CHAPTER 15

STATEMENT OF CASH FLOWS

DISCUSSION QUESTIONS

1. It is costly to accumulate the data needed and to prepare the statement of cash flows.

2. It focuses on the differences between net income and cash flows from operating activities, and the data

needed are generally more readily available and less costly to obtain than is the case for the direct method.

3. In a separate schedule of noncash investing and financing activities accompanying the statement of cash

flows.

6. a. $100,000 gain

b. Cash inflow of $600,000

c. The gain of $100,000 would be deducted from net income in determining net cash flow from operating

activities; $600,000 would be reported as cash flows from investing activities.

7. Cash flows from financing activities—issuance of bonds, $1,960,000 ($2,000,000 98%)

8. a. Cash flows from investing activities—Cash received from the disposal of fixed assets, $15,000

CHAPTER 15 Statement of Cash Flows

BASIC EXERCISES

BE 15–1

a. Investing d. Operating

BE 15–2

Net income ……………………………………………………………………………………….

$286,900

Adjustments to reconcile net income to net cash flow from

operating activities:

Net cash flow from operating activities ………………………………………………

$283,605

BE 15–3

Net income ……………………………………………………………………………………….

$75,800

Changes in current operating assets and liabilities:

3,380

Net cash flow from operating activities ………………………………………………

$66,730

BE 15–4

Cash flows from (used for) operating activities:

Net income……………………………………………………………….. $396,200

Adjustments to reconcile net income to net cash flow

from operating activities:

CHAPTER 15 Statement of Cash Flows

BE 15–5

The gain on the sale of land is subtracted from net income in the operating activities section.

Gain on sale of land …………………………………………………………………………… $ (30,000)

BE 15–6

Cash flows from (used for) financing activities:

BE 15–7

20Y2

20Y1

a. Net cash flow from operating activities ………………………….

$ 476,000

$ 455,000

Cash used to purchase property, plant, and

(341,600)*

(302,400)**

$ 134,400

$ 152,600

b. The change in free cash flow from $152,600 to $134,400 represents a decline.

Appendix 2 BE 15–8

Sales …………………………………………………………………………………………………….. $225,000

CHAPTER 15 Statement of Cash Flows

EXERCISES

EX. 15–1

There were net additions to the net loss reported on the income statement to convert the net

loss from the accrual basis to the cash basis. For example, depreciation is an expense in

The cash flows from operating activities detail is provided as follows for class discussion:

United Continental Holdings, Inc.

Cash Flows from Operating Activities

(Selected from Statement of Cash Flows)

(in millions)

Cash flows from (used for) operating activities:

Net income (loss)

$ (723)

Adjustments to reconcile net income (loss) to net cash flow

Depreciation and amortization

Special charges

389

Debt and lease discount amortization

Share based compensation

Other, net

251

Changes in current operating assets and liabilities:

Decrease (increase) in accounts receivable

(21)

Decrease (increase) in other assets

Increase (decrease) in accounts payable

285

Increase (decrease) in advanced ticket sales

246

Increase (decrease) in frequent flyer deferred revenue

Increase (decrease) in other liabilities

415

Net cash flow from operating activities

CHAPTER 15 Statement of Cash Flows

Ex. 15–2

a. Cash payment, $510,000

e.

Cash payment, $30,000

Cash receipt, $392,000

c. Cash receipt, $72,400

g.

Cash payment, $225,000

h.

Cash payment, $1,025,000

Ex. 15–3

a. operating

g.

financing

h.

investing

c. financing

financing

investing

Ex. 15–4

a. added

g.

added

h.

added

c. added

added

added

e. added

deducted

CHAPTER 15 Statement of Cash Flows

Ex. 15–5

a. Net income …………………………………………………………………….. $93,700

Adjustments to reconcile net income to net cash flow

from operating activities:

Depreciation …………………………………………………………….. 31,200

Changes in current operating assets and liabilities:

Net cash flow from operating activities…………………………….. $128,550

b. Cash flows from operating activities shows the cash inflow or outflow from a company’s

day–to-day operations. Net income reports the excess of revenues over expenses for a

company using the accrual basis of accounting. Revenues are recorded when they are

Ex. 15–6

a. Cash flows from (used for) operating activities:

Net income ………………………………………………………………………. $214,000

Adjustments to reconcile net income to net cash flow

from operating activities:

b. Yes. The amount of cash flows from operating activities reported on the statement of cash

flows is not affected by the method of reporting such flows.

