Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

481

CHAPTER 15

CAPITAL INVESTMENT ANALYSIS

CLASS DISCUSSION QUESTIONS

1. The principal objections to the use of the

average rate of return method are its failure

to consider the expected cash flows from the

proposals and the timing of these flows.

4. The cash payback period ignores the cash

flows that occur after the cash payback peri-

od; the net present value method includes

all cash flows in the analysis. The cash pay-

back period also ignores the time value of

money, which is included by the net present

value method.

5. A one-year payback will not equal a 100%

average rate of return because the payback

period is based on cash flows; the average

rate of return is based on income. The de-

preciation on the project will prevent the two

methods from being equal.

8. The $115,000 net present value indicates

the proposal is desirable because the pro-

posal is expected to recover the investment

and provide more than the minimum rate of

return.

9. The net present values indicate both projects

are desirable but not necessarily equal in

desirability. The present value index can be

used to compare the two projects. For

the method assumes the cash received from

the proposal during its useful life will be re-

invested at the rate of return used to com-

pute the present value of the proposal. This

assumption may not always be reasonable.

11. The computations for the internal rate of

return method are more complex than those

for the methods that ignore present value.

Also, the method assumes the cash received

from the proposal during its useful life will be

reinvested at the internal rate of return. This

assumption may not always be reasonable.

12. Allowable deductions for depreciation.

should be considered.

482

16. Monsanto indicated that it recognized the

market was demanding higher product quality

that could be achieved only with a large

investment in process control technology

Monsanto indicated the following six consid-

erations in making its investment:

