CHAPTER 15 Financial Statement Analysis

Ex. 15–14

c. Hasbro carries a larger proportion of debt to the stockholders’ equity than Mattel

(1.9 and 1.1 times stockholders’ equity). Both companies have strong interest

coverage; however, Mattel’s ratio is much stronger than Hasbro’s. Together, these

$88,835 11.6

Total Liabilities

Total Stockholders’ Equity

$2,818,008 =

1.9

a. Ratio of Liabilities to Stockholders’ Equity =

Hasbro:

$1,507,379

CHAPTER 15 Financial Statement Analysis

Ex. 15–15

c. Hershey uses more debt than does Mondelez. As a result, Hershey’s total liabilities

to stockholders’ equity ratio is higher than Mondelez’s (3.6 vs. 1.3). Mondelelz has

a lower ratio of fixed assets to long-term liabilities than Hershey. This ratio divides

the property, plant, and equipment (net) by the long-term debt. The ratio for

Mondelez is aggressive, with fixed assets covering only 40% of the long-term

Fixed Assets (net)

Long-Term Liabilities

a. =

Ratio of Liabilities to

Stockholders’ Equity

Total Liabilities

Total Stockholders’ Equity

b. Ratio of Fixed Assets to

Long-Term Liabilities =

CHAPTER 15 Financial Statement Analysis

Ex. 15–16

b. The ratio of sales to assets measures the number of sales dollars earned for

each dollar of assets. The greater the number of sales dollars earned for every

dollar of assets, the more efficient a firm is in using assets. Thus, the ratio is a

measure of the efficiency in using assets. The three companies are different in

their efficiency in using assets because they are different in the nature of their

operations. Union Pacific earns only 40 cents for every dollar of assets. This is

because Union Pacific is very asset intensive. That is, Union Pacific must invest in

Note to Instructors: Students may wonder how asset-intensive companies

overcome their asset efficiency disadvantages to competitors with better asset

efficiencies, as in the case between railroads and motor carriers. Asset efficiency

is part of the financial equation; the other part is the profit margin made on each

a. =Sales

Average Total Assets

Ratio of Sales to Total Assets

CHAPTER 15 Financial Statement Analysis

Ex. 15–17

1

$2,250,000 × 8%

2

($4,800,000 + $4,400,000) ÷ 2

3

$2,250,000 × 8%

4

($4,400,000 + $4,000,000) ÷ 2

*

($2,324,000 + $1,972,000) ÷ 2

**

($1,972,000 + $1,500,000) ÷ 2

1

$500,000 × 4%

2

($1,824,000 + $1,472,000) ÷ 2

b. The profitability ratios indicate that Robinson Inc.’s profitability has deteriorated.

Most of this change is from net income falling from $492,000 in 2015 to $372,000

in 2016. Because the rate of return on common stockholders’ equity exceeds the

rate earned on total assets in both years, there is positive leverage from the use

12.0%

a.

=

2016:

Rate Earned on Total Assets

=

Average Total Assets

Net Income + Interest Expense

$372,000 + $180,000

$4,600,000

Rate Earned on Common

Stockholders’ Equity =Average Common Stockholders’ Equity

Net Income – Preferred Dividends

2

1

CHAPTER 15 Financial Statement Analysis

Ex. 15–18

c. Both the rate earned on total assets and the rate earned on stockholders’

equity have increased over the two-year period. The rate earned on total

assets increased from 11.1% to 12.2%, and the rate earned on stockholders’

b.

=Average Total Stockholders’ Equity

Net Income

a. =

Rate Earned on Total Assets Net Income + Interest Expense

Average Total Assets

Rate Earned on Stockholders’ Equity

CHAPTER 15 Financial Statement Analysis

Ex. 15–19

Ratio of Sales to Assets = Average Total Assets

d.

Rate Earned on Total Assets = Net Income + Interest Expense

Average Total Assets

b.

Ratio of Liabilities to

Stockholders’ Equity =Total Liabilities

Total Stockholders’ Equity

e.

=Net Income

Average Total Stockholders’ Equity

c.

f.

Rate Earned on Common

Stockholders’ Equity

Rate Earned on

Stockholders’ Equity

a.

