EXERCISE 15-12

Plan One

Issue Stock

Plan Two

Issue Bonds

Income before interest and taxes

Interest ($2,700,000 X 10%)

Income before taxes

$800,000

—

800,000

$800,000

270,000

530,000

EXERCISE 15-13

(a) Total assets …………………………………………………… $1,000,000

Less: Total liabilities …………………………………….. 580,000

Total stockholders’ equity ……………………………… $ 420,000

EXERCISE 15-14

(a) Rent Expense …………………………………. 500

Cash ……………………………………….. 500

*EXERCISE 15-15

(a) 2017

Jan. 1 Cash ($600,000 X 103%) …………………… 618,000

Premium on Bonds Payable ………. 18,000

Bonds Payable …………………………. 600,000

(c) 2018

Jan. 1 Interest Payable ……………………………… 54,000

Cash ……………………………………….. 54,000

*EXERCISE 15-16

(a) 2016

Dec. 31 Cash ……………………………………………… 730,000

Discount on Bonds Payable ……………. 70,000

Bonds Payable ………………………… 800,000

*EXERCISE 15-17

(a) Cash …………………………..………………………………. 360,727

Discount on Bonds Payable …………………………. 39,273

Bonds Payable ……………………………………… 400,000

*EXERCISE 15-18

(a) Cash …………………………..………………………………. 407,968

Bonds Payable ……………………………………… 380,000

Premium on Bonds Payable …………………… 27,968

SOLUTIONS TO PROBLEMS

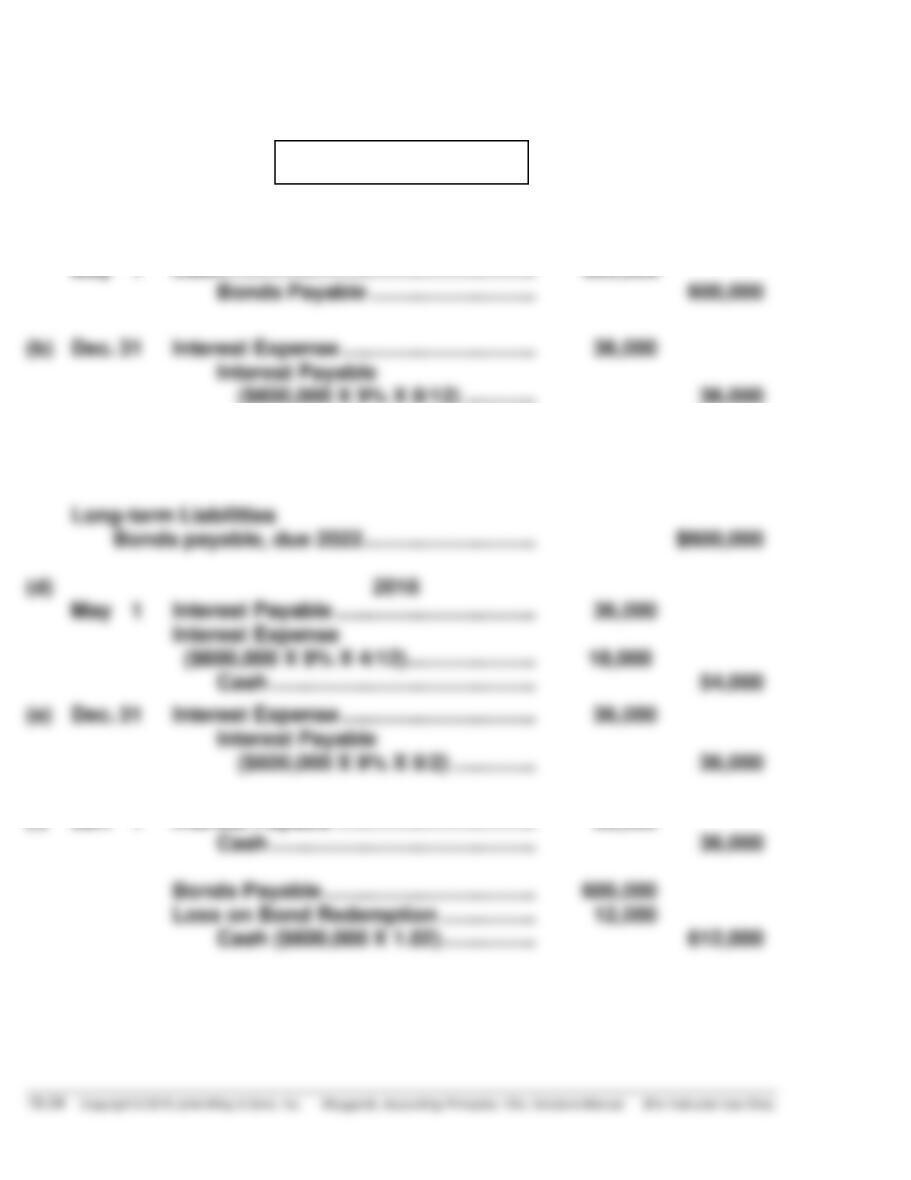

PROBLEM 15-1A

(a) 2017

May 1 Cash …………………………………………….. 600,000

Bonds Payable ………………………. 600,000

(c) Current Liabilities

Interest payable …………………………………….. $ 36,000

(d) 2018

May 1 Interest Payable ……………………………. 36,000

Interest Expense

($600,000 X 9% X 4/12)…………………. 18,000

(f) Jan. 1 Interest Payable ……………………………. 36,000

Cash ……………………………………… 36,000

PROBLEM 15–2A

(a) 2017

Jan. 1 Cash ($6,000,000 X 98%) ……………… 5,880,000

Discount on Bonds Payable ………….. 120,000

Bonds Payable …………………….. 6,000,000

PROBLEM 15-3A

(a) Jan. 1 Interest Payable ………………………….. 40,000

