Accounting Information Systems

CHAPTER 15

THE HUMAN RESOURCES MANAGEMENT/PAYROLL CYCLE

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

15.1 This chapter noted many of the benefits that can arise by integrating the HRM and

payroll databases. Nevertheless, many companies maintain separate payroll and

HRM information systems. Why do you think this is so? (Hint: Think about the

differences in employee background and the functions performed by the HRM and

payroll departments.)

Payroll and HRM systems are separate in many companies because integration was

generally not feasible using early data processing technology. Also, different events

generate data and two different professions were interested in using the data. As a result,

Reasons for integrating the personnel and HRM systems include the following:

• Integration will improve decision-making by providing access to more of the relevant

data needed for monitoring employee development.

• It is logical, since both systems are organized around the same entity: the employee.

Ch. 15: The Human Resources Management/Payroll Cycle

15-2

15.2 Some accountants have advocated that a company’s human assets be measured and

included directly in the financial statements. For example, the costs of hiring and

training an employee would be recorded as an asset that is amortized over the

employee’s expected term of service. Do you agree or disagree? Why?

This question should generate some debate. The issue is the trade-off between

“subjectivity” in measuring the value of a company’s investment in the knowledge and

skills of its employees versus the usefulness of at least attempting to explicitly measure

those assets.

15.3 You are responsible for implementing a new employee performance measurement

system that will provide factory supervisors with detailed information about each of

their employees on a weekly basis. In conversation with some of these supervisors,

you are surprised to learn they do not believe these reports will be useful. They

explain that they can already obtain all the information they need to manage their

employees simply by observing the shop floor. Comment on that opinion.

Formal reports on employee performance are not intended to replace direct observation,

How could formal reports supplement and enhance what the supervisors learn by

direct observation?

Well-designed reports provide quantitative summary measures of aspects of employee

performance that are believed to be important to the achievement of the organization’s

Accounting Information Systems

15.4 One of the threats associated with having employees telecommute is that they may

use company-provided resources (e.g., laptop, printer, etc.) for a side business. What

are some other threats?

Other threats are:

1. Not working or working less productively than if the employees were working onsite.

2. Security risks, such as the employee not proactively maintaining proper antivirus and

patch management practices or not protecting and/or backing up their data

adequately.

What controls can mitigate the risk of these threats?

The solutions to these potential threats primarily involve monitoring and the use of

security controls discussed in chapter 8. For example, software exists to enable

companies to monitor employees, including what they do on the Internet.

15.5 How would you respond to the treasurer of a small charity who tells you that the

organization does not use a separate checking account for payroll because the

benefits are not worth the extra monthly service fee?

A separate payroll account limits the organization’s exposure to only the amount of cash

deposited into the payroll account.

Ch. 15: The Human Resources Management/Payroll Cycle

15-4

15.6 This chapter discussed how the HR department should have responsibility for

updating the HRM/payroll database for hiring, firing, and promotions. What other

kinds of changes may need to be made?

Other types of changes include name changes (usually due to change in marital status),

What controls should be implemented to ensure the accuracy and validity of such

changes?

Allow employees to make these changes through a web-based application available on

the organization’s intranet. The application should include processing integrity checks to

prevent invalid entries.

Accounting Information Systems

15-5

SUGGESTED ANSWERS TO THE PROBLEMS

15.1 Match the terms in the left column with the appropriate definition from the right column.

1. _e__ Payroll service bureau

a. A list of each employee’s gross pay, payroll deductions,

and net pay in a multicolumn format.

2. _h__ Payroll clearing account

b. Used to record the activities performed by a salaried

professional for various clients.

3. _g__ Earnings statement

c. Used to record time worked by an hourly-wage

4. _a__ Payroll register

d. An organization that processes payroll and provides

other HRM services.

current pay period and for the year-to-date.

h. Special general ledger account used for payroll

processing.

Ch. 15: The Human Resources Management/Payroll Cycle

15-6

15.2 What internal control procedure(s) would be most effective in preventing the

following errors or fraudulent acts?

a. An inadvertent data entry error caused an employee’s wage rate to be overstated

in the payroll master file.