=

Ratio of Fixed Assets to

Long-Term Liabilities Long-Term Liabilities

Fixed Assets (net)

Net Income – Preferred Dividends

Average Common Stockholders’ Equity

=

Sales

(excluding long-term investments)

CHAPTER 15 Financial Statement Analysis

Ex. 15–20

Preferred Dividends

Dividends per Share of Common Stock

Market Price per Share of Common Stock

Market Price per Share of Common Stock

a.

=

Number of Times Bond

Interest Charges Are Earned

e.

Income Before Income Tax + Interest Expense

c.

Earnings per Share

on Common Stock

Interest Expense

f.

Dividend Yield

=

Dividends per Share

of Common Stock =Dividends on Common Stock

Shares of Common Stock Outstanding

Net Income – Preferred Dividends

b.

Number of Times Preferred

Dividends Are Earned =

=

Net Income

Common Stock Outstanding

Price-Earnings Ratio

d.

=Earnings per Share

CHAPTER 15 Financial Statement Analysis

Ex. 15–21

Market Price per Share of Common Stock

a.

=Earnings per Share

b.

=

Price-Earnings Ratio =

Common Dividends

Shares of Common Stock Outstanding

d.

Dividend Yield

Dividends per Share

c.

Earnings per Share of Common Stock

Net Income – Preferred Dividends

Shares of Common Stock Outstanding

=Dividends per Share of Common Stock

Market Price per Share of Common Stock

CHAPTER 15 Financial Statement Analysis

Ex. 15–22

b. Coca-Cola has a large dividend yield and a high price-earnings ratio. Stock market

participants value Coca-Cola common stock on the basis of both its dividend and its

potential share price appreciation. Google pays no dividend and, thus, has no

dividend yield. However, Google has the largest price-earnings ratio of the three

Google: $873.32

=

$36.75

a. =Price-Earnings Ratio Earnings per Share

Market Price per Share of Common Stock

Deere & Co.: $86.20 =

$8.71 9.9

23.8

CHAPTER 15 Financial Statement Analysis

Ex. 15–23

a. Earnings per share on income before extraordinary items:

Net income………………………………………………………………………

…

$4,000,000

Less gain on condemnation…………………………………………………

…

(800,000)

$4,000,000 – $200,000

500,000 shares

= $7.60 per share

=Net Income – Preferred Dividends

Shares of Common Stock Outstanding

b.

Earnings per Share on Common Stock

…

CHAPTER 15 Financial Statement Analysis

Ex. 15–25

a.

Income from continuing operations before income tax $1,000,000

Income tax expense* 400,000

b.

Earnings per common share:

Income from continuing operations $30.00

Ex. 15–26

a. Colston Company reported this item correctly in the financial statements. This

Partial Income Statement

For the Year Ended December 31, 20—

APEX, INC.

Partial Income Statement

For the Year Ended December 31, 20—

APEX, INC.

1

2

CHAPTER 15 Financial Statement Analysis

Prob. 15–1A

1.

2016 2015 Amount Percent

Sales $6,750,000 $6,000,000 $ 750,000 12.5%

Cost of goods sold 2,480,000 2,000,000 480,000 24.0%

Gross profit $4,270,000 $4,000,000 $ 270,000 6.8%

2. Net income has declined from 2015 to 2016. Sales have increased by 12.5%;

however, the cost of goods sold has increased by 24.0%, causing the gross profit to

PROBLEMS

Increase (Decrease)

