Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15-1

CHAPTER 15

Target Costing and Cost Analysis for Pricing

Decisions

ANSWERS TO REVIEW QUESTIONS

15-1 In the long run, every organization must price its product or service above the total

15-2 The statement that prices are determined by production costs is too simplistic.

15-3 Four major influences on pricing decisions are as follows:

(1) Customer demand: Management must consider customers’ demand for their

15-4 It is crucial to define the firm’s product when considering the reaction of

competitors, so that the competitors can be identified. For example, is a firm that

15-2

15-5 In most industries, both market forces and cost considerations heavily influence

prices. No organization can price its products below their production costs in the

15-6 The profit-maximizing price is the price for which the associated quantity is

15-7 (a) Total revenue: Price multiplied by quantity sold.

15-9 Three limitations of the economic, profit-maximizing model of pricing are as follows:

15–10 Determining the best approach to pricing requires a cost-benefit trade-off. While the

Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15-3

15–11 The general formula for cost-plus pricing is as follows:

15–12 The four cost bases commonly used in cost-plus pricing are the following:

absorption manufacturing cost, total cost, variable manufacturing cost, and total

15–13 Four reasons often cited for the widespread use of absorption cost as the cost base

in cost-plus pricing formulas are as follows:

(1) In the long run, the price must cover all costs and a normal profit margin.

15–14 The primary disadvantage of absorption-cost or total-cost pricing formulas is that

15–15 Three advantages of pricing based on variable cost are as follows:

(2) Variable-cost data do not require allocation of common fixed costs to individual

product lines.

15-4

fixed costs.

15–17 Return-on-investment pricing is an approach under which the price is set so that it

15–18 Price-led costing refers to the process under target costing of first determining the

15–19 To be successful at target costing, management must listen to the company’s

15–20 Value-engineering is a cost-reduction and process-improvement technique used to

15–21 Tear-down methods can be used in a service-industry firm just as they are used in

15–22 Under time-and-material pricing, the price includes a cost-based charge for labor, a

15–23 When a firm has excess capacity, there is no opportunity cost in accepting an

additional production job. Therefore, it is not necessary to reflect such an

15-5

15–24 The decision to accept or reject a special order and the selection of a price for a

special order are similar decisions. If a price has been offered for a special order,

15–25 (a) Skimming pricing: Setting a high initial price for a new product in order to reap

(c) Target costing: Conducting market research to determine the price at which a

15–26 (a) Unlawful price discrimination: Quoting different prices to different customers for

15–27 Traditional, volume-based product-costing systems often overcost high-volume and

relatively simple products while undercosting low-volume and complex products.

Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15-6

SOLUTIONS TO EXERCISES

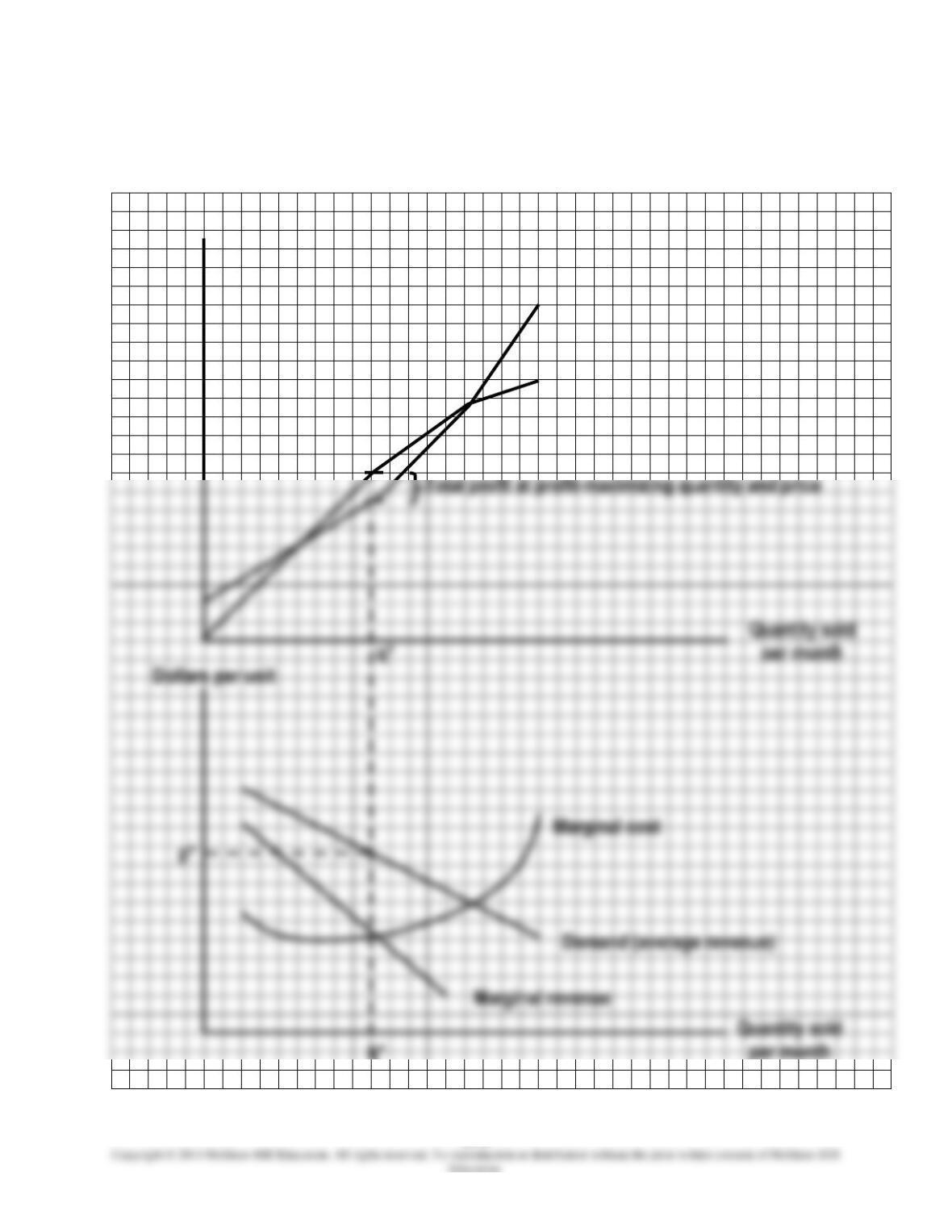

EXERCISE 15-28 (25 MINUTES)

q*

Dollars

Total cost

Total revenue

Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15-7

EXERCISE 15-29 (30 MINUTES)

1. Tabulated price, quantity, and revenue data:

(1)

Quantity

Sold per

Month

(2)

Unit

Sales

Price

(3)

Total

Revenue

per

Month*

(4)

Changes

in Total

Revenue†

20

…………………………..

$500

…………………………..

$10,000

40

…………………………..

…………………………..

60

…………………………..

…………………………..

80

…………………………..

…………………………..

15-8

EXERCISE 15-29 (CONTINUED)

