489

CHAPTER 15

CAPITAL INVESTMENT ANALYSIS

CLASS DISCUSSION QUESTIONS

1. The principal objections to the use of the

average rate of return method are its failure

to consider the expected cash flows from the

proposals and the timing of these flows.

4. The cash payback period ignores the cash

flows that occur after the cash payback peri-

od, while the net present value method in-

cludes all cash flows in the analysis. The

cash payback period also ignores the time

value of money, which is included by the net

present value method.

two methods from being equal.

6. The cash payback period ignores cash flows

occurring after the payback period, which

will often include large residual values.

7. The majority of the cash flows of a new mo-

tion picture are earned within two years of

release. Thus, the time value of money

9. The net present values indicate that both

projects are desirable, but not necessarily

equal in desirability. The present value index

can be used to compare the two projects.

method assumes that the cash received

from the proposal during its useful life will be

reinvested at the rate of return used to com-

pute the present value of the proposal. This

assumption may not always be reasonable.

11. The computations for the internal rate of

return method are more complex than those

12. Allowable deductions for depreciation.

13. The life of the proposal with the longer life

can be adjusted to a time period that is

equal to the life of the proposal with the

shorter life.

14. The major advantages of leasing are that it

16. Monsanto indicated that it recognized that

the market was demanding higher product

quality that could be achieved only with a

Monsanto indicated the following considera-

tions in making its investment:

a. After-tax cash flows

491

EXERCISES

E15–1

Testing Diagnostic

Equipment Software

Estimated average annual income:

$243,000 ÷ 6 years…………………………………………………. $40,500

$88,400 ÷ 8 years ………………………………………………….. $11,050

E15–2

Return of

Rate

Average

=

Investment Average

Income Annual AverageEstimated

492

E15–3

Return of

Rate

Average

=

Investment Average

Income AnnualAverageEstimated

*The depreciation of the equipment is included in the factory overhead cost per

unit.

