1. Horizontal analysis is the percentage analysis of increases and decreases in corresponding

statements. The percent change in the cash balances at the end of the preceding year from the

2. Comparative statements provide information as to changes between dates or periods. Trends

p

3. Before this question can be answered, the increase in net income should be compared with

changes in sales, expenses, and assets devoted to the business for the current year. The return

5. a. A high inventory turnover minimizes the amount invested in inventories, thus freeing

funds for more advantageous use. Storage costs, administrative expenses, and losses

b

b

6. The ratio of fixed assets to long-term liabilities increased from 3.4 for the preceding year to

p

7. a. The rate earned on total assets adds interest expense to the net income, which is divided

b

y average total assets. It measures the profitability of the total assets, without regard for how

CHAPTER 15

FINANCIAL STATEMENT ANALYSIS

DISCUSSION QUESTIONS

15-1

p

CHAPTER 15 Financial Statement Analysis

DISCUSSION QUESTIONS (Concluded)

8. a. Due to leverage, the rate on stockholders’ equity will often be greater than the rate on

total assets. This occurs because the amount earned on assets acquired through the use of

10. One report is the Report on Internal Control, which verifies management’s conclusions on

15-2

CHAPTER 15 Financial Statement Analysis

PE 15–1A

PE 15–1B

PE 15–2A

Amount Percentage

PE 15–2B

Amount Percentage

PE 15–3A

a. Current Ratio = Current Assets ÷ Current Liabilities

PRACTICE EXERCISES

15-3

PE 15–3B

a. Current Ratio = Current Assets ÷ Current Liabilities

PE 15–4A

a. Accounts Receivable Turnover = Net Sales ÷ Average Accounts Receivable

PE 15–4B

a. Accounts Receivable Turnover = Net Sales ÷ Average Accounts Receivable

15-4

CHAPTER 15 Financial Statement Analysis

PE 15–5A

a. Inventory Turnover = Cost of Goods Sold ÷ Average Inventory

PE 15–5B

a. Inventory Turnover = Cost of Goods Sold ÷ Average Inventory

15-5

PE 15–6A

PE 15–6B

PE 15–7A

PE 15–7B

Fixed Assets

Long-Term Liabilities

Income Before Income Tax +

Interest Expense

Interest Expense

Ratio of Fixed Assets to Long-Term Liabilities

Ratio of Fixed Assets to Long-Term Liabilities

Number of Times

Interest Charges Are Earned =

Number of Times

Interest Charges Are Earned

Interest Expense

Interest Expense

=

Income Before Income Tax +

Fixed Assets

Long-Term Liabilities

a.