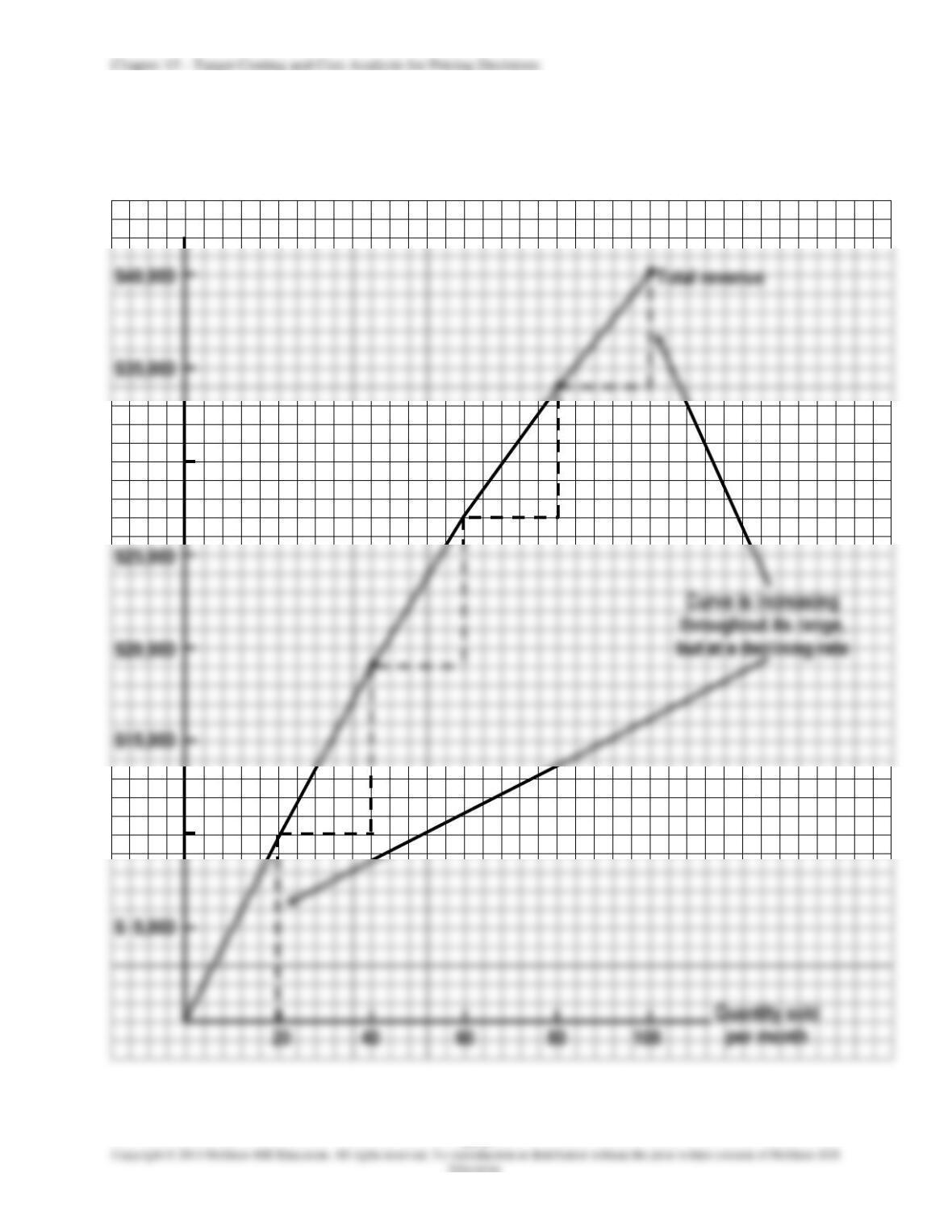

2. Total revenue curve:

$ 5,000

$25,000

$20,000

$15,000

Dollars

$40,000

$35,000

•

•

$30,000

$10,000

•

•

15-9

EXERCISE 15-30 (30 MINUTES)

1. Tabulated cost and quantity data:

(1)

Quantity

Produced

and Sold per

Month

(2)

Average

Cost per

Unit

(3)

Total

Cost per

Month*

(4)

Changes

in Total

Cost†

20

…………………………..

$450

…………………………..

$ 9,000

40

…………………………..

…………………………..

60

…………………………..

…………………………..

80

…………………………..

…………………………..

Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15–10

EXERCISE 15-30 (CONTINUED)

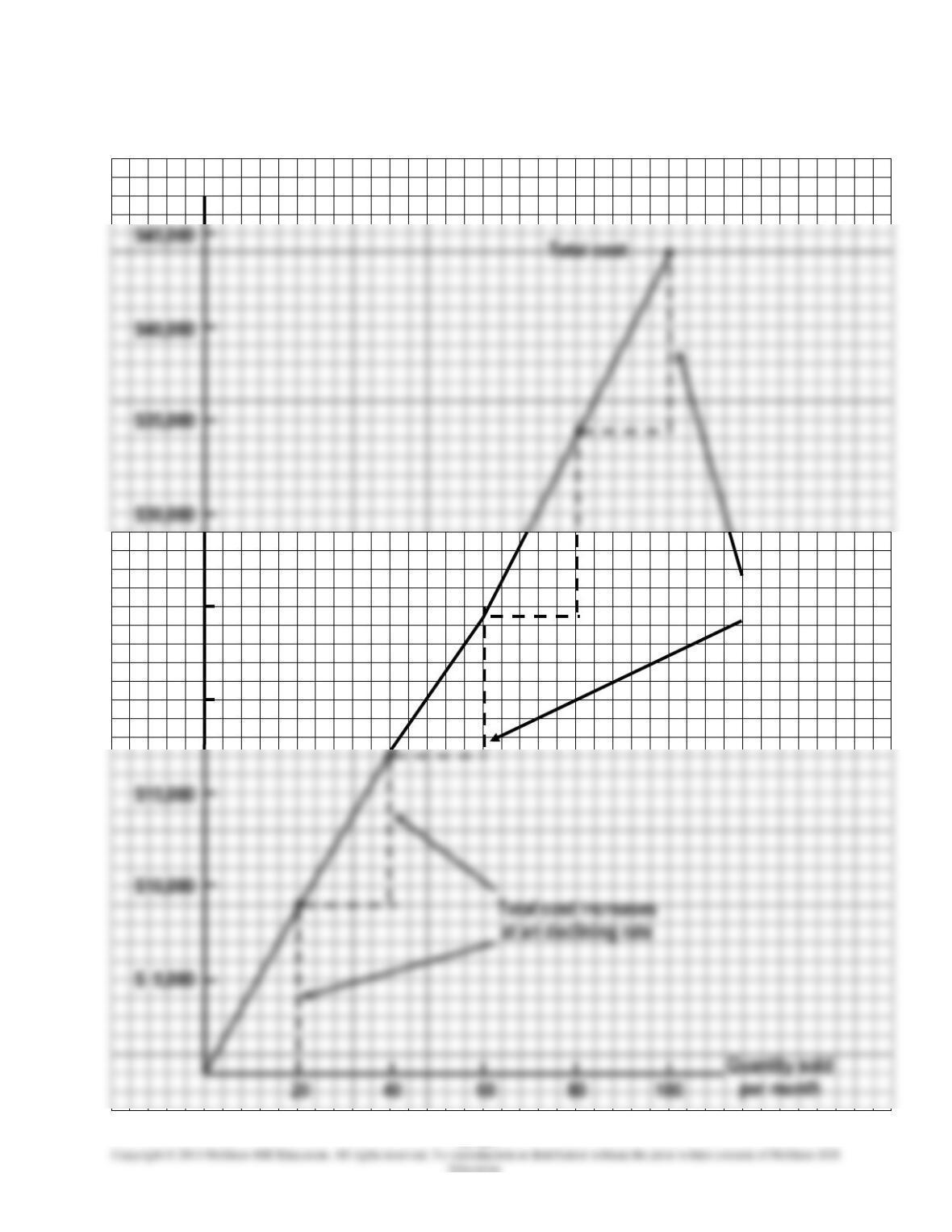

2. Total cost curve:

$15,000

$10,000

$ 5,000

Total cost increases

at an increasing rate

Dollars

$45,000

$40,000

$30,000

$25,000

$20,000

•

Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15–11

EXERCISE 15-31 (40 MINUTES)

1. Tabulated revenue, cost, and profit data:

(1)

Quantity

Produced

and Sold

per Month

(2)

Sales

Price

per Unit

(3)

Total

Revenue

per

Month*

(4)

Total

Cost

per

Month†

(5)

Profit

per

Month**

20

…………………………..

$500

…………………………..

$10,000

$ 9,000

…………………………..

$1,000

40

…………………………..

