PROBLEM 15-2C

(a) 2017

Jan. 1 Cash ($800,000 X 1.05) ………………….. 840,000

Bonds Payable ………………………. 800,000

Premium on Bonds Payable ……. 40,000

(b) Current Liabilities

Interest payable ($800,000 X 9%) …………………….. $72,000

(c) 2019

Jan. 1 Bonds Payable ……………………………… $800,000

Premium on Bonds Payable ………….. 32,000

PROBLEM 15-3C

(a) Jan. 1 Interest Payable …………………………... 84,000

Cash …………………………………….. 84,000**

(b) Jan. 1 Bonds Payable …………………………….. 300,000

PROBLEM 15-4C

(a)

Annual

Interest Period

Cash

Payment

Interest

Expense

Reduction

of Principal

Principal

Balance

Issue Date

1

2

$89,418

89,418

$48,000

44,687

$41,418

44,731

$600,000

558,582

513,851

(b) 2016

Dec. 31 Cash …………………………………………….. 600,000

Mortgage Payable …………………… 600,000

2017

(c) 12/31/17

Current Liabilities

Current portion of mortgage payable $ 44,731**

PROBLEM 15-5C

(a) Gomez Enterprises should record the Rich Co. lease as a capital lease

because the lease term is greater than 75% of the estimated economic

life of the leased property.

(b) The Rich Co. lease is a capital lease. The entry to record the capital

lease on January 1, 2017 therefore is as follows:

(c) The Pagel Inc. lease is an operating lease. The entry to record the

lease payment in 2017 therefore is as follows:

*PROBLEM 15-6C

(a) 2016

Jan. 1 Cash ($6,000,000 X 96%) ……………… 5,760,000

(b) See page 15-17.

(c) 2016

Dec. 31 Interest Expense …………………………. 552,000

Discount on Bonds

2017

Jan. 1 Interest Payable ………………………….. 540,000

Cash ……………………………………. 540,000

(d) Current Liabilities

Interest payable …………………………………. $ 540,000

*PROBLEM

15-6C (Continued)

Annual

Interest

Periods

(A)

Interest to

Be Paid

(9% X $6,000,000)

(B)

Interest

Expense

to Be Recorded

(A) + (C)

(C)

Discount

Amortization

($240,000 ÷

20)

(D)

Unamortized

Discount

(D) – (C)

(E)

Bond

Carrying Value

[$6,000,000 –

(D)]