=

a. =

15-6

CHAPTER 15 Financial Statement Analysis

PE 15–8A

PE 15–8B

PE 15–9A

PE 15–9B

Rate Earned on Total Assets = Net Income + Interest Expense

Average Total Assets

Rate Earned on Total Assets =

Net Income + Interest Expense

Average Total Assets

15-7

CHAPTER 15 Financial Statement Analysis

PE 15–10A

PE 15–10B

a. Rate Earned on Stockholders’ Equity = Net Income

Average Stockholders’ Equity

a. Rate Earned on Stockholders’ Equity = Net Income

Average Stockholders’ Equity

15-8

CHAPTER 15 Financial Statement Analysis

PE 15–11A

Earnings per Share

on Common Stock

PE 15–11B

Earnings per Share

on Common Stock

on Common Stock

a. =Net Income – Preferred Dividends

Shares of Common Stock Outstanding

a. Net Income – Preferred Dividends

Shares of Common Stock Outstanding

=

b. Market Price per Share of Common Stock

Earnings per Share on Common Stock

Price-Earnings Ratio =

15-9

CHAPTER 15 Financial Statement Analysis

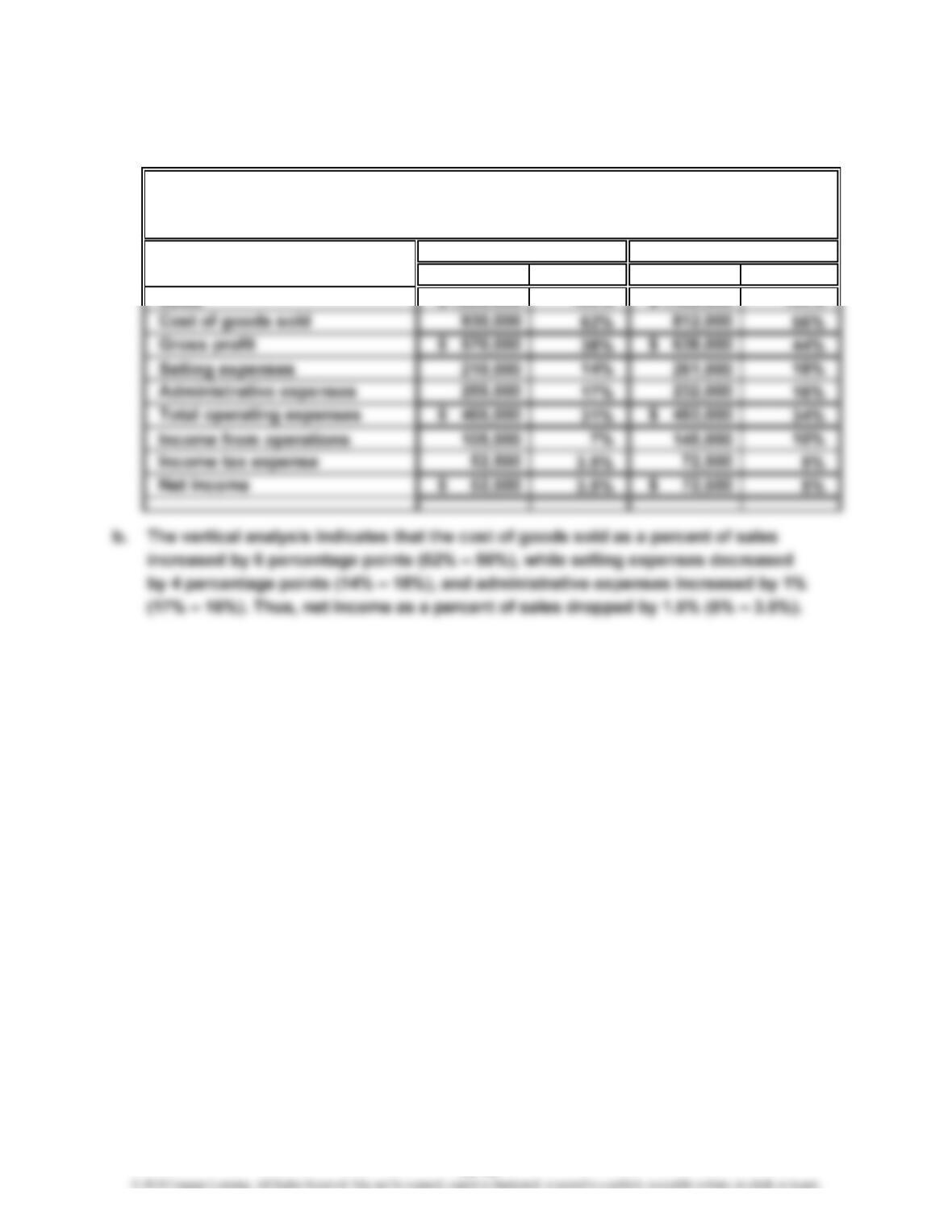

Ex. 15–1

a.

Amount Percent Amount Percent

Sales $1,500,000 100% $1,450,000 100%

2014 2013

EXERCISES

SOLDNER, Inc.

