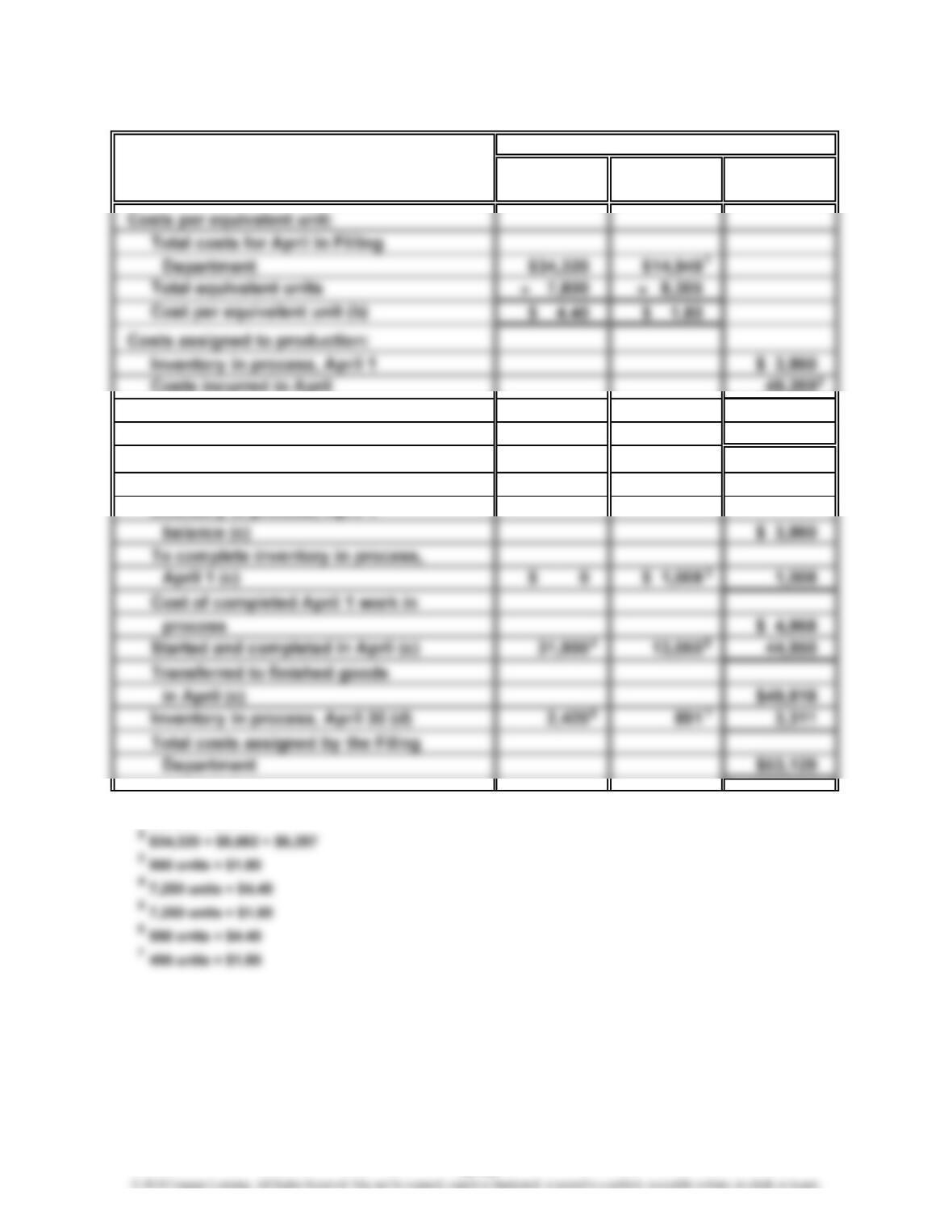

Direct

COSTS Materials Conversion Total

Total costs accounted for by the

Filling Department $53,129

Cost allocated to completed and

partially completed units:

Inventory in process, April 1

1$8,562 + $6,387

Costs

18-49

Prob. 18–4A (FINMAN); Prob. 3–4A (MAN) (Continued)