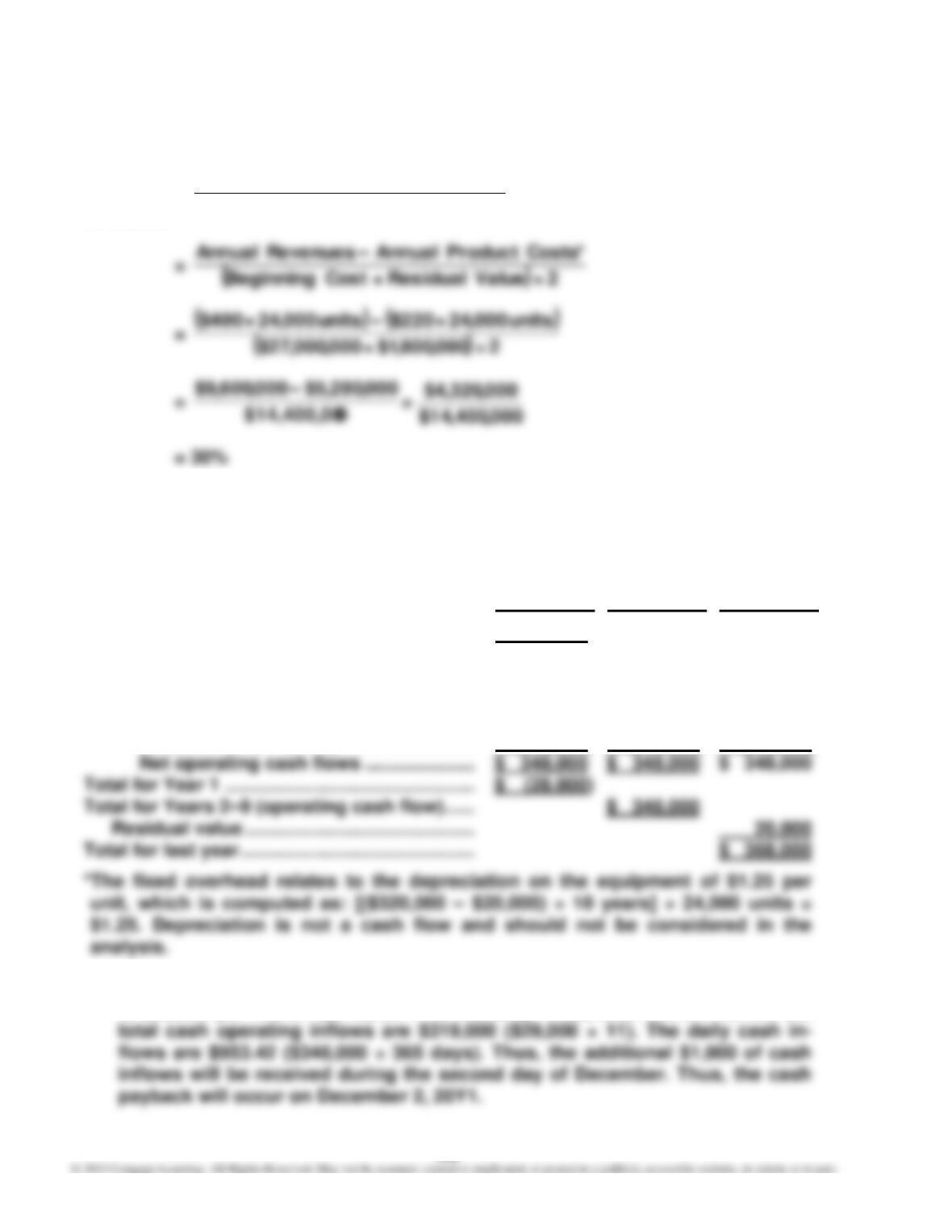

E15–4

a. Year 1 Years 2–9 Last Year

Initial investment ……………………………………… $ (320,000)

Operating cash flows:

Annual revenues (120,000 units × $9) …… $1,080,000 $1,080,000 $1,080,000

Selling expenses (15% × $1,080,000) …….. (162,000) (162,000) (162,000)

Cost to manufacture

(120,000 units × $4.75)*……………………. (570,000) (570,000) (570,000)

b. December 2, 20Y1. Operating cash flows for the first year are $348,000, which

is $29,000 per month ($348,000 ÷ 12 months). Thus, after eleven month, the

493

E15–5

Location 1: $350,000 ÷ $70,000 = 5-year cash payback period.

Location 2: 4-year cash payback period, as indicated below.