a. After-tax cash flows

b. Labor savings

483

E15–1

Testing Diagnostic

Equipment Software

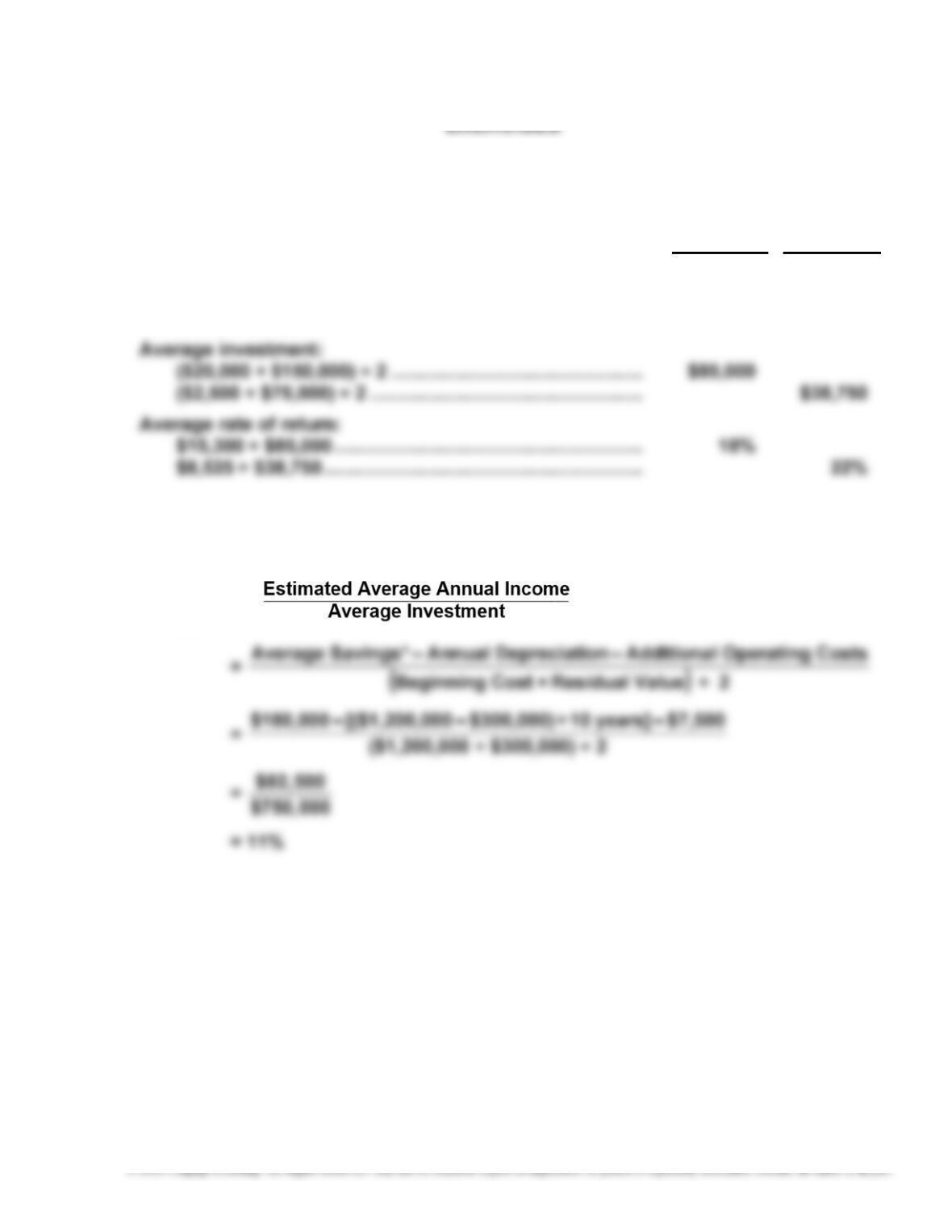

Estimated average annual income:

$122,400 ÷ 8 years.......................................................... $15,300

$42,625 ÷ 5 years ........................................................... $ 8,525

E15–2

Return of

Rate

Average

=

*The effect of the savings in wages expense is an increase in income.

