COMPREHENSIVE PROBLEM (Continued)

(c) QUIGLEY CORPORATION

Income Statement

For the Year Ended December 31, 2017

Sales Revenue …………………………………………

Cost of Goods Sold ………………………………….

Gross Profit ……………………………………………..

Operating Expenses

Salaries and Wages Expense …………………

Other Operating Expenses …………………….

$ 65,000

39,000

$570,000

400,000

170,000

(d) QUIGLEY CORPORATION

Retained Earnings Statement

For the Year Ended December 31, 2017

Balance, January 1 …………………………………..

Add: Net income ……………………………………

$ 75,050

55,750

COMPREHENSIVE PROBLEM (Continued)

(e) QUIGLEY CORPORATION

Balance Sheet

December 31, 2017

Assets

Current assets

Cash …………………………..…………………………..

Accounts receivable …………………………..

Less: Allowance for doubtful accounts …………

Inventory ………………………………………………..

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable ……………………………………

Dividends payable …………………………..

$51,000

5,100

$ 55,800

45,900

22,700

$ 19,300

6,750

COMPREHENSIVE PROBLEM (Continued)

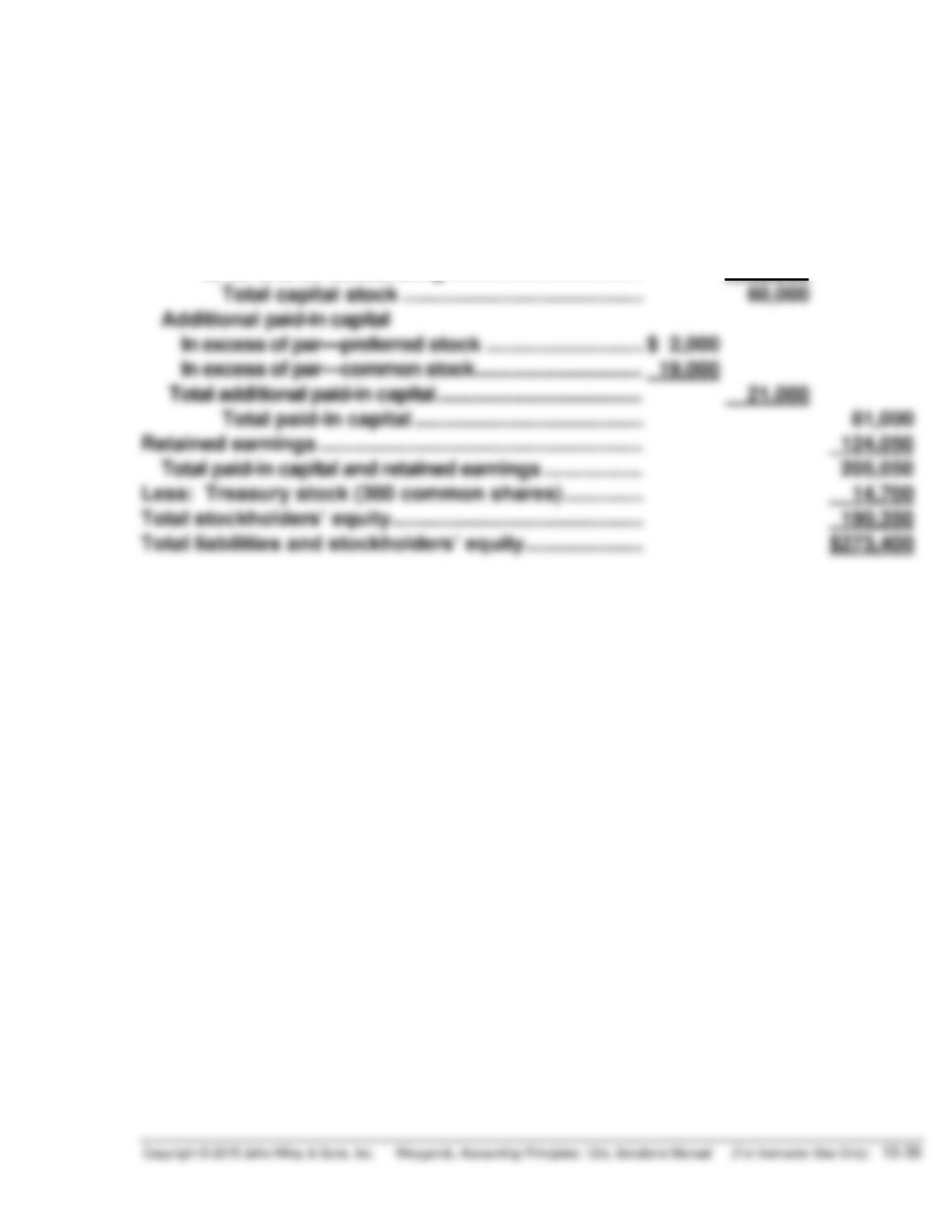

Stockholders’ equity

Paid-in capital

Capital stock

6% Preferred stock, $20 par, 1,000 shares issued ……………….

Common stock $10 par, 4,000 shares issued,

3,700 shares outstanding …………………………………………

$ 20,000

40,000

BYP 15-1 FINANCIAL REPORTING PROBLEM

(a) At September 28, 2013, Apple’s total long-term liabilities was $39,793

million. There was a $20,481 million increase ($39,793 – $19,312) in

long-term liabilities during the year.

