15–1

CHAPTER 15

UNDERSTANDING THE ISSUES

1. GASB Statement No. 34 stipulates a new

reporting model that includes two separate,

but related sets of financial statements. The

accrual-basis accounting. The value of both

perspectives is the retention of a near cash

ning for increased expenditures in future

periods. Capital assets and long-term

2. Separating activity into governmental, pro-

prietary, and fiduciary funds allows for

3. Budgets are the legal authorization to raise

revenue, incur long-term debt, and appro-

priate resources. Authorized expenditures

4. The advantage of reporting designations of

the fund balance is improved communica-

ment’s ability to cover financial obligations

and invest in future assets. Further classify-

for payment of an “expected liability.” It is

an estimate of an expenditure that may or

15–2

cash is recorded in the fund, and the debt

is removed from the account group. Since

7. (Appendix) The 13 basic principles of gov-

ernment accounting are found in GASB

15–3 Ch. 15—Exercises

EXERCISES

EXERCISE 15-1

(2) d (a), (b), and (c) represent outflows of financial resources to acquire goods and services.

The consumption, not the purchase of inventory, is an expenditure.

(4) d Revenues are credited when the taxpayers are billed.

(6) c Governmental organization reporting is designed to demonstrate the accountability for

(7) a Acquisition of a new police car in a city’s general fund would be displayed as an expenditure in

its governmental fund statement of revenues, expenditures, and changes in fund balances.

(9) d When a purchase order is approved, Encumbrances is debited to reflect the expected

(10) a The lease obligation is long-term debt and should be recorded in the account group.

EXERCISE 15-2

(1) a Grants without restriction are recorded as revenue when received.

(3) b This is an expenditure by the general fund.

(5) e A loan only affects the balance sheet accounts.

(7) b Payments on an operating lease are expenditures for the general fund.

Ch. 15—Exercises 15–4

EXERCISE 15-3

Estimated Revenues ($205,000 + $7,000 + $90,000 + $50,000) …. 352,000

EXERCISE 15-4

Jan. Cash …………………………………………………………………………. 275,000

Tax Anticipation Notes Payable ………………………………. 275,000

To record borrowing.

Feb. Cash …………………………………………………………………………. 12,000

Apr. Cash …………………………………………………………………………. 104,500

Delinquent Property Taxes Receivable …………………….. 100,000

Revenues …………………………………………………………….. 4,500

To record collection of delinquent property taxes.

Tax Liens Receivable ………………………………………………….. 5,000

Exercise 15-4, Concluded

Sept. Cash …………………………………………………………………………. 345,000

EXERCISE 15-5

(1) Cash …………………………………………………………………………….. 45,000

(2) No entry in the general fund for land. Record in the general

fixed assets account group:

(3) Due from State ………………………………………………………………. 30,000

(4) Cash …………………………………………………………………………….. 9,000

Other Financing Sources ……………………………………………. 9,000

(5) Cash …………………………………………………………………………….. 5,000

Revenues …………………………………………………………………. 2,500

EXERCISE 15-6

(1) Expenditures ($100,000 + $50,000 + $125,000 + $13,000) ….. 288,000

(2) Other Financing Uses ……………………………………………………… 50,000

(3) Expenditures ………………………………………………………………….. 43,000

Inventory of Supplies …………………………………………………. 43,000

EXERCISE 15-7

(1) Encumbrances ……………………………………………………………….. 18,000

(2) Encumbrances ……………………………………………………………….. 70,000

(3) Fund Balance—Assigned or Committed ……………………………. 88,000

Encumbrances ………………………………………………………….. 88,000

To reverse encumbrances for orders received.

Inventory of Supplies ………………………………………………………. 82,000

Vouchers Payable ……………………………………………………… 82,000

To record purchase of inventory.

