Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

chapter

15(14)

Financial Statement

Analysis

______________________________________________

OPENING COMMENTS

This chapter presents techniques for analyzing financial statements and the contents of annual reports.

The techniques for analyzing financial statements include horizontal analysis, vertical analysis, and ratio

analysis. Since an analytical technique has been presented at the end of most chapters, some of the

material presented in Chapter 15(14) will be a review. The appendix presents unusual items on the

income statement.

When covering this chapter, you should guard against getting bogged down in the calculations

surrounding ratio analysis. Try to spend at least as much class time interpreting ratios as calculating them.

Emphasize that computing ratios is only the starting point for assessing the performance of a business. To

be meaningful, current-year ratios must be compared with ratios from prior years and ratios of other

companies in the same industry. The influence of the general economic and business environment should

be considered. Finally, sound financial judgment should be applied.

After studying the chapter, your students should be able to:

2. Use financial statement analysis to assess the solvency of a business.

4. Describe the contents of corporate annual reports.

KEY TERMS

accounts receivable analysis

accounts receivable turnover

290 Chapter 15(14) Financial Statement Analysis

common-sized statement

current position analysis

current ratio

dividend yield

dividends per share

earnings per share on common stock

extraordinary item

horizontal analysis

inventory analysis

inventory turnover

leverage

liquidity

Management’s Discussion and Analysis (MD&A)

number of days’ sales in inventory

number of days’ sales in receivables

number of times interest charges are earned

price-earnings (P/E) ratio

profitability

quick assets

quick ratio

STUDENT FAQS

• Do we have to memorize all these formulas?

• Which formulas are the most important?

• What are the top five formulas?

• Should we use these formulas to tell how a company is doing before we invest in it?

• These are hard since I did not learn some of this information earlier. What do you suggest I do?

• What do these formulas really tell us about the company?

• How do I know if a ratio of fixed assets to long-term liabilities of 3.8 is good or bad?

• Is vertical or horizontal analysis better?

• How are some of these ratios related? If a company’s accounts receivable turnover is poor, then won’t

the numbers of days’ sales in receivables be poor too?

• How much emphasis should I put on unusual items in a company’s income statement when evaluating

its financial condition?

Chapter 15(14) Financial Statement Analysis 291

OBJECTIVE 1

Describe basic financial statement analytical methods.

SYNOPSIS

Three methods to analyze a company’s financial statements are horizontal analysis, vertical analysis, and

common-size statements. To complete a horizontal analysis, a minimum of two financial statements is

used. Each item on the most recent statement is compared with the same item on an earlier statement in

terms of the amount of increase or decrease and the percent of increase or decrease. Exhibits 1, 2, 3, and 4

show the horizontal comparison of various financial statements. The percentage analysis of the

Key Terms and Definitions

• Common-Sized Statement - A financial statement in which all items are expressed only in

relative terms.

• Horizontal Analysis - Financial analysis that compares an item in a current statement with the

same item in prior statements.

• Vertical Analysis - An analysis that compares each item in a current statement with a total

amount within the same statement.

Relevant Example Exercises and Exhibits

• Example Exercise 15(14)-1 Horizontal Analysis

• Example Exercise 15(14)-2 Vertical Analysis

• Exhibit 1 – Comparative Balance Sheet—Horizontal Analysis

• Exhibit 2 – Comparative Schedule of Current Assets—Horizontal Analysis

SUGGESTED APPROACH

The basic financial statement analytical procedures are horizontal analysis, vertical analysis, and ratio

analysis. Ratio analysis is covered under Objectives 2 and 3.

292 Chapter 15(14) Financial Statement Analysis

DEMONSTRATION PROBLEM—Horizontal Analysis

Ask your students to turn to the annual report for Nike in Appendix C at the end of the text. Specifically,

direct them to the Consolidated Statements of Income. Ask your students to compute the dollar increase

in sales (Gross Margin) between fiscal year 2010 and fiscal year 2011. (Answer: $708 million, or

$708,000,000)

Most likely, a few students will have 7.4 percent as an answer. These students have compared the $708

million increase in sales to sales in fiscal year 2011. Remind them that a percentage change in a financial

statement item is computed by comparing the change in dollars to the base year amount. The base year is

the starting point—fiscal year 2010 in this case.