Comparative Income Statement

For the Years Ended December 31, 2014 and 2013

15-10

CHAPTER 15 Financial Statement Analysis

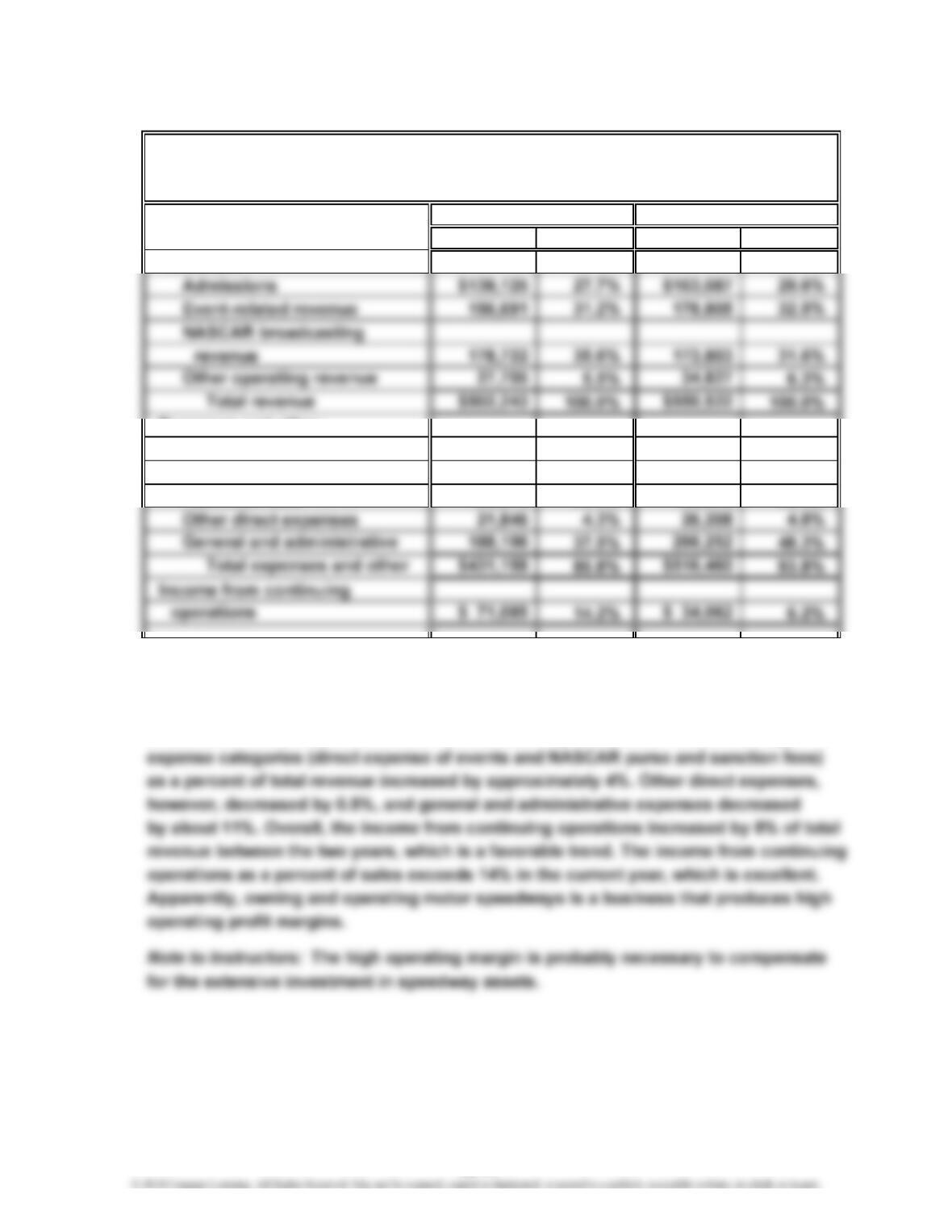

Ex. 15–2

a.

