Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1. Horizontal analysis is the analysis of increases and decreases in financial statement items. The

change in the amount and the percentage increase (decrease) in the item is presented. The amount

2. Comparative statements provide information as to changes between dates or periods. Trends

3. Before this question can be answered, the increase in net income should be compared with

changes in sales, expenses, and assets devoted to the business for the current year. The return

5. a. A high inventory turnover minimizes the amount invested in inventories, thus freeing

funds for more advantageous use. Storage costs, administrative expenses, and losses

6. The ratio of fixed assets to long-term liabilities increased from 3.4 for the preceding year to

7. a. The rate earned on total assets adds interest expense to the net income, which is divided

b

y average total assets. It measures the profitability of the total assets, without regard for how

CHAPTER 15

FINANCIAL STATEMENT ANALYSIS

DISCUSSION QUESTIONS

15-1

CHAPTER 15 Financial Statement Analysis

DISCUSSION QUESTIONS (Concluded)

8. The price-earnings ratio measures the market’s expectations of a company’s future earnings

9. The dividend yield measures the rate of return common stockholders receive from a cash dividend.

10. One report is the Report on Internal Control, which verifies management’s conclusions on

15-2

CHAPTER 15 Financial Statement Analysis

PE 15–1A

PE 15–1B

PE 15–2A

Amount Percentage

PE 15–2B

Amount Percentage

PE 15–3A

= 2.2

= 1.5

PRACTICE EXERCISES

CHAPTER 15 Financial Statement Analysis

PE 15–3B

a. Current Ratio = Current Assets ÷ Current Liabilities

= 3.0

b. Quick Ratio = Quick Assets ÷ Current Liabilities

PE 15–4A

= 10.4

Average Accounts Receivable

Average Daily Sales

PE 15–4B

a. Accounts Receivable Turnover = Sales ÷ Average Accounts Receivable

Average Accounts Receivable

Average Daily Sales

b. =

b. =Number of Days’ Sales in Receivables

Number of Days’ Sales in Receivables

CHAPTER 15 Financial Statement Analysis

PE 15-5A

a. Inventory Turnover = Cost of Goods Sold ÷ Average Inventory

Average Inventory

Average Daily Cost of Goods Sold

PE 15–5B

a. Inventory Turnover = Cost of Goods Sold ÷ Average Inventory

Average Inventory

Average Daily Cost of Goods Sold

=$72,500 ÷ ($435,000 ÷ 365)

b. =

b. =

Number of Days’ Sales in Inventory

Number of Days’ Sales in Inventory

15-5

CHAPTER 15 Financial Statement Analysis

PE 15–6A

PE 15–6B

PE 15–7A

PE 15–7B

Fixed Assets

Long-Term Liabilities

Total Liabilities

Total Stockholders’ Equity

Total Stockholders’ Equity

=

Ratio of Fixed Assets to Long-Term Liabilities

Ratio of Liabilities to Stockholders’ Equity

Ratio of Fixed Assets to Long-Term Liabilities

Number of Times

Interest Charges Are Earned =

Number of Times

Interest Charges Are Earned

Interest Expense

Interest Expense

Income Before Income Tax +

=

Income Before Income Tax +

Interest Expense

Interest Expense

Total Liabilities

Fixed Assets

Long-Term Liabilities

a.