GROUP LEARNING ACTIVITY—Horizontal Analysis

Divide your class into small groups. Ask them to perform the horizontal analysis requested on

Transparency Master (TM) 15(14)-1 using the financial statements. The correct answers are displayed on

TM 15(14)-2.

GROUP LEARNING ACTIVITY—Vertical Analysis

Under vertical analysis, all financial statement items are shown as a percentage of a significant total on

the statement. On an income statement, all items are shown as a percentage of sales. On a balance sheet,

all items are shown as a percentage of total assets.

Chapter 15(14) Financial Statement Analysis 293

OBJECTIVE 2

Use financial statement analysis to assess the solvency of a business.

SYNOPSIS

Users of financial statements are interested in the ability of a company to maintain liquidity, solvency,

and profitability. The ability of a company to convert assets into cash is called liquidity, and the ability to

pay its debts is called solvency. Current position analysis concerns a company’s ability to pay its current

liabilities; it includes working capital, current ratio, and quick ratio. Working capital is computed as

working capital = current assets – current liabilities and is used to evaluate a company’s ability to pay

Accounts receivable analysis assesses a company’s ability to collect the money due from customers. It

includes accounts receivable turnover and number of days’ sales in receivables. Accounts receivable

turnover is calculated as accounts receivable turnover = sales/average accounts receivable. Number of

days’ sales in receivables is computed as number of days’ sales in receivables = average accounts

receivable/average daily sales and is an estimate of the time (in days) that the accounts receivable have

been outstanding.

Inventory analysis analyzes the company’s ability to manage its inventory and includes inventory

turnover and number of days’ sales in inventory. Excess inventory ties up cash and increases insurance

The ratio of fixed assets to long-term liabilities provides a measure of whether note holders or

bondholders will be paid. Calculated as ratio of fixed assets to long-term liabilities = fixed assets (net)/

long-term liabilities. A related ratio, the ratio of liabilities to stockholders’ equity, measures how much of

the company is financed by debt and equity. It is computed as ratio of liabilities to stockholders’ equity =

total liabilities/total stockholders’ equity. The fixed charge coverage ratio is also known as the number of

times interest charges are earned and measures the risk that interest payments will not be made if earnings

decrease. It is computed as number of times interest charges are earned = (income before income tax +

interest expense)/interest expense. The higher the ratio, the more likely payments will be made.

Key Terms and Definitions

• Accounts Receivable Analysis - A company’s ability to collect its accounts receivable.

• Accounts Receivable Turnover - The relationship between sales and accounts receivable,

computed by dividing the sales by the average net accounts receivable; measures how frequently

294 Chapter 15(14) Financial Statement Analysis

• Inventory Turnover - The relationship between the volume of goods sold and inventory,

computed by dividing the cost of goods sold by the average inventory.

• Liquidity - The ability to convert assets into cash.

• Number of Days’ Sales in Inventory - The relationship between the volume of sales and

• Quick Ratio - A financial ratio that measures the ability to pay current liabilities with quick

assets (cash, marketable securities, accounts receivable).

• Ratio of Fixed Assets to Long-Term Liabilities - A leverage ratio that measures the margin of

safety of long-term creditors, calculated as the net fixed assets divided by the long-term liabilities.

• Ratio of Liabilities to Owner’s (Stockholders’) Equity - A comprehensive leverage ratio that

measures the relationship of the claims of creditors to stockholders’ equity.

• Solvency - The ability of a firm to pay its debts as they come due.

• Working Capital - The excess of the current assets of a business over its current liabilities.

Relevant Example Exercises and Exhibits

• Example Exercise 15(14)-3 Current Position Analysis

SUGGESTED APPROACH

Solvency, which is a company’s ability to pay debts as they become due, is assessed through ratio

analysis. TM 15(14)-4 lists the ratios that measure a firm’s solvency.