CLAPTON COMPANY

Comparative Income Statement

For the Years Ended December 31, 2016 and 2015

CHAPTER 15 Financial Statement Analysis

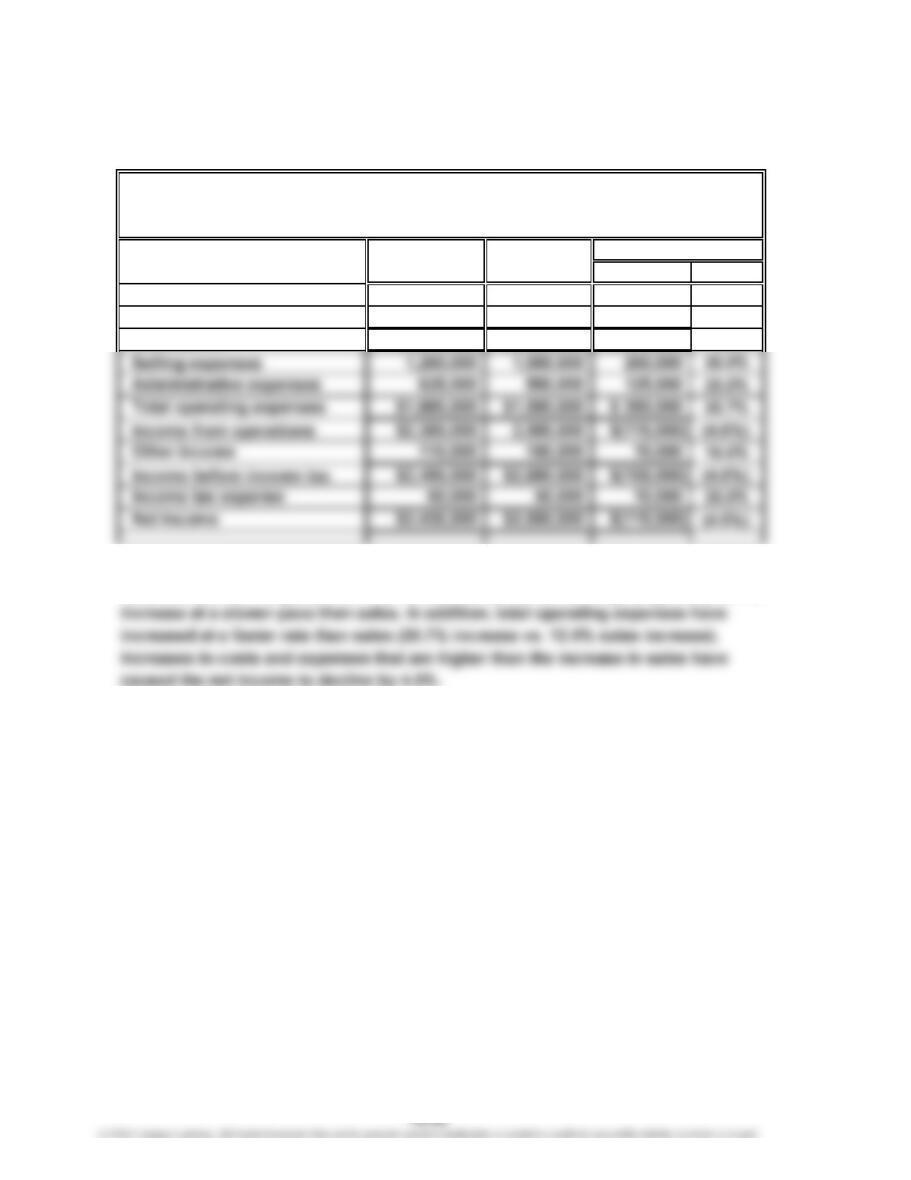

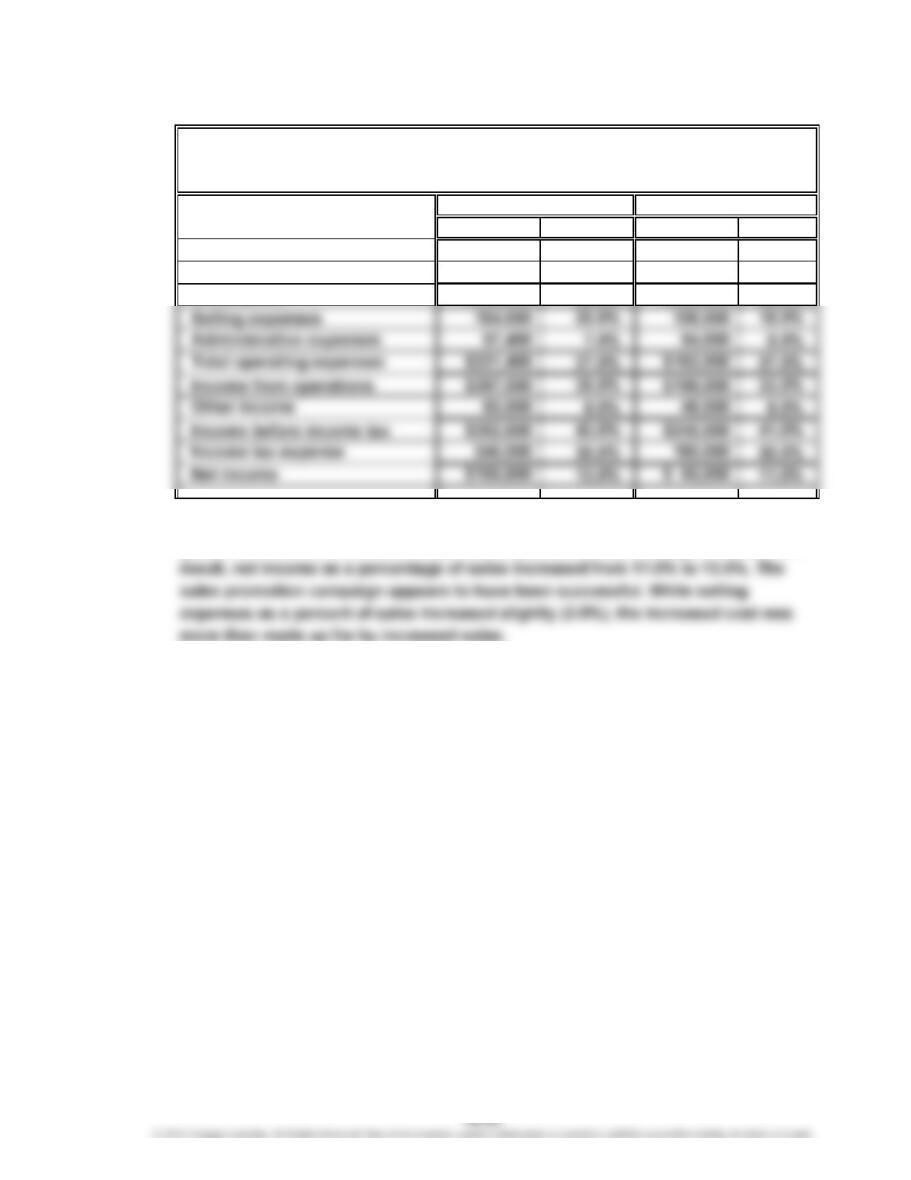

Prob. 15–2A

1.

