CHAPTER 15

Long-Term Liabilities

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Describe the major

characteristics of bonds.

1, 2, 3, 4

1

1

2. Explain how to account for

bond transactions.

5, 6, 7, 8, 9

1, 2, 3, 4, 5,

6, 13

2a, 2b

2, 3, 4, 5, 6,

7, 8

1A, 2A, 3A

3. Explain how to account for

long–term notes payable.

7

3

15, 16

8, 9, 10

11, 12, 13,

1A, 2A, 4A,

*5. Apply the straight-line

method of amortizing bond

discount and bond premium.

17, 18

11, 12

15, 16

6A, 7A, 8A

*6. Apply the effective-interest

method of amortizing bond

discount and bond premium.

19, 20

13

17, 18

9A, 10A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare entries to record issuance of bonds, interest

accrual, and bond redemption.

Moderate

20–30

2A

Prepare entries to record issuance of bonds, interest

accrual, and bond redemption.

Moderate

15–20

3A

Prepare entries for interest payment, bond redemption,

and interest accrual.

Moderate

15–20

5A

Analyze three different lease situations and prepare

journal entries.

Moderate

20–30

*6A

Prepare entries to record issuance of bonds, interest

accrual, and straight-line amortization for two years.

Simple

30–40

*7A

Prepare entries to record issuance of bonds, interest, and

straight-line amortization of bond premium and discount.

Simple

30–40

*8A

Prepare entries to record interest payments, straight-line

premium amortization, and redemption of bonds.

Moderate

30–40

*9A

Prepare entries to record issuance of bonds, payment

of interest, and amortization of bond discount using

effective-interest method.

Moderate

30–40

Prepare journal entries to record issuance of bonds,

Moderate

30–40

WEYGANDT ACCOUNTING PRINCIPLES 12E

CHAPTER 15

LONG-TERM LIABILITIES

Number

LO

BT

Difficulty

Time (min.)

BE1

2

AP

Simple

2–3

BE2

2

AP

Simple

2–3

BE3

2

AP

Simple

4–6

BE4

2

AP

Simple

3–5

BE5

2

AP

Simple

4–6

BE6

2

AP

Simple

3–5

BE7

3

AP

Simple

6–8

BE8

4

AP

Simple

3–5

BE9

4

AP

Simple

6–8

BE10

4

AP

Simple

3–5

BE11

5

AP

Simple

4–6

BE12

5

AP

Simple

4–6

*BE13

2, 6

AP

Simple

4–6

DI1

1

C

Simple

2–3

DI2a

2

AP

Simple

4–6

DI2b

2

AP

Simple

3–5

DI3

3

AP

Simple

4–6

DI4

4

AP

Simple

4–6

EX1

1

C

Simple

4–6

EX2

2

AP

Simple

4–6

EX3

2

AP

Simple

4–6

EX4

2

AP

Simple

5–7

EX5

2

AP

8–10

EX6

2

AP

Simple

6–8

EX7

2

AP

Simple

6–8

EX8

2

AP

8–10

EX9

3

AP

Simple

6–8

EX10

3

AP

Simple

8–10

EX11

4

AP

Simple

3–5

EX12

4

AN

Simple

4–6

EX13

4

AN

Simple

4–6

LONG-TERM LIABILITIES (Continued)

Number

LO

BT

Difficulty

Time (min.)

*EX15

5

AP

Simple

6–8

*EX16

5

AP

Simple

6–8

*EX17

6

AP

Moderate

8–10

6

AP

Moderate

8–10

P1A

AP

Moderate

20–30

P2A

AP

Moderate

15–20

P3A

2

AP

Moderate

15–20

P4A

3, 4

AP

Moderate

20–30

P5A

4

AP

Moderate

20–30

*P6A

4, 5

AP

Simple

30–40

*P7A

4, 5

AP

Simple

30–40

*P8A

5

AP

Moderate

30–40

*P9A

6

AP

Moderate

30–40

*P10A

4, 6

AP

Moderate

30–40

BYP1

2, 4

AN

Simple

5–10

BYP2

4

AP

Simple

10–15

BYP3

4

AP

Simple

10–15

BYP4

1

Simple

BYP5

AN

Moderate

15–20

BYP6

1

Simple

10–15

BYP7

Simple

10–15

BYP8

Simple

5–10

BYP9

AP

Moderate

10–15

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Describe the major characteristics of

bonds.