15–7 Ch. 15—Exercises

EXERCISE 15-8

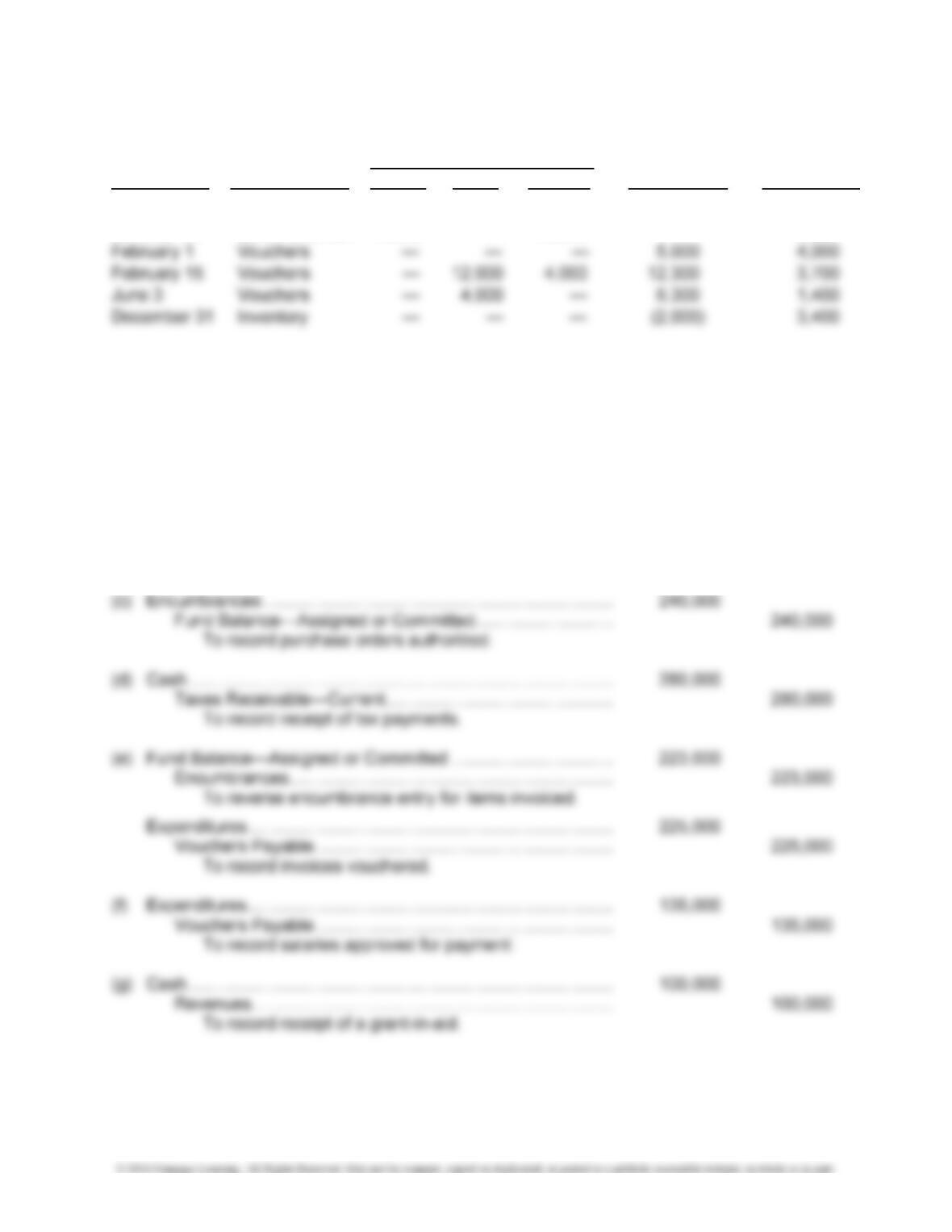

Encumbrances

Unobligated

Date Item Debit Credit Balance Expenditures Balance

January 1 Budget — — — — 25,000

January 15 Encumbrances 16,000 — 16,000 — 9,000

EXERCISE 15-9

(a) Estimated Revenues ………………………………………………………. 520,000

Appropriations …………………………………………………………… 515,000

Budgetary Fund Balance—Unassigned ………………………… 5,000

To record budget for the year.

(b) Taxes Receivable—Current …………………………………………….. 378,788

Allowance for Uncollectible Current Taxes ……………………. 3,788

Revenues …………………………………………………………………. 375,000

To record tax levy.

Exercise 15-9, Concluded

(h) Cash …………………………………………………………………………….. 10,000

Revenues …………………………………………………………………. 10,000

To record receipt of miscellaneous revenues.

(i) Expenditures ………………………………………………………………….. 120,000

Cash ……………………………………………………………………….. 120,000

To record purchase of property. (The property would also

be entered in the general fixed assets account group.)

(l) Due from State ………………………………………………………………. 30,000

Revenues …………………………………………………………………. 30,000

To record share of state sales taxes receivable.

(m) Vouchers Payable ………………………………………………………….. 175,000

Cash ……………………………………………………………………….. 175,000

To record vouchers paid.

