CHAPTER 16 Statement of Cash Flows

Prob. 16-2B (Concluded)

Appendix 1 (Optional)

Balance, Balance,

Account Title Dec. 31, 20Y3 Dec. 31, 20Y4

Operating activities:

and equipment (j) 22,680

Amortization of patents (i) 5,040

Increase in accounts

receivable (o) 73,080

Decrease in inventories (n) 134,680

Increase in prepaid expenses (m) 6,440

Investing activities:

Construction of building (l) 579,600

Financial activities:

Declaration of cash dividends (b) 131,040

Issuance of mortgage note

payable (e) 224,000

Increase in dividends payable (g) 7,560

Debit Credit

Harris Industries Inc.

Spreadsheet (Work Sheet) for Statement of Cash Flows

For the Year Ended December 31, 20Y4

Transactions

CHAPTER 16 Statement of Cash Flows

Prob. 16-3B

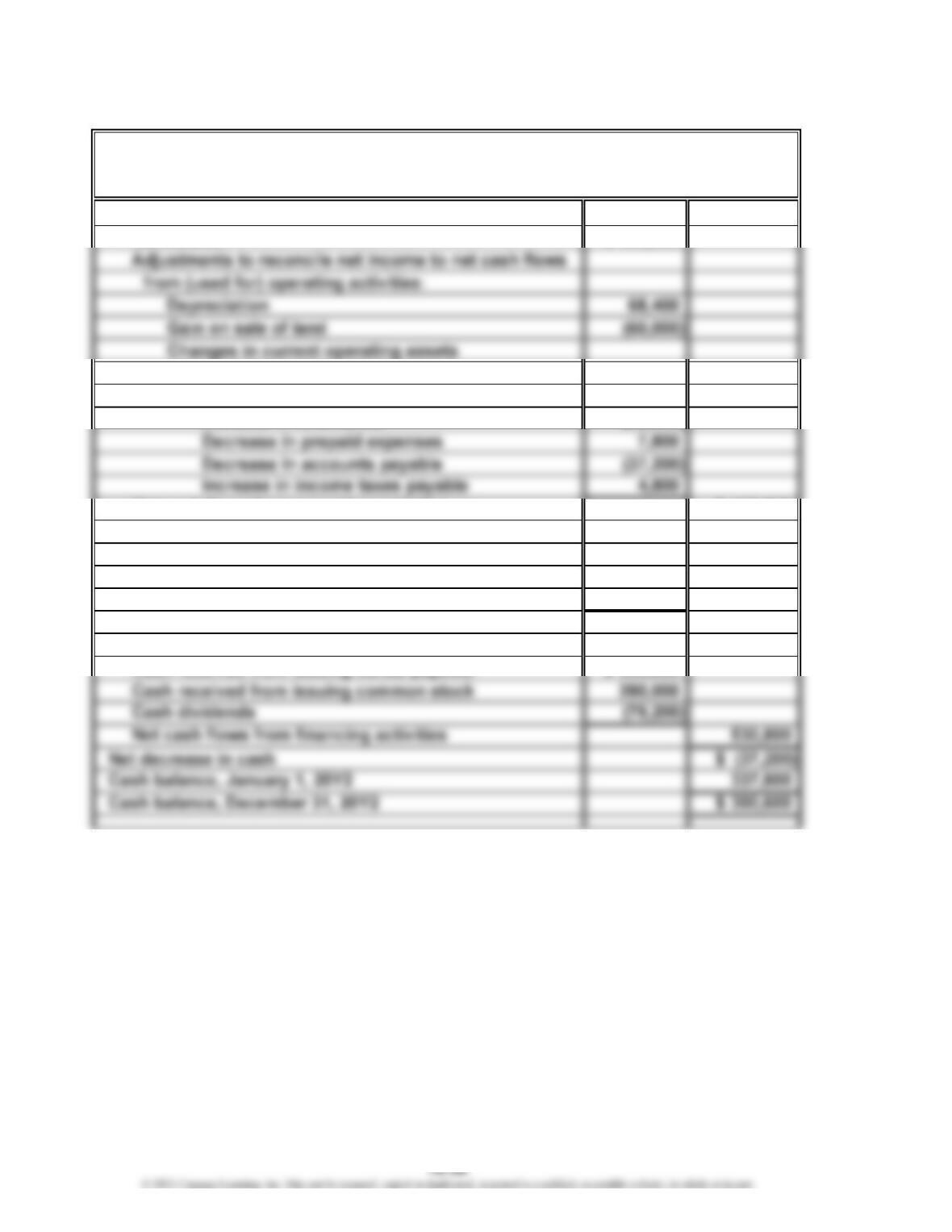

Cash flows from (used for) operating activities:

Net income $ 326,600

and liabilities:

Increase in accounts receivable (94,800)

Increase in inventories (52,800)

Net cash flows from operating activities $ 162,800

Cash flows from (used for) investing activities:

Cash received from sale of land $ 456,000

Cash paid for acquisition of building (990,000)

Cash paid for purchase of equipment (196,800)

Net cash flows used for investing activities (730,800)

Cash flows from (used for) financing activities:

For the Year Ended December 31, 20Y2

Coulson, Inc.

Statement of Cash Flows

CHAPTER 16 Statement of Cash Flows

Prob. 16-3B (Concluded)

Appendix 1 (Optional)

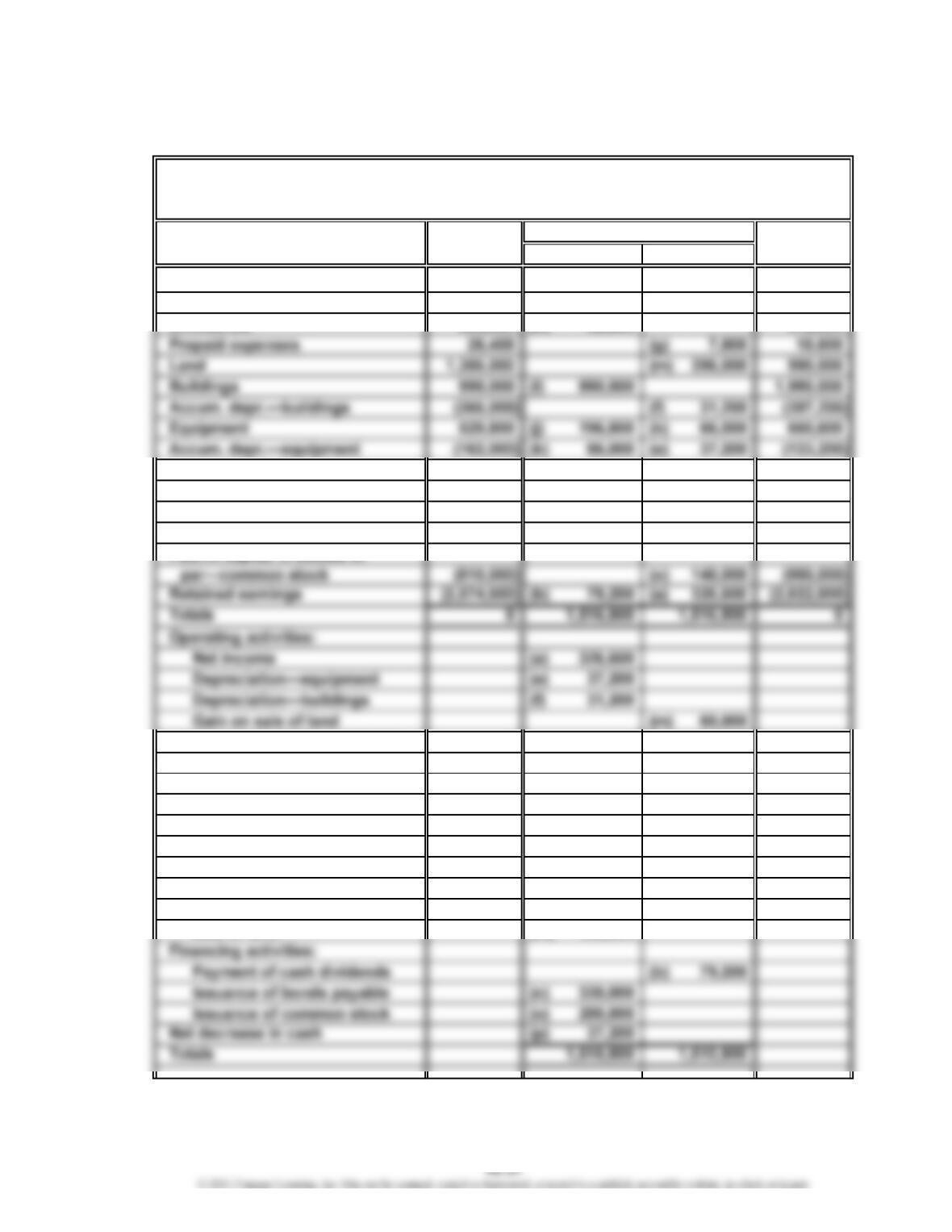

Balance, Balance,

Account Title Dec. 31, 20Y1 Dec. 31, 20Y2

Cash 337,800 (p) 37,200 300,600

Accounts receivable (net) 609,600 (i) 94,800 704,400

Accounts payable (631,200) (d) 37,200 (594,000)