484

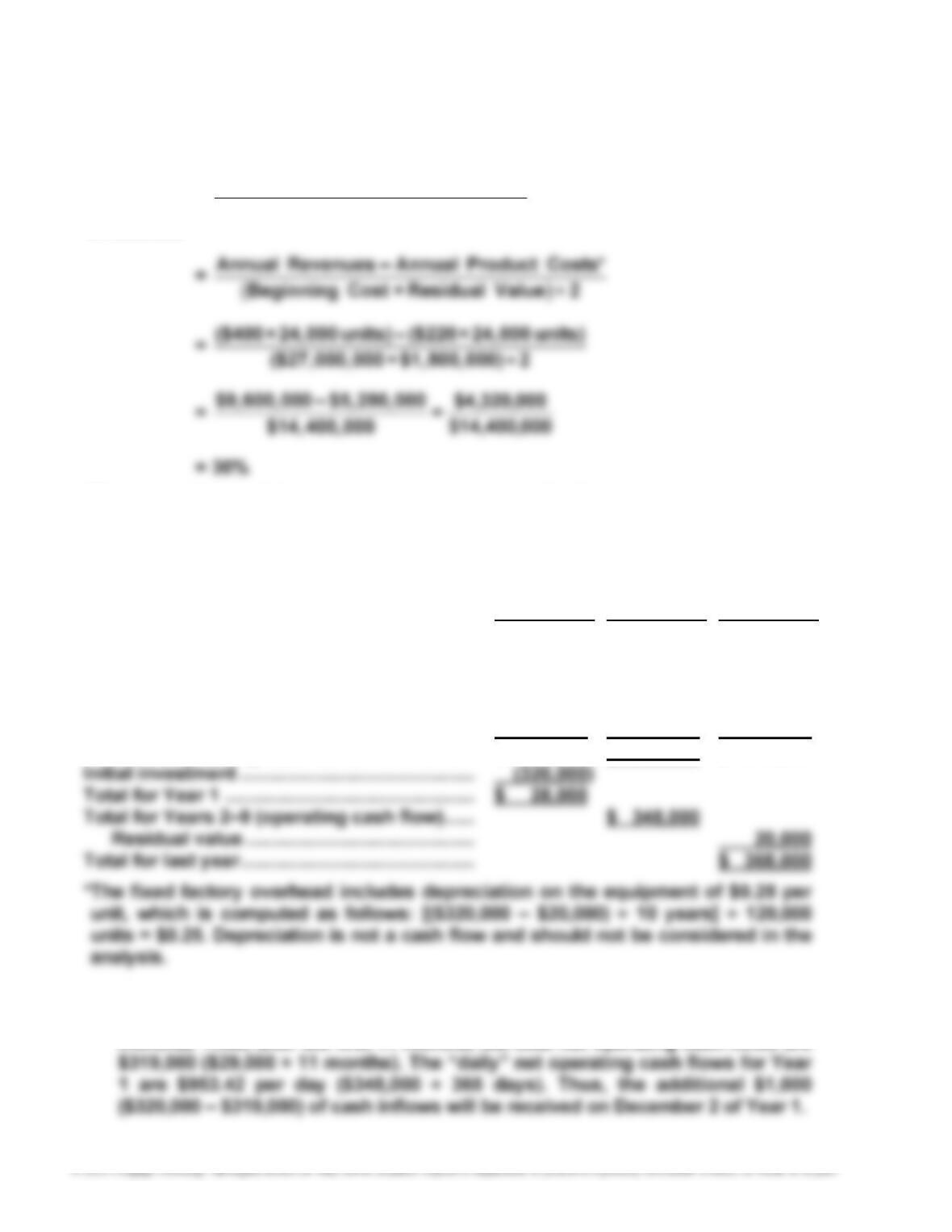

E15–3

Return

on

Investment

= Investment Average

Income AnnualAverageEstimated

*The depreciation of the equipment is included in the factory overhead cost per

unit.

E15–4

a. Year 1 Years 2–9 Last Year

Operating cash flows:

Annual revenues (120,000 units × $9) ...... $1,080,000 $1,080,000 $1,080,000

Selling expenses (15% × $1,080,000) ........ (162,000) (162,000) (162,000)

Cost to manufacture

(120,000 units × $4.75)*......................... (570,000) (570,000) (570,000)

Net operating cash flows ..................... $ 348,000 $ 348,000 $ 348,000

b. The cash payback will occur on December 2 of Year 1. Net operating cash

flows for Year 1 are $348,000, which is $29,000 per month ($348,000 ÷ 12

485

E15–5

Location 1: $500,000 ÷ $125,000 = 4-year cash payback period.

Location 2: Three-year cash payback period, as indicated next.

Net Cash Cumulative

Flow Net Cash Flows

Year 1 ............................................................... $200,000 $200,000

E15–6

a. The Shampoo/Conditioner product line is recommended, based on its shorter

cash payback period. The cash payback period for both products can be

determined using the following schedule:

Initial investment: $2,800,000

Shampoo/Conditioner Body Wash

Net Cash Cumulative Net Net Cash Cumulative Net

Flow Cash Flows Flow Cash Flows

Year 1 $700,000 $ 700,000 $400,000 $ 400,000

Year 2 650,000 1,350,000 400,000 800,000

Year 3 550,000 1,900,000 400,000 1,200,000

b. The cash payback periods are different between the two product lines

because Shampoo/Conditioner earns cash faster than does Body Wash. The

cash payback method emphasizes the initial years’ net cash flows in deter-

less net cash flows in the initial years.

486

E15–6, Concluded

c. The cash payback would be 4 years, 8 months, determined as follows:

At the end of Year 4 the cumulative net cash flows for Shampoo/Conditioner

E15–7

a.

Present Value Net Cash Present Value of

Year of $1 at 10% Flow Net Cash Flow

1 0.909 $ 50,000 $ 45,450

2 0.826 45,000 37,170

487

E15–8

a.

20Y4 20Y5 20Y6 20Y7 20Y8

Revenues ............. $ 35,000 $ 35,000 $ 35,000 $ 35,000 $ 35,000

Driver salary ........ (25,000) (26,000) (27,000) (28,000) (29,000)

Operating costs ... (4,500) (4,500) (4,500) (4,500) (4,500)

b.

Net Cash Flow Present Value of Present Value of

Year [from part (a)] $1 at 12% Net Cash Flow

20Y4 $5,500 0.893 $ 4,911.50

20Y5 4,500 0.797 3,586.50

488

E15–9

a.

(in millions)

Annual revenues .................................................................................. $7.5

Total expenses ..................................................................................... $3.0

b.

(in millions,

except present

value factor)

Annual net cash flow ........................................................................... $ 6.5

Present value of an annuity of $1 at 10% for 20 periods .................. × 8.5136

489

E15–10

a. Annual cash inflows:

Hours of operation ...................................... 1,850

Revenue per hour ........................................ × $140

Revenue per year ........................................ $ 259,000

Annual cash outflows:

Hours of operation ...................................... 1,850

Fuel cost per hour ................................... $48

b. Annual net cash flow (at the end of each of five years) ................... $ 92,000

Present value of annuity of $1 at 10% for five periods (Exhibit 5) .. × 3.791

490

E15–11

a. Revenues (3,600 × 300 days × $450) ............................................ $ 486,000,000

Less: Variable expenses (3,600 × 300 days × $90) .................... (97,200,000)

Fixed expenses (other than depreciation) ....................... (100,000,000)

