CHAPTER 15 Investments

Prob. 15-2A

1. 20Y6

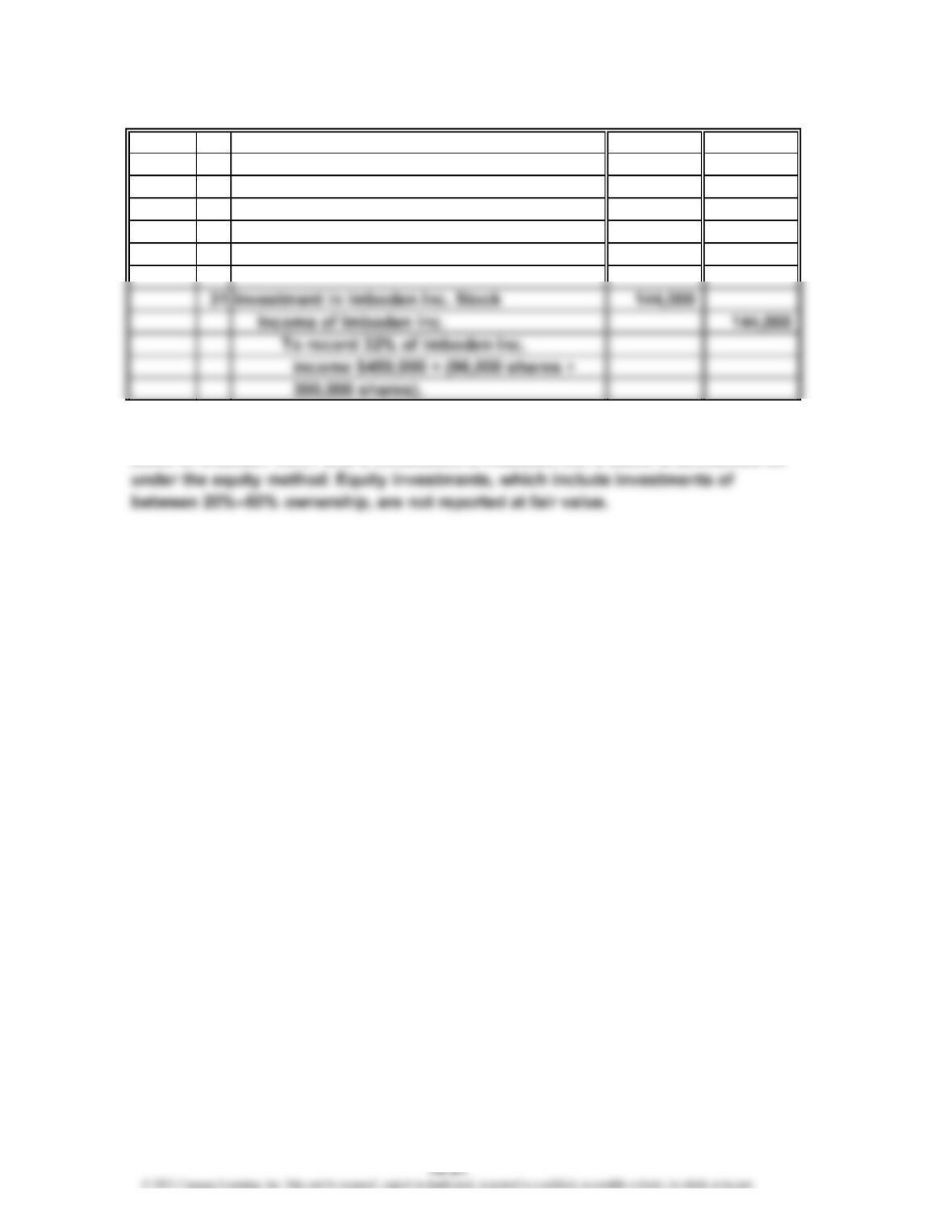

10 Investment in Imboden Inc. Stock 720,000

Cash 720,000

31 Cash 57,600

Investment in Imboden Inc. Stock 57,600

2. No. Since Forte Inc. owns 32% (96,000 shares ÷ 300,000 shares) of the outstanding

Jan.