b. =

b. =

a. =

Ratio of Liabilities to Stockholders’ Equity

15-6

CHAPTER 15 Financial Statement Analysis

PE 15–8A

Ratio of Sales to Assets = Sales ÷ Average Total Assets

PE 15–8B

Ratio of Sales to Assets = Sales ÷ Average Total Assets

PE 15–9A

PE 15–9B

$410,000 + $90,000

$5,000,000

=

Rate Earned on Total Assets = Net Income + Interest Expense

Average Total Assets

Rate Earned on Total Assets =

Net Income + Interest Expense

Average Total Assets

15-7

CHAPTER 15 Financial Statement Analysis

PE 15–10A

PE 15–10B

b. Net Income – Preferred Dividends

Average Common Stockholders’ Equity

a. Rate Earned on Stockholders’ Equity = Net Income

Average Stockholders’ Equity

a. Rate Earned on Stockholders’ Equity = Net Income

Average Stockholders’ Equity

b. Rate Earned on Common

Stockholders’ Equity =Net Income – Preferred Dividends

Average Common Stockholders’ Equity

=

Rate Earned on Common

Stockholders’ Equity

CHAPTER 15 Financial Statement Analysis

PE 15-11A

PE 15–11B

b. Market Price per Share of Common Stock

Earnings per Share on Common Stock

Price-Earnings Ratio =

a. Net Income – Preferred Dividends

Shares of Common Stock Outstanding

$7.00

Earnings per Share

on Common Stock =

a. =

Earnings per Share

on Common Stock

Net Income – Preferred Dividends

Shares of Common Stock Outstanding

=Price-Earnings Ratiob. Market Price per Share of Common Stock

Earnings per Share on Common Stock

15-9

CHAPTER 15 Financial Statement Analysis

Ex. 15–1

a.

Amount Percent Amount Percent

Sales $2,500,000 100% $2,350,000 100%

Cost of goods sold 1,500,000 60% 1,292,500 55%

Gross profit $1,000,000 40% $1,057,500 45%

b. The vertical analysis indicates that the cost of goods sold as a percent of sales

increased by 5 percentage points (60% – 55%), while selling expenses decreased

Current year Previous year

EXERCISES

GRESHAM, Inc.

Comparative Income Statement

For the Years Ended December 31, 20—

15-10

CHAPTER 15 Financial Statement Analysis

Ex. 15–2

a.

Amount Percent Amount Percent

Revenues:

Admissions $116,034 23.7% $130,239 25.7%

Expenses and other:

Direct expense of events $101,402 20.7% $106,204 21.0%

NASCAR purse and

sanction fees 122,950 25.1% 120,146 23.7%

b. Overall revenue decreased some between the two years, as did the overall mix of

revenue sources. The NASCAR broadcasting revenue increased by almost 3% of

total revenue, while admissions revenue decreased by 2% of total revenue. One

of the major expense categories, NASCAR purse and sanction fees, increased by

1.3% of total revenue. The Direct expenses of events and Other direct expenses

remained relatively constant during the two year period. General and administrative

Current Year Prior Year

SPEEDWAY MOTORSPORTS, INC.

Comparative Income Statement (in thousands of dollars)

For the Years Ended December 31, 20—

15-11

CHAPTER 15 Financial Statement Analysis

Ex. 15–3

a.