• Have the personnel department maintain a hash total of employee wage rates

b. A fictitious employee payroll record was added to the payroll master file.

• Use strong multifactor authentication techniques to restrict access to the payroll

master data to authorized personnel in the HR department..

c. During data entry, the hours worked on an employee’s time card for one day

were accidentally entered as 80 hours, instead of 8 hours.

• Use a limit check during data entry to check the hours-worked field for each

Accounting Information Systems

15-7

d. A computer operator used an online terminal to increase her own salary.

• Use passwords and an access control matrix to restrict access to authorized

personnel.

e. A factory supervisor failed to notify the HRM department that an employee had

been fired. Consequently, paychecks continued to be issued for that employee.

The supervisor pocketed and cashed those paychecks.

• Implement a policy prohibiting supervisors from picking up or distributing

paychecks. Instead, have the payroll department distribute all paychecks.

f. A factory employee punched a friend’s time card in at 1:00 P.M. and out at 5:00

P.M. while the friend played golf that afternoon.

• Use biometric controls to record time in and time out

g. A programmer obtained the payroll master file and increased his salary.

• Implement physical access controls such as a file library function to prevent

programmers from having unsupervised access to production databases

Ch. 15: The Human Resources Management/Payroll Cycle

15-8

h. Some time cards were lost during payroll preparation; consequently, when

paychecks were distributed, several employees complained about not being paid.

• Prepare a record count of job time records before they are submitted for

processing and compare record count subsequent to data entry against the number

of paychecks prepared.

i. A large portion of the payroll master file was destroyed when the disk pack

containing the file was used as a scratch file for another application.

• Use internal and external file labels to identify the contents and expiration date of

all active files

Accounting Information Systems

j. The organization was fined $5000 for making a late quarterly payroll tax

payment to the IRS.

• Use IRS Publication Circular E, which provides instructions for making required

Ch. 15: The Human Resources Management/Payroll Cycle

15.3 You have been hired to evaluate the payroll system for the Skip-Rope

Manufacturing Company. The company processes its payroll in-house. Use Table

15-1 as a reference to prepare a list of questions to evaluate Skip-Rope’s internal

control structure as it pertains to payroll processing for its factory employees. Each

question should be phrased so that it can be answered with either a yes or a no; all

no answers should indicate potential internal control weaknesses. Include a third

column listing the potential problem that could arise if that particular control were

not in place. (CPA Exam, adapted)

Question

Y/N

Threat if control missing

1. Are payroll changes (hires, separations, salary

changes, overtime, bonuses, promotions, etc.)

properly authorized and approved?

1. Unauthorized pay raises and

fictitious employees.

2. Are discretionary payroll deductions and

withholdings authorized in writing by employees?

2. Errors; employee lawsuits;

penalties if tax code

violated.

3. Are the employees who perform each of the

following payroll functions independent of the other

five functions?

• personnel and approval of payroll changes

3. Fraud; theft of paychecks.

4. Are changes in standard data on which payroll is

based (hires, separations, salary changes,

promotions, deduction and withholding changes,

etc.) promptly input to the system to process payroll?

4. Errors in future payroll;

possible fines and penalties.

verified?

supervisors or internal audit personnel?

corrected.

Accounting Information Systems

15-11

8. Is access to payroll master data restricted to

authorized employees?

8. Unauthorized changes in pay

rates or creation of fictitious

employees.