Annual net cash flows ................................................................... $ 288,800,000

b. Present value of annual net cash flows ($288,800,000 × 5.650) $ 1,631,720,000

E15–12

a. Present Value Index = Total Present Value of Net Cash Flow

Amount to Be Invested

Present value index of Somerset = $441,000

$450,000 = 0.98

491

E15–13

a. Annual net cash flows by machine:

Stitching: $135,000 = 7,500 hours × 60 incremental baseballs × $0.30

Golf Ball: $240,000 = 6,000 hrs. × $40 labor cost saved per hour

Stitching Machine

Annual net cash flows (at the end of each of 8 years) ..................... $135,000

Golf Ball Machine

Annual net cash flows (at the end of each of 8 years) ..................... $ 240,000

Present value of an annuity of $1 at 15% for 8 years (Exhibit 5) ..... × 4.487

b. Present Value Index = Invested Be to Amount

Flows Cash Net of ValuePresent Total

Present value index of the stitching machine: 600,484$

745,605$ = 1.25

492

E15–14

a. Average rate of return on investment: 1,700,000*

($10,000,000 + $2,000,000) ÷ 2 = 28.3%

*The annual income of $1,700,000 is equal to the annual cash flow of $2,500,000

less the annual depreciation expense of $800,000 [($10,000,000 – $2,000,000) ÷

10 years]