Cash ……………………………………. 40,000

(b) Jan. 1 Bonds Payable ……………………………. 200,000

Loss on Bond Redemption ………….. 6,000

PROBLEM 15-4A

(a)

Annual

Interest Period

Cash

Payment

Interest

Expense

Reduction of

Principal

Principal

Balance

Issue Date

1

2

$59,612

59,612

$32,000

29,791

$27,612

29,821

$400,000

372,388

342,567

(b) 2016

Dec. 31 Cash ……………………………………………… 400,000

Mortgage Payable ……………………. 400,000

(c) 12/31/17

Current Liabilities

Current portion of mortgage payable $ 29,821**

PROBLEM 15-5A

(a) Ruggiero Inc. should record the Judson Delivery lease as a capital

lease because: (1) the lease term is greater than 75% of the estimated

economic life of the leased property and (2) the present value of the

lease payments is 90% or more of the fair value of the computer. It should

be noted that only one condition needs to be met to require

capitalization.

(b) The Hester Co. lease is an operating lease. The entry to record the

lease payment in 2017 therefore is as follows:

(c) The Judson Delivery lease is a capital lease. The entry to record the

capital lease on January 1, 2017 therefore is as follows:

*PROBLEM 15-6A

(a) 2017

Jan. 1 Cash ($3,000,000 X 104%) ……………. 3,120,000

Bonds Payable …………………….. 3,000,000

Premium on Bonds Payable……. 120,000

(b) See page 15-30.

(c) 2017

Dec. 31 Interest Expense …………………………. 288,000

(d) Current Liabilities

Interest payable …………………………………… $ 300,000

*PROBLEM 15-6A (Continued)

(b)

Annual

Interest

Periods

(A)

Interest to

Be Paid

(10% X $3,000,000)

(B)

Interest Expense

to Be Recorded

(A) – (C)

(C)

Premium

Amortization

($120,000 ÷ 10)

(D)

Unamortized

Premium

(D) – (C)

(E)

Bond

Carrying Value

[$3,000,000 + (D)]