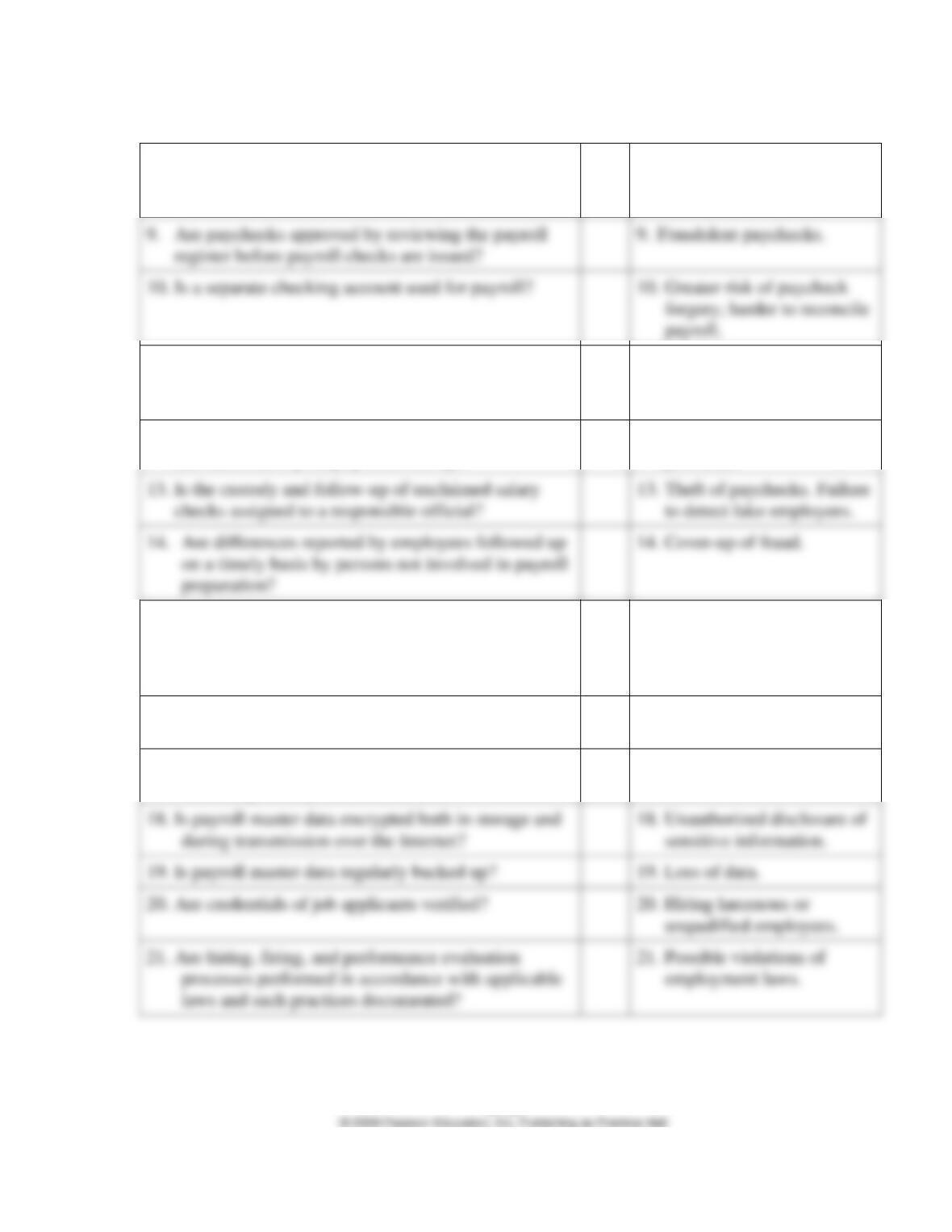

9. Are paychecks approved by reviewing the payroll

register before payroll checks are issued?

9. Fraudulent paychecks.

10. Is a separate checking account used for payroll?

10. Greater risk of paycheck

11. Is the payroll bank account reconciled to the general

ledger by someone not involved in payroll or

paycheck distribution?

11. Failure to detect errors

12. Are payroll bank reconciliations properly approved

and differences promptly followed up?

12. Failure to detect and correct

problems.

13. Is the custody and follow-up of unclaimed salary

checks assigned to a responsible official?

13. Theft of paychecks. Failure

to detect fake employees.

14. Are differences reported by employees followed up

14. Cover-up of fraud.

15. Are there procedures (e.g., tickler files) to assure

proper and timely payment of withholdings to

appropriate bodies and to file required information

returns?