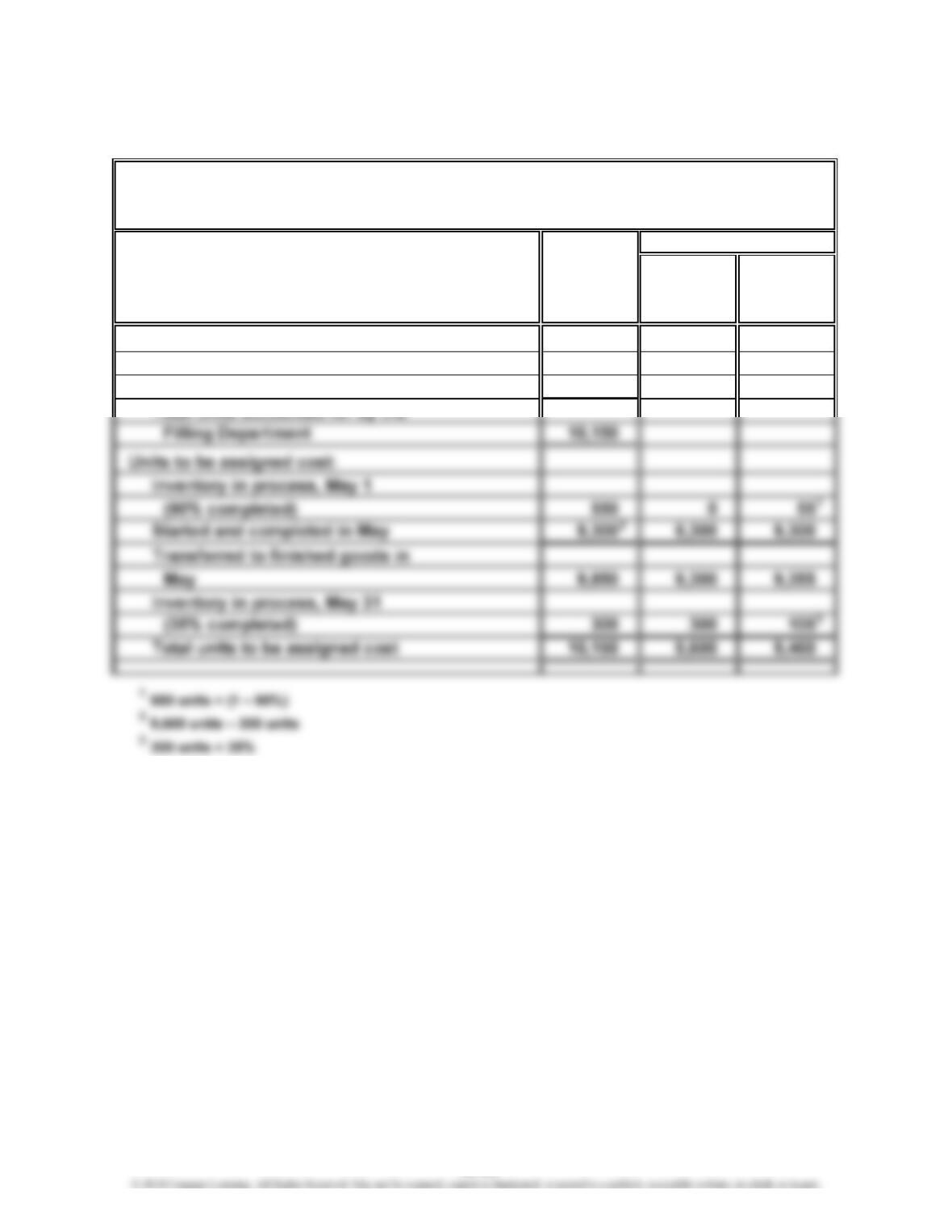

2.

Whole Direct

UNITS Units Materials Conversion

(a) (a)

Units charged to production:

Inventory in process, May 1 550

Received from Cooking Department 9,600

HEARTY SOUP CO.

Cost of Production Report—Filling Department

For the Month Ended May 31, 2014

Equivalent Units

18-50

Prob. 18–4A (FINMAN); Prob. 3–4A (MAN) (Concluded)

Direct

COSTS Materials Conversion Total

Total costs accounted for by the

Filling Department $66,391

Cost allocated to completed and

partially completed units:

Inventory in process, May 1 balance (c) $ 3,311

To complete inventory in process,

1$12,042 + $6,878

3. The cost per equivalent unit for direct materials increased from $4.30 in March

to $4.40 in April to $4.60 in May. Similarly, the cost per equivalent unit for

Costs

18-51

Appendix Prob. 18–5A (FINMAN); Appendix Prob. 3–5A (MAN)

Whole Equivalent Units

UNITS Units of Production

Units to account for during production:

COSTS

Unit costs:

Total costs for December in Roasting Department $572,130

Inventory in process, December 31

SUNRISE COFFEE COMPANY

Cost of Production Report—Roasting Department

For the Month Ended December 31, 2014

18-52

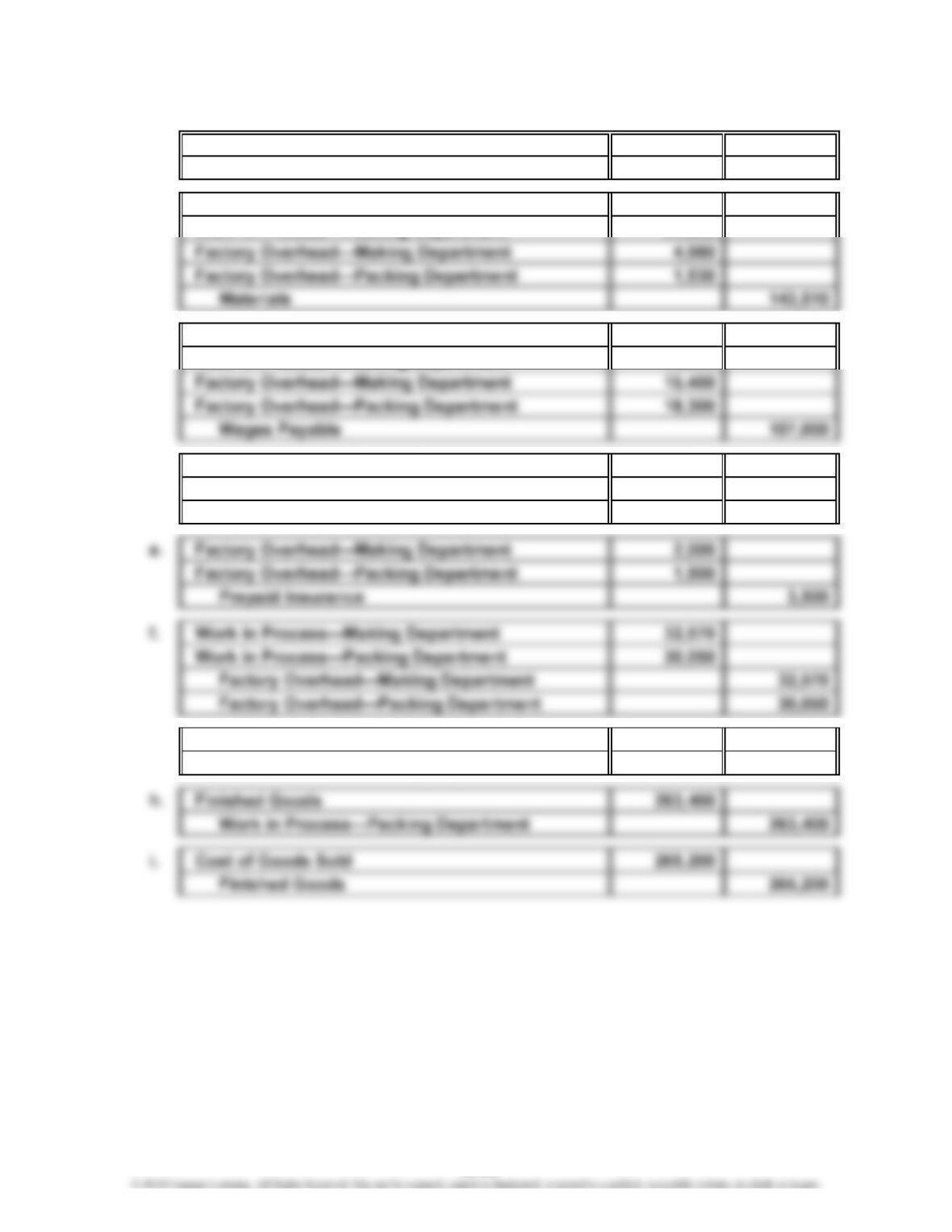

Prob. 18–1B (FINMAN); Prob. 3–1B (MAN)

1. a. Materials 149,800

Accounts Payable 149,800

b. Work in Process—Making Department 105,700

Work in Process—Packing Department 31,300

c. Work in Process—Making Department 32,400

Work in Process—Packing Department 40,900

d. Factory Overhead—Making Department 10,700

Factory Overhead—Packing Department 7,900

Accumulated Depreciation 18,600

g. Work in Process—Packing Department 166,790

Work in Process—Making Department 166,790

18-53

Prob. 18–1B (FINMAN); Prob. 3–1B (MAN) (Concluded)

2. Work in Work in

Process— Process— Finished

Materials Making Dept. Packing Dept. Goods

Balance, July 1……

…

$ 5,100 $ 6,790 $ 7,350 $ 13,500

3.