Issue date

1

2

$300,000

300,000

$288,000

288,000

$12,000

12,000

$120,000

108,000

96,000

$3,120,000

3,108,000

3,096,000

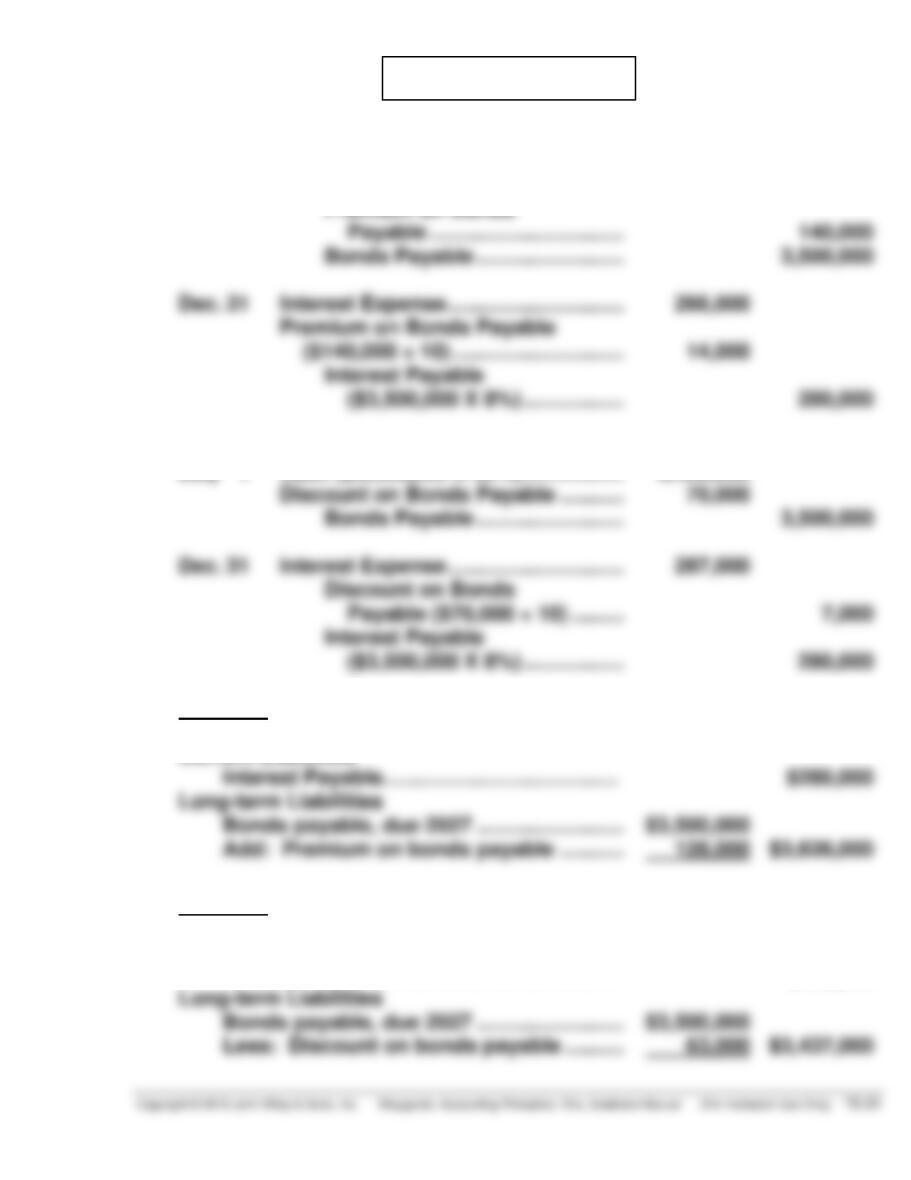

*PROBLEM 15-7A

(a) 2017

July 1 Cash ($3,500,000 X 104%) …………… 3,640,000

Premium on Bonds

Payable …………………………... 140,000

Bonds Payable ……………………. 3,500,000

(b) 2017

July 1 Cash ($3,500,000 X 98%) …………….. 3,430,000

Discount on Bonds Payable ……….. 70,000

Bonds Payable ……………………. 3,500,000

(c) Premium

Current Liabilities

Interest Payable…………………………………. $280,000

Long-term Liabilities

Discount

Current Liabilities

Interest Payable…………………………………. $280,000

*PROBLEM 15-8A

(a) 2018

Jan. 1 Interest Payable ………………………… 210,000