Use the following group learning activities to give your students the opportunity to practice ratio analysis

as it relates to solvency.

GROUP LEARNING ACTIVITY—Computing Solvency Measures

The ratios that assess solvency are listed in the text in the first section of Exhibit 10. Calculating these

ratios using real-life financial statements is a challenge for most students, due to the differences in

terminology used by companies. For example, a company may use the term “plant assets” or “property,

Chapter 15(14) Financial Statement Analysis 295

GROUP LEARNING ACTIVITY—Analyzing Solvency Measures

TM 15(14)-5 shows solvency ratios for Ace Company over a two-year period. The TM also presents

industry averages for the solvency ratios. Ask your students to analyze the data related to Ace Company

1. For each solvency ratio, state whether or not Ace has improved from the prior year.

3. Comment on any significant items noticed when reviewing the solvency ratios and Ace’s overall

solvency.

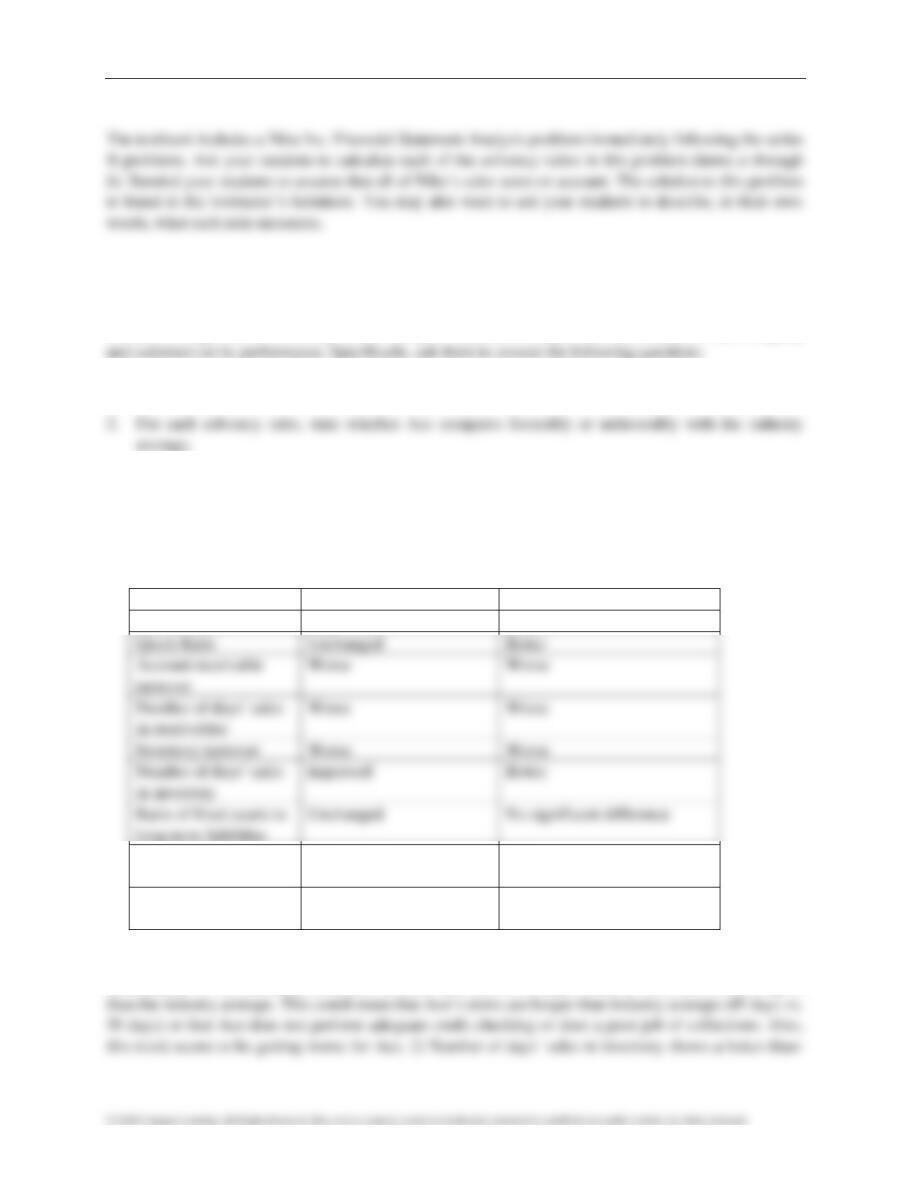

Possible response: The table below provides a summary of the questions listed above:

Ratio

Ace Prior Year

Ace vs. Industry

Current Ratio

Improved

Better

Ratio of liabilities to

stockholders’ equity

Improved

Better

Number of times

interest charges earned

Improved

Worse

Comments: 1) The accounts receivable turnover and number of days’ sales in receivables show higher

OBJECTIVE 3

Use financial statement analysis to assess the profitability of a business.

SYNOPSIS

Profitability analysis focuses on a company’s ability to earn profits. Eight different ratios are used to

analyze profit and both the income statement and the balance sheet are utilized. The ratio of sales to assets

per share on common stock, and it is a ratio that measures a company’s future earnings prospects.

Dividends per share measures the extent to which earnings are being distributed to common shareholders.

It is computed as dividends per share = dividends on common stock/shares of common stock outstanding.

The dividend yield on common stock measures the rate of return to common stockholders from cash

dividends. It is computed as dividend yield = dividends per share of common stock/market price per share

• Price-Earnings (P/E) Ratio - The ratio of the market price per share of common stock, at a

specific date, to the annual earnings per share.

Chapter 15(14) Financial Statement Analysis 297

• Rate Earned on Common Stockholders’ Equity - A measure of profitability computed by

dividing net income, reduced by preferred dividend requirements, by common stockholders’

equity.

Relevant Example Exercises and Exhibits

• Example Exercise 15(14)-8 Sales to Assets

• Example Exercise 15(14)-9 Rate Earned on Total Assets

• Example Exercise 15(14)-10 Common Stockholders’ Profitability Analysis

• Example Exercise 15(14)-11 Earnings per Share and Price-Earnings Ratio

• Exhibit 8 – Effect of Leverage

• Exhibit 9 – Dividends and Earnings per Share of Common Stock

• Exhibit 10 – Summary of Analytical Measures

SUGGESTED APPROACH

Profitability, which is a company’s ability to earn income, is also assessed through ratio analysis. TM

15(14)-6 lists the ratios that measure a firm’s profitability.

Use the Group Learning Activities below to give your students the opportunity to practice ratio analysis

as it relates to profitability.

GROUP LEARNING ACTIVITY—Computing Profitability Measures

The ratios that assess profitability are listed in the text in the second part of Exhibit 10. Ask your students

to calculate each of the profitability ratios (items i through m) for the Nike Inc. Financial Statement

GROUP LEARNING ACTIVITY—Analyzing Profitability Measures

TM 15(14)-7 shows profitability ratios for Ace Company over a two-year period. The TM also presents

industry averages for the profitability ratios.

1. For each profitability ratio, state whether or not Ace has improved from the prior year.

298 Chapter 15(14) Financial Statement Analysis

3. Comment on any significant items noticed when reviewing the profitability ratios and Ace’s overall

profitability.

Possible response: The table below provides a summary of the questions listed above:

Ratio

Ace Prior Year

Ace vs. Industry

Ratio of sales to assets

Improved

Better

Rate earned on total assets

No change

No significant difference

Rate earned on stockholders’

equity

Improved

Better

OBJECTIVE 4

Describe the contents of corporate annual reports.

SYNOPSIS

The annual report of a corporation contains financial statements, accompanying notes, and several other

requirements. The Securities and Exchange Commission (SEC) requires that annual reports include the

management’s analysis of current operations and their plans for the future. The Sarbanes-Oxley Act of

Key Terms and Definitions

• Management’s Discussion and Analysis (MD&A) - An annual report disclosure that provides

management’s analysis of the results of operations and financial condition.