…………………………..

19,000

17,000

…………………………..

60

…………………………..

…………………………..

27,000

24,600

…………………………..

80

…………………………..

…………………………..

34,000

34,400

…………………………..

Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15–12

EXERCISE 15-31 (CONTINUED)

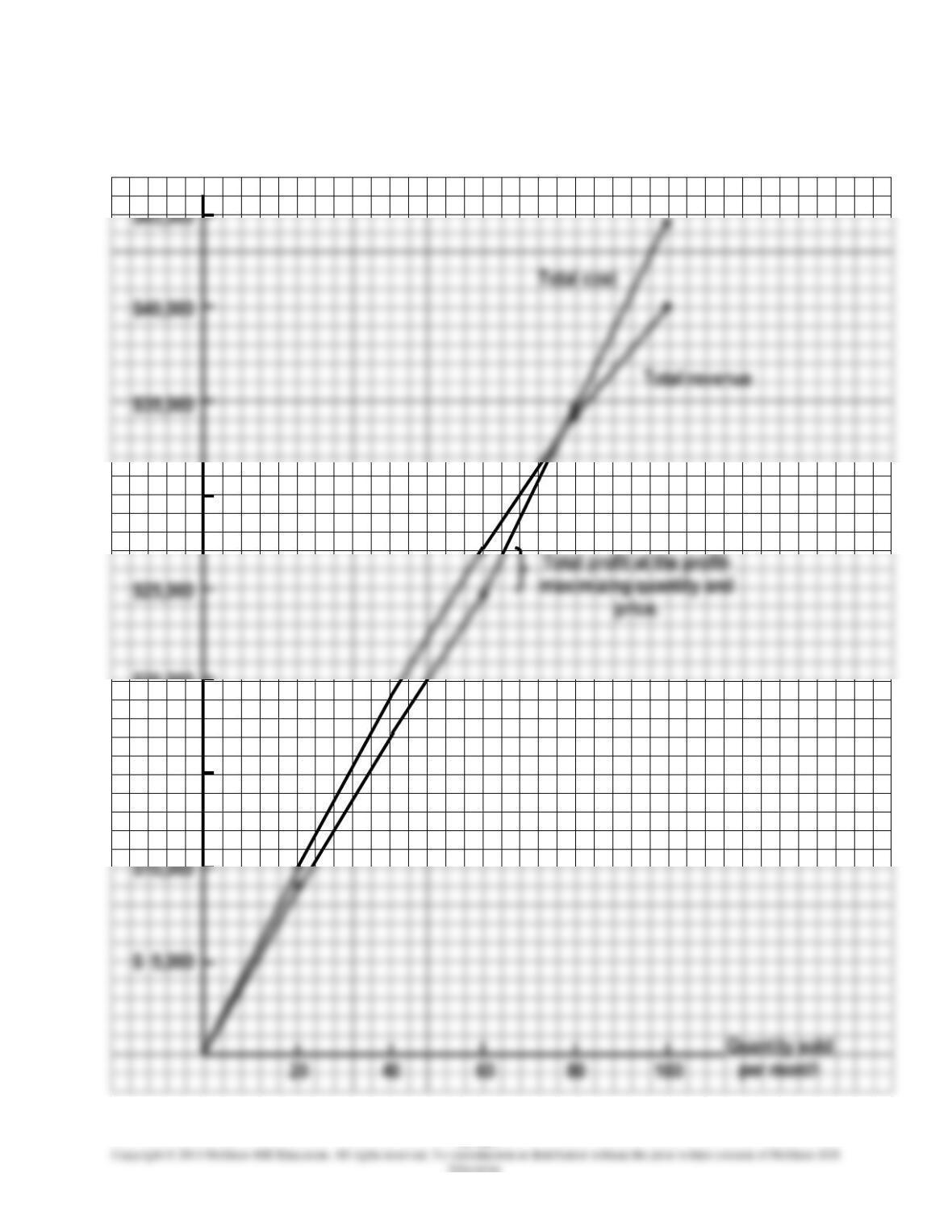

2. Total revenue and cost curves:

$40,000

•

•

$10,000

•

$25,000

Dollars

$30,000

$20,000

$15,000

•

•

Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15–13

EXERCISE 15-32 (30 MINUTES)

1. Price = total unit cost + (markup percentage total unit cost)

Allocated fixed

selling and

administrative cost

=

total

unit

cost

–

all

manufacturing

costs

–

variable

selling and

administrative cost

Cost-Plus Pricing Formula

2.

a.