Cash ………………………………….. 210,000

(b) Dec. 31 Interest Expense ……………………….. 190,000

(c) 2019

Jan. 1 Bonds Payable ………………………….. 1,200,000

Premium on Bonds Payable ………. 72,000

(d) Dec. 31 Interest Expense ……………………….. 114,000

Premium on Bonds Payable ………. 12,000

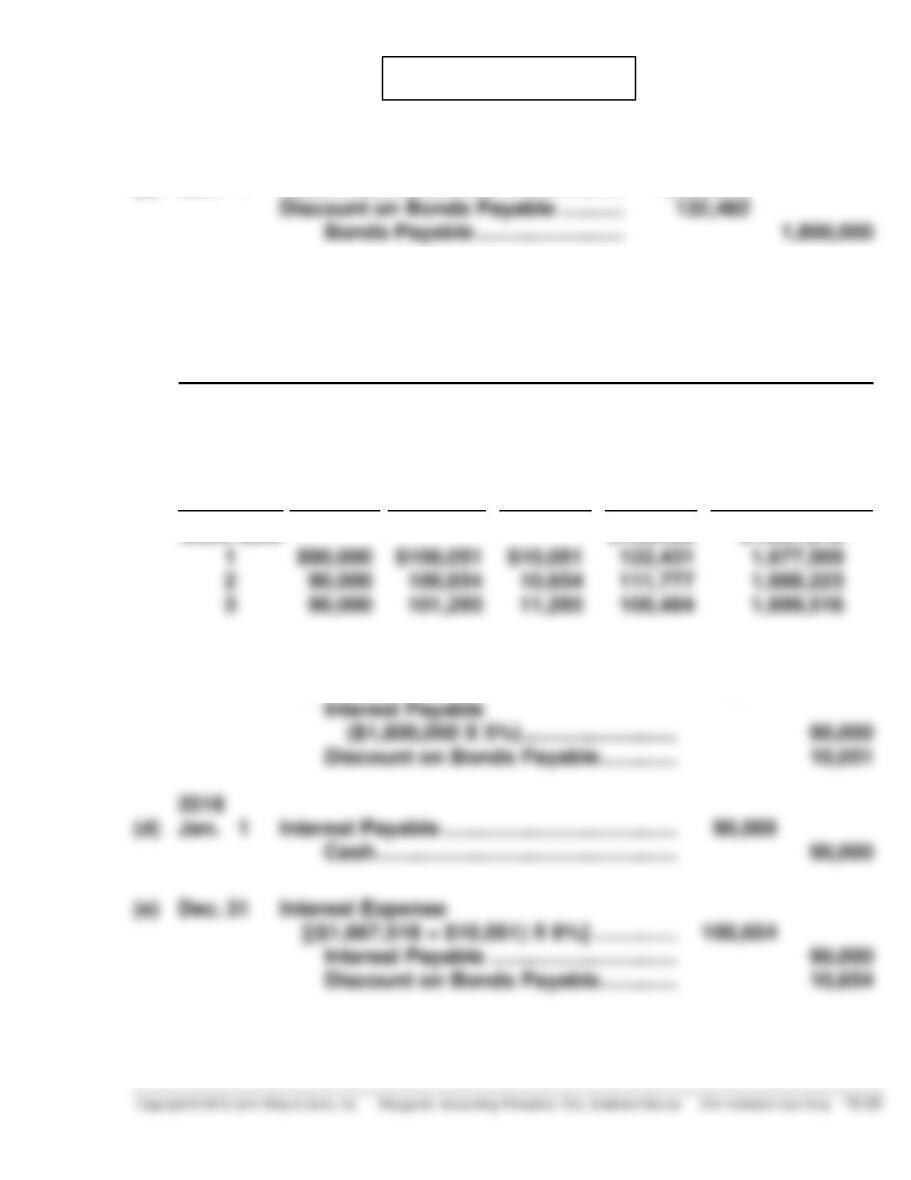

*PROBLEM 15-9A

2017

(a) Jan. 1 Cash …………………………………………. 1,667,518

(b) LOCK CORP.

Bond Discount Amortization

Effective-Interest Method—Annual Interest Payments

5% Bonds Issued at 6%

Annual

Interest

Periods

(A)

Interest

to Be

Paid

(B)

Interest

Expense

to Be

Recorded

(C)

Discount

Amor-

tization

(B) – (A)

(D)

Unamor-

tized

Discount

(D) – (C)

(E)

Bond

Carrying

Value

($1,800,000 – D)