15. Fines and/or penalties.

16. Are employee compensation records reconciled to

control accounts?

16. Inaccurate records; failure

to detect and correct errors.

17. Is access to personnel and payroll records, checks,

forms, signature plates, etc. limited?

17. Fraudulent payroll.

18. Is payroll master data encrypted both in storage and

during transmission over the Internet?

18. Unauthorized disclosure of

sensitive information.

unqualified employees.

21. Are hiring, firing, and performance evaluation

laws and such practices documented?

21. Possible violations of

employment laws.

Ch. 15: The Human Resources Management/Payroll Cycle

15-12

15.4 Although most medium and large companies have implemented sophisticated

payroll and HRM systems like the one described in this chapter, many smaller

companies still maintain separate payroll and HRM systems that employ many

manual procedures. Typical of such small companies is the Kowal Manufacturing

Company, which employs about 50 production workers and has the following

payroll procedures:

• The factory supervisor interviews and hires all job applicants. The new

employee prepares a W-4 form (Employee’s Withholding Exemption Certificate)

and gives it to the supervisor. The supervisor writes the hourly rate of pay for

the new employee in the corner of the W-4 form and then gives the form to the

payroll clerk as notice that a new worker has been hired. The supervisor

a. Identify weaknesses in current procedures, and explain the threats that they may

allow to occur.

Weakness

Threat

1. Factory supervisor hires all job

applicants and forwards their W-4

form to the payroll clerk.

The factory supervisor could hire fictitious

employees and submit their W-4 form.

Accounting Information Systems

15-13

rates

new hires

4. Blank time cards are readily

available.

even at work.

removing his timecard over the weekend

checks.

The supervisor can conveniently keep the pay

checks of fictitious or fired employees.

An employee could have another employee fill

out a time card when they were late or not

b. Suggest ways to improve the Kowal Manufacturing Company’s internal controls

over hiring and payroll processing. (CPA Examination, adapted)

1. A system of advice forms should be installed so that new hires, terminations, rate

2. Before applicants are hired, their backgrounds should be investigated by

3. The supply of blank time cards should be removed. At the beginning of each

4. The foreman should collect the time cards at the end of the week, approve them,

5. The payroll checks should be distributed to the workers by a responsible person

other than the foreman. Unclaimed checks should be sent to internal audit until

claimed by the worker.

In addition, the following changes should be made because the problem does not state

that these procedures are being followed:

• If the Company has a cost system that requires the workers to prepare production

Ch. 15: The Human Resources Management/Payroll Cycle

15-14

Accounting Information Systems

15-15

15.5 Arlington Industries manufactures and sells engine parts for large industrial

equipment. The company employs over 1,000 workers for three shifts, and most

employees work overtime when necessary. Figure 15-10 depicts the procedures

followed to process payroll. Additional information about payroll procedures

follows:

• The HRM department determines the wage rates of all employees. The process

begins when a form authorizing the addition of a new employee to the payroll

master file is sent to the payroll coordinator for review and approval. Once the

information about the new employee is entered in the system, the computer

automatically calculates the overtime and shift differential rates for that

employee.

• The payroll department manager performs all the other activities depicted in

Figure 15-10

• The payroll master file is backed up weekly, after payroll processing is finished.

(CMA Examination, adapted)

Ch. 15: The Human Resources Management/Payroll Cycle

a. Identify and describe at least three weaknesses in Arlington Industries’ payroll

process.

• The payroll processing system at Arlington Industries violates the principle of

segregation of duties. The same individual verifies time cards, inputs payroll

information into the master file, prints the checks, machine-signs the checks,

distributes the checks, and prepares the payroll journal entry.

b. Identify and describe at least two different areas in Arlington’s payroll

processing system where controls are satisfactory.

• The personnel department determines the wage rate and initiates the setup of

payroll records, which is a good example of segregation of duties.

