15

Transfer Pricing

Solutions to Review Questions

15–1.

15–2.

Yes, transfer prices exist in centralized organizations to record the transfer of goods and

15–3.

Market-based transfer pricing is considered optimal under many circumstances because it

15–4.

The key limitation is that market prices are often not readily available. The limitations of

15–5.

Direct intervention might be preferable when transfers between units are rare or where the

decision resulting from decentralized decision-making is considered too harmful to allow.

15–6.

Reasons not to use market prices include situations where: (1) market prices are not

15–7.

When actual costs are used as a basis for the transfer, any variances or inefficiencies in

15–8.

The advantage of negotiated transfer prices is that they can be used when market prices

15–9.

The general transfer pricing rule is:

15–10.

Transfer pricing is important in tax accounting, because transfers of goods or services

15–11.

Solutions to Critical Analysis and Discussion Questions

15–12.

15–13.

A cost-based or negotiated cost-based transfer pricing method would be necessary. We

15–14.

15–15.

15–16.

The transfer price becomes revenue for the selling segment and a cost to the buying

15–17.

Because transfer prices can affect the assignment of income from one jurisdiction to

15–18.

Transfer prices are similar to cost allocations in that they assign costs (and profit) to two or

15–19.

Corporate cost allocation is similar to transfer pricing where the “service” being transferred

Solutions to Exercises

15–20. (20 min.) Apply Transfer Pricing Rules: Best Practices, Inc.

15–21. (15 min.) Evaluate Transfer Pricing System: Clinton Corporation

a. If Alpha Division buys from outsiders because the transfer price is greater than $90,

15–22. (15 min.) Evaluate Transfer Pricing System

With the possibility of increased production, Maryland Division has an opportunity cost of

15–23. (20 min.) Evaluate Transfer Pricing System.

a.

Northeast

Southwest

Company

Transfer internally

Pays

$32

Receives

$30

Pays

$ 2

Pays

$11

Pays

11

Pays

Sell externally

Pays

$31

Receives

$30

Pays

Pays

Pays

b.

Northeast

Southwest

Company

Transfer internally

Pays

$32

Receives

$30

Pays

$ 2

Pays

Pays

Pays

15–24. (25 min.) Evaluate Transfer Pricing System: Seattle Transit Ltd.

a. Different prices:

(1) The opportunity cost might be considered the regular fare of $2.00 less the $0.50

15–25. (25 min.) Evaluate Transfer Pricing System: BGTS.

Total

Ms. Seville’s

Shares

(60% and

20%)

Mr. Turco’s

Shares

(40% and

60%)

15–26. (25 min.) International Transfer Prices–Ethical Issues: Trans Atlantic

Metals.

a. Analyze the tax liabilities in each jurisdiction using the alternative transfer prices. If the

transfer price is $30 million, the tax liabilities are:

Finland

U.S.

Sales revenue …………………………………………….

$30,000,000

$150,000,000

Third-party costs ………………………………………….

20,000,000

60,000,000

Transferred goods costs ……………………………….

Total costs ………………………………………………….

Taxable income …………………………………………..

Tax rate ……………………………………………………..

Tax liability ………………………………………………….

Total tax liability …………………………………………..

If the transfer price is $40 million, the tax liabilities are computed as follows:

Finland

U.S.

Sales revenue …………………………………………….

$40,000,000

$150,000,000

Third-party costs ………………………………………….

Transferred goods costs ……………………………….

Total costs ………………………………………………….

Taxable income …………………………………………..

Tax rate ……………………………………………………..

Tax liability ………………………………………………….

Total tax liability …………………………………………..

15–27. (20 min.) Transfer Pricing Policies – Ethical Issues: Best Practices, Inc.

a. As in 15-20, the minimum transfer price that the Corporate Division should obtain is

15–28. (20 min.) Evaluate Transfer Pricing System: San Jose Company.

15–29. (20 min.) International Transfer Prices: San Jose Company.

This exercise is designed to illustrate the conflict between the use of a transfer price to

motivate managerial decision making and the desire to minimize corporate taxes.

Ignoring the tax issues, leads to the same answers as in Exercise 15-28. However,

from a tax perspective, the company would prefer to be taxed in Country B (with a tax

rate of 40%) instead of Country A (with a tax rate of 60%). From a tax perspective,

15–30. (20 min.) Evaluate Transfer Pricing System: Dual Rates: Atascadero

Industries.

c. Although the dual-rate system allows both Division managers to show relatively high

profits, it suffers from the following defects. First, the total profit to the two divisions will

15–31. (20 min.) International Transfer Prices: Atascadero Industries.