Amount Percent

Net sales $4,000,000 100%

Operating income 160,000 4%

Other income 120,000 3%

$ 280,000 7%

Other expense 80,000 2%

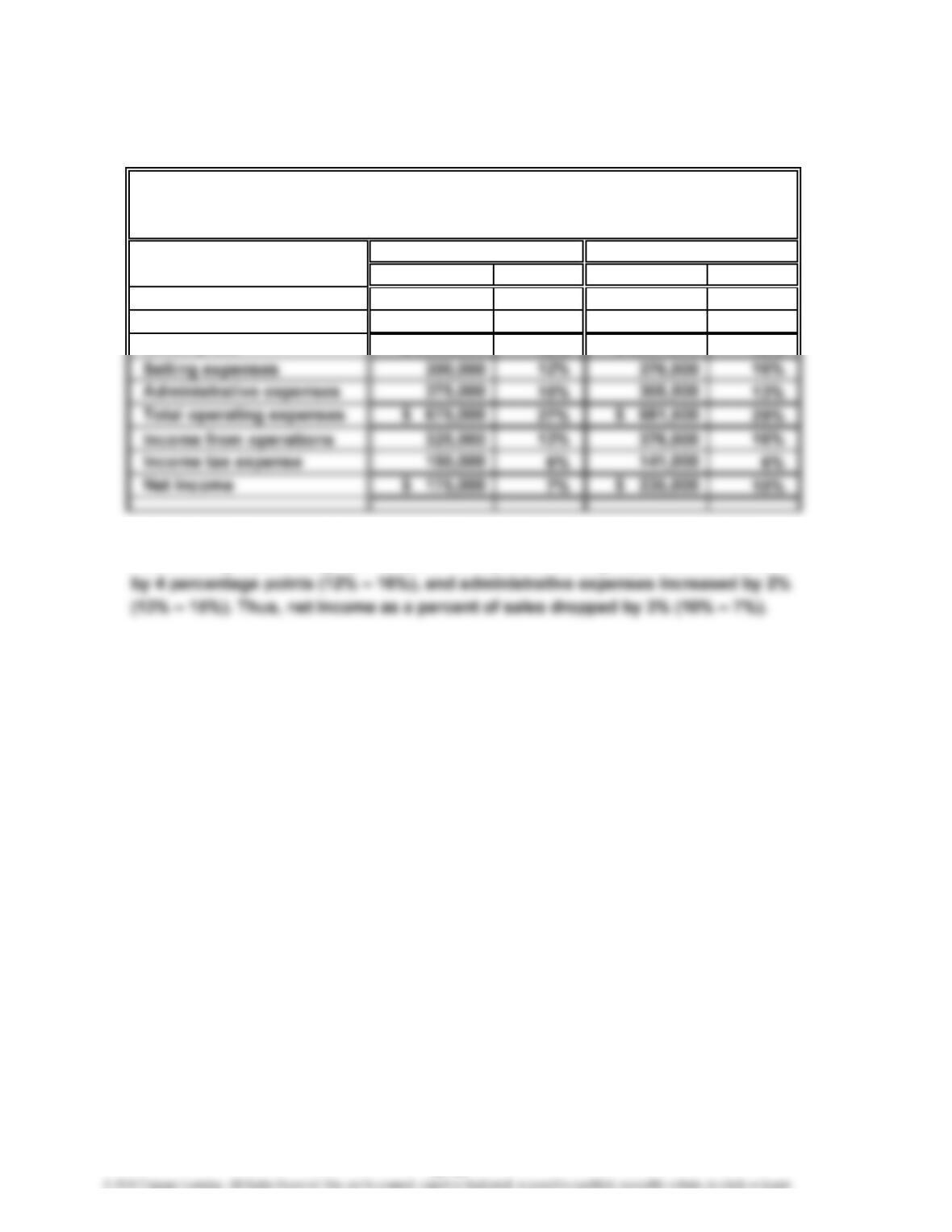

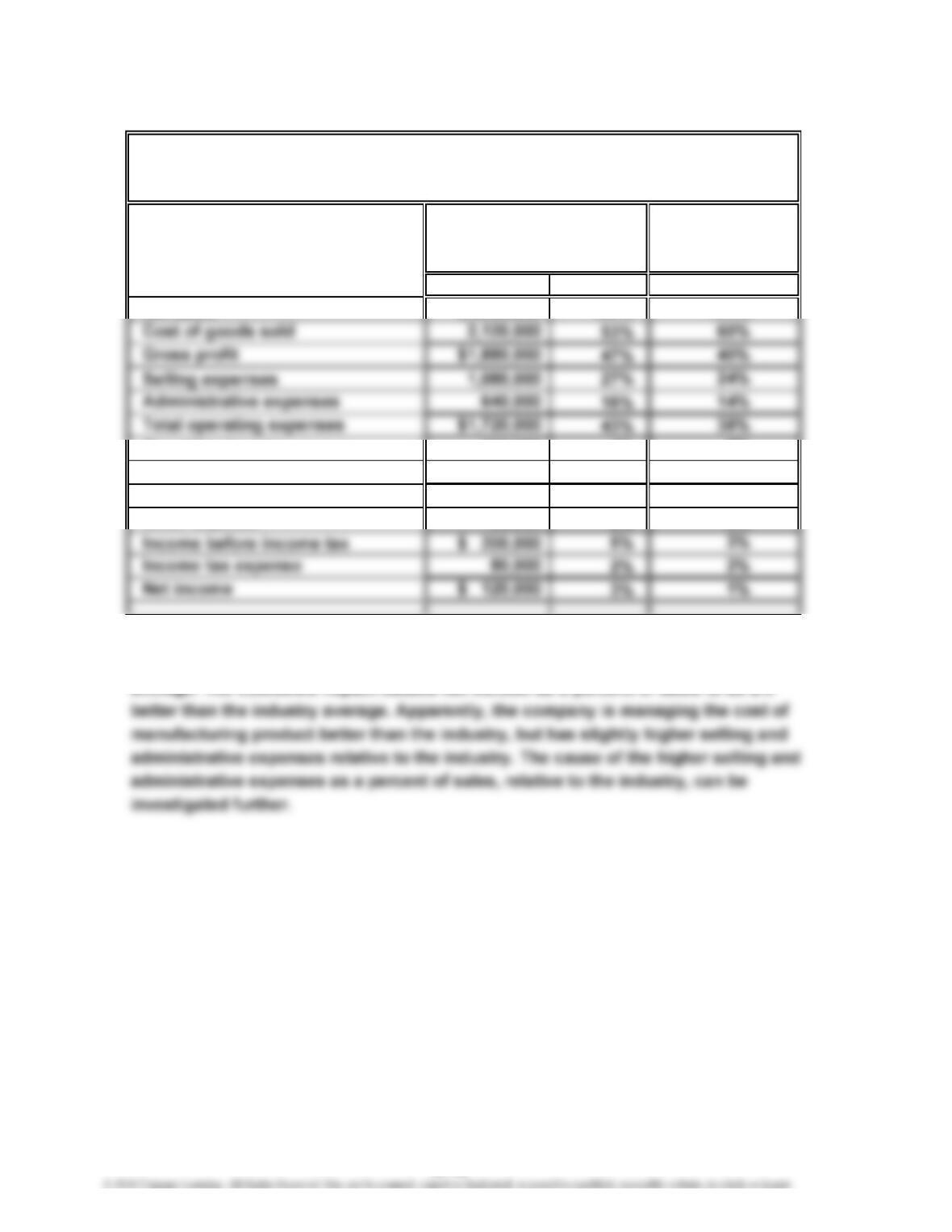

b. The cost of goods sold is 7% lower than the industry average, but the selling

expenses and administrative expenses are 3% and 2% higher than the industry

average. The combined impact causes net income as a percent of sales to be 2%

Electronics

TANNENHILL COMPANY

Common-Sized Income Statement

For the Year Ended December 31, 20—

Tannenhill

Company

Industry

Average

100%

2%

5%

2%

3%

15-12

CHAPTER 15 Financial Statement Analysis

Ex. 15–4

Amount Percent Amount Percent

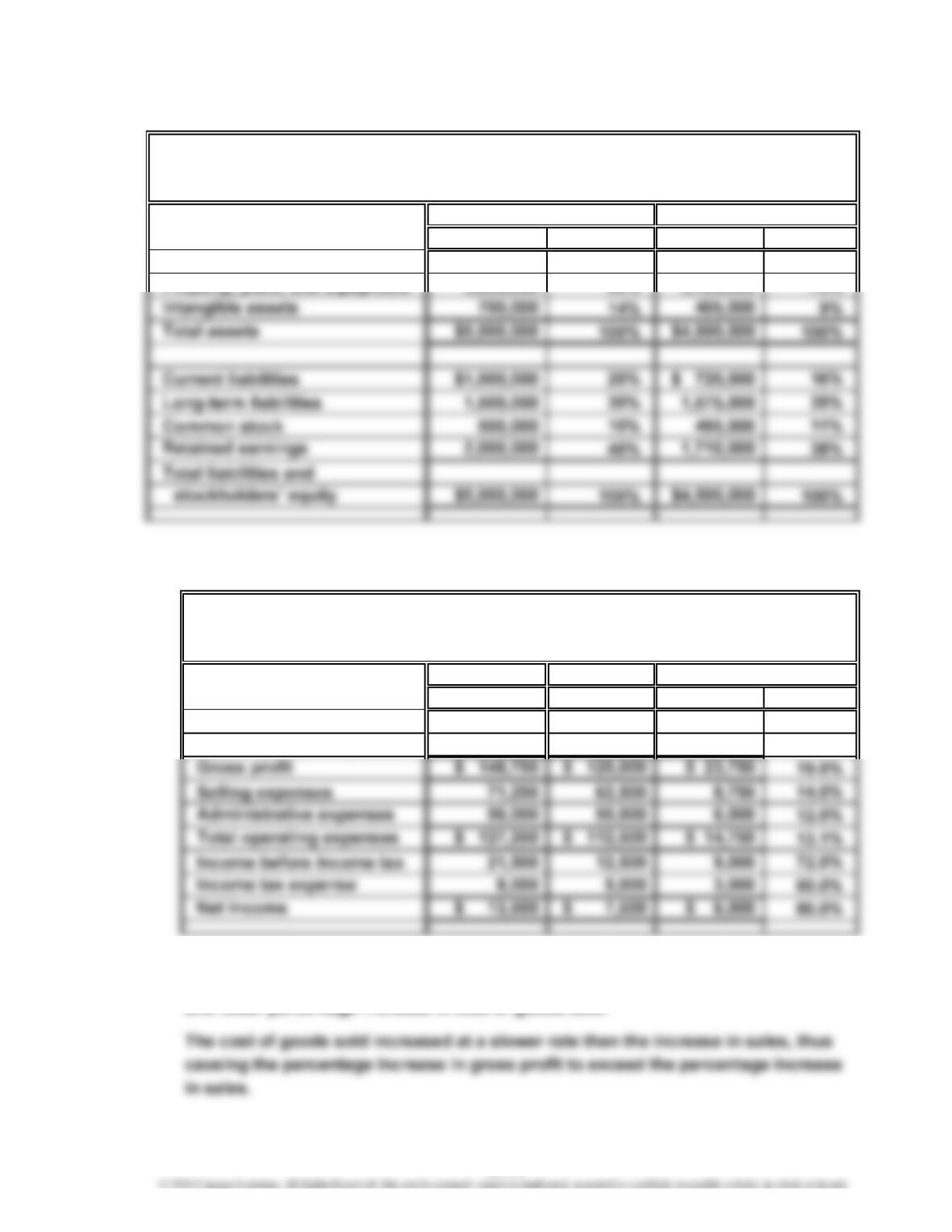

Current assets $1,300,000 26% $ 945,000 21%

Ex. 15–5

a.

Current year Previous year

Amount Amount Amount Percent

Sales $1,120,000 $1,000,000 $120,000 12.0%

Cost of goods sold 971,250 875,000 96,250 11.0%

b. The net income for Moreno Company increased by approximately 80% between

years. This increase was the combined result of an increase in sales of 12%