Net Cash Cumulative

Flows Net Cash Flows

Year 1 ……………………………………………………… $125,000 $125,000

E15–6

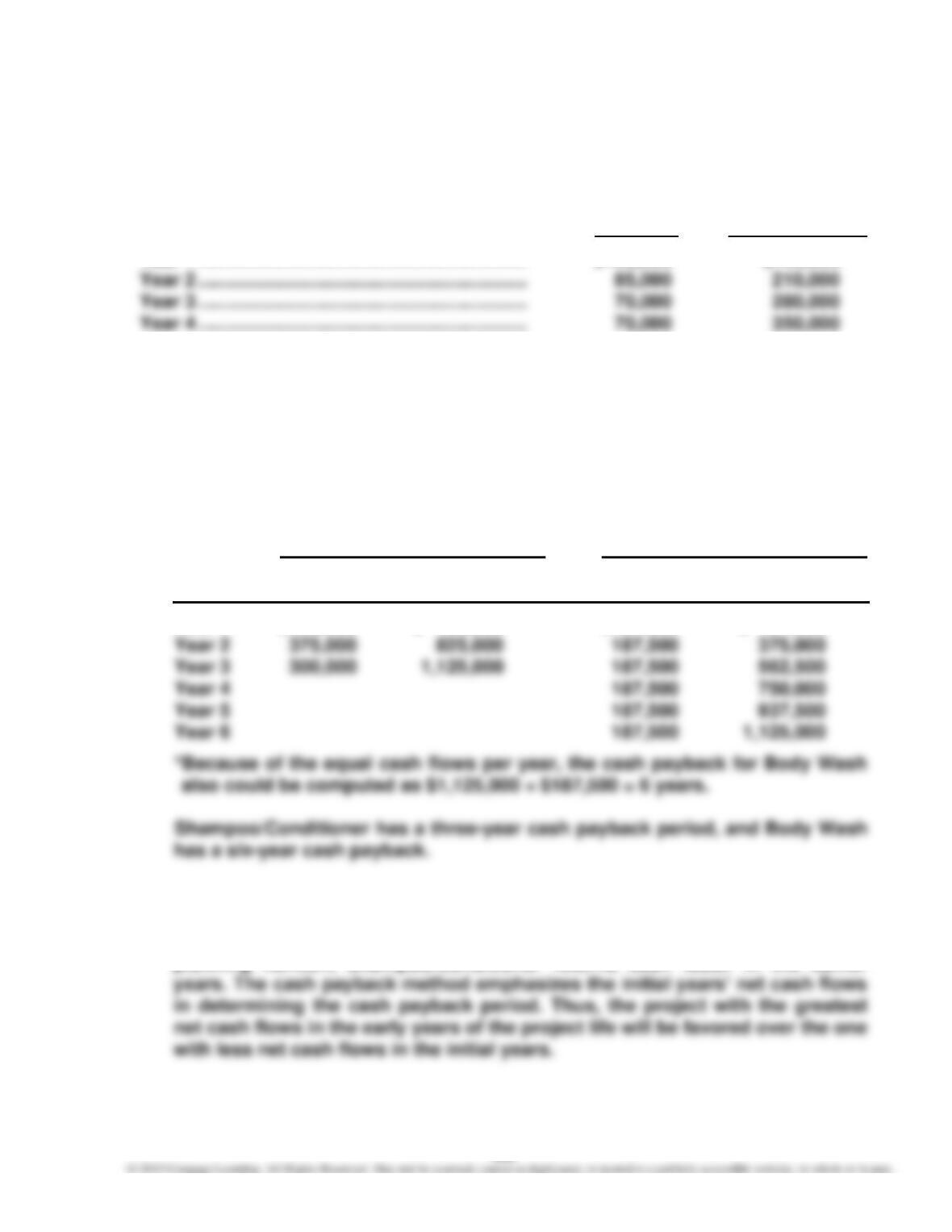

a. The Shampoo/Conditioner product line is recommended, based on its shorter

cash payback period. The cash payback period for both products can be de-

termined using the following schedule:

Initial investment: $1,125,000

Shampoo/Conditioner Body Wash*

Net Cash Cumulative Net Net Cash Cumulative Net

Flows Cash Flows Flows Cash Flows

Year 1 $450,000 $ 450,000 $187,500 $ 187,500

b. The cash payback periods are different between the two product lines be-

cause Shampoo/Conditioner earns cash faster than does Body Wash. Even

though both products earn the same total net cash flow over the eight-year

planning horizon, Shampoo/Conditioner returns cash faster in the earlier

494

E15–6, Concluded

c. The cash payback would be 3 years, 4 months, determined as follows:

At the end of Year 3, the cumulative net cash flows for Shampoo/Conditioner

would be $1,075,000 ($450,000 + $375,000 + $250,000). Assuming the cash

E15–7

a.

Present Value Net Cash Present Value of

Year of $1 at 20% Flows Net Cash Flows

1 0.833 $300,000 $ 249,900

2 0.694 250,000 173,500

495

E15–8

a.

20Y4 20Y5 20Y6 20Y7 20Y8

Revenues …………. $ 60,000 $ 60,000 $ 60,000 $ 60,000 $ 60,000

Driver’s salary ….. (30,000) (32,000) (34,000) (36,000) (38,000)

b.

Net Cash Flows Present Value of Present Value of

Year [from part (a)] $1 at 12% Net Cash Flows

20Y4 $29,000 0.893 $ 25,897

20Y5 27,000 0.797 21,519

20Y6 25,000 0.712 17,800

20Y7 23,000 0.636 14,628

20Y8 31,000 0.567 17,577

496

E15–9

a.

(in millions)

Annual revenues ………………………………………………………………………. $15

Total expenses …………………………………………………………………………. $6

b.