E15–15

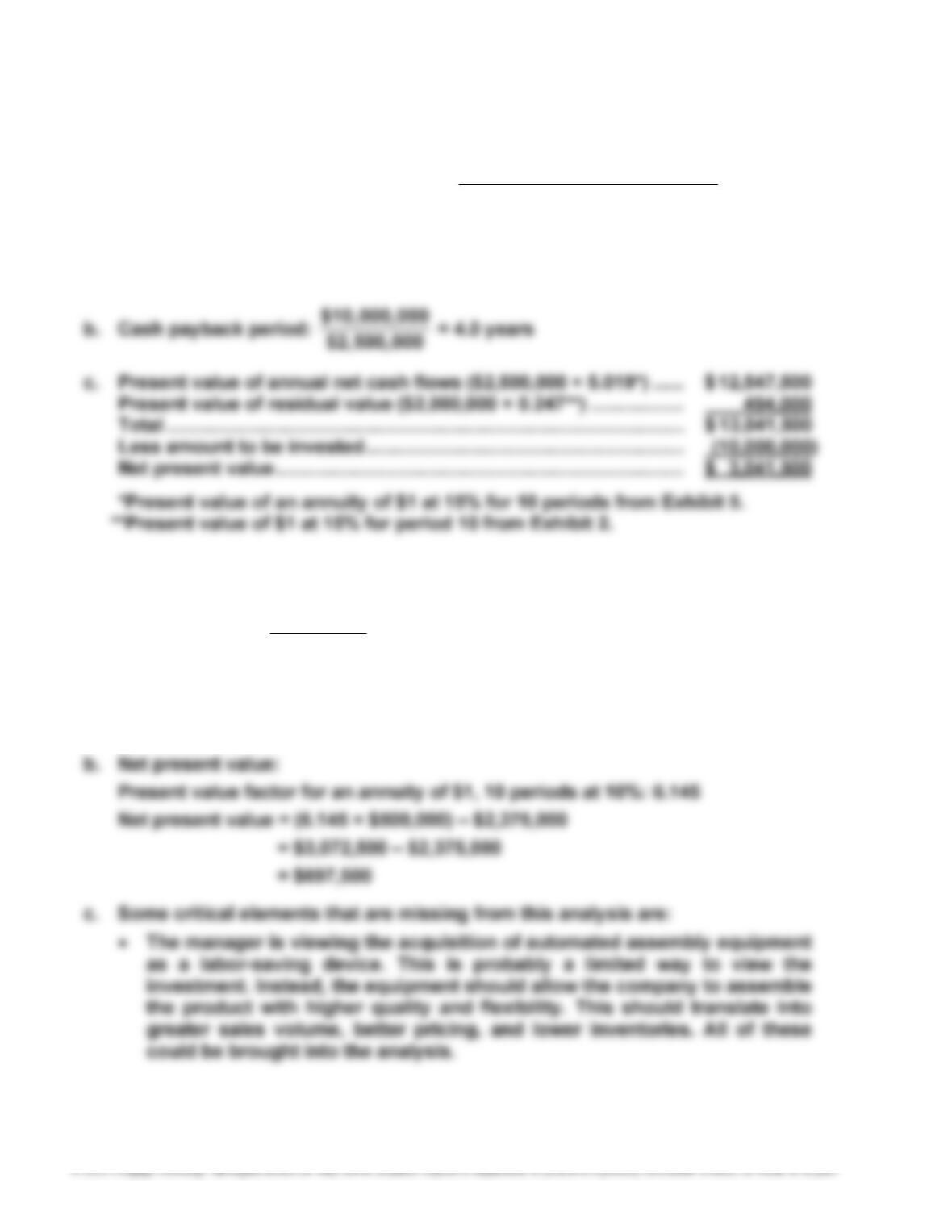

a. Payback period: $500,000

$2,375,000 = 4.75 years

Note: Assuming the cash flows evenly throughout the year, the cash payback

would be 4 years, 9 months or 4.75 years.

493

E15–15, Concluded

The cost of the automated assembly equipment does not stop with the

initial purchase price and installation costs. The equipment will require the

company to hire engineers and support personnel to keep the machines

running, to program the software, and to debug new programs. The

E15–16

a. Present Value Factor for an

Annuity of $1 for 8 Periods = Amount to Be Invested

Annual Net Cash Flow

E15–17

Periods 10 for $1 of Annuity

an for Factor luePresent Va = Flows Cash Net Annual

Invested Be to Amount

494

E15–18

a. Delivery Truck

Cash received from additional deliveries (90,000 bags × $0.35) ..... $31,500

Cash used for operating expenses (24,000 miles × $0.55) .............. (13,200)

Net cash flows for delivery truck ....................................................... $ 18,300

Bagging Machine

Direct labor savings (2.5 hrs. per day × $20 per hr. × 240 days per yr.) = $12,000

=

Amount to Be Invested

Annual Net Cash Flows

b. To: Management

Re: Investment Recommendation

An internal rate of return analysis was performed for the delivery truck and

bagging machine investments. The internal rate of return for the bagging

Present Value Factor for an

Annuity of $1 for 5 Periods

495

E15–19

a. Present value of annual net cash flows ($620,000 × 5.650*) ............ $ 3,503,000

Amount to be invested ........................................................................ (3,810,000)

Net present value ................................................................................ $ (307,000)

*Present value of an annuity of $1 at 12% for 10 periods from text Exhibit 5.

E15–20

With an expected useful life of eight years, the cash payback period could not be