and lower percentage increase in cost of goods sold.

NOVAK COMPANY

Comparative Balance Sheet

For the Years Ended December 31, 20—

Increase (Decrease)

MORENO COMPANY

Comparative Income Statement

For the Years Ended December 31, 20—

Current year Previous year

15-13

CHAPTER 15 Financial Statement Analysis

Ex. 15–6

a. (1) Working Capital = Current Assets – Current Liabilities

b. The liquidity of Gostkowski has improved from the preceding year to the current

Ex. 15–7

b. The solvency of PepsiCo has increased slightly over this time period. The

current ratio has increased from 1.0 to 1.1, and the quick ratio has increased by

0.2. PEPSICO appears to have ample resources to meet its short term

Current Assets

Current Liabilities

Quick Assets

Current Liabilities

Current Assets

Current Liabilities

= 1.0

$17,089 $18,154

= 1.1

a.

=(2) Current Ratio

(1) Current Ratio =

(3) Quick Ratio =

Current Year: $18,720 Previous Year: $17,441

15-14

CHAPTER 15 Financial Statement Analysis

Ex. 15–8

a. The working capital, current ratio, and quick ratio are calculated incorrectly. The

working capital and current ratio incorrectly include intangible assets and property,

plant, and equipment as a part of current assets. Both are noncurrent. The quick

ratio has both an incorrect numerator and denominator. The numerator of the quick

ratio is incorrectly calculated as the sum of inventories, prepaid expenses, and

The correct calculations are as follows:

= Current Assets – Current Liabilities

= $330,000 – $300,000

$330,000

$300,000

b. Unfortunately, the working capital, current ratio, and quick ratio are below the

minimum threshold required by the bond indenture. This may require the company

Working Capital

$30,000

Current Assets

Current Liabilities

=

1.1

0.9

$300,000 =

=

=

=

Current Ratio

15-15

CHAPTER 15 Financial Statement Analysis

Ex. 15–9

$487,500

$9,349

1

$487,500 = ($475,000 + $500,000) ÷ 2

Average Accounts Receivable

Average Accounts Receivable

Average Daily Sales

Sales

58.9 days

$457,500 =

(2)

$7,771

2016: = 52.1 days 2015:

=Number of Days’ Sales in Receivables

a. (1)

