Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 15 Financial Statement Analysis

Prob. 15–1B

1.

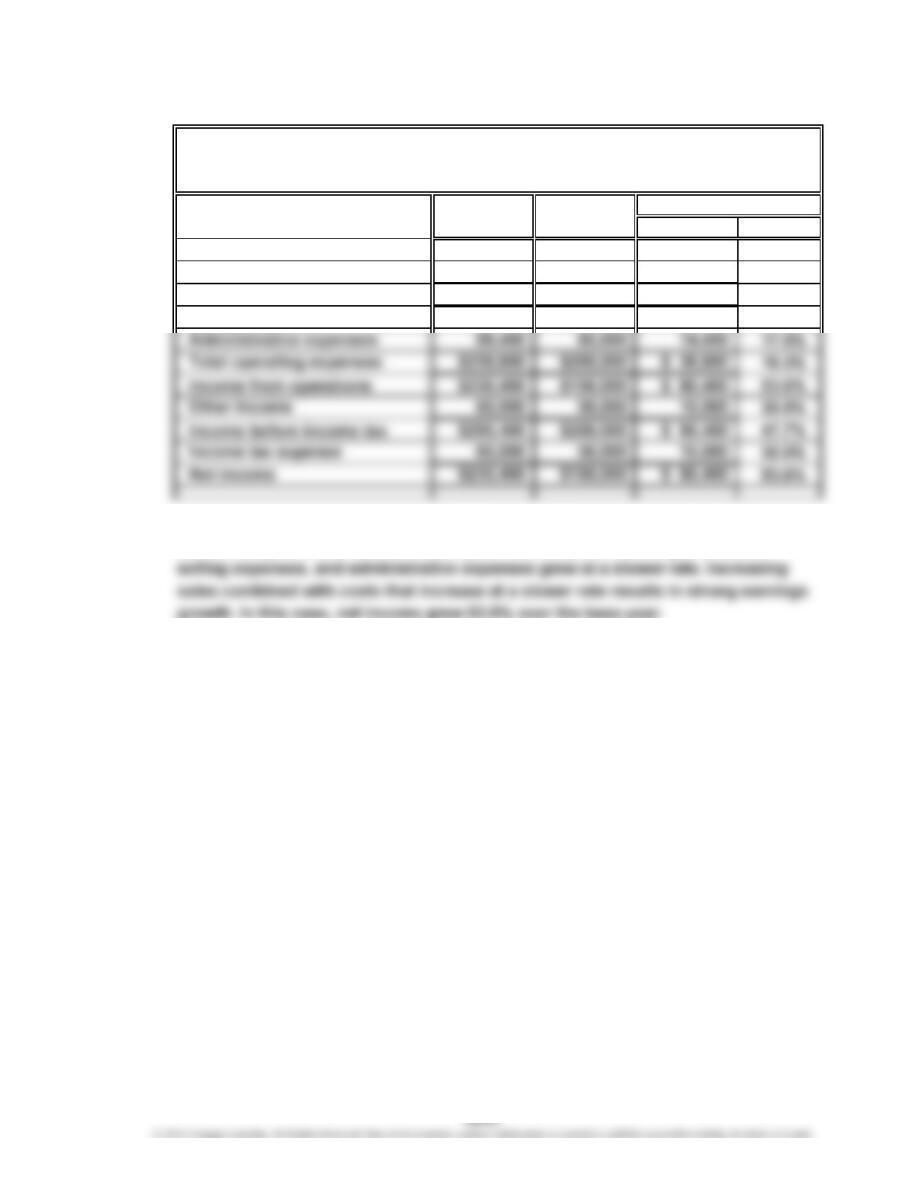

2016 2015 Amount Percent

Sales $910,000 $700,000 $210,000 30.0%

Cost of goods sold 441,000 350,000 91,000 26.0%

Gross profit $469,000 $350,000 $119,000 34.0%

Selling expenses 139,150 115,000 24,150 21.0%

2. The profitability has significantly improved from 2015 to 2016. Sales have

increased by 30% over the 2015 base year. However, the cost of goods sold,

Increase (Decrease)

MACKLIN INC.

Comparative Income Statement

For the Years Ended December 31, 2016 and 2015

CHAPTER 15 Financial Statement Analysis

Prob. 15–2B

1.