Dec.

CHAPTER 15 Investments

Prob. 15-3A

1.

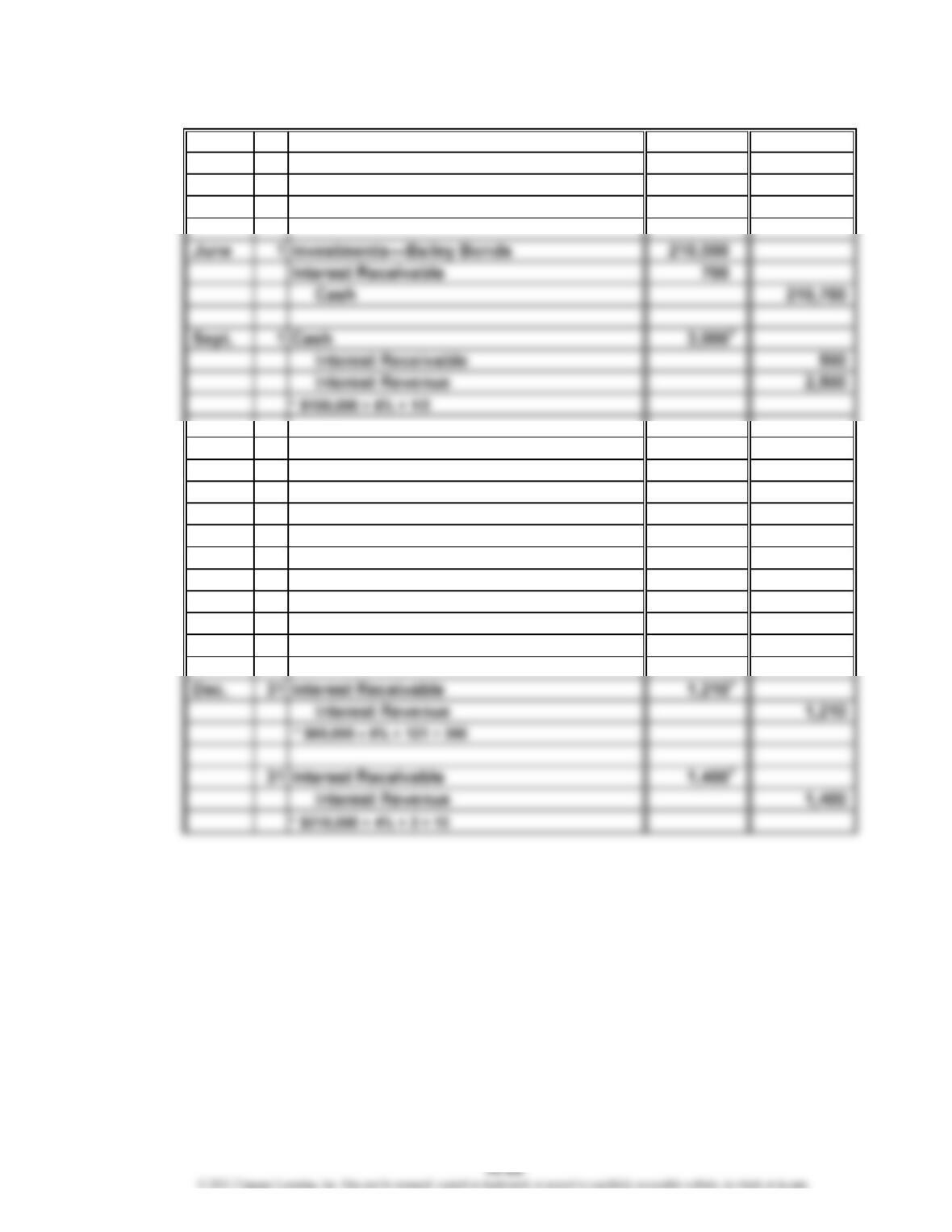

1 Investments—Welch Co. Bonds 100,000

Interest Receivable 500

Cash 100,500

30 Cash 39,000

Loss on Sale of Investments 1,200

Interest Revenue 200

Investments—Welch Co. Bonds 40,000

* ($40,000 × 0.97) + $200

1 Cash 4,200

Interest Receivable 700

Interest Revenue 3,500

* $210,000 × 4% × 1/2

20Y3

Apr.