Amount Percent Amount Percent

Sales $820,000 100.0% $600,000 100.0%

Cost of goods sold 311,600 38.0% 240,000 40.0%

Gross profit $508,400 62.0% $360,000 60.0%

2. The vertical analysis indicates that the costs other than selling expenses (cost of

goods sold and administrative expenses) improved as a percentage of sales. As a

2016 2015

INDIGO COMPANY

Comparative Income Statement

For the Years Ended December 31, 2016 and 2015

CHAPTER 15 Financial Statement Analysis

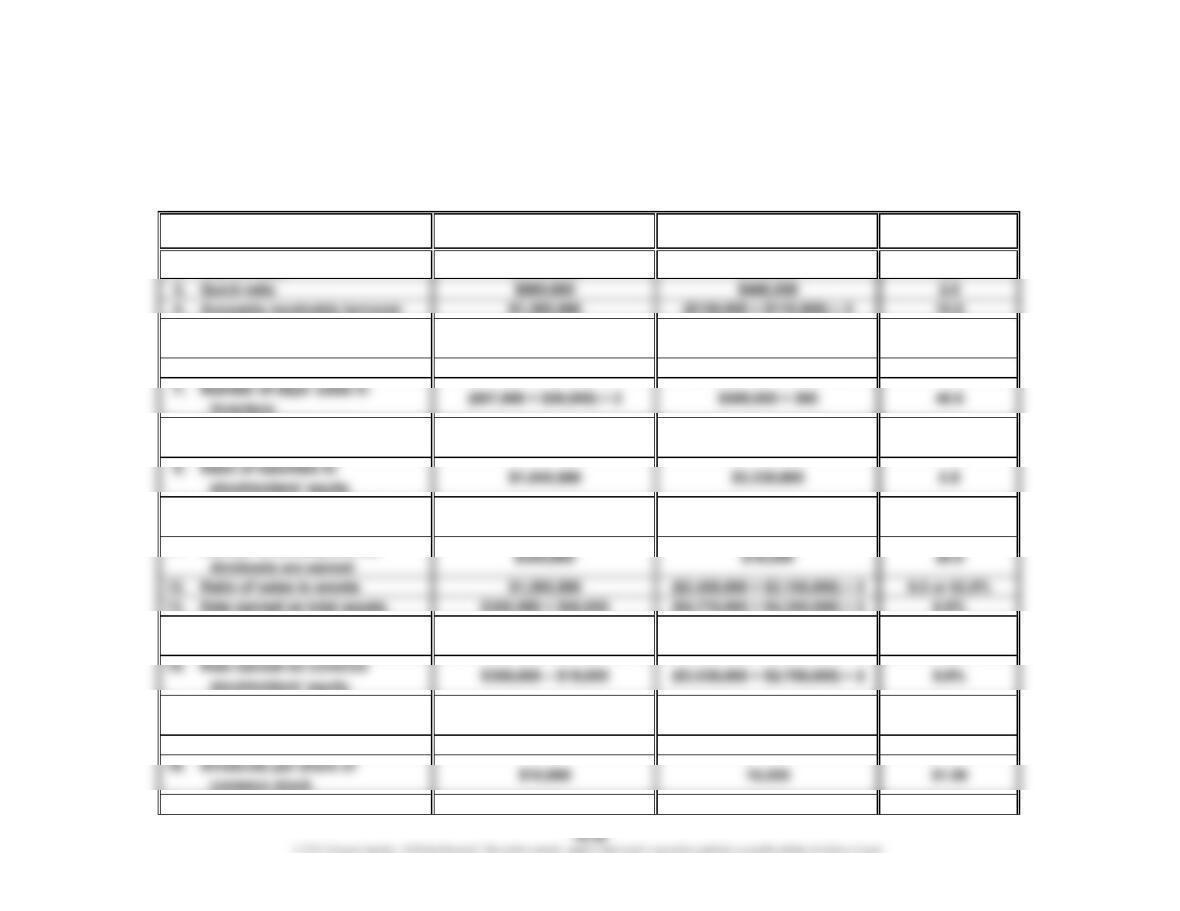

Prob. 15–3A

1. a. Working Capital = Current Assets – Current Liabilities

$1,650,000 – $750,000 = $900,000

$750,000

2.