=

Accounts Receivable Turnover

1

2

3

4

15-16

CHAPTER 15 Financial Statement Analysis

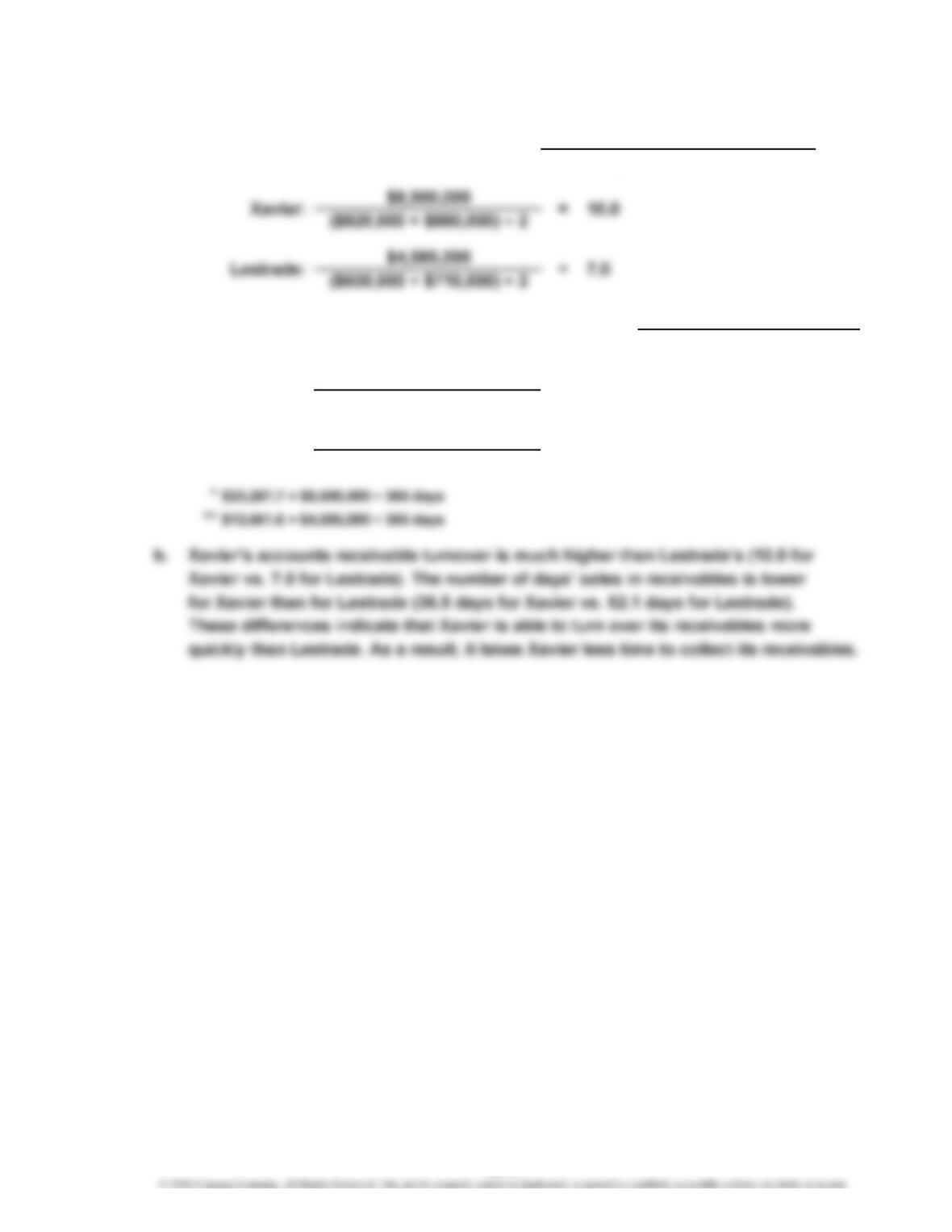

Ex. 15–10

52.1 days

Accounts Receivable Turnover Average Accounts Receivable

Sales

Lestrade: ($600,000 + $710,000) ÷ 2

$12,561.6 =

Average Accounts Receivable

Average Daily Sales

36.5 days

=

a. (1)

=

(2)