Amount Percent Amount Percent

Revenues:

Expenses and other:

Direct expense of events $100,843 20.1% $100,922 18.3%

NASCAR purse and

sanction fees 120,273 23.9% 123,078 22.4%

b. While overall revenue decreased some between the two years, the overall mix

of revenue sources did change somewhat. The NASCAR broadcasting revenue

increased as a percent of total revenue by 4 percentage points, while the percent

of admissions revenue to total revenue decreased by almost 2%. Two of the major

Current Year Prior Year

SPEEDWAY MOTORSPORTS, INC.

Comparative Income Statement (in thousands of dollars)

For the Years Ended December 31

15-11

CHAPTER 15 Financial Statement Analysis

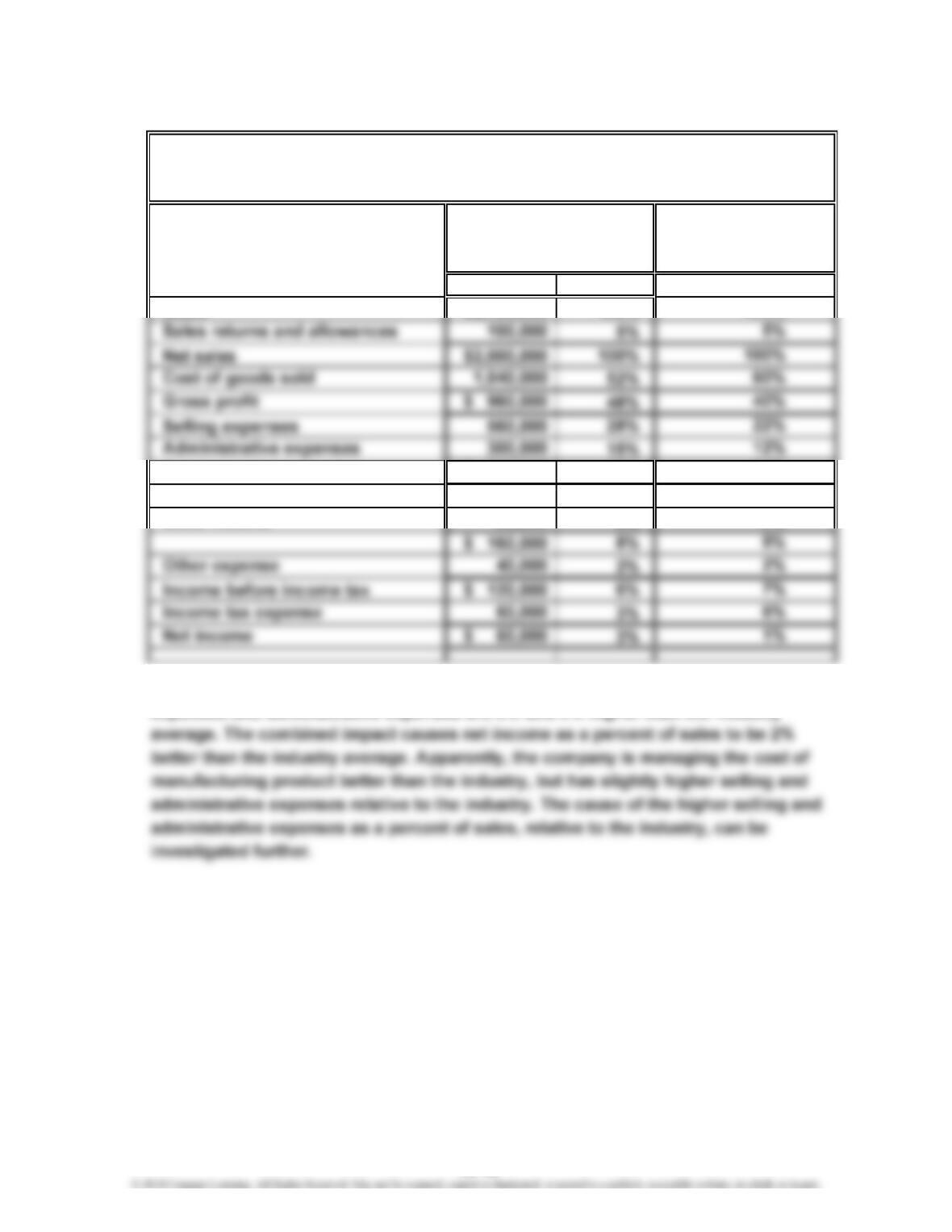

Ex. 15–3

a.