Working Quick Current

Capital Assets Liabilities

$ 900,000 $ 900,000 $750,000

900,000 900,000 860,000

750,000 900,000 900,000

1,125,000 1,125,000 750,000

1,500,000 1,500,000 750,000

= 2.2

AssetsTransaction

Current

Ratio

c. =

Quick

Ratio

Quick Ratio Quick Assets

Current Liabilities

Current

a. 2.2 1.2 $1,650,000

c. 2.0 1.0 1,760,000

e. 1.8 1.0 1,650,000

2,250,000

g. 2.5 1.5 1,875,000

Supporting Data

i. 3.0 2.0

CHAPTER 15 Financial Statement Analysis

Prob. 15–4A

1. Working Capital: $1,100,000 – $440,000 = $660,000

Calculated

Numerator Denominator Value

2. Current ratio $1,100,000 $440,000 2.5

5. Number of days’ sales in

receivables

6. Inventory turnover $500,000 ($67,000 + $58,000) ÷ 2 8.0

8. Ratio of fixed assets to

long-term liabilities

10. Number of times interest

charges are earned

11. Number of times preferred

14. Rate earned on

stockholders’ equity

16. Earnings per share on

common stock

17. Price-earnings ratio 71.25 28.50 2.5

19. Dividend yield $1.00 $71.25 1.4%

Ratio

$1,320,000 $1,100,000

36.5

1.2

($130,000 + $110,000) ÷ 2 $1,200,000 ÷ 365

6.8

$300,000

$380,000 + $66,000 $66,000

$28.50$300,000 – $15,000 10,000

9.7%

($3,230,000 + $2,955,000) ÷ 2

CHAPTER 15 Financial Statement Analysis

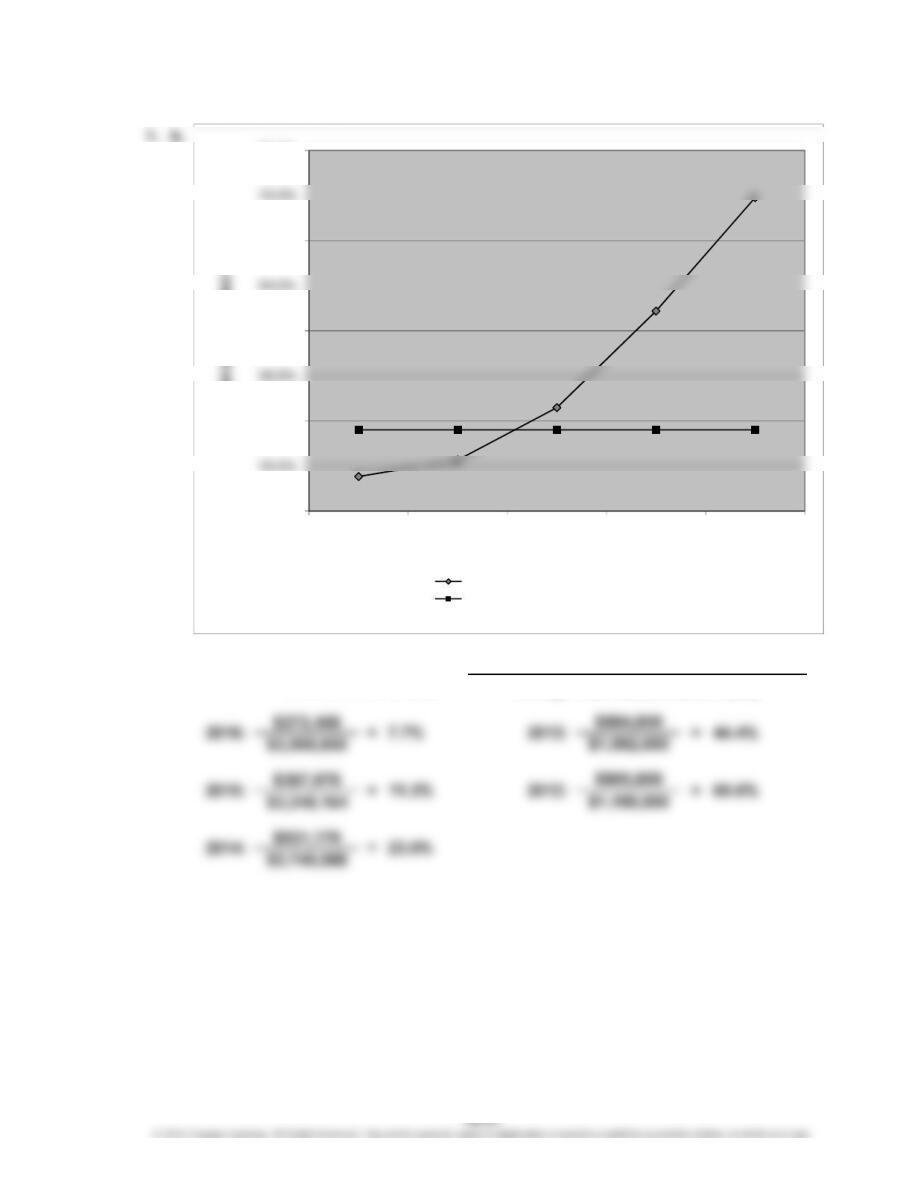

Prob. 15–5A

$4,270,764

2013: $1,379,000

45.3%

20.8%2016: =

=

$3,044,250

0.0%

10.0%

30.0%

50.0%

2016 2015 2014 2013 2012

Year

CHAPTER 15 Financial Statement Analysis

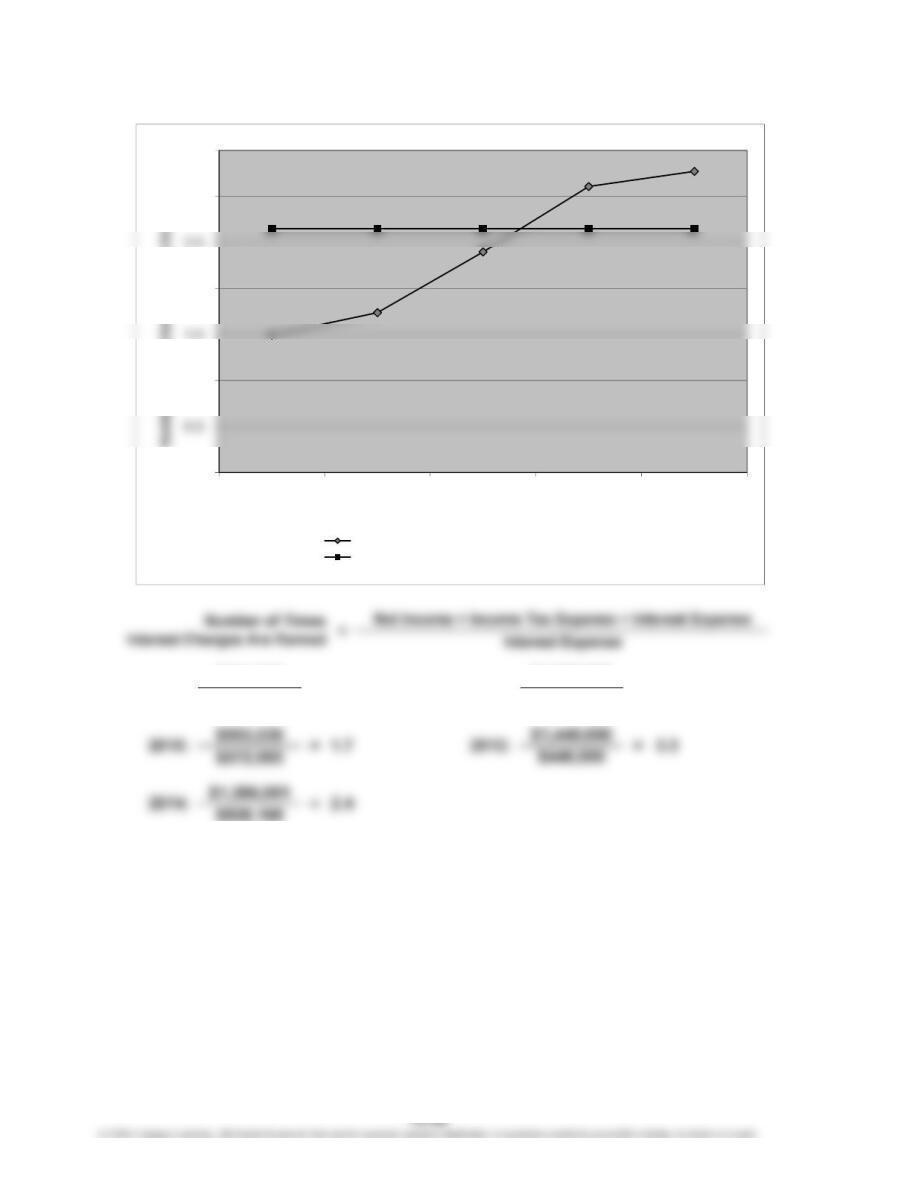

Prob. 15–5A (Continued)

Rate Earned on

Stockholders’ Equity

=Average Total Stockholders’ Equity

Net Income

0.0%

20.0%

40.0%

60.0%

80.0%

2016 2015 2014 2013 2012

Rate Earned on Stockholders’ Equity

Year

Company’s rate earned on stockholders’ equity

Industry rate earned on stockholders’ equity

CHAPTER 15 Financial Statement Analysis

Prob. 15–5A (Continued)

1. c.