Income taxes payable (21,600) (c) 4,800 (26,400)

Bonds payable — (n) 330,000 (330,000)

Common stock, $20 par (180,000) (o) 140,000 (320,000)

Increase in accts. receivable (i) 94,800

Increase in inventories (h) 52,800

Decrease in prepaid expenses (g) 7,800

Decrease in accounts payable (d) 37,200

Increase in income taxes

payable (c) 4,800

Investing activities:

Purchase of equipment (j) 196,800

Acquisition of building (l) 990,000

Sale of land (m) 456,000

Debit Credit

Coulson, Inc.

Spreadsheet (Work Sheet) for Statement of Cash Flows

For the Year Ended December 31, 20Y2

Transactions

CHAPTER 16 Statement of Cash Flows

Appendix 2 Prob. 16-4B

Cash flows from (used for) operating activities:

Cash received from customers1$ 5,293,500

Cash flows from (used for) investing activities:

Cash received from sale of investments $ 702,000

Cash paid for land (1,146,100)

Cash paid for equipment (286,500)

Net cash flows used for investing activities (730,600)

Cash flows from (used for) financing activities:

Cash received from issuing common stock $ 716,300

Cash dividends* (619,000)

Schedule Reconciling Net Income with Net Cash Flows from Operating Activities:

Cash flows from (used for) operating activities:

Net income……………………………………………………………………

…

$ 667,290

Adjustments to reconcile net income to net cash flows

from (used for) operating activities:

Depreciation expense…………………………………………………

…

135,000

Gain on sale of investments…………………………………………

…

(186,200)

Changes in current operating assets and liabilities:

For the Year Ended December 31, 20Y4

Suffridge Inc.

Statement of Cash Flows

CHAPTER 16 Statement of Cash Flows

Appendix 2 Prob. 16-4B (Concluded)

Computations:

1. Sales………………………………………………………………………… $5,386,900

Increase in accounts receivable………………………………………

…

(93,400)