This exercise is designed to illustrate the conflict between the use of a transfer price to

motivate managerial decision making and the desire to minimize corporate taxes.

15–32. (30 min.) Segment Reporting: Leapin’ Larry’s Pre-Owned Cars

($ in millions)

a. Using a $2 million transfer price:

Item

Operation

Division

Financing

Division

Outside sales revenue …………………………………

$17

$4

Transfer price ……………………………………………..

Total revenue ……………………………………………..

$17

Less:

Total costs …………………………………………………

b. Using a $1 million transfer price:

Item

Operation

Division

Financing

Division

Outside sales revenue …………………………………

$17

$4

Transfer price ……………………………………………..

1

Total revenue ……………………………………………..

Less:

Total costs …………………………………………………

Operating profit before tax …………………………...

$3

c. If the commercial rate for loan fees is really $1 million and assuming that Financing is

15–33. (30 min.) Segment Reporting: Perth Corporation.

($000)

Item

Casino

Hotel

Revenue:

Outside revenue ………………………………………

Total revenue …………………………………………..

Less:

Transfer ………………………………………………….

Total costs ………………………………………………

Solutions to Problems

15–34. (30 min.) Transfer Pricing With Imperfect Markets—ROI Evaluation, Normal

Costing: Oxford Company.

a. ROI for Thames Division.

b. Note: Capacity is 1,000,000 units, so regular sales would be reduced to 800,000 units

c. Because the investments will not change, we can determine the price by setting the

two incomes equal:

(800,000 x $100) + [200,000 x (TP – $40)] – $70,000,000 = $20,000,000

15–35. (30 min.) Transfer Pricing With Imperfect Markets—RI Evaluation, Normal

Costing: Oxford Company.

a. RI for Thames Division.

c. Because the investments will not change, we can determine the price by setting the

two incomes equal:

(800,000 x $100) + [200,000 x (TP – $40)] – $70,000,000 = $20,000,000

15–36. (50 min.) Evaluate Profit Impact of Alternative Transfer Decisions: Amazon

Beverages.

(All calculations are in $000.)

a. 1. The Container Division profits

Sales revenue …………………………………………….

$6,480

(= 1,200 x $5.40)

Sales revenue …………………………………………….

(= 1,200 x $15)

Sales revenue …………………………………………….

(= 1,200 x $15)

15-36. (continued)

b. 1. No

Container Division Volumes

Cases ………………………………………………………..

800

1,200

5,600

2. Yes

Mixing Division Volumes

3. Yes

Corporation Volumes

Cases ………………………………………………………..