Q15-1

Q15-2

Q15-3

Q15-4

DI15-1

E15-1

2. Explain how to account for bond

transactions.

Q15-5

Q15-6

Q15-8

Q15-7

Q15-9

BE15-1

BE15-2

BE15-3

BE15-4

BE15-5

BE15-6

DI15-2a

DI15-2b

E15-3

E15-4

E15-5

E15-6

E15-7

E15-8

P15-1A

P15-2A

P15-3A

DI15-4

E15-11

E15-14

P15-1A

P15-10A

*5. Apply the straight–line method of

amortizing bond discount and bond

premium.

Q15-17

Q15-18

Q15-17

BE15-11

BE15-12

E15-15

E15-16

P15-6A

P15-7A

P15-8A

*6. Apply the effective-interest method

Q15-19

BE15-13

P15-9A

ANSWERS TO QUESTIONS

1. (a) Long-term liabilities are obligations that are expected to be paid after one year. Examples

include bonds, long-term notes, and lease obligations.

(b) Bonds are a form of interest-bearing notes payable used by corporations, universities, and

governmental agencies.

2. (a) Secured bonds have specific assets of the issuer pledged as collateral. In contrast, unse–

cured bonds are issued against the general credit of the borrower. These bonds are called

debenture bonds.

4. The two major obligations incurred by a company when bonds are issued are the interest

payments due on a periodic basis and the principal which must be paid at maturity.

5. Less than. Investors are required to pay more than the face value; therefore, the market interest

rate is less than the contractual rate.

8. Debits: Bonds Payable (for the face value) and Premium on Bonds Payable (for the

unamortized balance).

Credits: Cash (for 97% of the face value) and Gain on Bond Redemption (for the difference

between the cash paid and the bonds’ carrying value).

9. A convertible bond permits bondholders to convert it into common stock at the option of the

bondholders.

Questions Chapter 15 (Continued)

11. The nature and the amount of each long-term liability should be presented in the balance sheet

or in schedules in the accompanying notes to the statements. The notes should also indicate the

interest rates, maturity dates, conversion privileges, and assets pledged as collateral.

12. (a) The major advantages are:

(1) Stockholder control is not affected—bondholders do not have voting rights, so current

stockholders retain full control of the company.

13. (a) A lease agreement is a contract in which the lessor gives the lessee the right to use an

asset for a specified period in return for one or more periodic rental payments. The lessor is

the owner of the property and the lessee is the renter or tenant.

(b) The two most common types of leases are operating leases and capital leases.

14. This lease would be reported as an operating lease. In an operating lease, each payment is debited

to Rent Expense. Neither a leased asset nor a lease liability is capitalized.

15. In a capital lease agreement, the lessee records the present value of the lease payments as an

asset and a liability. Therefore, Benedict Company would debit Leased Asset—Equipment for

$186,300 and credit Lease Liability for the same amount.

16. Apple did not redeem any of its debt during the 2013 fiscal year.

*17. The straight-line method results in the same amortized amount being assigned to Interest

Expense each interest period. This amount is determined by dividing the total bond discount or

premium by the number of interest periods the bonds will be outstanding.

*18. $28,000. Interest expense is the interest to be paid in cash less the premium amortization for the

year. Cash to be paid equals 8% X $400,000 or $32,000. Total premium equals 5% of $400,000

*19. Kelli is probably indicating that since the borrower has the use of the bond proceeds over the

term of the bonds, the borrowing rate in each period should be the same. The effective-interest

method results in a varying amount of interest expense but a constant rate of interest on the

Questions Chapter 15 (Continued)

*20. Decrease. Under the effective-interest method the interest charge per period is determined by

multiplying the carrying value of the bonds by the effective-interest rate. When bonds are issued