Amount Percent

Sales $2,100,000 105%

Total operating expenses $ 860,000 43%

Operating income 100,000 5%

Other income 60,000 3%

b. The cost of goods sold is 8% lower than the industry average, but the selling

expenses and administrative expenses are 6% and 3% higher than the industry

Bull Run

Company

Industry

Average

Electronics

BULL RUN COMPANY

Common-Sized Income Statement

For the Year Ended December 31, 20—

6%

3%

105%

34%

15-12

CHAPTER 15 Financial Statement Analysis

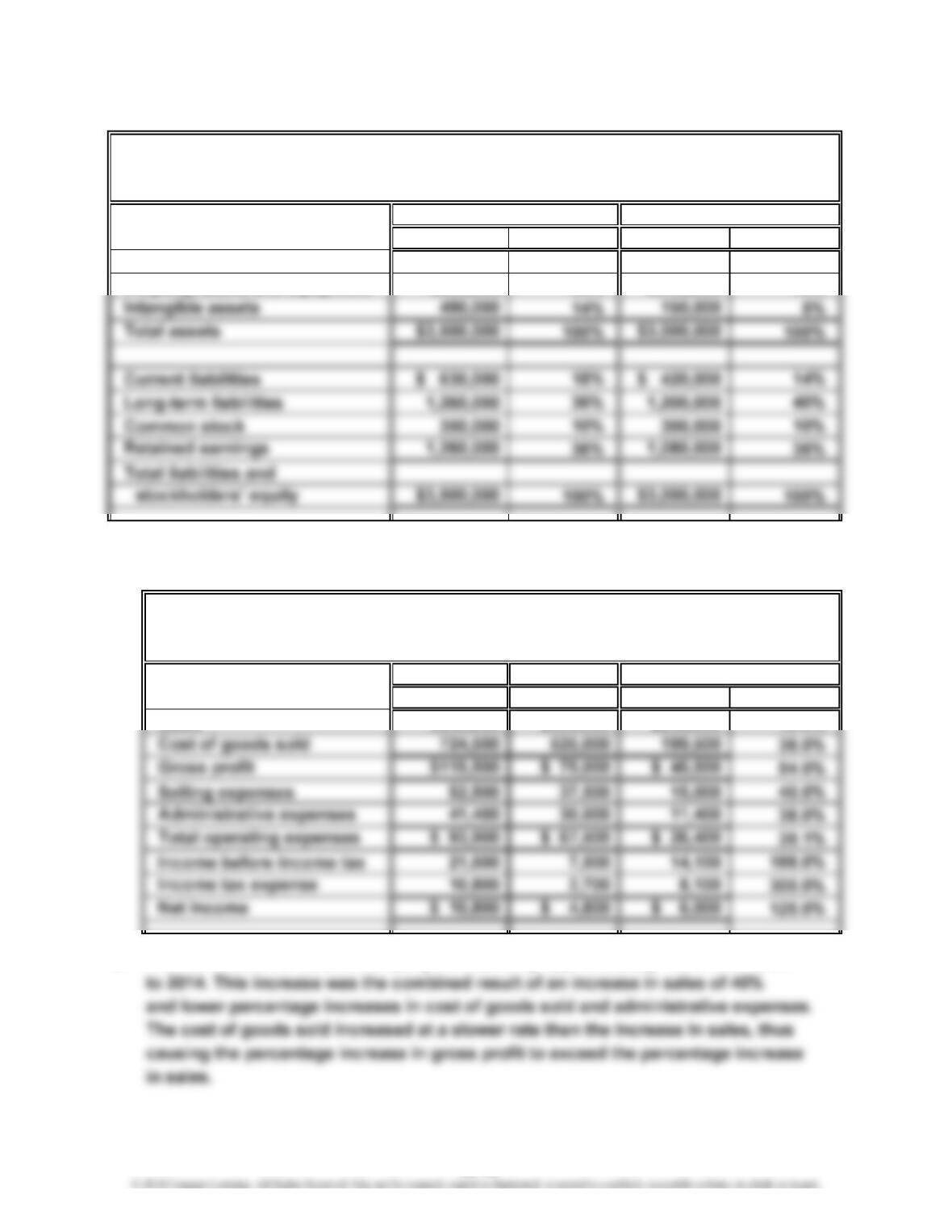

Ex. 15–4

Amount Percent Amount Percent

Current assets $1,050,000 30% $ 750,000 25%

Property, plant, and equipment 1,960,000 56% 2,100,000 70%

Ex. 15–5

a.

2014 2013

Amount Amount Amount Percent

Sales $840,000 $600,000 $240,000 40.0%

b. The net income for Bezos Company increased by approximately 125% from 2013

PEACOCK COMPANY

Comparative Balance Sheet

December 31, 2014 and 2013

Increase (Decrease)

BEZOS COMPANY

Comparative Income Statement

For the Years Ended December 31, 2014 and 2013

2014 2013

15-13

CHAPTER 15 Financial Statement Analysis

Ex. 15–6

a. (1) Working Capital = Current Assets – Current Liabilities

b. The liquidity of Mossberg has improved from the preceding year to the current year.

Ex. 15–7

b. The solvency of PepsiCo has decreased some over this time period. Both the

Current Assets

Current Liabilities

Current Assets

Current Liabilities

a.

=(2) Current Ratio

(1) Current Ratio =

15-14

CHAPTER 15 Financial Statement Analysis

Ex. 15–8

a. The working capital, current ratio, and quick ratio are calculated incorrectly. The

working capital and current ratio incorrectly include intangible assets and property,

The correct calculations are as follows:

= Current Assets – Current Liabilities

= $330,000 – $300,000

b. Unfortunately, the working capital, current ratio, and quick ratio are below the

Working Capital

$30,000

15-15

CHAPTER 15 Financial Statement Analysis

Ex. 15–9

b. The collection of accounts receivable has improved. This can be seen in both the

Number of Days’ Sales in Receivables

Average Accounts Receivable

Average Accounts Receivable

Average Daily Sales

Net Sales

(2)