CHAPTER 15 Statement of Cash Flows

Ex. 15–7

a. Cash flows from (used for) operating activities:

Net income ……………………………………………………………………. $508,000

Adjustments to reconcile net income to net cash flow

from operating activities:

Net cash flow from operating activities …………………………... $525,410

Note: The change in dividends payable would be used to adjust the dividends

declared in obtaining the cash paid for dividends in the financing activities section

of the statement of cash flows.

b. Cash flows from operating activities reports the cash inflow or outflow from a company’s

day–to-day operations. Net income reports the excess of revenues over expenses for a

accrual basis of accounting.

Ex. 15–8

Cash flows from investing activities:

Cash received from sale of equipment ……………………………………………………….. $105,900

Ex. 15–9

Cash flows from investing activities:

Cash received from sale of equipment ……………………………………………………….. $20,200

CHAPTER 15 Statement of Cash Flows

Ex. 15–10

Cash flows from (used for) investing activities:

Cash received from sale of land ………………………………………………………….. $ 106,800

Cash paid for purchase of land …………………………………………………………… (134,300)

Ex. 15–11

Dividends declared …………………………………………………………………………………. $1,200,000

Decrease in dividends payable ………………………………………………………………… 150,000

Dividends paid to stockholders during the year ……………………………………….. $1,350,000

Ex. 15–12

Cash flows from (used for) financing activities:

Ex. 15–13

Cash flows from (used for) investing activities:

Cash paid for purchase of land …………………………………………………………… $(246,000)

Ex. 15–14

Cash flows from (used for) financing activities:

CHAPTER 15 Statement of Cash Flows

Ex. 15–15

a. Net cash flow from (used for) operating activities ……………………… $357,500

Increase in accounts receivable …………………………..…………………… 14,300

Increase in prepaid expenses …………………………………………………… 2,970

Note to Instructors: The net income must be determined by working backward through the

“Cash flows from operating activities” section of the statement of cash flows. Hence,

those items that were added (deducted) to determine net cash flows from operating

activities must be deducted (added) to determine net income.

b. Curwen’s net income differed from cash flows from operations because of:

• $29,480 of depreciation expense which has no effect on cash flows from operating

activities,

CHAPTER 15 Statement of Cash Flows

Ex. 15–16

a.

National Beverage Co.

Cash Flows from Operating Activities

(in thousands)

Cash flows from (used for) operating activities:

Net income

$49,311

Adjustments to reconcile net income to net

Depreciation

Gain on disposal of property

Other items involving noncash expenses

1,383

Changes in current operating assets and

liabilities:

Net cash flow from operating activities

b. National Beverage is doing well financially. The company has positive earnings and

positive net cash flow from operating activities. The increase in accounts receivable is a

positive sign, indicating an increase in sales.

CHAPTER 15 Statement of Cash Flows

Ex. 15–17

a.

Olson-Jones Industries Inc.

Statement of Cash Flows

For the Year Ended December 31, 20Y2

Cash flows from (used for) operating activities:

Net income

$ 62

Adjustments to reconcile net income to net

26

liabilities:

Increase in accounts receivable

(6)

Increase in inventories

(18)

Increase in accounts payable

14

Net cash flow from operating activities

$ 38

Cash flows from (used for) investing activities:

Cash received from sale of land

Cash paid for purchase of equipment

(30)

Net cash flow from investing activities

Cash flows from (used for) financing activities:

Cash received from sale of common stock

$ 60

Net cash flow from financing activities

Net increase in cash

Cash balance, January 1, 20Y2

Cash balance, December 31, 20Y2

* Dividends = $24 – $5 = $19

b. Olson-Jones Industries Inc.’s net income was more than the cash flows from operations

because of:

• $26 of depreciation expense, which has no effect on cash.