Issue date

1

$540,000

$552,000

$12,000

$240,000

228,000

$5,760,000

5,772,000

*PROBLEM 15-7C

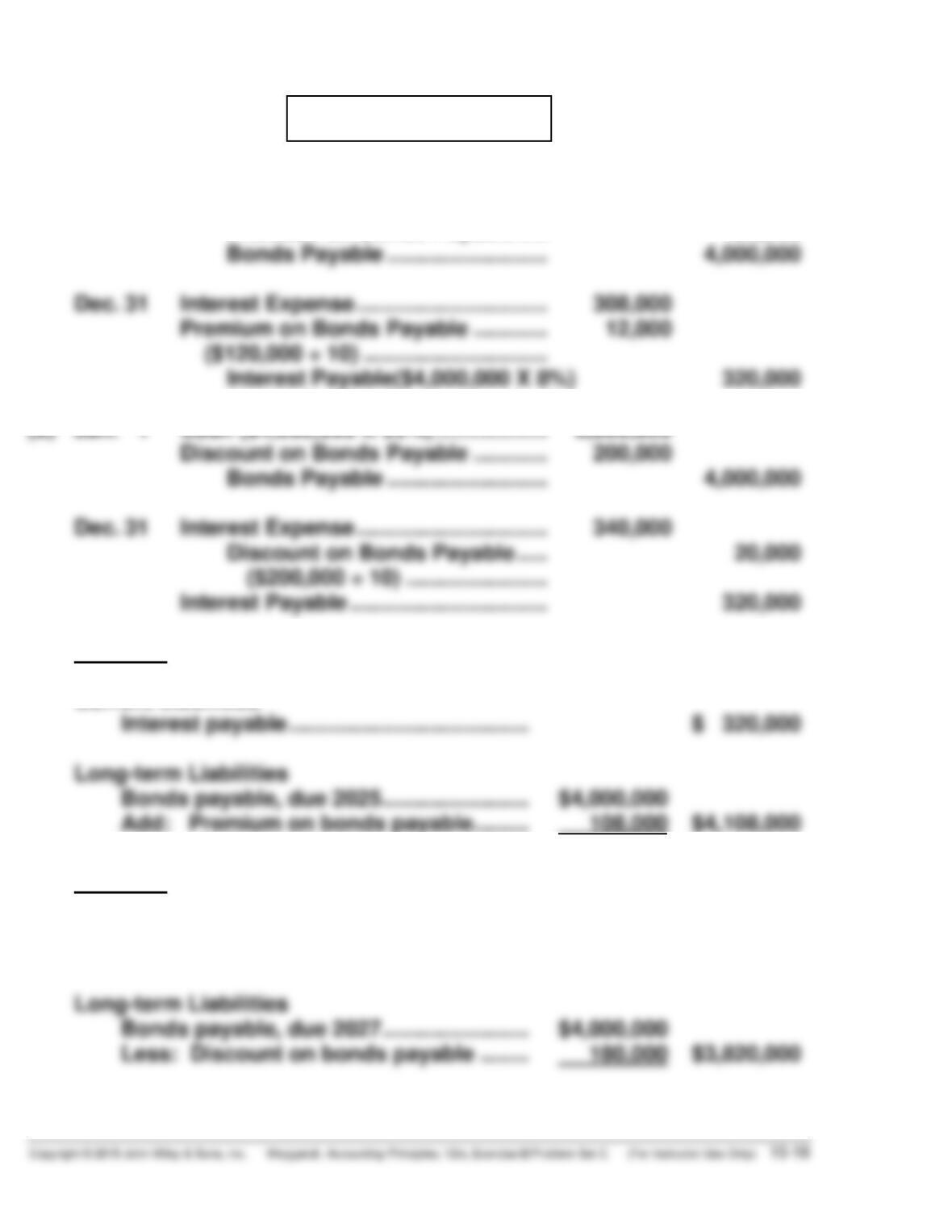

(a) Jan. 1 Cash ($4,000,000 X 103%) ……………. 4,120,000

Premium on Bonds Payable ….. 120,000

Bonds Payable …………………….. 4,000,000

(b) Jan. 1 Cash ($4,000,000 X 95%) ……………… 3,800,000

Discount on Bonds Payable ………… 200,000

Bonds Payable …………………….. 4,000,000

(c) Premium

Current Liabilities

Interest payable ………………………………… $ 320,000

Discount

Current Liabilities

Interest payable ………………………………… $ 320,000

*PROBLEM 15-8C

2017

(a) Jan. 1 Interest Payable ………………………….. 225,000

Cash ……………………………………. 225,000**