Issue date

1

$90,000

$100,051

$10,051

$132,482

122,431

$1,667,518

1,677,569

(c) Dec. 31 Interest Expense

($1,667,518 X 6%) ……………………………. 100,051

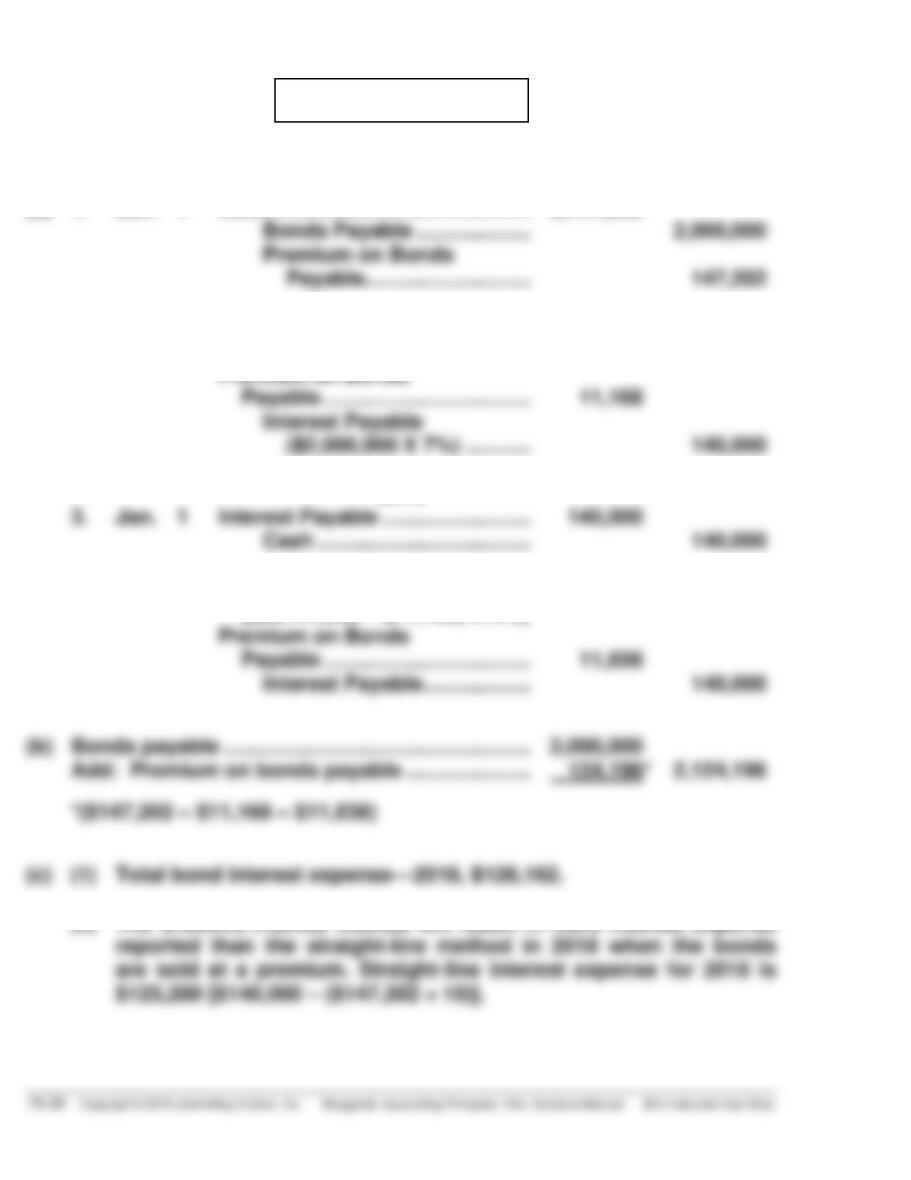

*PROBLEM 15-10A

2017

(a) 1. Jan. 1 Cash …………………………………….. 2,147,202

Bonds Payable ………………. 2,000,000

Premium on Bonds

Payable………………………. 147,202

2. Dec. 31 Interest Expense

($2,147,202 X 6%) ………………. 128,832

2018

3. Jan. 1 Interest Payable ……………………. 140,000

Cash ……………………………… 140,000

4. Dec. 31 Interest Expense …………………… 128,162

[($2,147,202 – $11,168) X 6%]

(b) Bonds payable ……………………………………………. 2,000,000

Add: Premium on bonds payable ………………… 124,196* 2,124,196

COMPREHENSIVE PROBLEM: CHAPTERS 13 TO 15

(a) 1. Cash…………………………………………………………. 22,000

Preferred Stock (1,000 X $20) ……………….. 20,000

Paid-in Capital in Excess of

Par—PS ……………………………………………. 2,000

4. Cash Dividends …………………………………………. 6,750*

Dividends Payable ……………………………….. 6,750

*$20,000 X .06 + [(3,000 + 1,000 – 300) X $1.50]

5. Bad Debt Expense …………………………………….. 4,650

Allowance for Doubtful

Accounts ($5,100 – $450) ………………….. 4,650

8. Unearned Rent Revenue ($8,000 X 3/4) ……….. 6,000

Rent Revenue………………………………………. 6,000

COMPREHENSIVE PROBLEM (Continued)

(b) QUIGLEY CORPORATION

Adjusted Trial Balance

December 31, 2017

Debit

Credit

Cash ………………………………………………………..

Accounts Receivable ………………………………..

Inventory …………………………………………………

Allowance for Doubtful Accounts ……………..

Accumulated Depreciation—Buildings ………

Accumulated Depreciation—Equipment …….

Accounts Payable …………………………………….

Interest Payable …………………………..…………..

Dividends Payable ……………………………………

Treasury Stock …………………………………………

Cash Dividends ………………………………………..

Sales Revenue …………………………………………

Rent Revenue …………………………………………..

Bad Debts Expense …………………………..……..

Interest Expense ………………………………………

$ 55,800

51,000

22,700

14,700

6,750

4,650

5,000

$ 5,100

33,000

18,000

19,300

5,000

6,750

570,000

6,000