Number of Days’ Sales in Receivables

Xavier: =

($820,000 + $880,000) ÷ 2

$23,287.7

*

**

15-17

CHAPTER 15 Financial Statement Analysis

Ex. 15–11

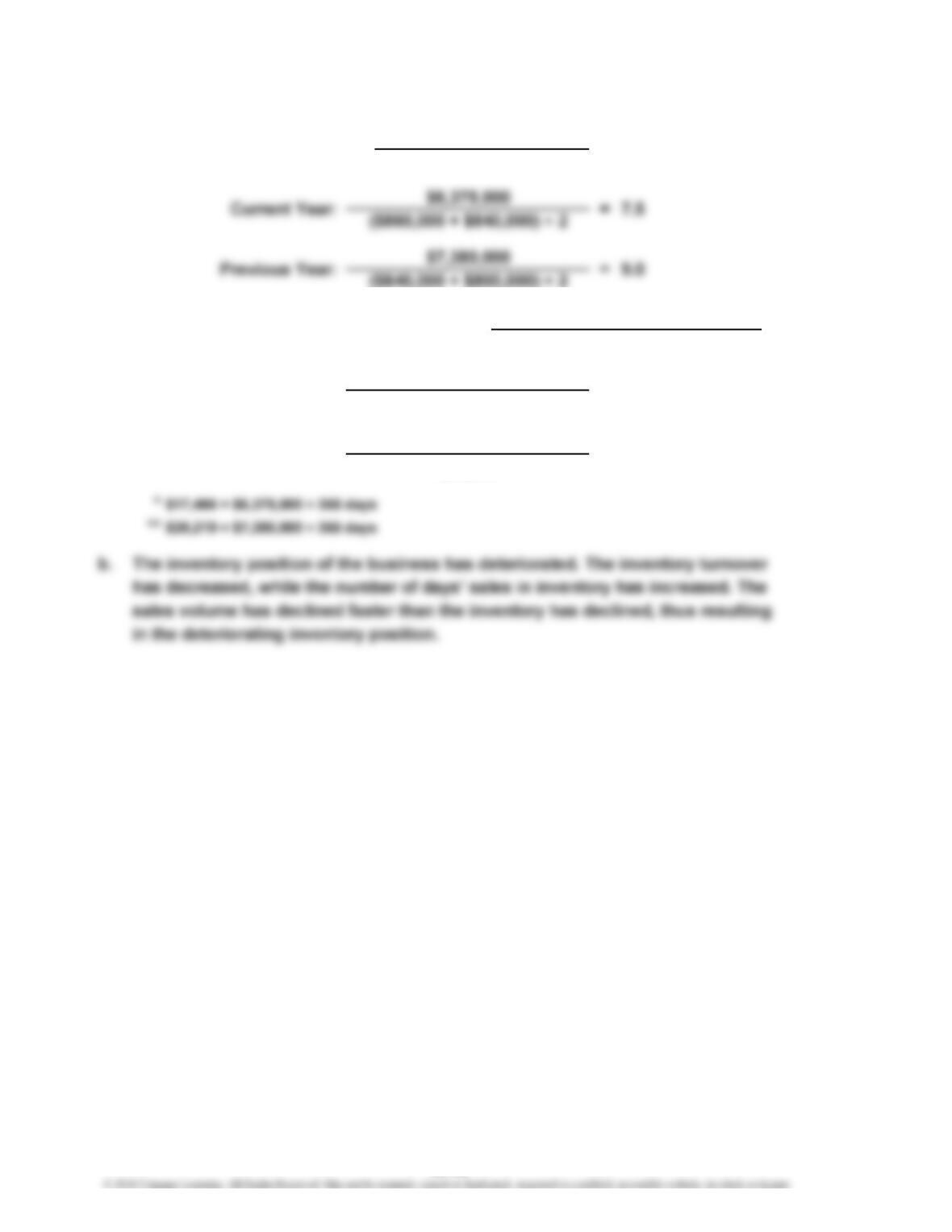

Number of Days’ Sales in Inventory

Inventory Turnover

a. (1)

=

Cost of Goods Sold

Average Inventory

(2)

48.7 days

40.6 days=

=

=Average Inventory

Average Daily Cost of Goods Sold

($860,000 + $840,000) ÷ 2

Current Year:

Previous Year:

$17,466

($840,000 + $800,000) ÷ 2

$20,219

**

*

15-18

CHAPTER 15 Financial Statement Analysis

Ex. 15–12

b. Dell has a much higher inventory turnover ratio than does HP (32.1 vs. 13.4).