(in millions,

except present

value factor)

Annual net cash flow ……………………………………………………….……….. $ 13

Present value of an annuity of $1 at 10% for 20 periods ……………… × 8.5136

497

E15–10

a. Cash inflows:

Hours of operation ……………………………….. 1,850

Revenue per hour …………………………………. × $140

Revenue per year …………………………………. $ 259,000

Cash outflows:

Annual net cash flow ……………………………. $ 92,000

b. Annual net cash flow (at the end of each of five years) ………………. $ 92,000

Present value of annuity of $1 at 10% for five periods (Exhibit 2) .. × 3.791

Present value of annual net cash flows …………………………………….. $ 348,772

Less amount to be invested ……………………………………………………… (315,000)

Net present value …………………………………………………………………….. $ 33,772

498

E15–11

a. Revenues (3,600 × 300 days × $450) …………………………………….. $ 486,000,000

Less: Variable expenses (3,600 × 300 days × $90) ……………….. (97,200,000)

Fixed expenses (other than depreciation) ………………….. (100,000,000)

Annual net cash flows …………………………………………………………. $ 288,800,000

E15–12

Present Value Index =

Invested BetoAmount

Flows CashNetof ValuePresent Total

499

E15–13

a. Annual net cash flows by machine:

Stitching: $135,000 = 7,500 hours × 60 incremental baseballs × $0.30

Golf Ball: $240,000 = 6,000 hrs. × $40 labor cost saved per hour

Stitching Machine

Golf Ball Machine

Annual net cash flows (at the end of each of 8 years) ………………… $ 240,000

b. Present Value Index =

Invested Be to Amount

Flows Cash Net of ValuePresent Total

c. The present value index indicates that the stitching machine would be the

preferred investment, assuming that all other qualitative considerations are

500

E15–14

a. Average rate of return on investment:

2/)000,000,2$+000,000,8($

*000,800$

= 16%

*The annual earnings are equal to the cash flows less the annual depreciation

expense, shown as follows:

$1,600,000 – ($8,000,000 ÷ 10 years) = $800,000

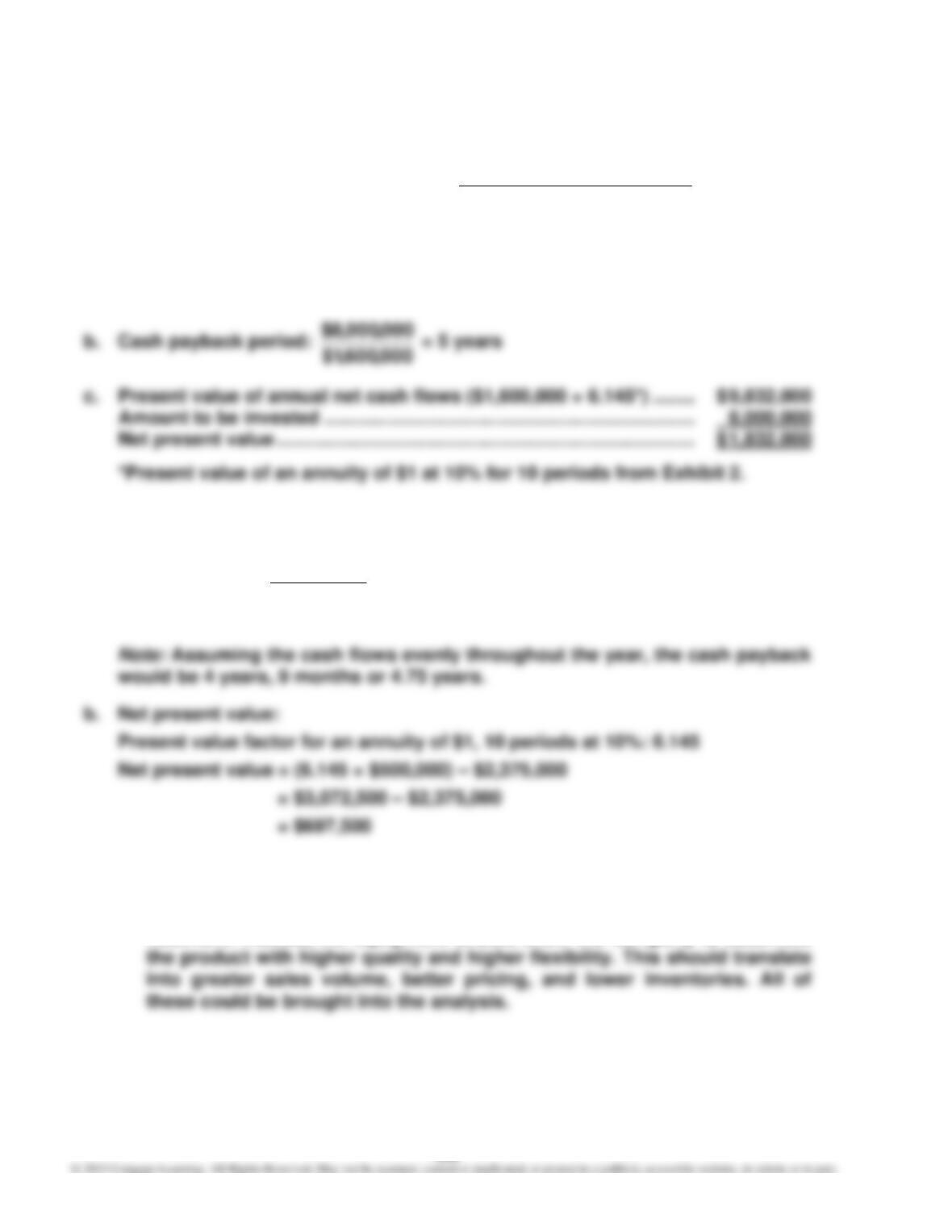

E15–15

a. Payback period:

$500,000

$2,375,000

= 4.75 years

c. Some critical elements that are missing from this analysis are:

• The manager is viewing the acquisition of automated assembly equipment

as a labor-saving device. This is probably a limited way to view the in-

vestment. Instead, the equipment should allow the company to assemble

501

E15–15, Concluded

• The cost of the automated assembly equipment does not stop with the

initial purchase price and installation costs. The equipment will require the

company to hire engineers and support personnel to keep the machines

running, to program the software, and to debug new programs. The opera-

E15–16

a.

Periods 6 for $1 of Annuity

an for Factor luePresent Va

=

Flows Cash Net Annual

Invested Be to Amount

E15–17

Periods 10 for $1 of Annuity

an for Factor luePresent Va

=

Flows Cash Net Annual

Invested Be to Amount

502

E15–18

a. Delivery Truck

Cash received from additional delivery (90,000 bags × $0.35) …….. $31,500

Cash used for operating expenses (24,000 miles × $0.55) ………….. 13,200

Net cash flows for delivery truck ………………………………………………. $ 18,300

Internal Rate of Return = 12% (from text Exhibit 2 for 5 periods)

Bagging Machine

Direct labor savings (2.5 hrs. per day × $20 per hr. × 240 days per yr.) = $12,000

Internal Rate of Return = 20% (from text Exhibit 2 for 5 periods)

b. To: Management

Re: Investment Recommendation

An internal rate of return analysis was performed for the delivery truck and

bagging machine investments. The internal rate of return for the bagging

503

E15–19

a. Present value of annual net cash flows ($620,000 × 5.650*) ………… $ 3,503,000

Amount to be invested ……………………………………………………………… 3,810,000

Net present value …………………………………………………………………….. $ (307,000)

*Present value of an annuity of $1 at 12% for 10 periods from text Exhibit 2.

b. The rate of return is less than 12% because there is a negative net present

value.

E15–20

With an expected useful life of eight years, the cash payback period could not be

greater than eight years. This would indicate that the cost of the initial investment