Variable manufacturing cost …………………………..

$275

$495 = $275 + (80% $275)*

Applied fixed manufacturing cost …………………………..

Variable manufacturing cost …………………………..

**($495 – $341) ÷ $341 = 45.16% (rounded)

15–14

EXERCISE 15-33 (15 MINUTES)

1.

Profit on sales of 60,000 units:

Sales revenue (60,000 9.00p) ……………………………………….

540,000p

Less: Variable costs:

Contribution margin ………………………………………………………

Less: Fixed costs (90,000p + 7,500p) ………………………………

Profit …………………………………………………………………………….

2. Required price on special order:

Unit contribution margin

required on special order

=

order special in volumesalesunit

profit additional target

=

Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15–15

EXERCISE 15-34 (25 MINUTES)

Cost-Plus Pricing Formula

$600 = $300 + (100% $300)a

Applied fixed manufacturing cost …………………………..

(2)

Absorption manufacturing cost …………………………..

$405

$600 = $405 + (48.15% $405)b

Variable selling and administrative cost …………………………

(3)

Total cost

$525

Variable manufacturing cost …………………………..

Variable selling and administrative cost …………………………

Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15–16

EXERCISE 15-35 (30 MINUTES)

Markup percentage

applied to cost base in

cost-plus

pricing formula

=

profit required to

achieve target ROI

+

total annual costs not

included in cost base

annual

volume

cost base per unit

used in cost-plus

pricing formula

15–17

EXERCISE 15-35 (CONTINUED)

In the preceding formula:

$60,000

=

target profit (given)

480

=

annual volume of Wave Darter production and sales (from Exhibit 15-5)

=

variable manufacturing cost per unit (from Exhibit 15–5)

$50

=

variable selling and administrative cost per unit (from Exhibit 15-5)

=

applied fixed manufacturing cost per unit (from Exhibit 15-5)

=

allocated fixed selling and administrative cost per unit (from Exhibit 15-5)

2.

Markup percentage

=

*$650 480

costs tiveadministra

andselling total

$60,000

+

=

42.31% (rounded)

Thus the Wave Darter’s price would be set equal to $925, where

Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15–18

EXERCISE 15-36 (15 MINUTES)

1. Material component of time and material pricing formula:

handling material

material

material

2. Material component of price, using formula developed in requirement (1):

New price to be quoted on yacht refurbishment:

Total price of job = time charges + material charges

EXERCISE 15-37 (30 MINUTES)

Answers will vary widely, depending on the company and the product chosen. The answer

Chapter 15 – Target Costing and Cost Analysis for Pricing Decisions

15–19

SOLUTIONS TO PROBLEMS

PROBLEM 15-38 (45 MINUTES)

1. The order will boost Heartland’s net income by $13,950, as the following calculations

show.

Sales revenue ……………………………………………..

$82,500

Less: Sales commissions (10%) …………………..

8,250

$74,250

Less manufacturing costs:

$14,600

8,400

Income before taxes ……………………………………

Income taxes (40%) ……………………………………..

2. Yes. Although this amount is below the $82,500 full-cost price, the order is still

profitable. Heartland can afford to pick up some additional business, because the

company is operating at 75 percent of practical capacity.

Sales revenue …………………………………………………..

$63,500

Less: Sales commissions (10%) ………………………..

6,350

$57,150

Less manufacturing costs:

$14,600

8,400

Income before taxes …………………………………………

$ 6,150

Income taxes (40%) …………………………………………..

2,460