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 15-1

Mar. 1 Cash ($30,000 X 98%) ………………… 294,000

Discounts on Bonds Payable …….. 6,000

Bonds Payable …………………… 300,000

BRIEF EXERCISE 15-2

BRIEF EXERCISE 15-3

2017

(a) Jan. 1 Cash ………………………………………… 4,000,000

Bonds Payable

(4,000 X $1,000) ………………. 4,000,000

BRIEF EXERCISE 15-4

(a) Jan. 1 Cash ($2,000,000 X 97%) ……………. 1,940,000

Discount on Bonds Payable ………. 60,000

Bonds Payable …………………… 2,000,000

BRIEF EXERCISE 15-5

1. Jan. 1 Cash (1,000 X $1,000) ………………… 1,000,000

Bonds Payable …………………… 1,000,000

BRIEF EXERCISE 15-6

Bonds Payable ………………………………………………… 1,000,000

Loss on Bond Redemption

BRIEF EXERCISE 15-7

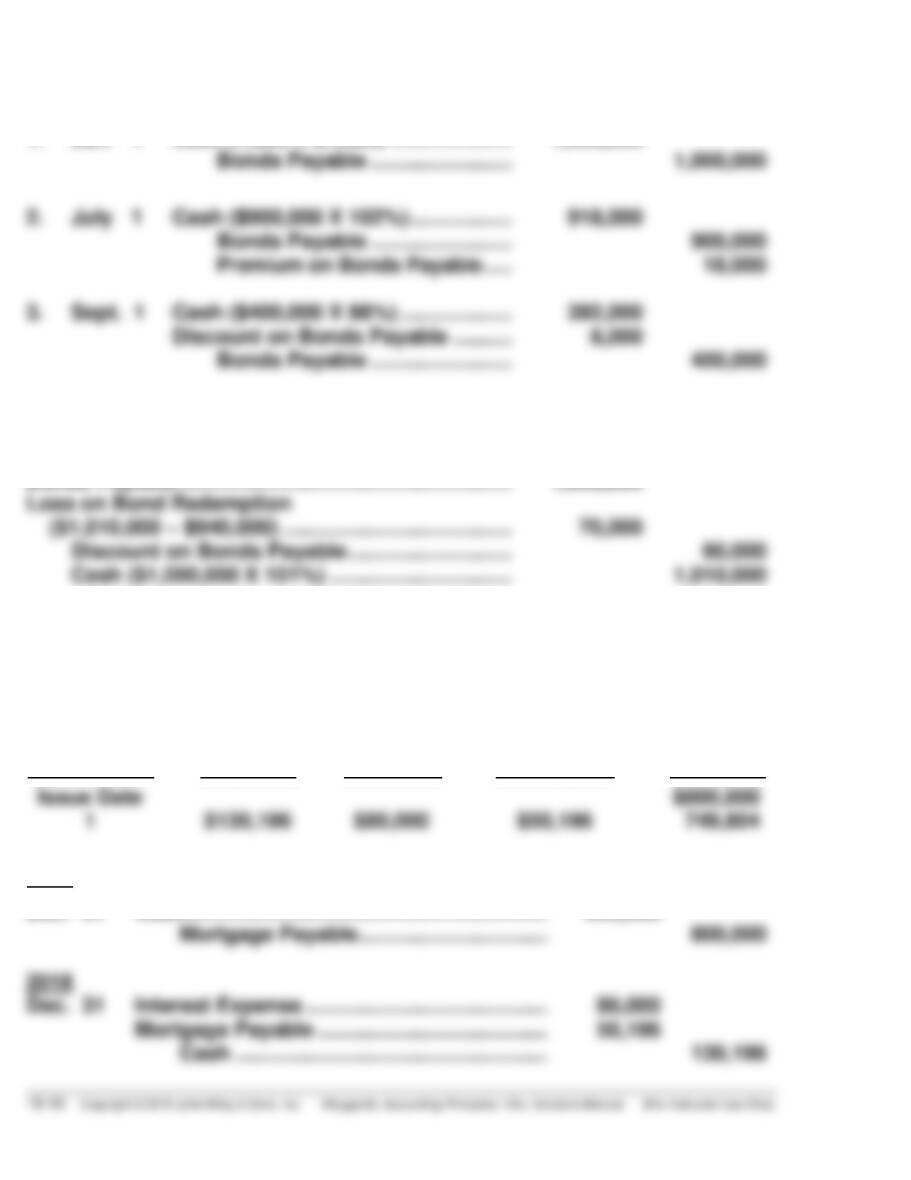

Semiannual

Interest

Period

(A)

Cash

Payment

(B)

Interest

Expense

(D) X 10%

(C)

Reduction

of Principal

(A) – (B)

(D)

Principal

Balance

(D) – (C)

Issue Date

1

$130,196

$80,000

$50,196

$800,000

749,804

2017

Dec. 31 Cash ……………………………………………………. 800,000

BRIEF EXERCISE 15-8

Long-term liabilities

Bonds payable, due 2019 ……………………………….. $600,000

Less: Discount on bonds payable ………………….. 45,000 $555,000

BRIEF EXERCISE 15-9

Issue Stock

Issue Bond

Income before interest and taxes

Interest ($2,000,000 X 8%)

$700,000

0

$700,000

160,000

Net income is higher if stock is used. However, earnings per share is lower

than earnings per share if bonds are used because of the additional shares

of stock that are outstanding.