400

800

1,200

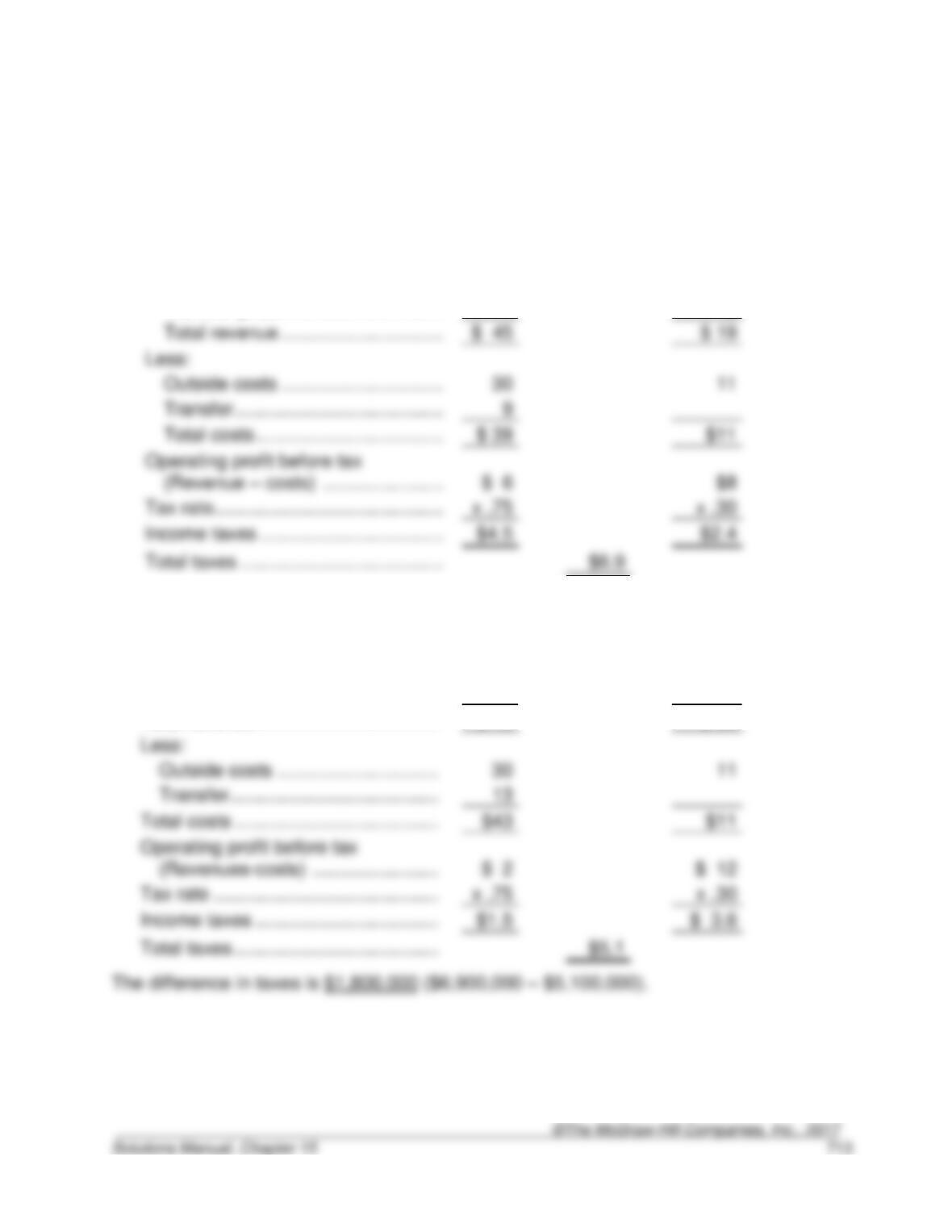

15–37. (40 min.) International Transfer Prices: Skane Shipping, Ltd.

All revenues and costs are in millions of dollars.

• Malaysian basis for transfer price:

Item

Shipping

Company

Dock

Facility

Sales revenue:

Outside sales revenue ………………………………

$ 45

$ 10

Transfer price …………………………..……………..

9

Total revenue ………………………………………….

Less:

Transfer ………………………………………………….

9

Total costs ………………………………………………

$ 39

$11

Operating profit before tax

(Revenue – costs) …………………………………..

$ 6

$8

Tax rate ……………………………………………………..

x .30

Income taxes ……………………………………………..

$4.5

$2.4

Total taxes …………………………………………………

• Sweden basis for transfer price:

Item

Shipping

Company

Dock

Facility

Outside sales revenue …………………………………

$ 45

$10

Transfer price……………………………………………..

13

Total revenue ……………………………………………..

$ 45

$ 23

Less:

Outside costs ………………………………………….

11

Transfer ………………………………………………….

Total costs …………………………………………………

$43

Operating profit before tax

(Revenues-costs) ……………………………………

$ 2

$ 12

Tax rate …………………………………………………….

x .30

Income taxes ……………………………………………..