Likewise, Dell has a much smaller number of days’ sales in inventory (11.4 days

vs. 27.3 days). These significant differences are a result of Dell’s make-to-order

strategy. Dell has successfully developed a manufacturing process that is able to

fill a customer order quickly. As a result, Dell does not pre-build as many computers

a. (1)

Inventory Turnover =

$44,754

($6,317 + $7,490) ÷ 2

=

(2)

HP:

13.4

Cost of Goods Sold

Average Inventory

=

Number of Days’ Sales in Inventory Average Inventory

15-19

CHAPTER 15 Financial Statement Analysis

Ex. 15–13

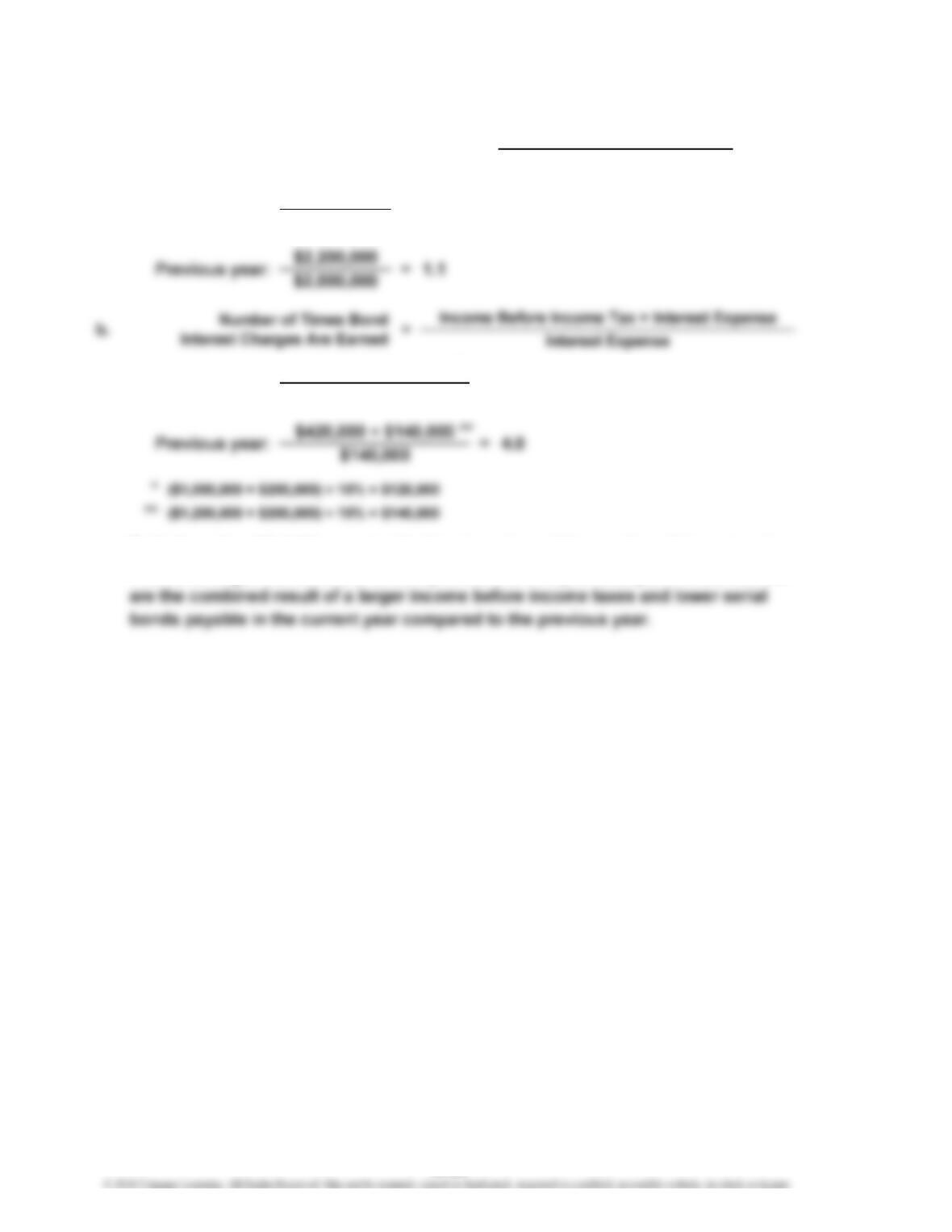

c. Both the ratio of liabilities to stockholders’ equity and the number of times bond

interest charges were earned have improved from the previous year. These results

a.

Current year:

$2,124,000

$2,360,000

=Ratio of Liabilities to Stockholders’ Equity Total Stockholders’ Equity

Total Liabilities

0.9=

$480,000 + $120,000

$120,000

5.0Current year:

=

*

15-20