$921,202

$616,047

1.5

=2013:2016:

=

3.1

$1,539,000

$495,000

0.0

1.0

2.0

3.0

3.5

2016 2015 2014 2013 2012

Year

Company’s number of times interest charges are earned

Industry number of times interest charges are earned

CHAPTER 15 Financial Statement Analysis

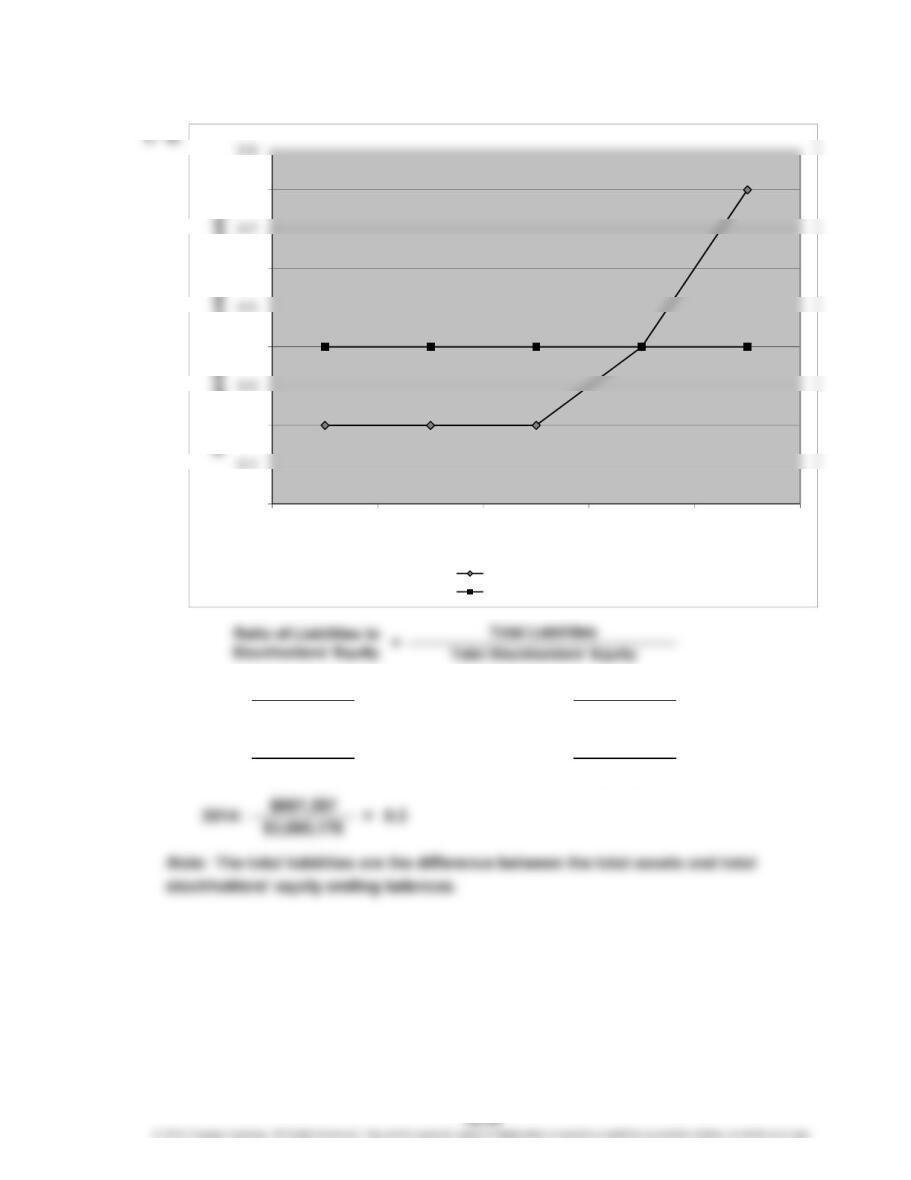

Prob. 15–5A (Continued)

$710,621

$3,706,557

$691,198

$3,433,152

0.22016:

=

2015: = 0.2 0.8

0.4

$904,500

$2,434,000

$1,200,000 =

=

$1,550,000

2012:

2013:

0.0

0.2

0.4

0.6

0.8

2016 2015 2014 2013 2012

Year

Company’s liabilities to equity

Industry liabilities to equity

CHAPTER 15 Financial Statement Analysis

Prob. 15–5A (Concluded)

2. Both the rate earned on total assets and the rate earned on stockholders’ equity

have been moving in a negative direction in the last five years. Both measures have

moved below the industry average over the last two years. The cause of this decline

is driven by a rapid decline in earnings. The use of debt can be seen from the ratio