15-17

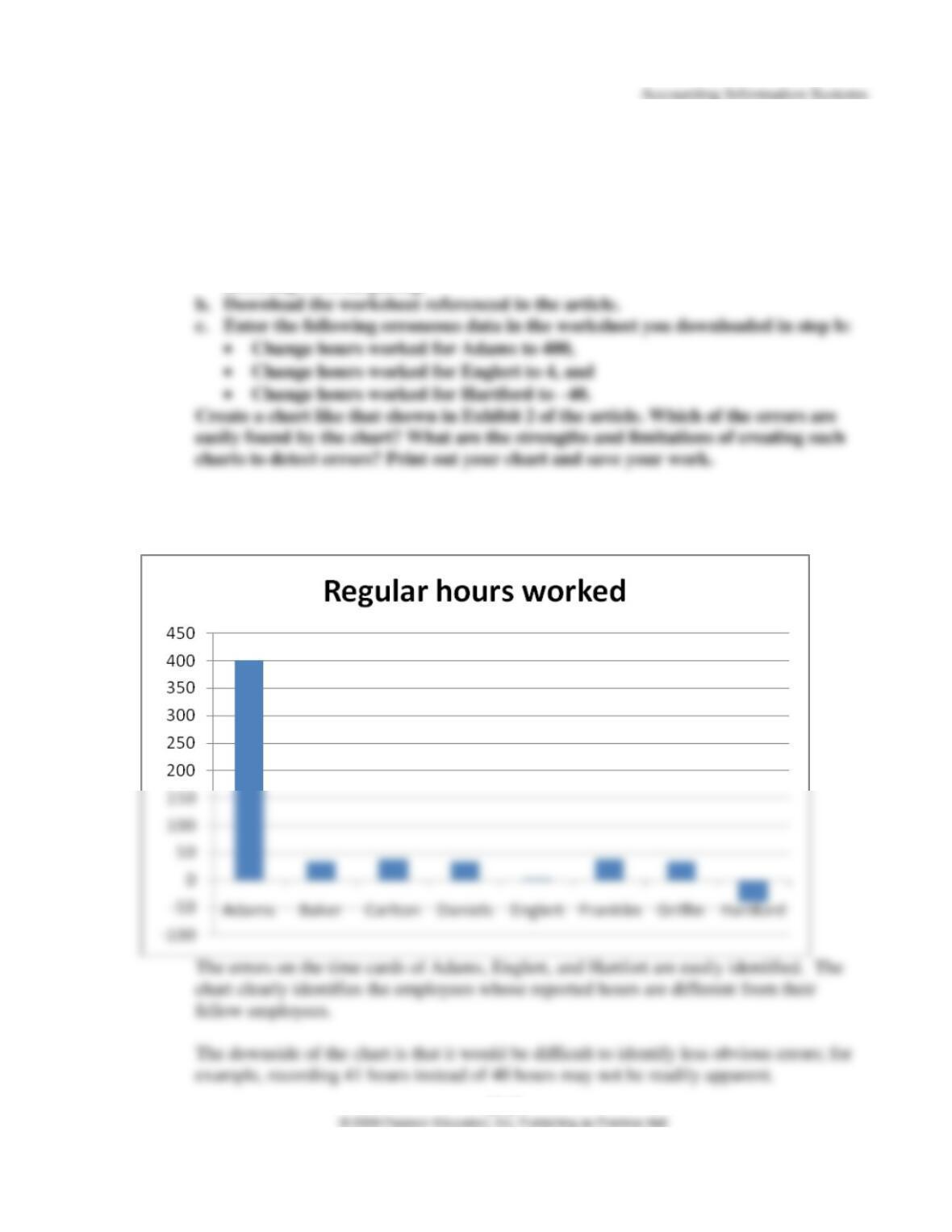

15.6 Excel Problem

Objective: Learn how to find and correct errors in complex spreadsheets used for

payroll.

a. Read the article “Ferret Out Spreadsheet Errors” by Mark G. Simkin, in the

Journal of Accountancy (February 2004). You can find a copy online by

accessing www.aicpa.org.