• A $40 gain on the sale of land. The proceeds from this sale of $120, which include the

gain, are reported in the investing activities section of the statement of cash flows.

CHAPTER 15 Statement of Cash Flows

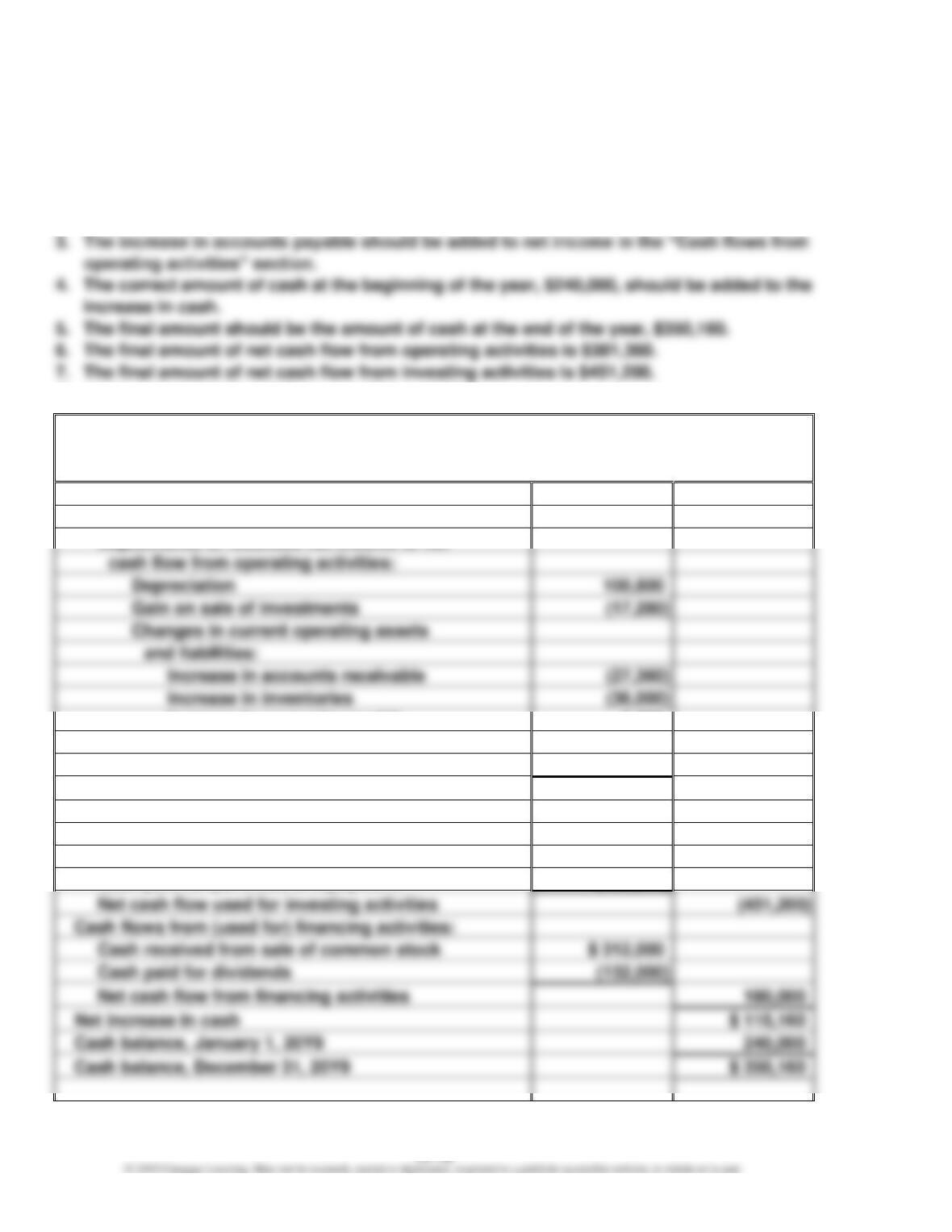

Ex. 15–18

1. The increase in accounts receivable should be deducted from net income in the “Cash

flows from operating activities” section.

2. The gain on the sale of investments should be deducted from net income in the “Cash

flows from operating activities” section.