$1.5

Total taxes …………………………………………………

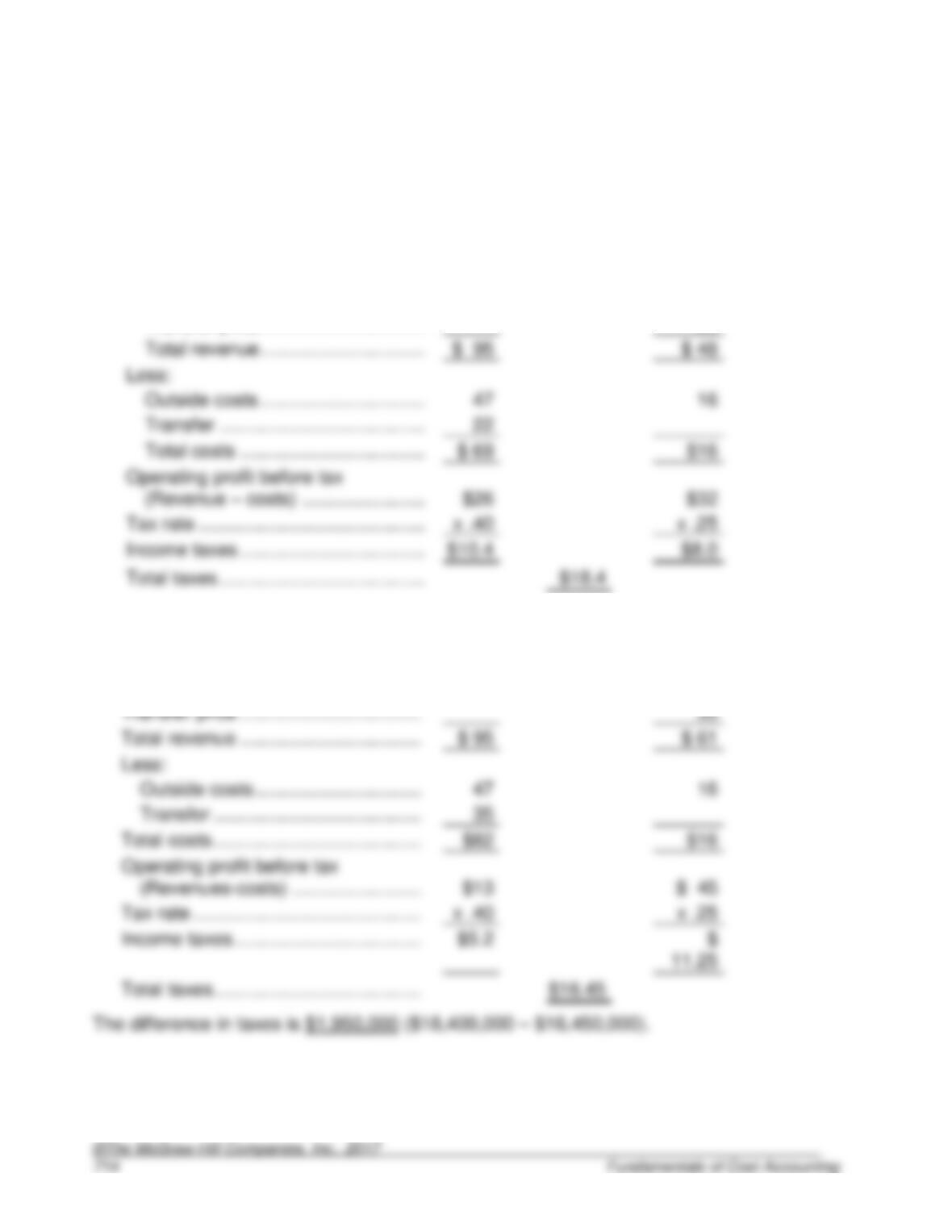

15–38. (40 min.) International Transfer Prices: Badger Air.

All revenues and costs are in millions of dollars.

• Philippine basis for transfer price:

Item

Cargo

Division

Maintenance

Division

Sales revenue:

Outside sales revenue ………………………………

$ 95

$ 26

Transfer price …………………………………………..

22

Total revenue …………………………………………..

Less:

Outside costs …………………………………………..

Transfer ………………………………………………….

Total costs ………………………………………………

Operating profit before tax

(Revenue – costs) ……………………………………

$32

Tax rate ……………………………………………………..

x .25

Income taxes ………………………………………………

$8.0

Total taxes ………………………………………………….

• US basis for transfer price:

Item

Cargo

Division

Maintenance

Division

Outside sales revenue ………………………………….

$ 95

$26

Transfer price ……………………………………………..

Total revenue …………………………..…………………

Less:

Outside costs …………………………………………..

Transfer ………………………………………………….

Total costs ………………………………………………….

$16

Operating profit before tax

(Revenues-costs) …………………………………….

$ 45

Tax rate ……………………………………………………..

x .25

Income taxes ………………………………………………

Total taxes ………………………………………………….

$16.45

15–39.

(60 min.) Analyze Transfer Pricing Data: Elsinore Electronics.

a. If Home sells 87,500 units to outside

Outside sales revenue 87,500 @ $72.00 ………..

$6,300,000

Less material and out-of-pocket costs for outside

sales (87,500 @ $7.20) ………………………….

630,000

$5,670,000

Less material and out-of-pocket costs for units

transferred (28,125 @ $7.20) ………………….