2018

(c) Jan 1 Bonds Payable ……………………………. 800,000

(d) Dec. 31 Interest Expense …………………………. 159,120

Discount on Bonds Payable ….. 6,120**

Interest Payable……………………. 153,000**

*PROBLEM 15-9C

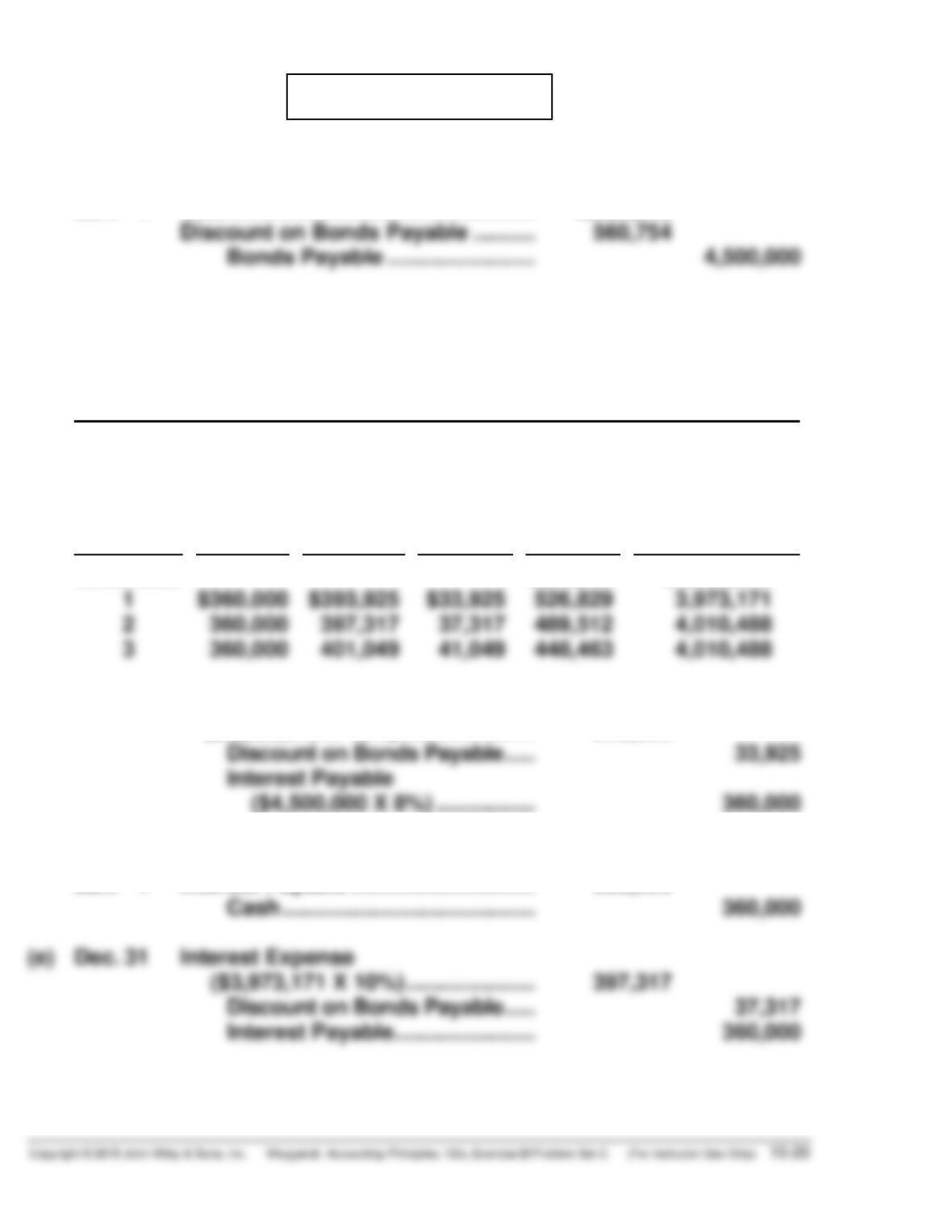

(a) 2016

Jan. 1 Cash …………………………………………. 3,939,246

(b) EUROPA SATELLITES

Bond Discount Amortization

Effective-Interest Method—Annual Interest Payments

8% Bonds Issued at 10%

Annual

Interest

Periods

(A)

Interest

to Be

Paid

(B)

Interest

Expense

to Be

Recorded

(C)

Discount

Amor-

tization

(B) – (A)

(D)

Unamor-

tized

Discount

(D) – (C)

(E)

Bond

Carrying

Value

($4,500,000 – D)