Cash received from customers………………………………………… $5,293,500

3. Operating expenses other than depreciation………………………

…

$1,605,610

Decrease in accrued expenses payable………………………………

…

13,700

Cash paid for operating expenses……………………………………

…

$1,619,310

CHAPTER 16 Statement of Cash Flows

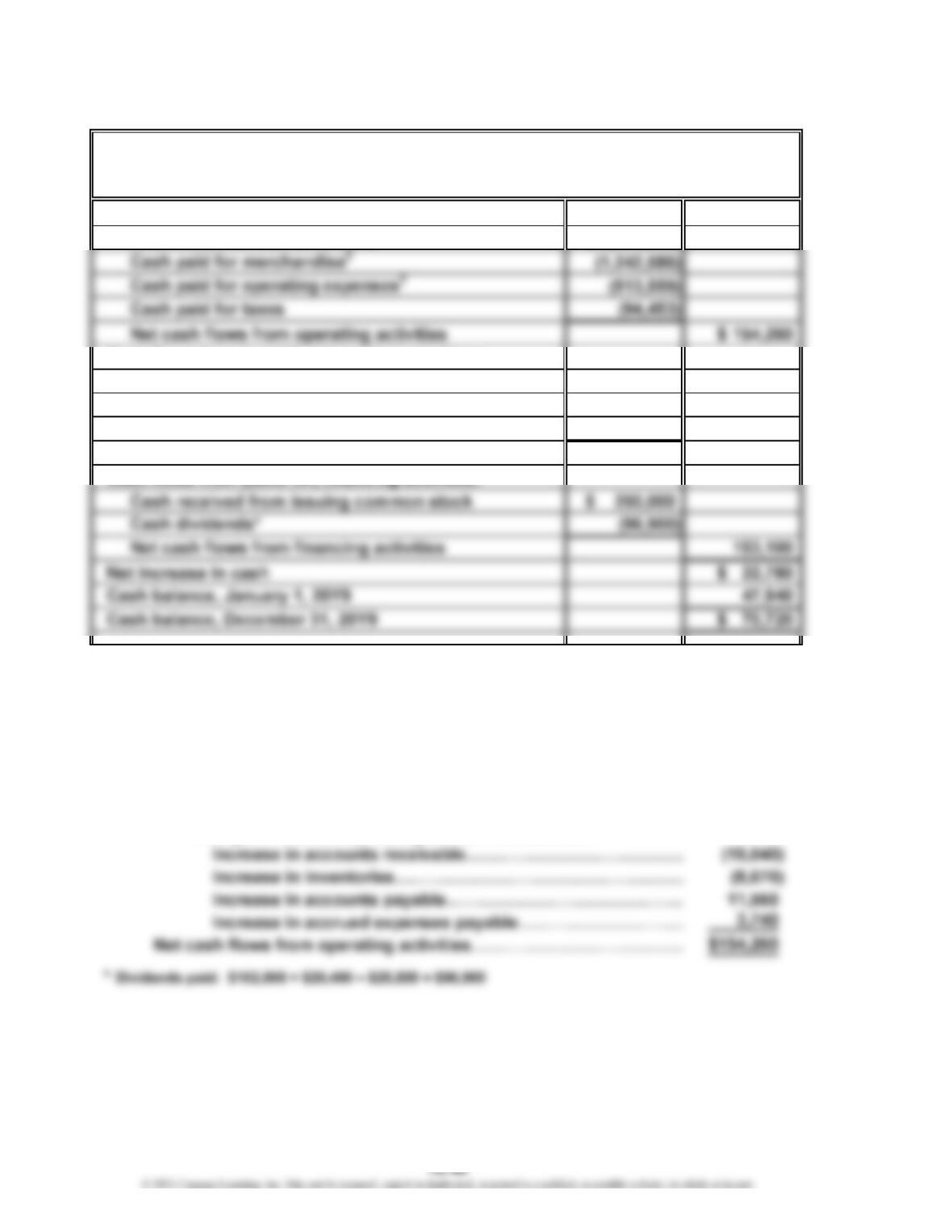

Appendix 2 Prob. 16-5B

Cash flows from (used for) operating activities:

Cash received from customers1$ 2,004,858

Cash flows from (used for) investing activities:

Cash received from sale of investments $ 91,800

Cash paid for purchase of land (295,800)

Cash paid for purchase of equipment (80,580)

Net cash flows used for investing activities (284,580)

Schedule Reconciling Net Income with Net Cash Flows from Operating Activities:

Cash flows from (used for) operating activities:

Net income……………………………………………………………………

…

$141,680

Adjustments to reconcile net income to net cash flows

from (used for) operating activities:

Depreciation……………………………………………………………

…

14,790

Loss on sale of investments………………………………………… 10,200

Changes in current operating assets and liabilities:

For the Year Ended December 31, 20Y9

Merrick Equipment Co.

Statement of Cash Flows

CHAPTER 16 Statement of Cash Flows

Appendix 2 Prob. 16-5B (Concluded)

Computations:

2. Cost of merchandise sold…………………………………………………… $1,245,476

Increase in inventories………………………………………………………

…

8,670

Increase in accounts payable………………………………………………

…

(11,560)

Cash paid for merchandise…………………………………………………

…

$1,242,586

CHAPTER 16 Statement of Cash Flows

CP 16-1

Although this situation might seem harmless at first, it is, in fact, a violation of

generally accepted accounting principles. The operating cash flow per share figure

should not be shown on the face of the income statement. The income statement is

constructed under accrual accounting concepts, and operating cash flow fiundoes”

the accounting accruals. Thus, unlike Lucas’s assertion that this information would be

useful, more likely the information would be confusing to users. Some users might not

be able to distinguish between earnings and operating cash flow per share—or how to

interpret the difference. By agreeing with Lucas, John has breached his professional

CP 16-2

A sample solution based on Nike Inc.’s Form 10-K for the fiscal year ended May 31, 2018,

follows:

1. a. $4,955 million

b. $276 million

c. $(4,835) million

d. $441 million*

CASES & PROJECTS

CHAPTER 16 Statement of Cash Flows

CP 16-3

Memo

To: My Instructor

From: A+ Student

Re: Tidewater Inc. Financial Condition

Tidewater Inc. is a retailer that has been unprofitable in recent years. While the company

has returned to profitability, there are several fired flags” indicating that the company’s

future prospects are highly uncertain. These red flags are discussed below.