Balance, July 1……

…

$0 $0

Factory Overhead— Factory Overhead—

Making Dept. Packing Dept.

18-54

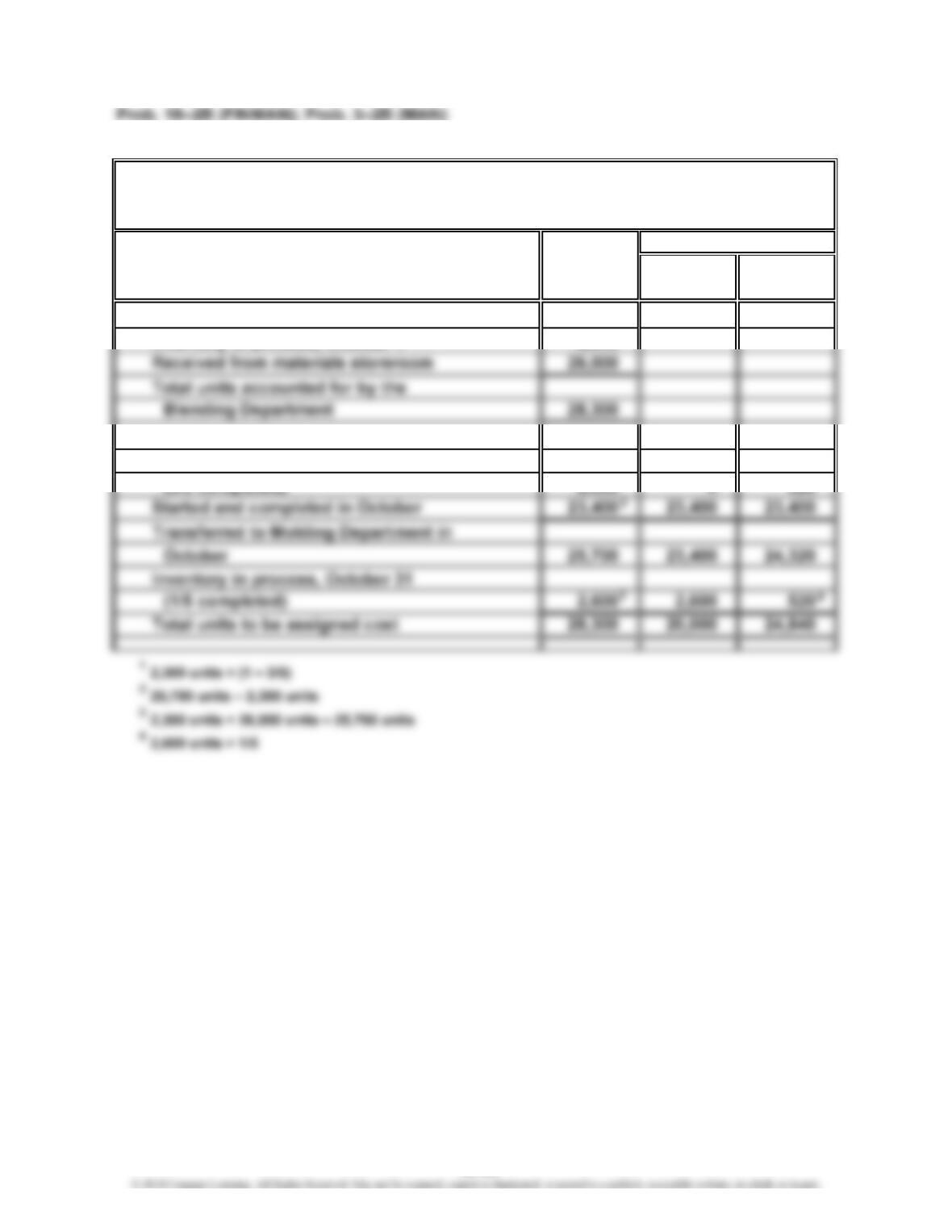

1.