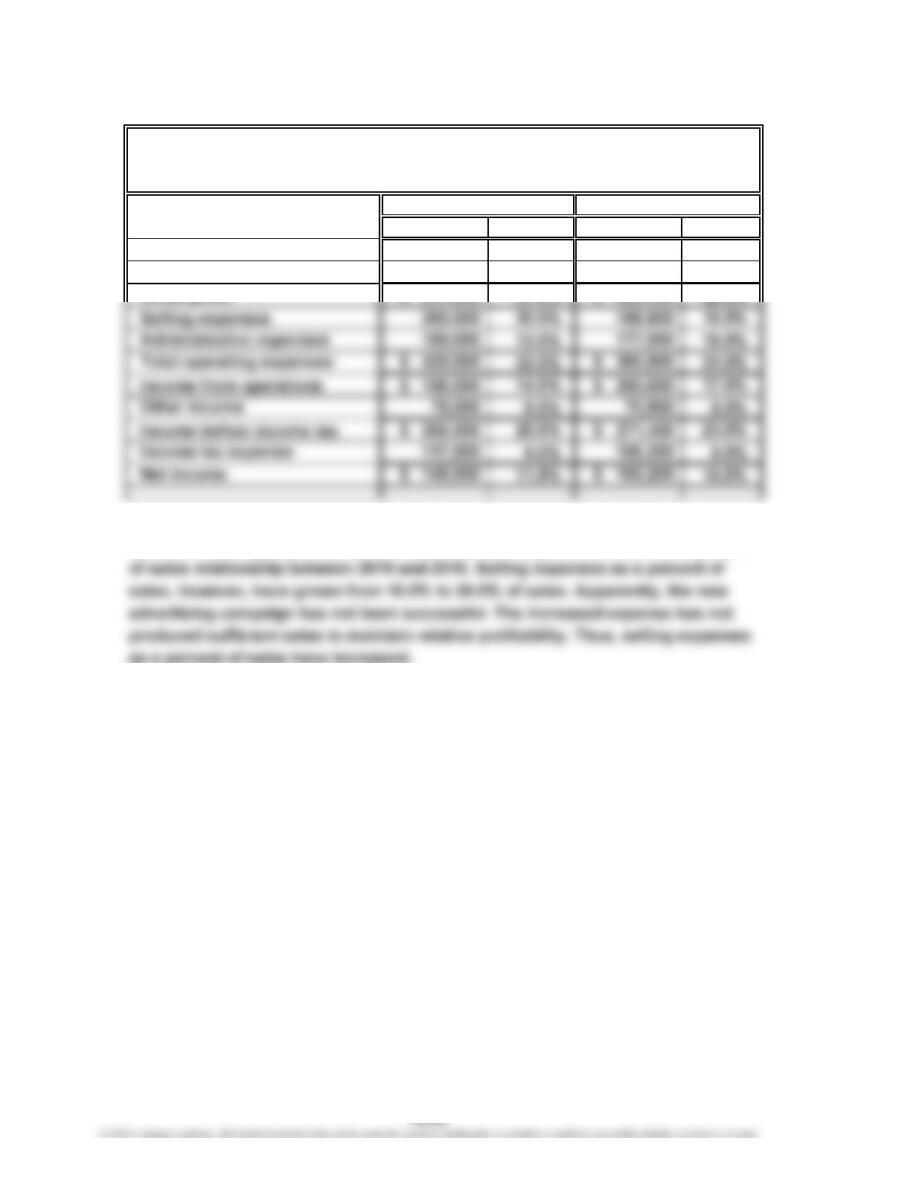

Amount Percent Amount Percent

Sales $1,300,000 100.0% $1,180,000 100.0%

Cost of goods sold 682,500 52.5% 613,600 52.0%

Gross profit $ 617,500 47.5% $ 566,400 48.0%

2. The net income as a percent of sales has declined. All the costs and expenses,

other than selling expenses, have maintained their approximate cost as a percent

2016 2015

FIELDER INDUSTRIES INC.

Comparative Income Statement

For the Years Ended December 31, 2016 and 2015

CHAPTER 15 Financial Statement Analysis

Prob. 15–3B

1. a. Working Capital = Current Assets – Current Liabilities

$3,200,000 – $2,000,000 = $1,200,000

$2,000,000

2.