Chapter 15(14) Financial Statement Analysis 299

SUGGESTED APPROACH

The text presents information on the Management Discussion and Analysis section of the annual report

plus the Independent Auditor’s Report. You may want to briefly mention other components of the annual

report. TM 15(14)-8 lists several sections typically included in a corporate annual report. Briefly review

these sections and their content with your students, using the notes below.

1. Financial Highlights—presents selected financial data that summarize operations for the past year or

two.

3. Financial Statements

4. Notes to the Financial Statements—presents supplemental information needed to interpret the

6. Management Report—affirms management’s responsibility for internal controls and the accuracy of

financial statements; usually signed by the company’s CFO.

8. Historical Summary—presents key financial data for the past five to ten years.

Ask your students to look through the financial statements of Nike and locate as many of these sections as

possible.

Use the following Group Learning Activity to cover the independent auditors’ report and the management

report in more detail.

GROUP LEARNING ACTIVITY—Independent Auditors’ Report

Obtain copies of several different annual reports. Divide the class into small groups; give each group an

annual report. Ask each group to locate the independent auditors’ report. Next, instruct the groups to

outline the auditors’ report by briefly describing the main point(s) in each paragraph. Ask two or more

300 Chapter 15(14) Financial Statement Analysis

INTERNET ACTIVITY—Annual Reports

It is possible to find the annual reports of many companies by searching the Internet. Ask your students to

WRITING EXERCISE—Historical Summary

Ask your students to write an answer to the following question [TM 15(14)-10]:

Many annual reports include a Historical Summary section, which shows key financial data for the past

five to ten years. Why would information that is five to ten years old be presented in an annual report?

APPENDIX—UNUSUAL ITEMS ON THE

INCOME STATEMENT

SYNOPSIS

GAAP requires that unusual items be reported separately on the income statement. Without separate

reporting on the income statement, users of financial statements might be misled. Unusual items either

affect the current period or affect a prior period. Extraordinary item include those that are unusual in

nature and infrequent in occurrence. Earnings per share are usually included with the income statement

but are only required in the report for continuing operations and net income.

Key Terms and Definitions

• Extraordinary Item - An event or a transaction that is both (1) unusual in nature and (2)

infrequent in occurrence.

Relevant Example Exercises and Exhibits

Chapter 15(14) Financial Statement Analysis 301

SUGGESTED APPROACH

The text presents unusual items in two sections, those affecting the current period income statement

(discontinued operations and extraordinary items) and those affecting a prior period income statement

LECTURE AID—Unusual Income Statement Items

1. Fixed Asset Impairments: A fixed asset impairment occurs when the carrying amount (book value) of

2. Restructuring Charges: These are costs associated with involuntarily terminating employees,

terminating contracts, consolidating facilities, or relocating employees. For example, assume a

restaurant chain decides to close several of its unprofitable locations. Closing the restaurants may

create the following costs: severance packages for managers, fees associated with breaking a lease, or

fees paid to an employment agency to help workers find other jobs. The company may be willing to

incur these costs because the short-term restructuring costs are less than the long-term costs of

running unprofitable restaurants.

3. Discontinued Operations: This section contains information concerning any component of a business

(such as a division, department, or product line) that is sold or closed during the year. The amount

displayed in this section is calculated as follows:

4. Extraordinary Items: These are revenues or expenses that result from events that are “unusual and

infrequent.” Examples include natural disasters (flood, earthquake, fire) and condemnation of land or

5. Changes in Accounting Principles: This section shows the effect of changing from one accepted

accounting principle to another. For example, a corporation might choose to change its depreciation

method from the straight-line to the declining-balance method. That corporation would need to re-

compute depreciation for all of its assets under the new method (declining-balance) for any prior

WRITING EXERCISE—Below-the-Line Items Reported on the Income

Statement

Ask your students to write a response to the following questions found on TM 15(14)-11:

1. Why are the results of discontinued operations and extraordinary items shown in separate sections at

the bottom of the income statement?