A correct statement of cash flows would be as follows:

Shasta Inc.

Statement of Cash Flows

For the Year Ended December 31, 20Y9

Cash flows from (used for) operating activities:

Net income

$ 360,000

Adjustments to reconcile net income to net

and liabilities:

Increase in accounts receivable

Increase in inventories

Increase in accounts payable

3,600

Decrease in accrued expenses

payable

(2,400)

Net cash flow from operating activities

$ 381,360

Cash flows from (used for) investing activities:

Cash received from sale of investments

$ 240,000

Cash paid for purchase of land

(259,200)

Cash paid for purchase of equipment

(432,000)

Net cash flow used for investing activities

(451,200)

Cash flows from (used for) financing activities:

Cash received from sale of common stock

$ 312,000

Cash paid for dividends

(132,000)

Net cash flow from financing activities

Net increase in cash

$ 110,160

Cash balance, January 1, 20Y9

CHAPTER 15 Statement of Cash Flows

Appendix 2 Ex. 15–19

a. Sales ………………………………………………………………………………………. $753,500

Decrease in accounts receivable balance …………………………………. 48,400

Cash received from customers ………………………………………………… $801,900

Appendix 2 Ex. 15–20

a. Cost of goods sold ………………………………………………………………….. $1,031,550

Decrease in accounts payable …………………………..……………………… 9,660

CHAPTER 15 Statement of Cash Flows

Appendix 2 Ex. 15–21

a. Cash flows from (used for) operating activities:

Cash received from customers …………………………………. $ 522,7601

Computations:

1. Sales…………………………………………………………………………………………… $511,000

Decrease in accounts receivable ………………………………………………….. 11,760

Cash received from customers …………………………………………………….. $522,760

2. Cost of goods sold ………………………………………………………………………. $290,500

Increase in inventories ………………………………………………………………… 3,920

3. Operating expenses other than depreciation …………………………………. $105,000

4. Income tax expense …………………………..………………………………………… $ 21,700

Add decrease in income tax payable …………………………………………….. 2,660

Cash payments for income taxes …………………………………………………. $ 24,360

CHAPTER 15 Statement of Cash Flows

Appendix 2 Ex. 15–22

Cash flows from (used for) operating activities:

Cash received from customers ……………………………………… $ 440,4401

Computations:

1. Sales ……………………………………………………….…………………………….. $445,500

Increase in accounts receivable …………………………..………………….. (5,060)