Nov.

*

*

CHAPTER 15 Investments

Prob. 15-3A (Concluded)

1 Cash 1,800

Interest Receivable 1,210

Interest Revenue 590

* $60,000 × 6% × 1/2

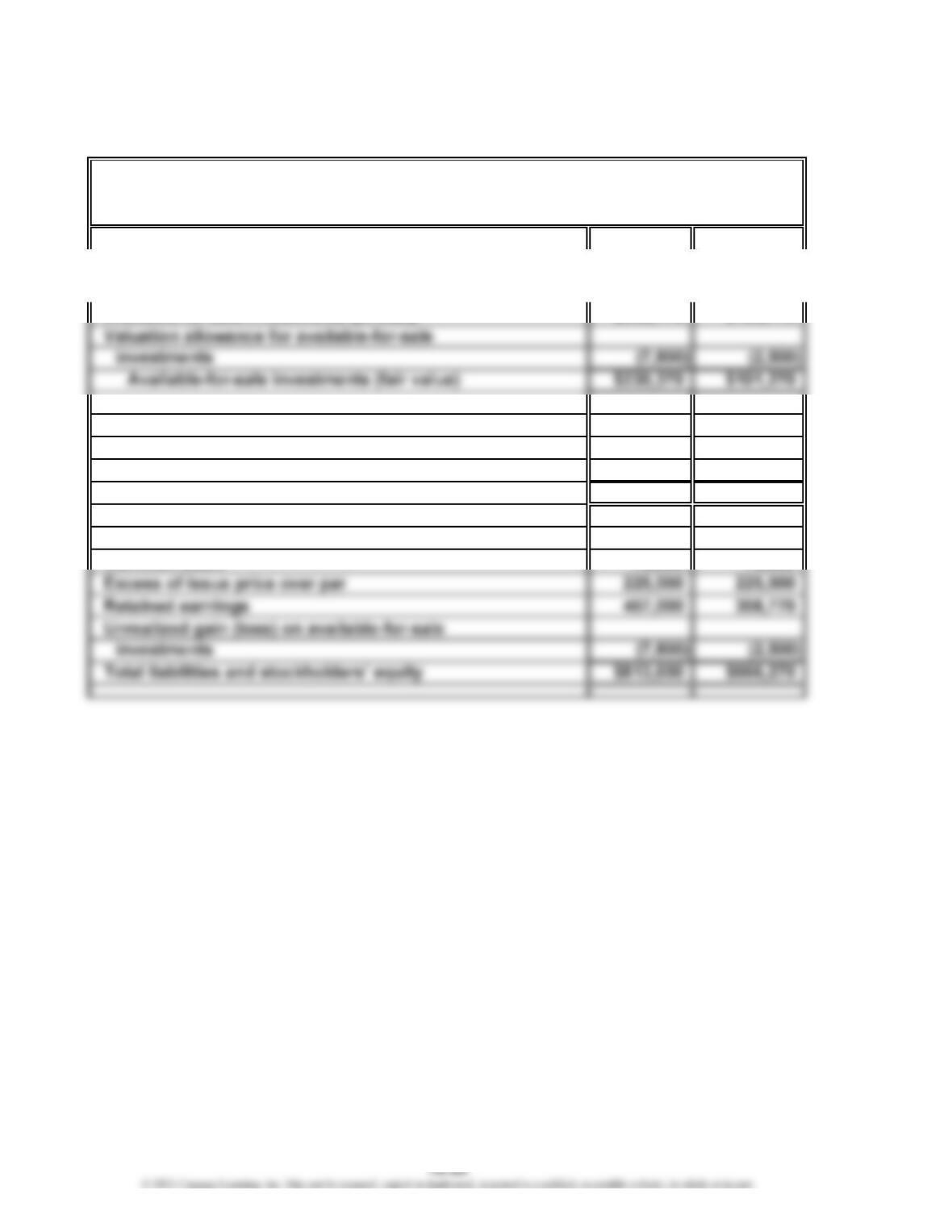

2. If the bonds are classified as available-for-sale securities, then the portfolio

of bonds would be adjusted to fair value. This would be accomplished by using

a valuation allowance account and an unrealized gain (loss) account as part of

20Y4

Mar.