Labor costs 375,000 hrs. @ $14.40 ……………….

b. If Home sells 75,000 units to Mobile

Units transferred 75,000 @ $81 …………………….

$6,075,000

transferred (75,000 @ $7.20) ………………….

540,000

Less material and out-of-pocket costs for outside

sales (25,000 @ $7.20) ………………………….

Labor costs 375,000 hrs. @ $14.40 ……………….

Contribution margin ………………………………….

Less material and out-of-pocket costs for units

15-39. (continued)

c. and d.a

Home

Mobile

Company

Sales by Home to outside (87,500 x $72)………..

$6,300,000

$6,300,000

Sales by Home to Mobile (28,125 x $81) ………..

2,278,125

2,278,125

Sales by Mobile to outside (75,000 x $204) …….

15,300,000

Total sales ………………………………………………….

$8,578,125

Cost of labor in Home …………………………………..

Cost of units transferred to Mobile ………………….

2,278,125

by Mobile (75,000 – 28,125) x $84 ……………..

Conversion cost in Mobile $36 x 75,000 ………….

Contribution …………………………………………….

$ 2,345,625

a This is based on the optimal company policy. If Home sold 75,000 units to Mobile,

15-39 (continued)

Alternative approach.

The following is an alternative approach to determining the optimal company policy that

uses the concepts of chapter 4.

The scarce resource in this company is labor-hours. Regardless of the production plan,

the company will use 375,000 labor-hours (the maximum) because Home production for

both their own market and the Mobile market is profitable.

The value of a labor-hour used in the two alternatives is:

Used in Regular

Home Units

Used in Units

Transferred to

Mobile

Value of 1 unit …………………………………………….

$72.00

$84.00

Material and out-of-pocket cost ……………………..

7.20

7.20

Hours to make 1 unit ……………………………………

15–40. (40 min.) Transfer Pricing—Performance Evaluation Issues: Pima

Corporation.

a. Border would not supply Metro with the thermal switch for the $60 per unit price.

b. Pima would be $66 better off, in the short run, if Border supplied Metro the switch for

$60 and the kitchen appliance was sold for $594 plus markup. Assuming the $96 per

c. In the short run there is an advantage to Pima of transferring the switch at the $60

CMA adapted.

15–41. (30 min.) Evaluate Transfer Price System: Weaver, Inc.

The purpose of this problem is to illustrate possible problems that can arise when

applying static rules, such as determining the optimal transfer price in a series of

decisions over time.

15–42. (40 min.) Evaluate transfer price system: Western States Supply.

a. Northwest division management’s attitude at the present time should be positive to

each of these prices in decreasing order (obviously preferring a higher to lower price)

b. Negotiation between the two divisions is the best method to settle on a transfer price.

Western States Supply, Inc. is organized on a highly decentralized basis and each of

the four conditions necessary for negotiated transfer prices exists. These conditions

are:

• An outside market exists that provides both parties with an alternative.

c. No, the management of Western States Supply should not become involved in this

controversy. The company is organized on a highly decentralized basis which top

15–43. (30 min.) Transfer Prices and Tax Regulations—Ethical Issues: Gage

Corporation.

a. The transfer price economically optimal for Gage Corporation is $12 per unit. As

Profit after tax at the transfer price of $5 per unit

Adams Division, U.S.

Bute Division, England

Selling Price ……………………………………………….

$23.00

Transfer Price……………………………………………..

Transfers from U.S. ……………………………………..

Variable Cost………………………………………………

Shipping costs …………………………………………….

Additional processing costs …………………………..

Profit before tax …………………………………………..

Tax @ 70% ………………………………………………..

Profit after tax at the transfer price of $12 per unit

Adams Division, U.S.

Bute Division, England

Transfer Price……………………………………………..

$12.00

Selling Price ……………………………………………….

$23.00

Variable Cost………………………………………………

5.00

Transfers from U.S. ……………………………………..

$12.00

Profit ………………………………………………………

Shipping costs …………………………………………….

Tax @ 40% ………………………………………………..

Additional processing costs …………………………..

Profit after tax ……………………………………………..

Profit before tax …………………………………………..

Tax @ 70% ………………………………………………..

15–44. (40 min.) Segment Reporting: Midwest Entertainment.

a. ($ thousands)

Bus

Charters

Lodging

Concerts

Ticket

Services

Outside revenue ………………………………………….

$12,250

$5,300

$4,450

$1,600

Hotel award coupons ……………………………………

1,300

Concert discounts (bus) ……………………………….