Cash received from customers ……………………………………………….. $440,440

2. Cost of goods sold …………………………………………………………………. $154,000

3. Operating expenses other than depreciation ……………………………. $115,280

CHAPTER 15 Statement of Cash Flows

PROBLEMS

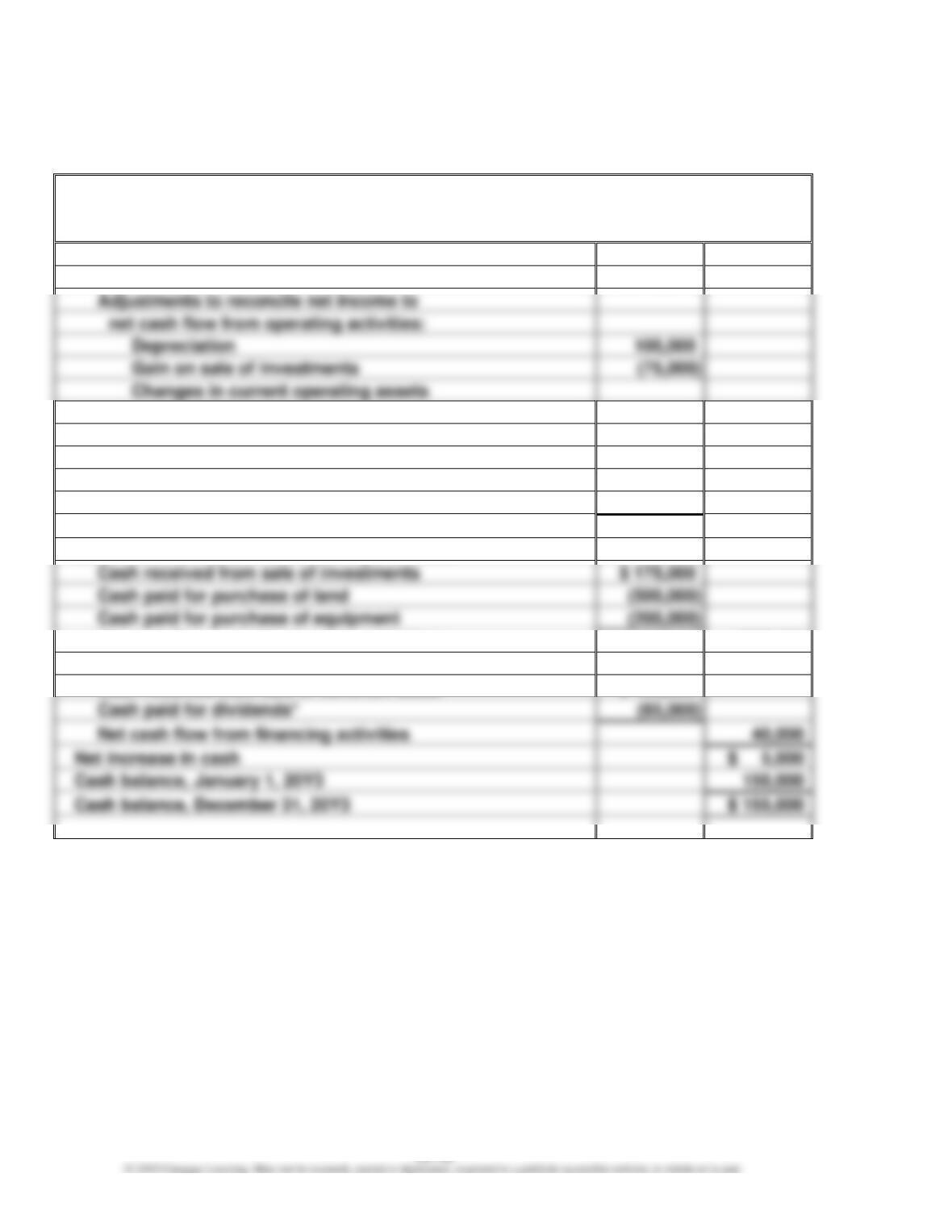

Prob. 15–1A

Livers Inc.

Statement of Cash Flows

For the Year Ended December 31, 20Y3

Cash flows from (used for) operating activities:

Net income

$ 500,000

Adjustments to reconcile net income to

(75,000)

and liabilities:

Increase in accounts receivable

(50,000)

Increase in inventories

(20,000)

Increase in accounts payable

40,000

Decrease in accrued expenses payable

(5,000)

Net cash flow from operating activities

$ 490,000

Cash flows from (used for) investing activities:

Cash received from sale of investments

$ 175,000

Cash paid for purchase of land

Cash paid for purchase of equipment

(200,000)

Net cash flow used for investing activities

(525,000)

Cash flows from (used for) financing activities:

Cash received from sale of common stock

$ 125,000

Cash paid for dividends*

Net cash flow from financing activities

40,000

Net increase in cash

$ 5,000

Cash balance, January 1, 20Y3

Cash balance, December 31, 20Y3

$ 155,000

* Cash paid for dividends = $90,000 + $25,000 – $30,000 = $85,000

CHAPTER 15 Statement of Cash Flows

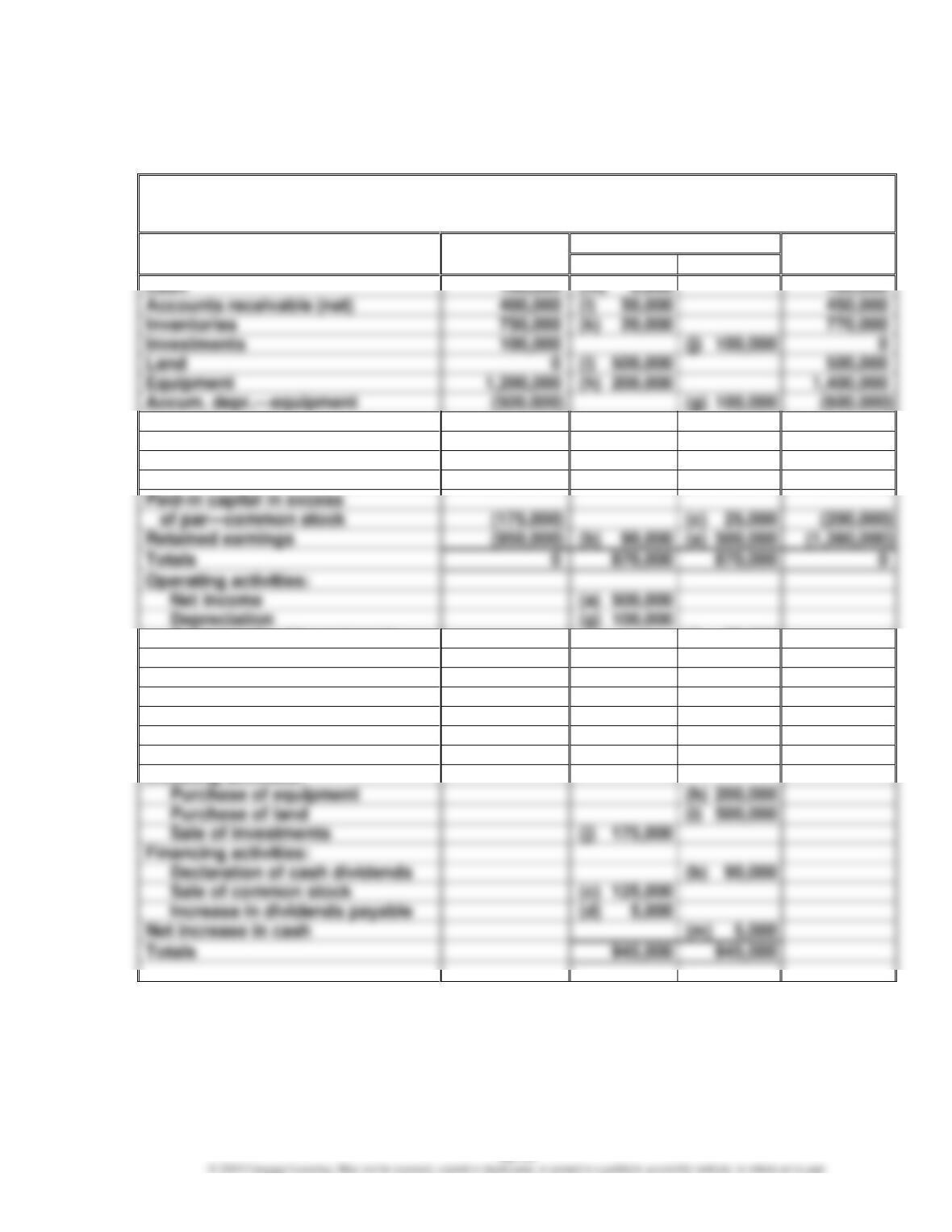

Prob. 15–1A (Concluded)

(Optional)

Livers Inc.

Spreadsheet (Work Sheet) for Statement of Cash Flows

For the Year Ended December 31, 20Y3

Balance,

Transactions

Balance,

Account Title

Dec. 31, 20Y2

Debit

Credit

Dec. 31, 20Y3

Accounts receivable (net)

(j) 100,000

(i) 500,000

(h) 200,000

1,400,000

Accum. depr.—equipment

(500,000)

(g) 100,000

(600,000)

Accounts payable

(300,000)

(f) 40,000

(340,000)

Accrued expenses payable

(50,000)

(e) 5,000

(45,000)

Dividends payable

(25,000)

(d) 5,000

(30,000)

Common stock, $4 par

(600,000)

(c) 100,000

(700,000)

Paid-in capital in excess

of par—common stock

(175,000)

(c) 25,000

(200,000)

Retained earnings

(950,000)

(b) 90,000

(a) 500,000

870,000

Operating activities:

Net income

(a) 500,000

Depreciation

(g) 100,000

Gain on sale of investments

(j) 75,000

Increase in accounts

receivable

(l) 50,000

Increase in inventories

(k) 20,000

Increase in accounts payable

(f) 40,000

Decrease in accrued

expenses payable

(e) 5,000

Investing activities:

Purchase of equipment

(h) 200,000

Purchase of land

(i) 500,000

Sale of investments

(j) 175,000

Financing activities:

Declaration of cash dividends

(b) 90,000

Sale of common stock

(c) 125,000

Increase in dividends payable

(d) 5,000

Net increase in cash

(m) 5,000

Totals

Note to Instructors: The letters in the debit and credit columns are included for

reference purposes only.