*

CHAPTER 15 Investments

Prob. 15-4A

a. $238,170 (from table)

b. $(7,800) ($230,370 – $238,170, from table)

c. $230,370 ($238,170 – $7,800)

Fai

r

Issuing Company Cost

V

alue

Bernard Co. ………………………………………………

…

$ 38,250 $ 34,650

Chadwick Co. .……………………………………………

…

65,520 57,960

Gozar Inc. …………………………………………………

…

94,400 98,560

Nightline Co. ………………………………………………

…

40,000 39,200

$238,170 $230,370

CHAPTER 15 Investments

Prob. 15-4A (Concluded)

The partial balance sheets with the missing amounts are as follows:

20Y5 20Y4

^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^

^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^

Interest receivable $ 600 —

Investment in Jolly Roger Co. stock 98,100 $ 77,000

Office equipment (net) 115,000 130,000

Total assets $813,600 $666,270

Accounts payable $ 69,400 $ 65,000

O’Brien Industries Inc.

Partial Balance Sheets

December 31

CHAPTER 15 Investments

Prob. 15-1B

1.

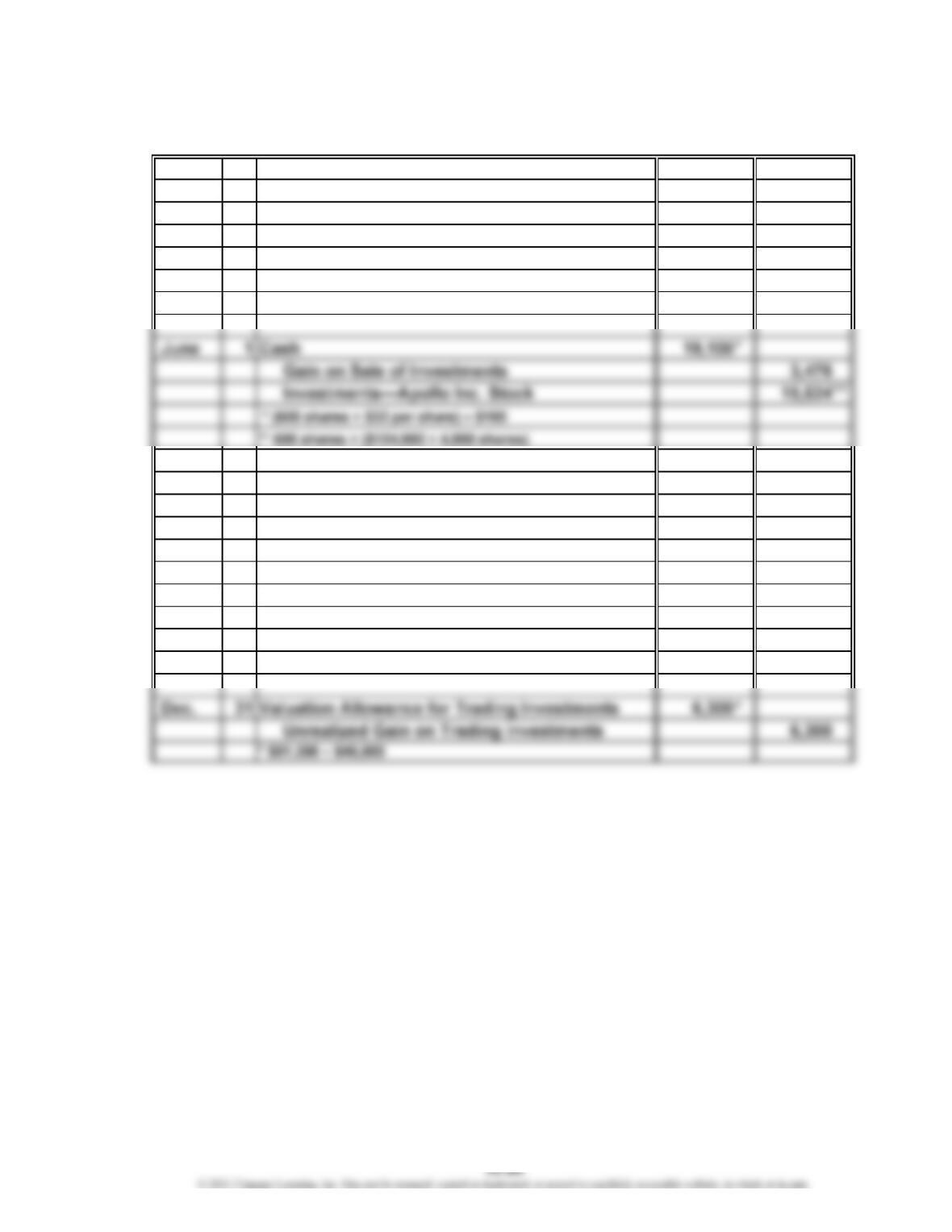

14 Investments—Apollo Inc. Stock 124,992

Cash 124,992

* (4,800 shares × $26 per share) + $192

1 Trading Investments—Ares Inc. 45,000

Cash 45,000

27 Cash 840

Dividend Revenue 840

* (4,800 shares – 600 shares) × $0.20

Oct. 15 Cash 106,800

Loss on Sale of Investments 2,568

Investments—Apollo Inc. Stock 109,368

* (4,200 shares × $25.50 per share) – $300

** 4,200 shares × ($124,992 ÷ 4,800 shares)

20Y8

Feb.

Apr.