Note: Disable data validation on the hours worked column in order to input erroneous

data.

Ch. 15: The Human Resources Management/Payroll Cycle

15-18

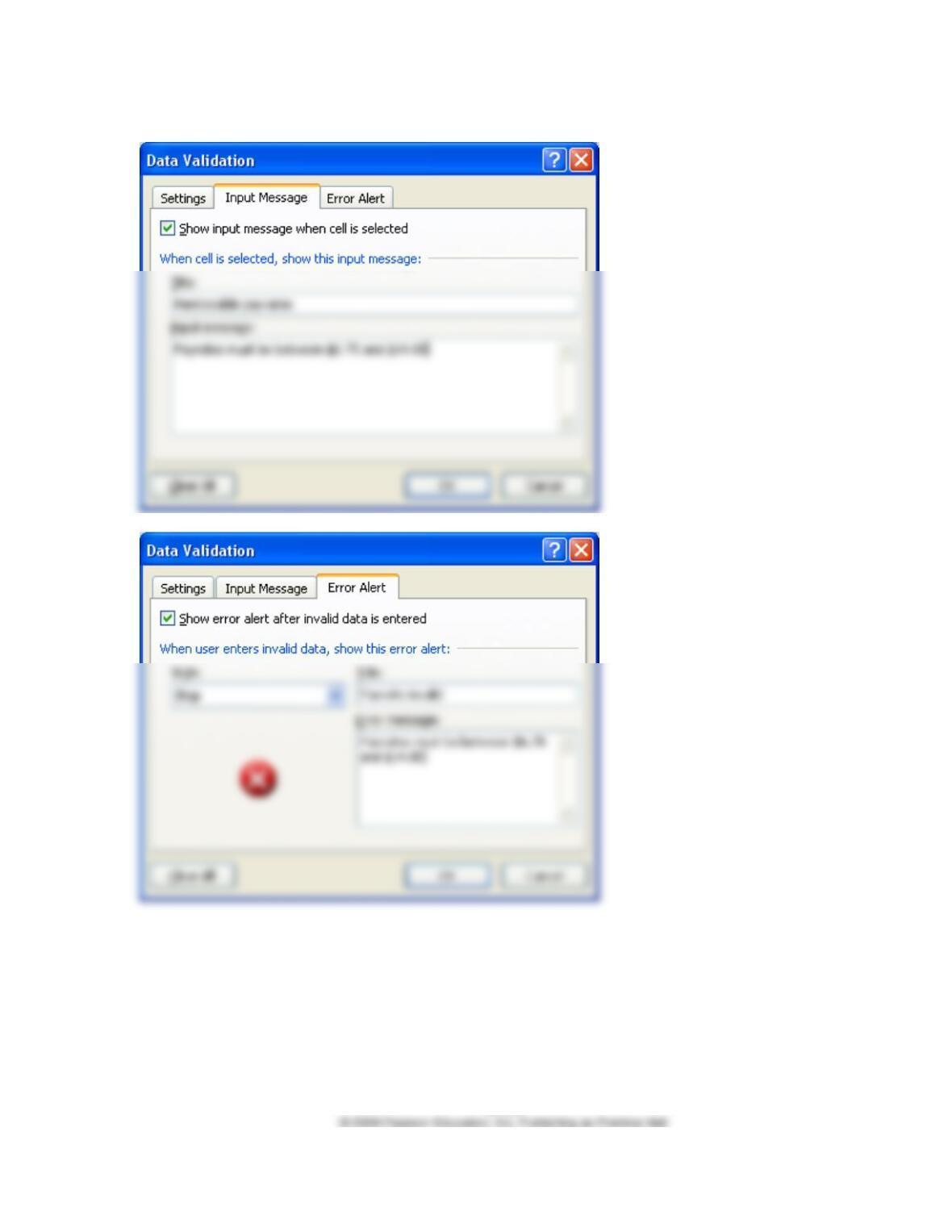

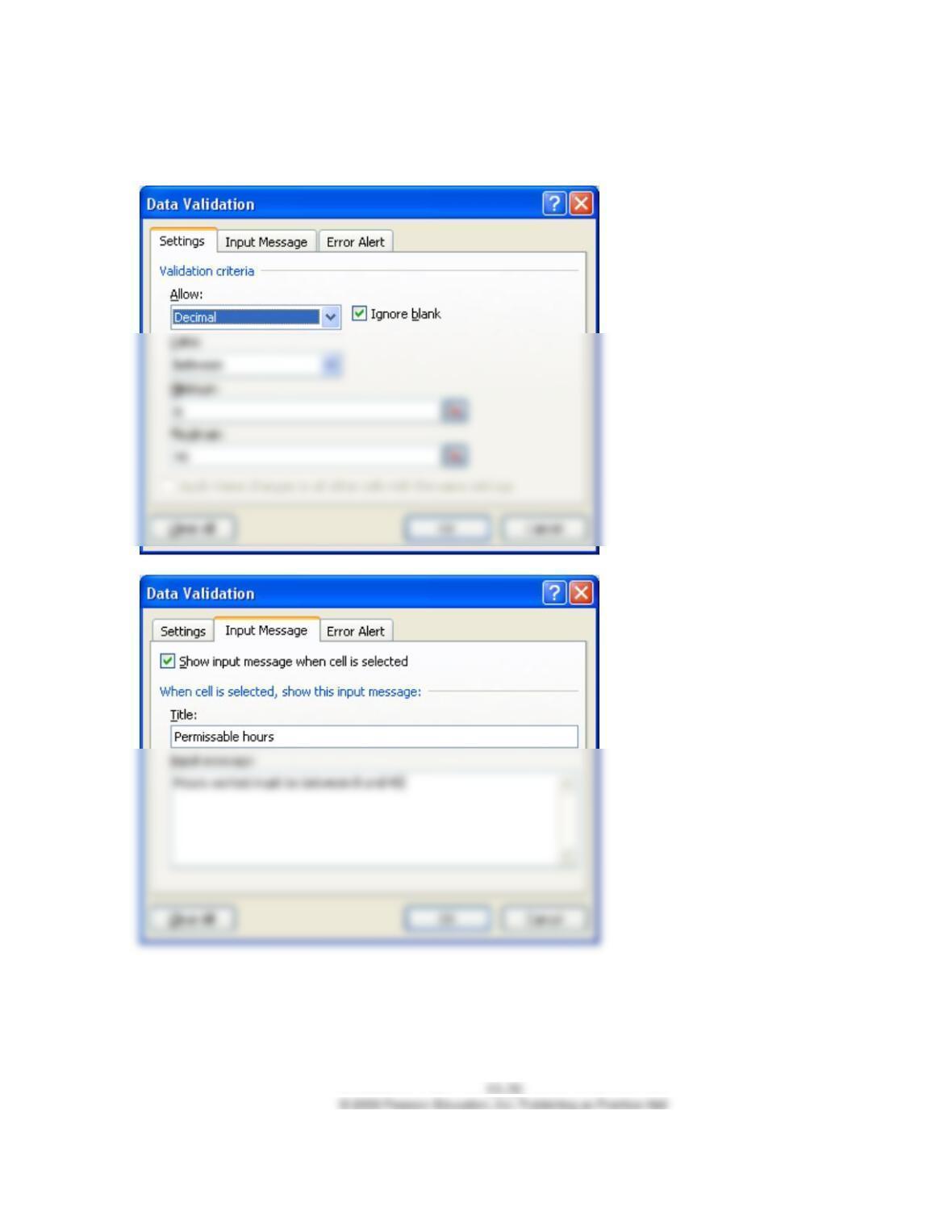

d. Create the three data validation rules described in the article (Exhibits 4–7

illustrate how to create the first rule). Print out screen shots of how you create

each rule, and save your work. (Note: The article “Block That Spreadsheet

Error” by Theo Callahan, in the Journal of Accountancy (August 2002) provides

additional examples of data validation rules.)