Issue date

1

$360,000

$393,925

$33,925

$560,754

526,829

$3,939,246

3,973,171

(c) Dec. 31 Interest Expense

($3,939,246 X 10%) …………………. 393,925

Discount on Bonds Payable ….. 33,925

(d) 2017

Jan. 1 Interest Payable ………………………… 360,000

Cash ………………………………….. 360,000

(e) Dec. 31 Interest Expense

*PROBLEM 15-10C

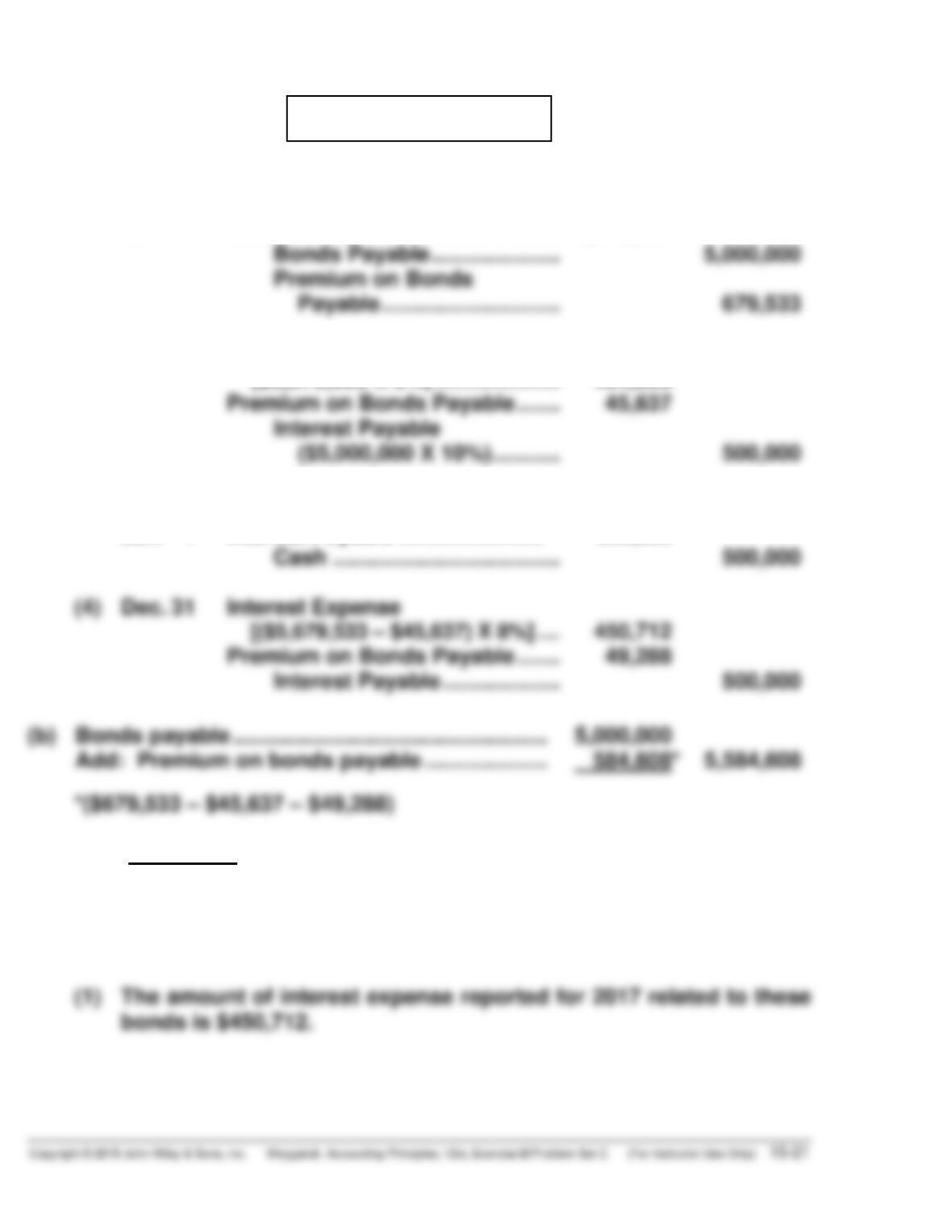

(a) (1) 2016

Jan. 1 Cash ……………………………………… 5,679,533

(2) Dec. 31 Interest Expense

($5,679,533 X 8%) ……………….. 454,363

($5,000,000 X 10%) ……….. 500,000

(3) 2017

Jan. 1 Interest Payable ……………………. 500,000

Cash ………………………………. 500,000

(4) Dec. 31 Interest Expense

(b) Bonds payable …………………………………………… 5,000,000

(c) Dear :

Thank you for asking me to clarify some points about the bonds issued

by Georgia Chemical Company.

*PROBLEM 15–10C (Continued)

(2) When the bonds are sold at a premium, the effective-interest method

will result in more interest expense reported than the straight-line

method in 2017. Straight-line interest expense for 2017 is $432,047

($500,000 – $67,953).