BRIEF EXERCISE 15-10

1. Rent Expense ………………………………………………… 80,000

Cash ………………………………………………………. 80,000

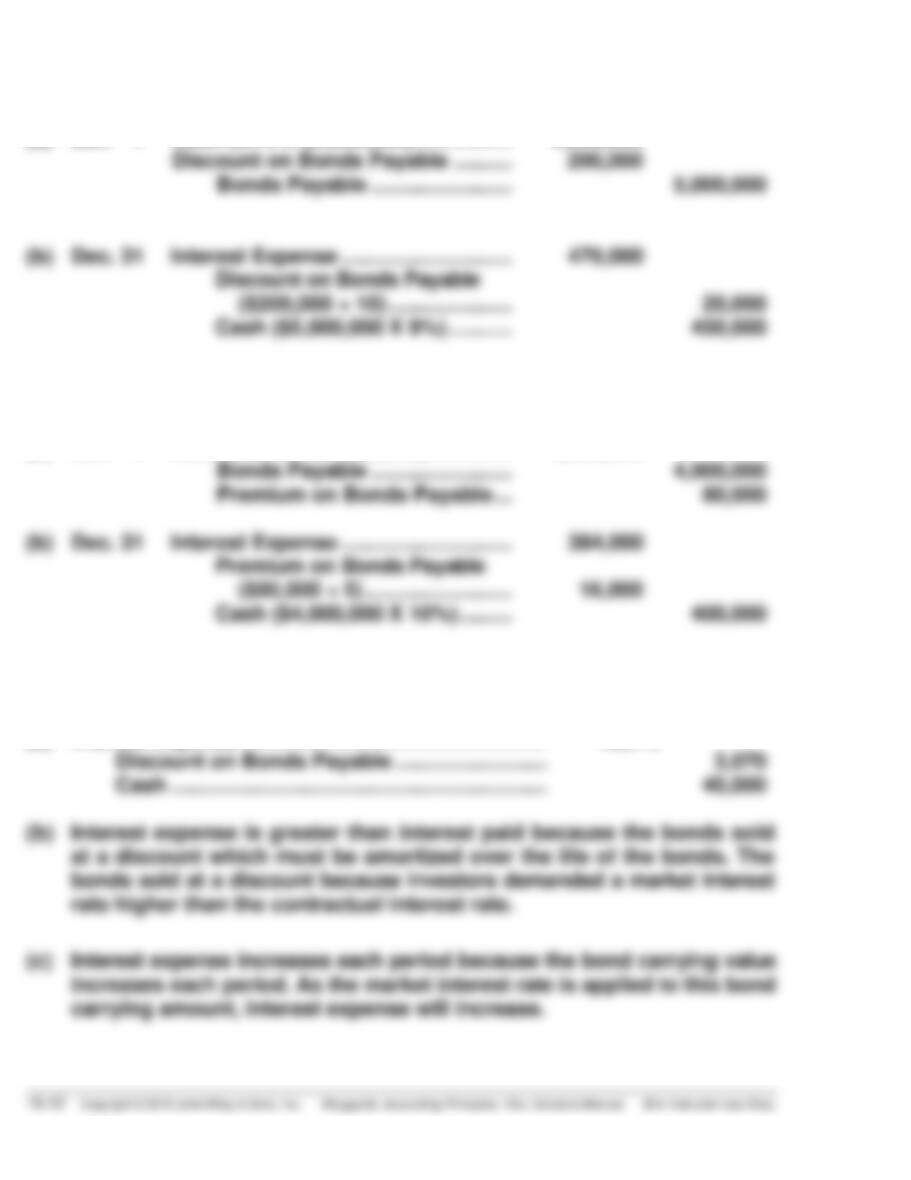

*BRIEF EXERCISE 15-11

(a) Jan. 1 Cash (96% X $5,000,000) ……………. 4,800,000

Discount on Bonds Payable ………. 200,000

Bonds Payable …………………… 5,000,000

*BRIEF EXERCISE 15-12

(a) Jan. 1 Cash (102% X $4,000,000) ………….. 4,080,000

Bonds Payable …………………… 4,000,000

Premium on Bonds Payable … 80,000

*BRIEF EXERCISE 15-13

(a) Interest Expense ……………………………………………. 48,070

Discount on Bonds Payable …………………….. 3,070

Cash ………………………………………………………. 45,000

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 15-1

1. False. Mortgage bonds and sinking fund bonds are both examples of

secured bonds.

2. False. Convertible bonds can be converted into common stock at the

DO IT! 15-2a

(a) Cash ……………………………………………………………… 520,000

Bonds Payable ……………………………………….. 500,000

DO IT! 15-2b

Loss on Bond Redemption ……………………………………. 6,000

DO IT! 15-3

Cash ……………………………………………………………………. 700,000

Mortgage Payable ………………………………………….. 700,000

(To record mortgage loan)

DO IT! 15-4

(a) Leased Asset—Equipment ………………………………… 192,000

Lease Liability …………………………………………… 192,000

(To record leased asset and lease liability)

SOLUTIONS TO EXERCISES

EXERCISE 15-1

1. True.

2. True.

EXERCISE 15-2

2017

(a) Jan. 1 Cash ……………………………………………… 500,000

Bonds Payable ………………………… 500,000

EXERCISE 15-3

2017

(a) Jan. 1 Cash ……………………………………………….. 400,000

Bonds Payable ………………………….. 400,000

EXERCISE 15-4

2017

(a) Jan. 1 Cash ……………………………………………….. 400,000

Bonds Payable ………………………….. 400,000

EXERCISE 15-5

At 100

(a) (1) Cash ……………………………………………………. 2,000,000

Bonds Payable ……………………………….. 2,000,000

At 98

At 103