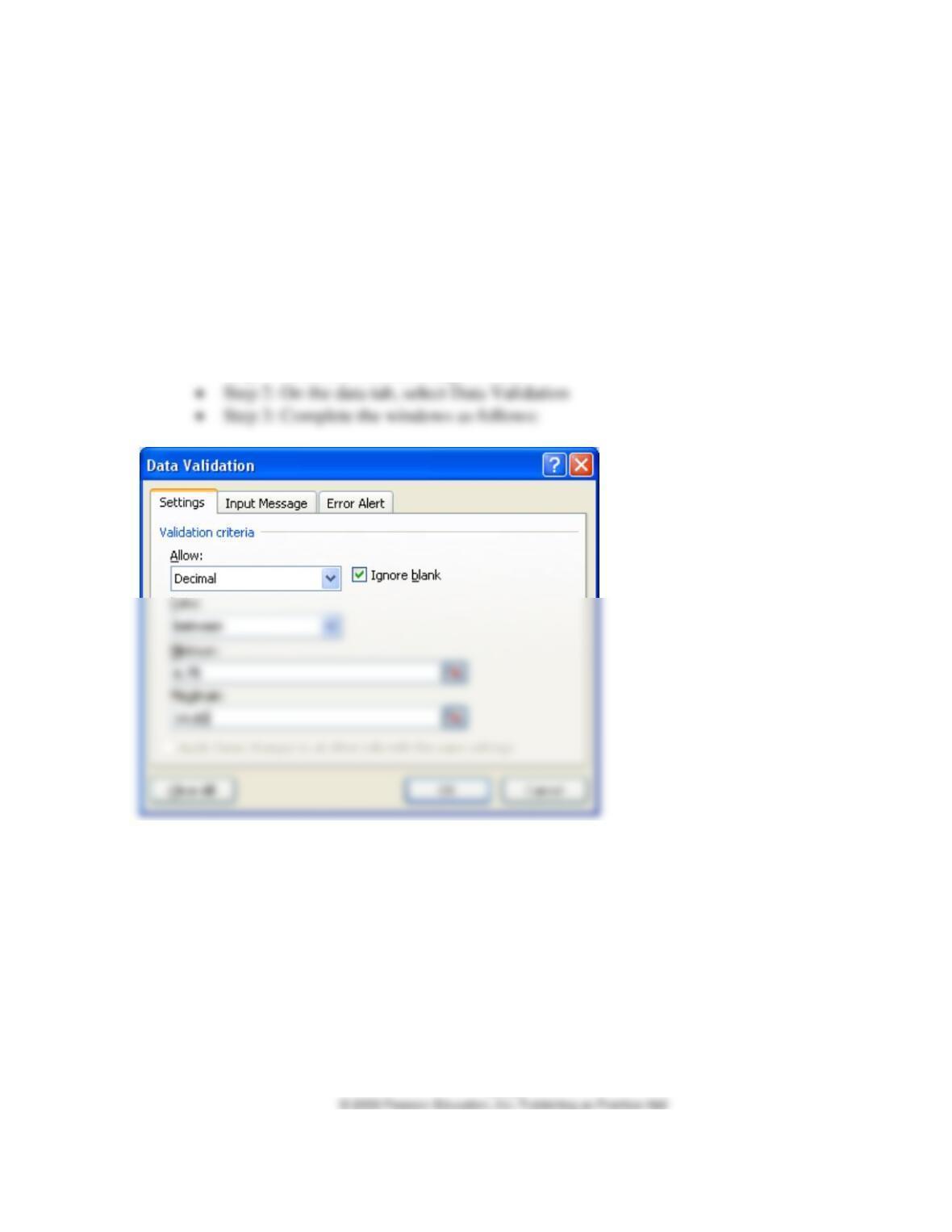

Rule 1: Payrates must be between $6.75 and $14.00.

• Step 1: Select the relevant range of cells

Accounting Information Systems

15-19

Ch. 15: The Human Resources Management/Payroll Cycle

Rule 2: Hours worked must be between 0 and 40