=

a. (1) =

Accounts Receivable Turnover

15-16

CHAPTER 15 Financial Statement Analysis

Ex. 15–10

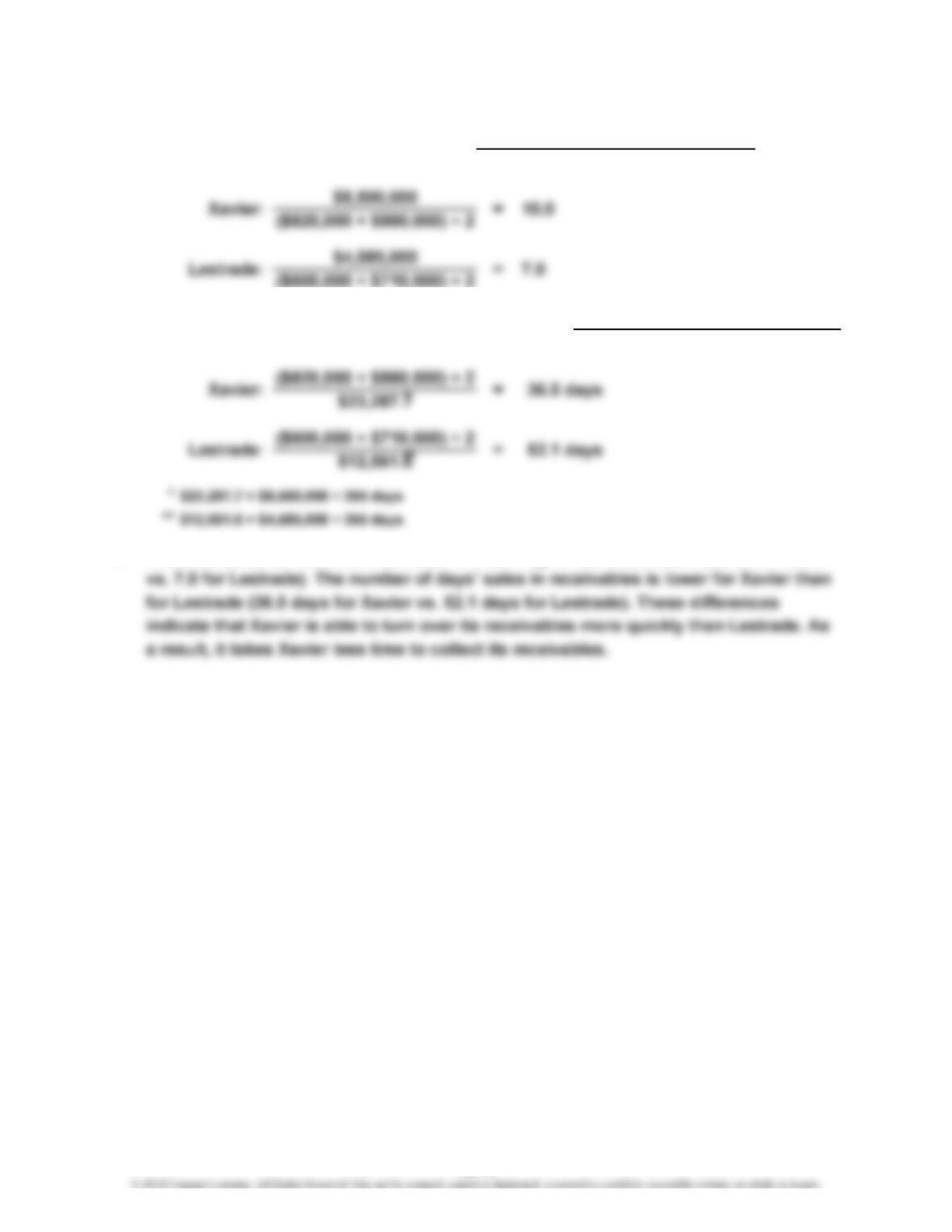

b. Xavier’s accounts receivable turnover is much higher than Lestrade’s (10.0 for Xavier

(2)

Accounts Receivable Turnover Average Accounts Receivable

Net Sales

a. (1) =

Average Accounts Receivable

Average Daily Sales

Number of Days’ Sales in Receivables

=

15-17

CHAPTER 15 Financial Statement Analysis

Ex. 15–11

b. The inventory position of the business has deteriorated. The inventory turnover

Number of Days’ Sales in Inventory

Inventory Turnover

a. (1) =

Cost of Goods Sold

Average Inventory

(2)