Working Quick Current

Capital Assets Liabilities

1,200,000 1,912,500 1,712,500

1,200,000 2,075,000 1,875,000

1,200,000 2,200,000 2,000,000

1,200,000 2,200,000 2,000,000

1,200,000 2,000,000 2,000,000

= 1.6

AssetsTransaction

Current

Ratio

Quick

Ratio

Current

b. 1.7 1.1 2,912,500

d. 1.6 1.1 3,075,000

f. 1.6 1.1 3,200,000

h. 1.6 1.1 3,200,000

Supporting Data

j. 1.6 1.0 3,200,000

CHAPTER 15 Financial Statement Analysis

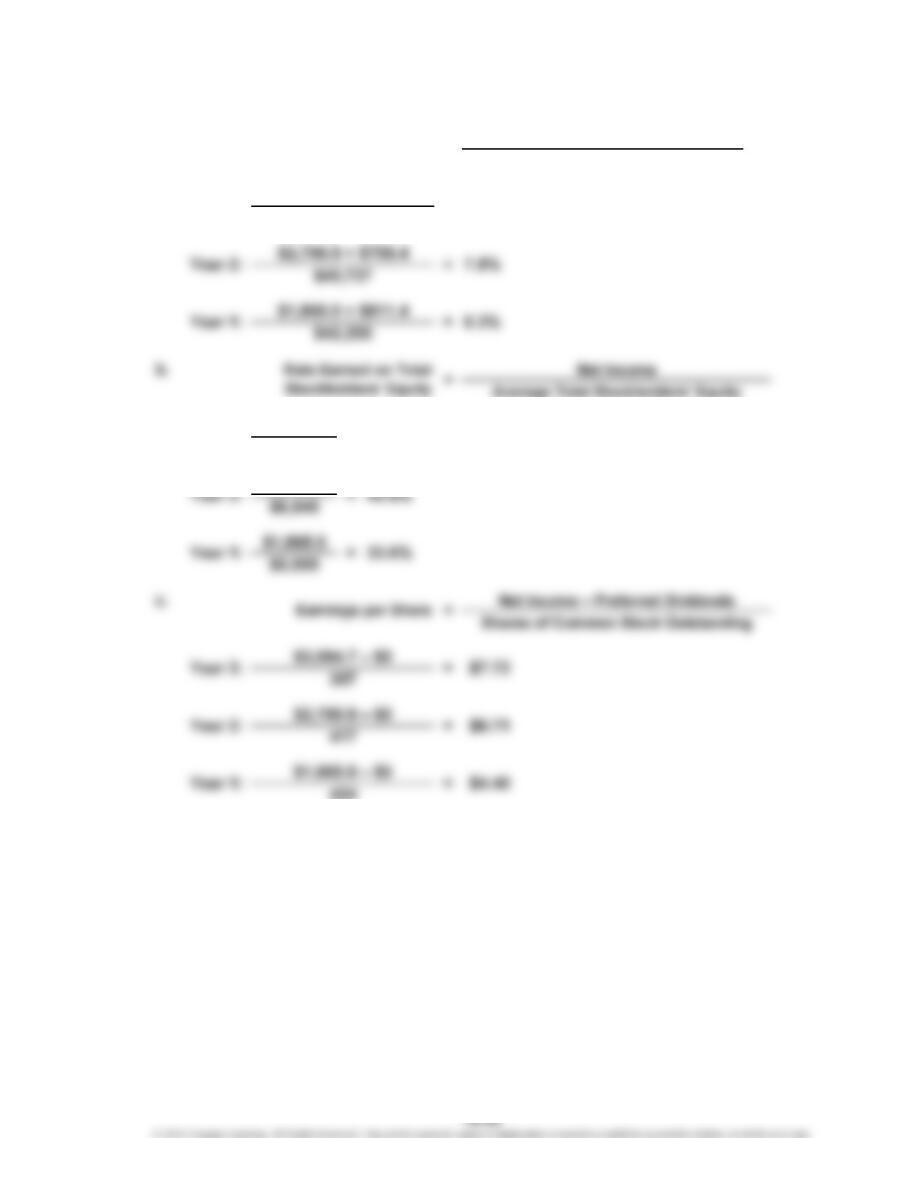

Prob. 15–4B

1. Working Capital: $3,690,000 – $900,000 = $2,790,000

Calculated

Numerator Denominator Value

3. Quick ratio $2,250,000 $900,000 2.5