350

(Lodging) …………………………………………………..

Crew lodging ………………………………………………

650

Ticket commissions:

Bus…………………………………………………………

200

Lodging …………………………………………………..

100

Concerts …………………………………………………

50

Total revenues …………………………………………….

$13,550

$5,950

$4,950

$1,950

Outside costs ………………………………………………

$7,850

Hotel award coupons ……………………………………

Concert discounts (bus) ……………………………….

(Lodging) …………………………………………………..

150

Crew lodging ………………………………………………

Ticket commissions:

Bus…………………………………………………………

Lodging …………………………………………………..

100

Concerts …………………………………………………

Total costs ………………………………………………….

$9,050

Operating profits ………………………………………….

$4,500

$1,600

15-44. (continued)

b. Adjust the operating profits in requirement a for the changed transfer prices.

Bus Charters

Lodging

Concerts

Ticket

Services

Operating profits (a) ……………………………………

$4,500

$850

$1,600

$450

Hotel awards ………………………………………………

1,050

Concert discounts ……………………………………….

Operating profits (b) ……………………………………

$3,750

$1,900

$1,300

$450

c. Divide the operating profits in requirements a and b by division assets, which are given

in the problem. The following rankings result:

For (a):

Ticket services ………………………………………..

13.85%

=

($450 ÷ $3,250)

=

($1,600 ÷ $16,050)

=

($4,500 ÷ $47,750)

Lodging ………………………………………………….

=

($850 ÷ $19,250)

For (b):

=

($450 ÷ $3,250)

Lodging ………………………………………………….

=

($1,900 ÷ $19,250)

=

($1,300 ÷ $16,050)

=

($3,750 ÷ $47,750)

15–45. (20 min.) Two-Part Transfer Prices: Mathes Corporation.

a.

Mathes should transfer at the Landfill’s variable cost of receiving and processing the

material. Because the Landfill has excess capacity after satisfying all market demand that

preparing the landfill.

b.

Based on budgeted Landfill Costs:

15–46. (20 min.) Budget Versus Actual Costs: Mathes Corporation.

15–47. (20 min.) Two-Part Transfer Prices: CHS.

a.

This is a complicated problem, because of the requirement for a new server that would not

exist without the demands of Optics. (It is made less complicated by the fact that Health

Services leases the machine.) There is excess capacity on the machine, so the optimal

Therefore, the optimal transfer price consists of two parts:

Fixed:

Incremental lease cost ……………

($5,000 – $3,200)

$1,800

Incremental support cost …………

20,000

Less maintenance savings ………

Variable cost …………………………….

b.

Variable costs ……………………………………………..

15-47. (continued)

c.

Fixed fee ……………………………………………………

$21,000

Variable costs …………………………………………….

100

Average hourly cost …………………………………….

15–48. (20 min.) Two-Part Transfer Prices: CHS.

a.

Solutions to Integrative Cases

15–49. Custom Freight Systems (A): Transfer Pricing.

a. The Logistics division should accept the bid from Forwarders division. Custom Freight

Option I: Purchase Internally

Air Cargo

Division

Forwarders

Division

Logistics

Division

b. If we assume it is optimal for the transfer to be made internally, then the question

arises as to the appropriate transfer price. The economic transfer pricing rule for

making transfers to maximize a company’s profits is to transfer at the differential outlay

15-49. (continued)

c. Espinosa has many alternatives to intervention or to forcing the manager of the

Forwarders division to lower his price below $210. Each has advantages and

disadvantages.

• Espinosa must trade off the benefits of intervention on this particular transaction

d. The reward system at Custom Freight Systems creates an environment that

15–50. (30 min.) Custom Freight Systems (B): Transfer Pricing.

Similar to Case A, the Logistics division should accept the bid from the Forwarders

division. However, if we eliminate the Forwarders Division from the bidding process, the

Option I: (from 15–49) Purchase internally

Air Cargo

Division

Forwarders

Division

Logistics

Division

Sales revenue ……………………………….

$155

$210

–0–

Variable Costs ………………………………

Operating Profit/(Cost) ……………………

$ 62

$ 35

Option II: (from 15–49) Purchase externally (United Systems)

Option III: Purchase Externally (World Systems)

Air Cargo

Division

Forwarders

Division

Logistics

Division

Sales revenue ……………………………….

$155

Operating Profit (Cost) ……………………

$ 62