BYP 15-2 COMPARATIVE ANALYSIS PROBLEM

(a)

PepsiCo

Coca-Cola

1.

Debt to assets

$53,089

$77,478

= 68.5%

*

$56,615

$90,055

= 62.9%

(b) The higher the percentage of debt to assets, the greater the risk that a

company may be unable to meet its maturing obligations. PepsiCo’s

2013 debt to assets ratio was 9% more than Coca-Cola’s and it would

be considered slightly less able to meet its obligations. The times

BYP 15-3 COMPARATIVE ANALYSIS PROBLEM

(a)

Amazon

Wal-Mart

1.

Debt to assets

$30,413*

$40,159

= 75.7%

$123,412**

$204,751

= 60.3%

2.

Times interest

(b) The higher the percentage of debt to assets, the greater the risk that a

company may be unable to meet its maturing obligations. Amazon’s

2013 debt to assets ratio was 26% more than Wal-Mart’s and it would

BYP 15-4 REAL-WORLD FOCUS

(a) An ‘A’ rating means that the company has a strong capacity to meet

financial commitments, but is somewhat susceptible to adverse

economic conditions and changes in circumstances. A ‘C’ rating

means that a company is currently highly vulnerable due to obligations

and other defined circumstances.

BYP 15-5 DECISION MAKING ACROSS THE ORGANIZATION

(a) Face value of bonds …………………………………………………… $2,400,000

Proceeds from sale of bonds ($2,400,000 X .95) ……………. 2,280,000

Discount on bonds payable ………………………………………… $ 120,000

Bond discount amortization per year:

(b) 1. Bonds Payable …………………………………… 2,400,000

Discount on Bonds Payable …………. 72,000

2. Cash ………………………………………………….. 2,000,000

Bonds Payable …………………………….. 2,000,000

(c) Dear President Glover:

The early redemption of the 8%, 5-year bonds results in recognizing a

BYP 15-5 (Continued)

1. The cash flow of the company as it relates to bonds payable will be

adversely affected as follows:

Additional cash outflows per year ……………………………… $ 28,000

2. The amount of interest expense shown on the income statement

will be higher as a result of the decision to issue new bonds:

Annual interest expense on new bonds …… $220,000

Annual interest expense on 8% bonds:

Interest payment…………………………….. $192,000

BYP 15-6 COMMUNICATION ACTIVITY

To: Sam Masasi

From: I. M. Student

Subject: Bond Financing

(1) The advantages of bond financing over common stock financing include:

1. Stockholder control is not affected.

(2) The types of bonds that may be issued are:

1. Secured or unsecured bonds. Secured bonds have specific assets

of the issuer pledged as collateral. Unsecured bonds are issued

against the general credit of the borrower.

(3) State laws grant corporations the power to issue bonds after formal

approval by the board of directors and stockholders. The terms of the

BYP 15-7 ETHICS CASE

(a) The stakeholders in the Olathe case are:

Ken Iwig, president, founder, and majority stockholder.

Barb Lowery, minority stockholder.

(b) The ethical issues:

The desires of the majority stockholder (Ken Iwig) versus the desires

of the minority stockholders (Barb Lowery and others).

Doing what is right for the company and others versus doing what is best

for oneself.

Questions:

Is what Ken wants to do legal? Is it unethical? Is Ken’s action brash

(c) The rationale provided by the student will be more important than the

specific position because this is a borderline case with no right answer.

BYP 15-8 ALL ABOUT YOU

Results will vary depending on article chose by the student. Some common

signals identified in articles are: bills more than two months in arrears; must

BYP 15-9 FASB CODIFICATION ACTIVITY

(a) Long-term obligations are those scheduled to mature beyond one year

(or the operating cycle, if applicable) from the date of an entity’s balance

sheet.

(b) The Codification provides the following guidance for disclosure of long-

term obligations:

Bonds, mortgages and other long-term debt, including capitalized

lease.

(1) State separately, in the balance sheet or in a note thereto, each

issue or type of obligation and such information as will indicate

(see §210.4–06):

(i) The general character of each type of debt including the rate of

interest;

(2) The amount and terms (including commitment fees and the condi-

tions under which commitments may be withdrawn) of unused

IFRS EXERCISES

IFRS 15-1

The similarities between GAAP and IFRS include: (1) the basic definition of

a liability, and (2) liabilities are normally reported in the order of their

liquidity.

Differences between GAAP and IFRS include: (1) GAAP allows straight line

amortization of bond discounts and premiums, but IFRS requires the

IFRS 15-2

(a) Jan. 1 Cash (€2,000,000 X .97) …………………… 1,940,000

Bonds Payable ………………………… 1,940,000

IFRS 15-3

Cash (£4,000,000 X .99) …………………………..…………….. 3,960,000

Bonds Payable ………………………………………………. 3,800,000

Share Premium—Conversion Equity ……………….. 160,000

IFRS15-4 INTERNATIONAL FINANCIAL REPORTING PROBLEM

(a) Long-term gross borrowings consist of Bonds and Euro Medium Term

Notes, Finance and other long-term leases, and Bank borrowings.

(b) Borrowings are measured at amortized cost, i.e. nominal value net of

premium and issue expenses, which are charged progressively to net

financial income/expense using the effective interest method.