(3) Cash ……………………………………………………. 2,060,000

Bonds Payable ……………………………….. 2,000,000

Premium on Bonds Payable ……………. 60,000

EXERCISE 15-5 (Continued)

Redemption of bonds before maturity at 98

(c) Bonds Payable …………………………………….. 2,000,000

Conversion of bonds into common stock

(d) Bonds Payable ……………………………………. 2,000,000

EXERCISE 15-6

(a) (1) Cash ………………………………………………………. 485,000

Discount on Bonds Payable …………………….. 15,000

Bonds Payable ………………………………….. 500,000

OR

Principal at maturity ………………………………… $500,000

Annual interest payments

(b) (1) Cash ………………………………………………………. 525,000

Bonds Payable ………………………………….. 500,000

Premium on Bonds Payable ………………. 25,000

EXERCISE 15-6 (Continued)

(2) Annual interest payments

($40,000 X 5) ………………………………………… $200,000

OR

Principal at maturity ………………………………… $500,000

Annual interest payments

EXERCISE 15-7

(a) Jan. 1 Interest Payable ……………………………… 112,000

Cash ……………………………………….. 112,000

EXERCISE 15-8

1. June 30 Bonds Payable ………………………………. 130,000

Loss on Bond Redemption

EXERCISE 15-8 (Continued)

2. June 30 Bonds Payable ……………………………… 150,000

Premium on Bonds Payable …………… 1,000

3. Dec. 31 Bonds Payable ……………………………… 20,000

EXERCISE 15-9

2017

Issuance of Note

Dec. 31 Cash …………………………………………………….. 300,000

2018

First Installment Payment

Dec. 31 Interest Expense

($300,000 X 10%) ……………………………….. 30,000

2019

Second Installment Payment

EXERCISE 15-10

January 1, 2017

(a) Cash ……………………………………………………………. 300,000

December 31, 2017

Interest Expense

($300,000 X 8%) ………………………………………… 24,000

December 31, 2018

Interest Expense

[($300,000 – $16,000) X 8%] ………………………… 22,720

(b) Current: $17,280

[$40,000 – ($284,000 X 8%)]

EXERCISE 15-11

Long-term liabilities

Bonds payable, due 2022 …………………………. $180,000