greater than eight years. This would indicate the cost of the initial investment

would not be recovered during the useful life of the asset. However, there would

496

E15–21

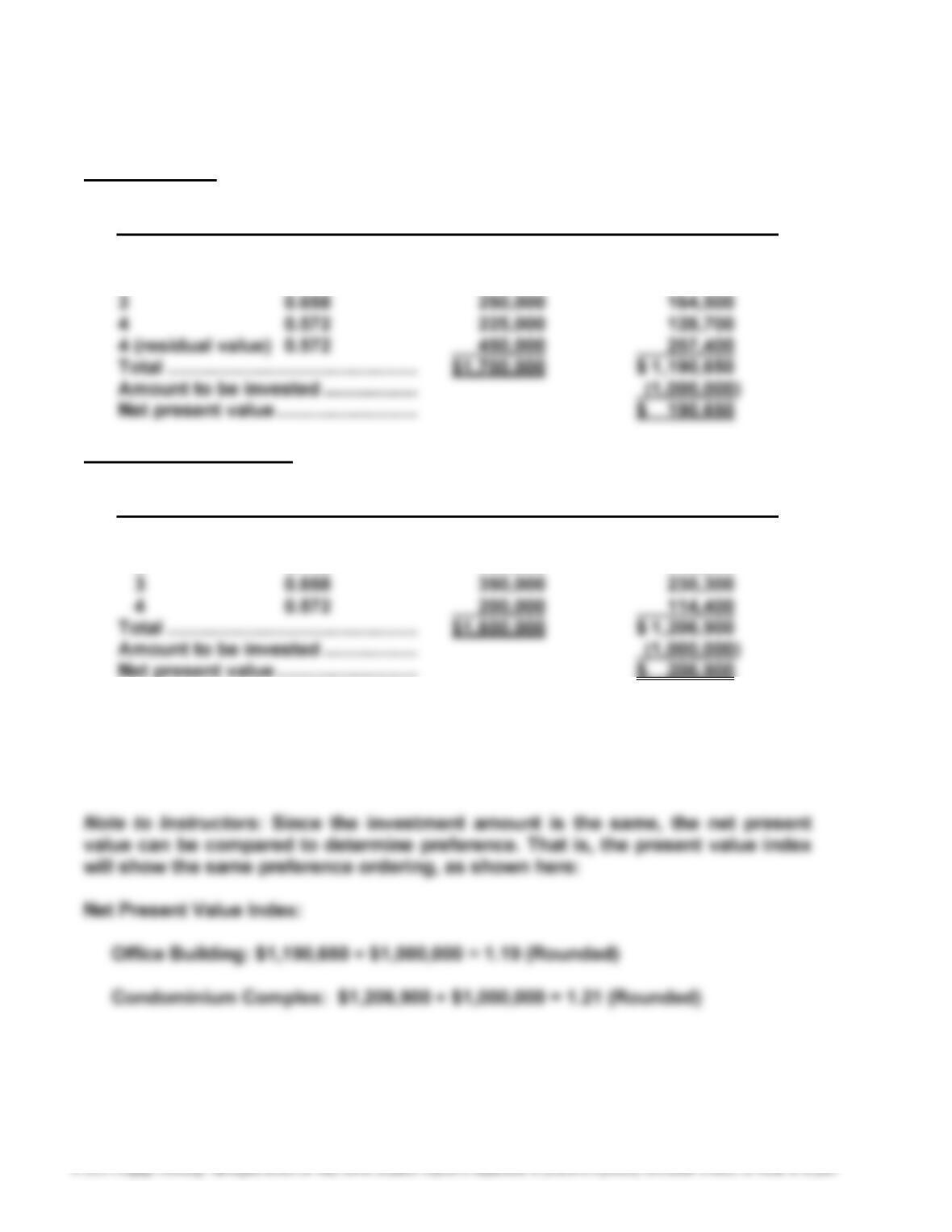

Office Building

Present Value Net Cash Present Value of

Year of $1 at 15% Flow Net Cash Flow

1 0.870 $ 475,000 $ 413,250

2 0.756 300,000 226,800

Condominium Complex

Present Value Net Cash Present Value of

Year of $1 at 15% Flow Net Cash Flow

1 0.870 $ 600,000 $ 522,000

2 0.756 450,000 340,200

Net present value ........................... $ 206,900

The net present value of both projects is positive; thus, both proposals are ac-

ceptable. However, the net present value of the condominium complex exceeds

that of the office building. Thus, the condominium complex should be preferred if

there is enough investment money for only one of the projects.

497

E15–22

a.

Blending Equipment

Equal annual cash flows for Years 1–4 ............................... $ 18,000

Present value of a $1 annuity at 12% for four periods ....... × 3.037

Computer System

Equal annual cash flows for Years 1–4 ............................... $ 10,000

Present value of a $1 annuity at 12% for four periods ....... × 3.037

b.

Present value index of blending equipment: 000,45$

846,57$ = 1.29 (Rounded)

498

PROBLEMS

P15–1

1. a. Average rate of return for both projects:

()

2÷ 0$+000,800$

5÷ 000,330$ = 000,400$

000,66$ = 16.5%

b. Net present value analysis:

Present Value of

Net Cash Flows Net Cash Flows

Distribution Internet Distribution Internet

Present Value of Center Tracking Center Tracking

Year $1 at 15% Expansion Technology Expansion Technology

1 0.870 $ 226,000 $ 360,000 $ 196,620 $ 313,200

2. The report to the capital investment committee can take many forms. The

report should, as a minimum, present the following points:

a. Both projects offer the same average annual rate of return.

499

P15–2

1. a. Cash payback period for both products: 2 years (the year in which accu-

mulated net cash flows equal $200,000), shown as follows:

Primitive Camping Lakeside Fishing

Net Cash Cumulative Net Cash Cumulative

Year Flows Net Cash Flow Year Flows Net Cash Flow

b. Net present value analysis:

Present Value of Present Value of

Net Cash Flow Net Cash Flow

Primitive Lakeside Primitive Lakeside

Year $1 at 10% Camping Fishing Camping Fishing

1 0.909 $110,000 $ 94,000 $ 99,990.00 $ 85,446.00

2. The report can take many forms and should include the following four points:

a. Both products offer the same total net cash flows.

b. Both products offer the same cash payback period.