=Average Inventory

Average Daily Cost of Goods Sold

15-18

CHAPTER 15 Financial Statement Analysis

Ex. 15–12

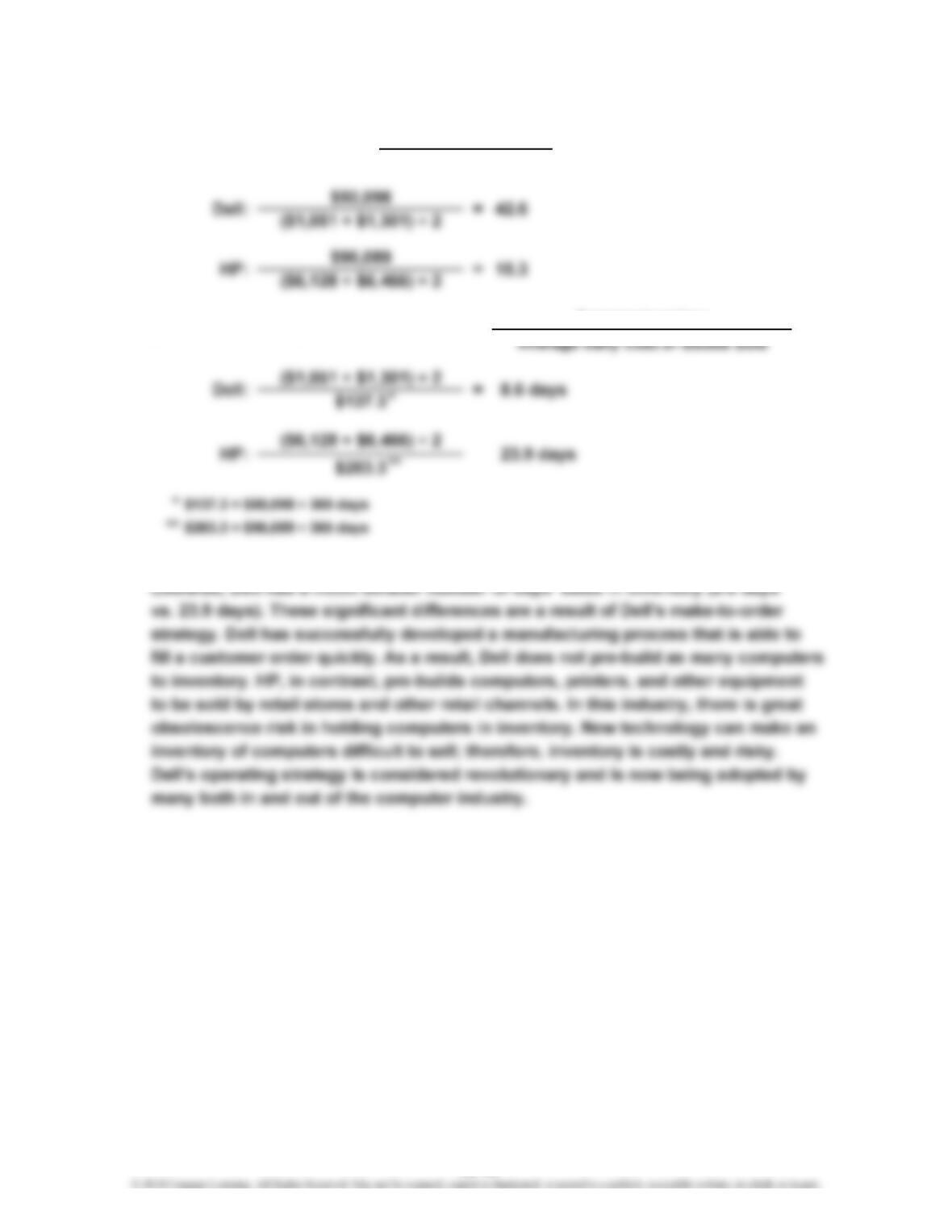

b. Dell has a much higher inventory turnover ratio than does HP (42.6 vs. 15.3).

=

Average Inventory

a. (1) Inventory Turnover =

(2)

Cost of Goods Sold

Number of Days’ Sales in Inventory Average Inventory

15-19

CHAPTER 15 Financial Statement Analysis

Ex. 15–13

c. Both the ratio of liabilities to stockholders’ equity and the number of times bond

a.

b.

Number of Times Bond

Interest Charges Are Earned

=Ratio of Liabilities to Stockholders’ Equity Total Stockholders’ Equity

Total Liabilities

=

Income Before Income Tax + Interest Expense

Interest Expense

15-20