*

*

*

**

CHAPTER 15 Investments

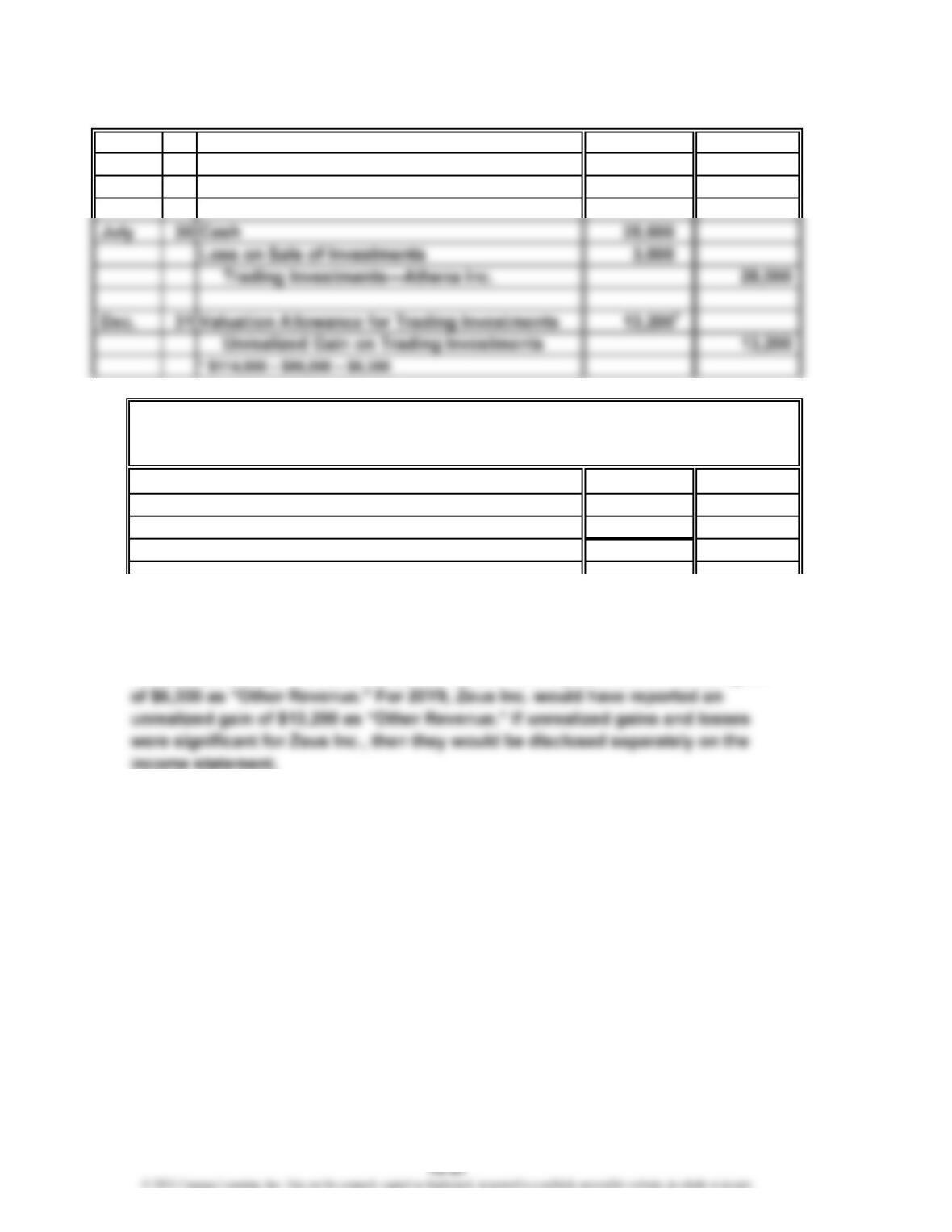

Prob. 15-1B (Concluded)

14 Trading Investments—Athena Inc. 78,000

Cash 78,000

2.

Current assets:

Trading investments (at cost) $95,000

V

aluation allowance for trading investments 19,500

Trading investments (at fair value) $114,500

*$45,000 + $50,000

** $6,300 (from 20Y8) + $13,200 (from 20Y9)

3. Unrealized gains or losses are reported on the income statement, often as “Other

Revenue (Losses).” For 20Y8, Zeus Inc. would have reported an unrealized gain

20Y9

Mar.

December 31, 20Y9

Balance Sheet (selected items)

Zeus Inc.

*

**

CHAPTER 15 Investments

Prob. 15-2B

1. 20Y3

25 Investment in Helsi Co. Stock 800,000

Cash 800,000

31 Cash 38,000

Investment in Helsi Co. Stock 38,000

2. No. Since Glacier Products Inc. owns 30% (75,000 shares ÷ 250,000 shares) of the

outstanding stock of Helsi Co., Glacier Product Inc.’s investment in Helsi Co.’s

Jan.

Dec.

CHAPTER 15 Investments

Prob. 15-3B

1.