Whole Direct

UNITS Units Materials Conversion

Units charged to production:

Inventory in process, October 1 2,300

Units to be assigned cost:

Inventory in process, October 1

(3/5 completed) 2,300 0920

BAVARIAN CHOCOLATE COMPANY

Cost of Production Report—Blending Department

For the Month Ended October 31, 2014

Equivalent Units

1

18-55

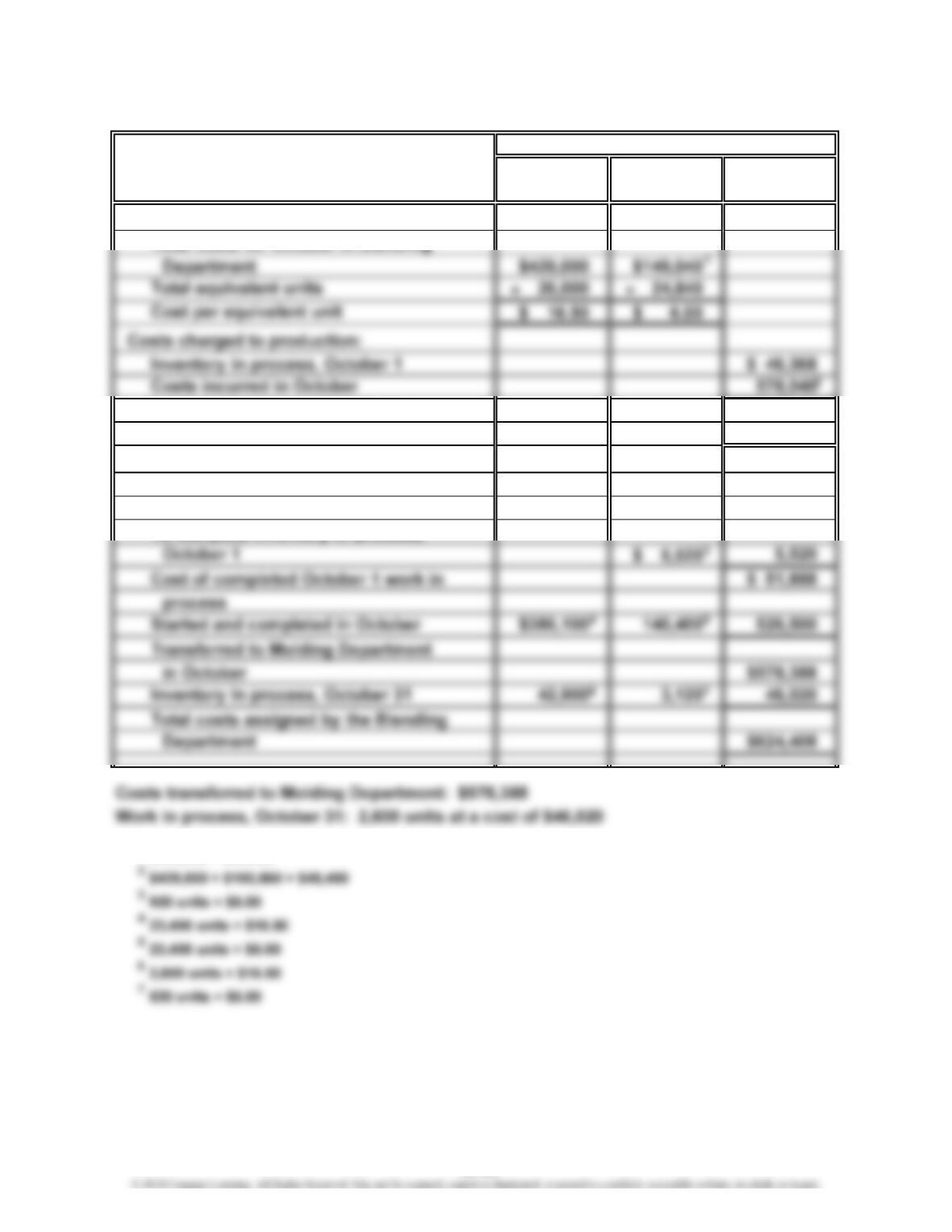

Prob. 18–2B (FINMAN); Prob. 3–2B (MAN) (Continued)

Direct

COSTS Materials Conversion Total

Costs per equivalent unit:

Total costs for October in Blending

Total costs accounted for by the

Blending Department $624,408

Cost allocated to completed and

partially completed units:

Inventory in process, October 1 balance $ 46,368

To complete inventory in process,

1$100,560 + $48,480

Costs

18-56

Prob. 18–2B (FINMAN); Prob. 3–2B (MAN) (Concluded)

Computations:

18-57