•The company has initiated a new marketing campaign that significantly increased

the number of customers who are purchasing merchandise on credit using the

company’s branded credit card. This campaign significantly increased revenue

and has helped the company return to profitability. However, it appears that the

•The purchases of deeply discounted merchandise appear to be backfiring. The

company has received some figood deals” on price. However, the merchandise is

only a figood deal” if the company can resell the merchandise at a profit. The

•The company has not been able to pay off its accounts payable in a timely manner,

resulting in significant overdue accounts payable balances. While the company

reports that most of the past-due payables have been paid, it is concerning that

These red flags suggest that the company is having severe operating cash flow

difficulties, and the company’s future prospects are highly uncertain.

CHAPTER 16 Statement of Cash Flows

CP 16-4

Start-up companies are unique in that they frequently have negative retained

earnings and operating cash flows. The negative retained earnings are often due to

losses from high start-up expenses. The negative operating cash flows are typical

because growth requires cash. Growth must be financed with cash before the cash

returns. For example, a company must expend cash to provide the service in Period 1

before selling it and receiving cash in Period 2. The start-up company constantly faces

the problem of spending cash today for the next period’s growth. For Giraffe Inc., the

CP 16-5

a. 1. Normal practice for determining net cash flows from operating activities

during the year is to begin with the reported net income. This net income

must ordinarily be adjusted upward or downward to determine the amount of

cash flows. Although many operating expenses decrease cash, depreciation

does not. The amount of net income understates the amount of cash flows

2. Generally accepted accounting principles require that significant transactions

affecting future cash flows be reported in a separate schedule to the

statement even though they do not affect cash. Accordingly, even though the

3. The $180,000 cash received from the sale of the investments is reported in the

Cash Flows from (used for) Investing Activities section. Because the net income

CP 16-5 (Concluded)

4. The balance sheets for the last two years will indicate the increase in cash but

will not indicate the firm’s activities in meeting its financial obligations, paying

dividends, and maintaining and expanding operating capacity. Such information,

as provided by the statement of cash flows, assists creditors in assessing the

firm’s solvency and profitability—two very important factors impacting the

evaluation of a potential loan.

CP 16-6

a. and b.

Recent statements of cash flows for Johnson & Johnson and JetBlue Airways Corp. are

shown on the following pages. The actual analysis may be different due to updated

information. However, this answer shows the structure for a possible response.

Johnson & Johnson

Johnson & Johnson (J&J) is a powerful generator of cash flows from operating

activities, with almost $22.2 billion in net cash flows from operating activities. This is

JetBlue Airways Corp.

JetBlue is weaker than J&J. JetBlue had net cash flows from operating activities of

around $1.2 billion. In addition, JetBlue had net cash flows used for investing activities

CHAPTER 16 Statement of Cash Flows

CP 16-6 (Continued)

Cash flows from operating activities:

Net earnings $ 15,297

Gain on sale of assets/businesses (1,217)

Deferred tax provision (1,016)

Accounts receivable allowances (31)

Net cash flows from operating activities $ 22,201

Cash flows from investing activities:

Additions to property, plant, and equipment $ (3,670)

Proceeds from the disposal of assets 3,203

Acquisitions, net of cash acquired (899)

Purchases of investments (5,626)

Sales of investments 4,289

Other (primarily intangibles) (464)

Net cash used by investing activities $ (3,167)

Cash flows from financing activities:

Dividends to shareholders $ (9,494)

Repurchase of common stock (5,868)

Proceeds from short-term debt 80

Retirement of short-term debt (2,479)

Statement of Cash Flows

Johnson & Johnson

For Period Ended December 31, 2018

(in millions)

CHAPTER 16 Statement of Cash Flows

CP 16-6 (Concluded)

Cash flows from operating activities:

Net income $ 188

Adjustments to reconcile net income to net cash provided (used)

by operating activities:

Changes in certain operating assets and liabilities:

Decrease (increase) in receivables 46

Increase (decrease) in inventories, prepaid and other (174)

Increase (decrease) in air traffic liability 131

Increase (decrease) in accounts payable and other accrued liabilities 96

Other, net 2

Net cash provided by operating activities $ 1,217

Other, net (14)

Net cash used in investing activities $(1,156)

Cash flows from financing activities:

Proceeds from:

Issuance of common stock $ 48

Issuance of long-term debt 687

Repayment of long-term debt and capital lease obligations (222)

For Period Ended December 31, 2018

JetBlue Airways Corp.

Consolidated Statement of Cash Flows

(in millions)