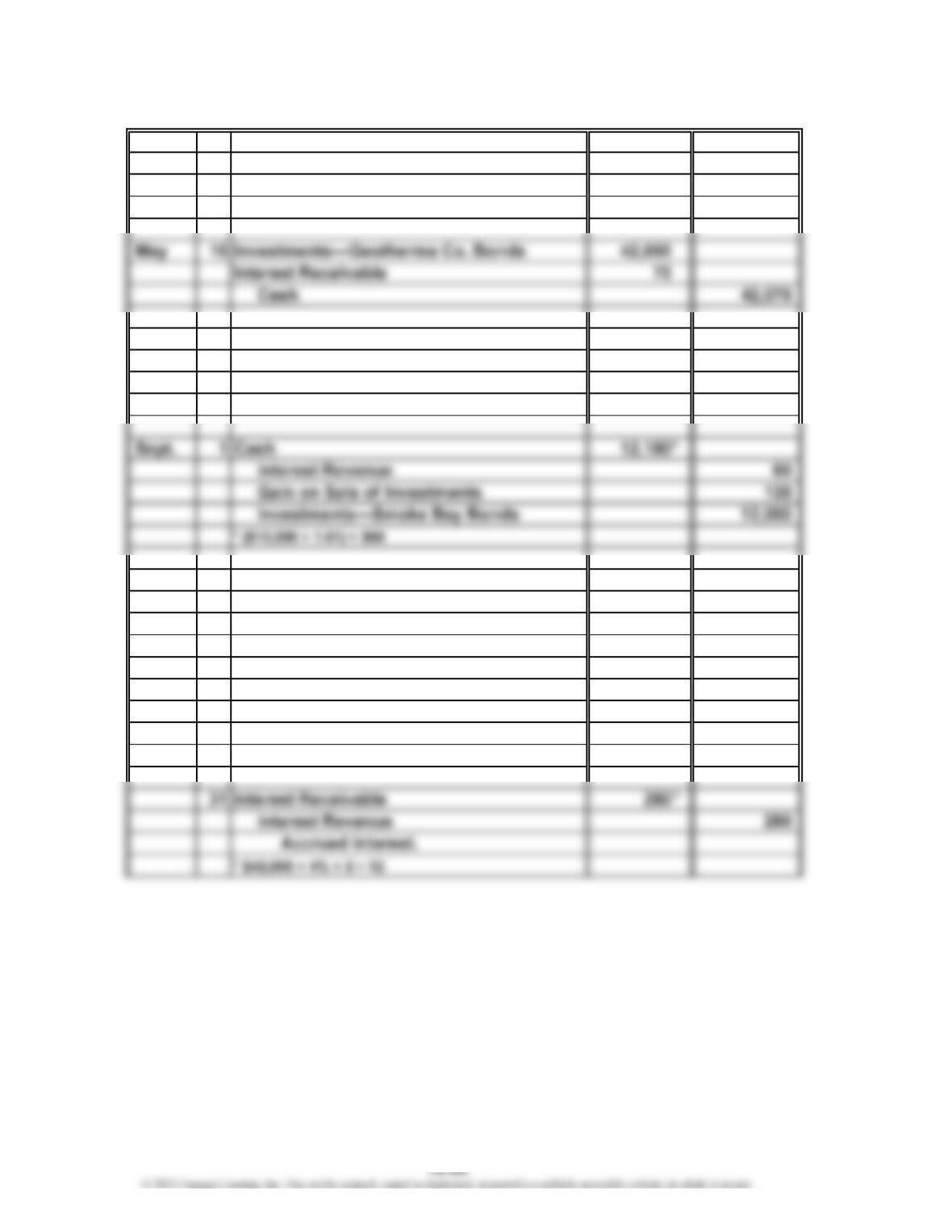

1 Investments—Smoke Bay Bonds 90,000

Interest Receivable 900

Cash 90,900

1 Cash 2,700

Interest Receivable 900

Interest Revenue 1,800

* $90,000 × 6% × 1/2

1 Cash 840

Interest Receivable 70

Interest Revenue 770

* $42,000 × 4% × 1/2

31 Interest Receivable 1,950

Interest Revenue 1,950

Accrued interest.

* $78,000 × 6% × 5 ÷ 12

Dec.

Nov.

20Y5

Aug.

Apr.

*

*

*

CHAPTER 15 Investments

Prob. 15-3B (Concluded)

1 Cash 2,340

Interest Receivable 1,950

Interest Revenue 390

* $78,000 × 6% × 1/2

2. If the bonds are classified as available-for-sale securities, then the portfolio

of bonds would need to be adjusted to fair value. This would be recorded

20Y6

Feb.

*

CHAPTER 15 Investments

Prob. 15-4B

a. $147,200 (from table)

b. $4,680 ($151,880 – $147,200, from table)

c. $151,880 (from table)

Fai

r

Issuing Company Cost

V

alue

Alvarez Inc. ………………………………………………………………..

.

$ 36,480 $ 39,840

Hirsch Inc. …………………………………………………………………. 54,720 49,400

d. $240 ($24,000 × 4% × 3/12)

e. $81,200 [$69,200 + ($80,000 × 30%) – $12,000]

f. $604,320 (same as total liabilities and stockholders’ equity)