2. Why are discontinued operations and extraordinary items shown net of tax?

Type Item Description LO(s) Difficulty Time Est BUSPROG AICPA ACBSP - APC Bloom's EE Excel GL SMH FAI Service Real World Writing Ethics Internet Group

DQ 1 1 Easy 5 min. Analytic Measurement Financial Statement Analysis Knowledge

DQ 2 1 Easy 5 min. Analytic Measurement Financial Statement Analysis Knowledge

DQ 3 1 Easy 5 min. Analytic Measurement Financial Statement Analysis Knowledge

DQ 4 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Knowledge

DQ 5 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Knowledge

PE 3A Current position analysis 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Application x

PE 3B Current position analysis 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Application x

PE 4A Accounts receivable analysis 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Application x

PE 4B Accounts receivable analysis 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Application x

PE 5A Inventory analysis 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Application x

PE 5B Inventory analysis 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Application x

PE 6A Long-term solvency analysis 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Application x

PE 6B Long-term solvency analysis 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Application x

PE 7A Times interest charges are earned 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Application x

PE 7B Times interest charges are earned 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Application x

EX 5 Horizontal analysis of the income statement 1 Easy 20 min. Analytic Measurement Financial Statement Analysis Application x x x

EX 6 Current position analysis 2 Easy 10 min. Analytic Measurement Financial Statement Analysis Application x x

EX 7 Current position analysis 2 Easy 10 min. Analytic Measurement Financial Statement Analysis Application x x

EX 8 Current position analysis 2 Moderate 15 min. Analytic Measurement Financial Statement Analysis Application x

EX 9 Accounts receivable analysis 2 Easy 10 min. Analytic Measurement Financial Statement Analysis Application x x

EX 10 Accounts receivable analysis 2 Easy 10 min. Analytic Measurement Financial Statement Analysis Application x

EX 11 Inventory analysis 2 Easy 10 min. Analytic Measurement Financial Statement Analysis Application x x

EX 12 Inventory analysis 2 Easy 10 min. Analytic Measurement Financial Statement Analysis Application x x

EX 13 Ratio of liabilities to stockholders' equity and number of times interest charges are earned 2 Easy 10 min. Analytic Measurement Financial Statement Analysis Application x

PR 3A Effect of transactions on current position analysis 2 Moderate 1 hour Analytic Measurement Financial Statement Analysis Application x

PR 4A Nineteen measures of solvency and profitability 2,3 Moderate 2 hours Analytic Measurement Financial Statement Analysis Application x

PR 5A Solvency and profitability trend analysis 2,3 Moderate 1.5 hours Analytic Measurement Financial Statement Analysis Application x

PR 1B Horizontal analysis of income statement 1 Moderate 1 hour Analytic Measurement Financial Statement Analysis Application x x x x

PR 2B Vertical analysis of income statement 1 Moderate 1 hour Analytic Measurement Financial Statement Analysis Application x x x

PR 3B Effect of transactions on current position analysis 2 Moderate 1 hour Analytic Measurement Financial Statement Analysis Application x

PR 4B Nineteen measures of solvency and profitability 2,3 Moderate 2 hours Analytic Measurement Financial Statement Analysis Application x

PR 5B Solvency and profitability trend analysis 2,3 Moderate 1.5 hours Analytic Measurement Financial Statement Analysis Application x

Nike Inc. Problem 1,2,3 Moderate 1.5 hours Analytic Measurement Financial Statement Analysis Application x

CP 1 Analysis of financial corporate growth 2 Easy 5 min. Analytic Measurement Financial Statement Analysis Analysis x

CP 2 Receivables and inventory turnover 2 Moderate 10 min. Analytic Measurement Financial Statement Analysis Analysis x

CP 3 Vertical analysis 1 Easy 15 min. Analytic Measurement Financial Statement Analysis Analysis x x

CP 4 Profitability and stockholder ratios 3 Moderate 20 min. Analytic Measurement Financial Statement Analysis Application x

CP 5 Comprehensive profitability and solvency analysis 2,3 Easy 15 min. Analytic Measurement Financial Statement Analysis Analysis x x

HOMEWORK CHART WITH LEARNING OUTCOMES TAGGING

TAGGING

RESOURCES

FOCUS