CHAPTER 15 Statement of Cash Flows

Prob. 15–2A

Yellow Dog Enterprises Inc.

Statement of Cash Flows

For the Year Ended December 31, 20Y8

Cash flows from (used for) operating activities:

Net income

$ 250,000

Adjustments to reconcile net income to

Decrease in accounts receivable

20,000

Increase in inventories

(70,000)

Increase in prepaid expenses

(10,000)

Increase in accounts payable

25,000

Net cash flow from operating activities

$ 350,000

Cash flows from (used for) investing activities:

Cash paid for equipment

$ (420,000)

Net cash flow used for investing activities

Cash flows from (used for) financing activities:

Cash received from sale of common stock

Cash paid for dividends

Cash paid to retire mortgage note payable

Net cash flow from financing activities

Net decrease in cash

Cash balance, January 1, 20Y8

Cash balance, December 31, 20Y8

$ 95,000

Note to Instructors: The disposal of fully depreciated equipment is not included in the cash

flow statement because there is no associated cash flow. This transaction strictly involves

the removal of $90,000 from the equipment and accumulated depreciation—equipment

accounts.

CHAPTER 15 Statement of Cash Flows

Prob. 15–2A (Concluded)

(Optional)

Yellow Dog Enterprises Inc.

Spreadsheet (Work Sheet) for Statement of Cash Flows

For the Year Ended December 31, 20Y8

Account Title

Balance,

Dec. 31, 20Y7

Transactions

Balance, Dec.

31, 20Y8

Debit

Credit

Cash

110,000

(l) 15,000

95,000

Accounts receivable (net)

280,000

(k) 20,000

Inventories

450,000

Prepaid expenses

15,000

Equipment

800,000

(h) 420,000

(g) 90,000

1,130,000

Accum. depr.—equipment

(190,000)

(g) 90,000

(235,000)

Accounts payable

(75,000)

(e) 25,000

(100,000)

Mortgage note payable

(500,000)

(d) 500,000

0

Common stock, $10 par

(200,000)

(c) 300,000

(500,000)

Paid-in capital in excess

of par—common stock

(100,000)

(c) 300,000

(400,000)

Retained earnings

(580,000)

(b) 45,000

(a) 250,000

(785,000)

Totals

0

1,135,000

1,135,000

0

Operating activities:

Net income

Depreciation

Decrease in accts. receivable

Increase in inventories

(j) 70,000

Increase in prepaid expenses

(i) 10,000

Increase in accounts payable

Investing activities:

Purchase of equipment

(h) 420,000

Financing activities:

Payment of cash dividends

(b) 45,000

Sale of common stock

Payment of mortgage note

(d) 500,000

Net decrease in cash

Totals

1,045,000

1,045,000

Note to Instructors: The letters in the debit and credit columns are included for reference

purposes only.