(n) Budgetary Fund Balance—Unassigned …………………………….. 5,000

EXERCISE 15-10

(1) Closing entries:

Appropriations …………………………………………………………………. 650,000

Estimated Other Financing Uses ……………………………………….. 50,000

Budgetary Fund Balance …………………………………………………… 50,000

(2) Shorewood Village

General Fund

Budgetary Comparison Schedule

For Fiscal Year Ended June 30, 2019

Variance—

Favorable

Budget

Actual (Unfavorable)

Revenues ………………………………………………………….. $ 600,000 $ 595,000 $ (5,000)

Expenditures ……………………………………………………… 650,000 588,000 62,000

Excess (shortage) of revenues over

Exercise 15-10, Concluded

(3) Shorewood Village

General Fund Balance Sheet

June 30, 2019

Assets Liabilities and Fund Equity

Cash ……………………………….. $190,000 Liabilities: Vouchers payable ……….. $ 91,000

Receivables (net) ……………… 120,000 Fund balances:

brances

EXERCISE 15-11

Event Fund or Group Entry

Purchase General Fund Expenditures …………………………………. 65,000

Cash ………………………………………… 65,000

Fund Balance—Assigned or Committed 70,000

Encumbrances …………………………… 70,000

15–11 Ch. 15—Exercises

EXERCISE 15-12

(a) Land …………………………………………………………………………………… 325,000

Buildings …………………………………………………………………………….. 975,000

Investment in General Fixed Assets—General Funds ………….. 1,300,000

To record property purchase.

(b) Land …………………………………………………………………………………… 330,000

Buildings …………………………………………………………………………….. 220,000

Investment in General Fixed Assets—Donations ………………… 550,000

To record donated property at its fair value.

(c) Construction in Progress ………………………………………………………. 800,000

Investment in General Fixed Assets—Capital Projects Funds

(General Obligation Bonds) ………………………………………… 800,000

To record cost of work to date.

EXERCISE 15-13

(1) Amount to Be Provided for Compensated Absences ………………… 2,200,000

(2) Unfunded Compensated Absences ………………………………………… 400,000

(3) Amount to Be Provided for Claims and Judgments …………………… 11,000,000

Claims and Judgments Payable ……………………………………….. 11,000,000

Exercise 15-13, Concluded

(4) Amount to Be Provided for Payment of Bonds ………………………. 100,000,000

(5) Amount Available in the Debt Service Fund ………………………….. 1,000,000

(6) Amount Available in the Debt Service Fund ………………………….. 4,800,000

EXERCISE 15-14

(a) Amount to Be Provided for Payment of Term Bonds ………………. 13,000,000

Term Bonds Payable ……………………………………………………. 13,000,000

To record issuance of general obligation bonds at

EXERCISE 15-15

(Note to Instructor: The GASB Web site lists all of the pronouncements of the board. Individual

15–13 Ch. 15—Problems

PROBLEMS

PROBLEM 15-1

(1) b Funds are used to separate reporting of the diverse variety of governmental activities

(3) b The GASB stipulated that the measurement focus for governmental funds is the flow of

financial resources.

(4) c Interperiod equity seeks to determine whether current-year revenues are sufficient to

pay for current-year services or whether future taxpayers will be required to assume

burdens for services previously provided. The flow of financial resources measurement

(5) a Long-term debt used to purchase fixed assets is recorded in the general fund as an

(6) d Current standards specify that neither interest nor principal on long-term debt should be

PROBLEM 15-2

(2) a Grants from outside units are revenues unless they require the prior recording of an ex-

penditure that is then reimbursed.

(4) c These notes are short-term operating debt that will be repaid out of current revenues.

(6) b A hypothetical entry to record the tax levy is:

Taxes Receivable—Current ………………………………………… 100,000

Problem 15-2, Concluded

(7) a Revenues are recognized when measurable and available to meet current-period ex-

(8) a The general fixed assets account group records the fixed assets of governmental funds

but not proprietary funds or trust funds.

(9) b Expenditures are recorded when the liability is incurred. Under the modified accrual

PROBLEM 15-3

(1) At inception of the lease:

General Fund Expenditures …………………………………………. 800,000

Other Financing Sources …………………… 800,000

To record the acquisition of the

(2) First interest payment:

General Fund Expenditures (interest) ($800,000 × 6%) …… 48,000

Expenditures (principal) ………………………….. 60,694

Problem 15-3, Concluded

General Capital Lease Obligation …………………………. 60,694

Long-Term Amount to Be Provided ……………………… 60,694

PROBLEM 15-4

(1) (a) Estimated Revenues ……………………………………………………….. 400,000

Appropriations …………………………………………………………. 362,000

Budgetary Fund Balance—Unassigned ………………………. 38,000

To record budget.

Encumbrances ……………………………………………………………….. 16,000