would not be recovered during the useful life of the asset. However, there would

504

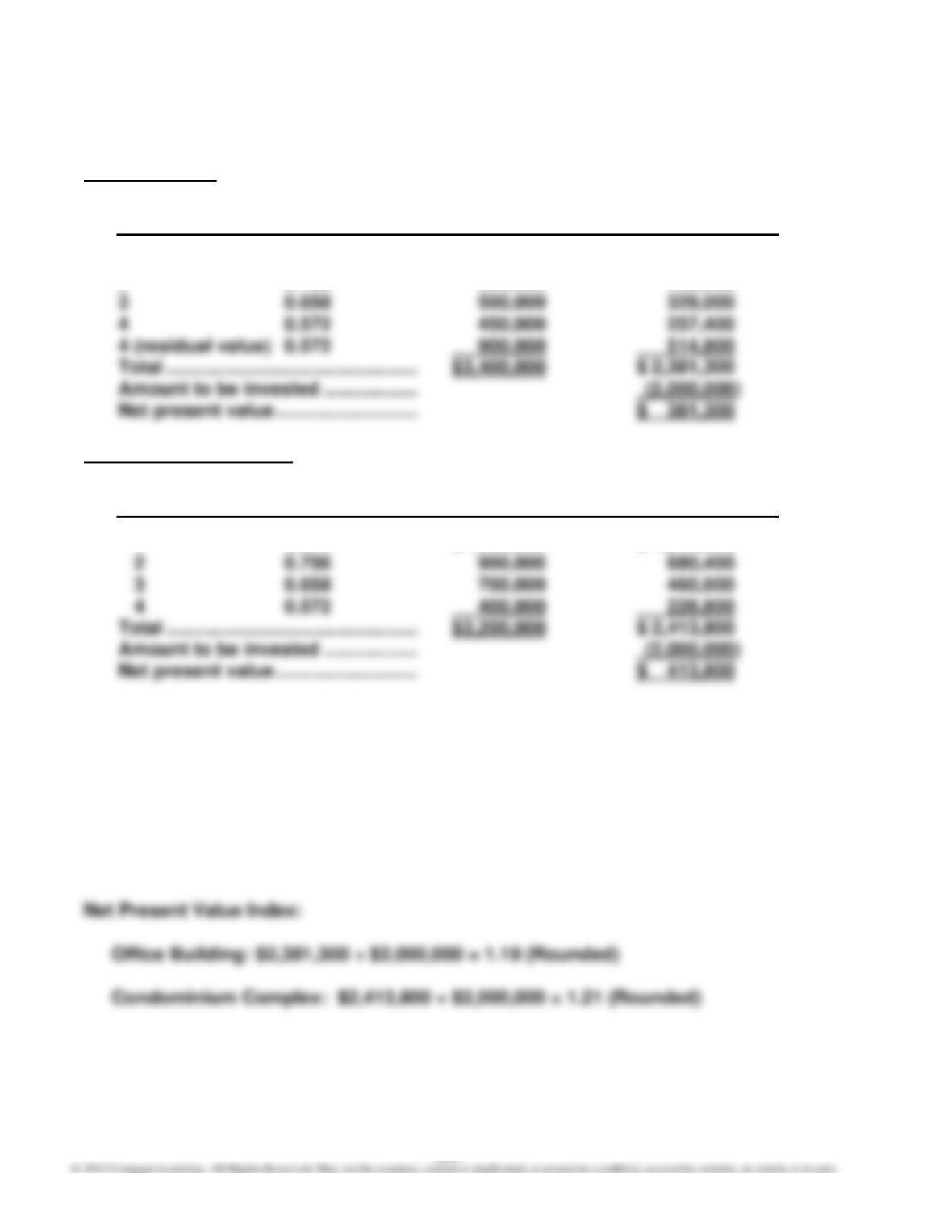

E15–21

Office Building

Present Value Net Cash Present Value of

Year of $1 at 15% Flows Net Cash Flows

1 0.870 $ 950,000 $ 826,500

2 0.756 600,000 453,600

Condominium Complex

Present Value Net Cash Present Value of

Year of $1 at 15% Flows Net Cash Flows

1 0.870 $1,200,000 $ 1,044,000

The net present value of both projects is positive; thus, both proposals are ac-

ceptable. However, the net present value of the condominium complex exceeds

that of the office building. Thus, the condominium complex should be preferred if

there is enough investment money for only one of the projects.

Note to Instructors: Since the investment amount is the same, the net present

value can be compared to determine preference. That is, the present value index

will show the same preference ordering, as shown below.

505

E15–22

a.

Blending Equipment

Equal annual cash flows for Years 1–4 …………………………. $ 18,000

Present value of a $1 annuity at 12% for four periods ……. × 3.037

Computer System

Equal annual cash flows for Years 1–4 …………………………. $ 10,000

Present value of a $1 annuity at 12% for four periods ……. × 3.037

Present value of cash flows …………………………………………. $ 30,370

Amount to be invested ………………………………………………… (17,000)

Net present value ………………………………………………………… $ 13,370

b.

Present value index of blending equipment:

000,45$

846,57$

= 1.29 (Rounded)