CHAPTER 15 Statement of Cash Flows

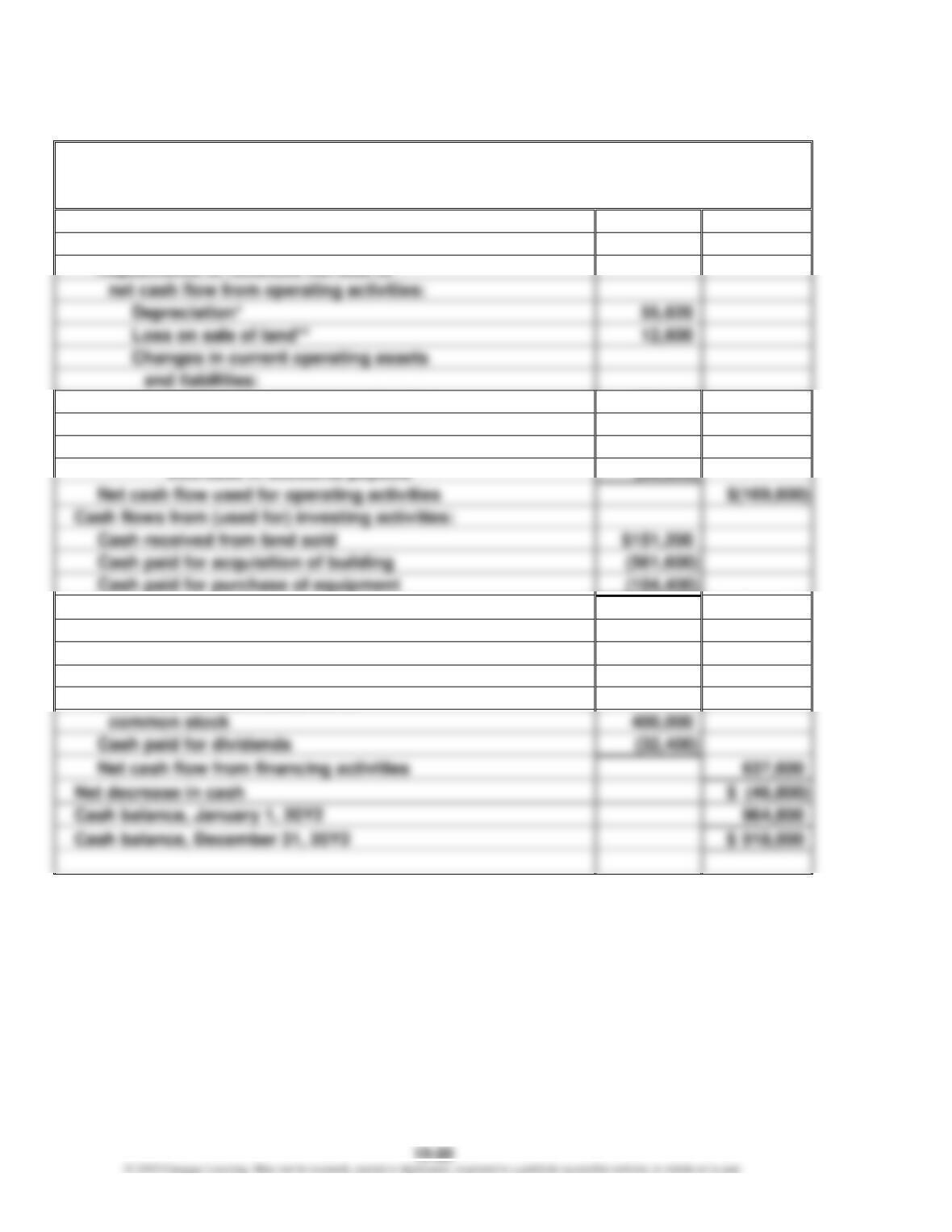

Prob. 15–3A

Whitman Co.

Statement of Cash Flows

For the Year Ended December 31, 20Y2

Cash flows from (used for) operating activities:

Net loss

$ (35,320)

Adjustments to reconcile net loss to

net cash flow from operating activities:

Increase in accounts receivable

(66,960)

Increase in inventories

(105,480)

Decrease in prepaid expenses

5,760

Decrease in accounts payable

(35,820)

Net cash flow used for operating activities

Cash flows from (used for) investing activities:

Cash received from land sold

$151,200

Cash paid for acquisition of building

(561,600)

Cash paid for purchase of equipment

(104,400)

Net cash flow used for investing activities

(514,800)

Cash flows from (used for) financing activities:

Cash received from issuance of

bonds payable

$270,000

Cash received from issuance of

common stock

Cash paid for dividends

(32,400)

Net cash flow from financing activities

Net decrease in cash

Cash balance, January 1, 20Y2

Cash balance, December 31, 20Y2

* Depreciation = $26,280 + $29,340

** Loss on sale of land = $151,200 – $163,800