4. Accounts receivable turnover $10,000,000 ($740,000 + $510,000) ÷ 2 16.0

7. Number of days' sales in

inventory

9. Ratio of liabilities to

stockholders’ equity

11. Number of times preferred

14. Rate earned on

stockholders’ equity

16. Earnings per share on

common stock

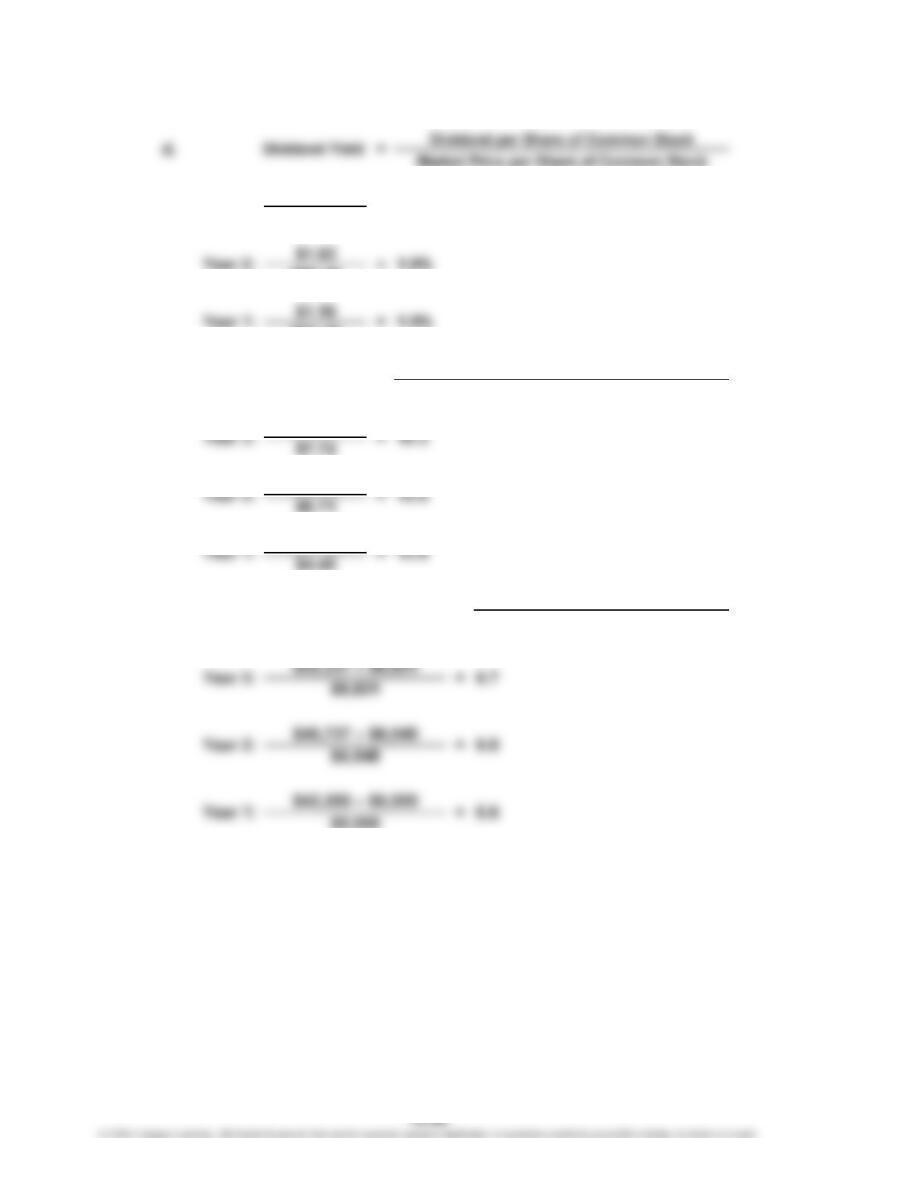

17. Price-earnings ratio 119.70 8.55 14.0

19. Dividend yield $0.50 $119.70 0.4%

Ratio

($1,190,000 + $950,000) ÷ 2 $5,350,000 ÷ 365

73.0

$7,180,000

$900,000

0.4

$2,600,000

$8.55$900,000 – $45,000 100,000

13.3%

($7,180,000 + $6,375,000) ÷ 2

CHAPTER 15 Financial Statement Analysis

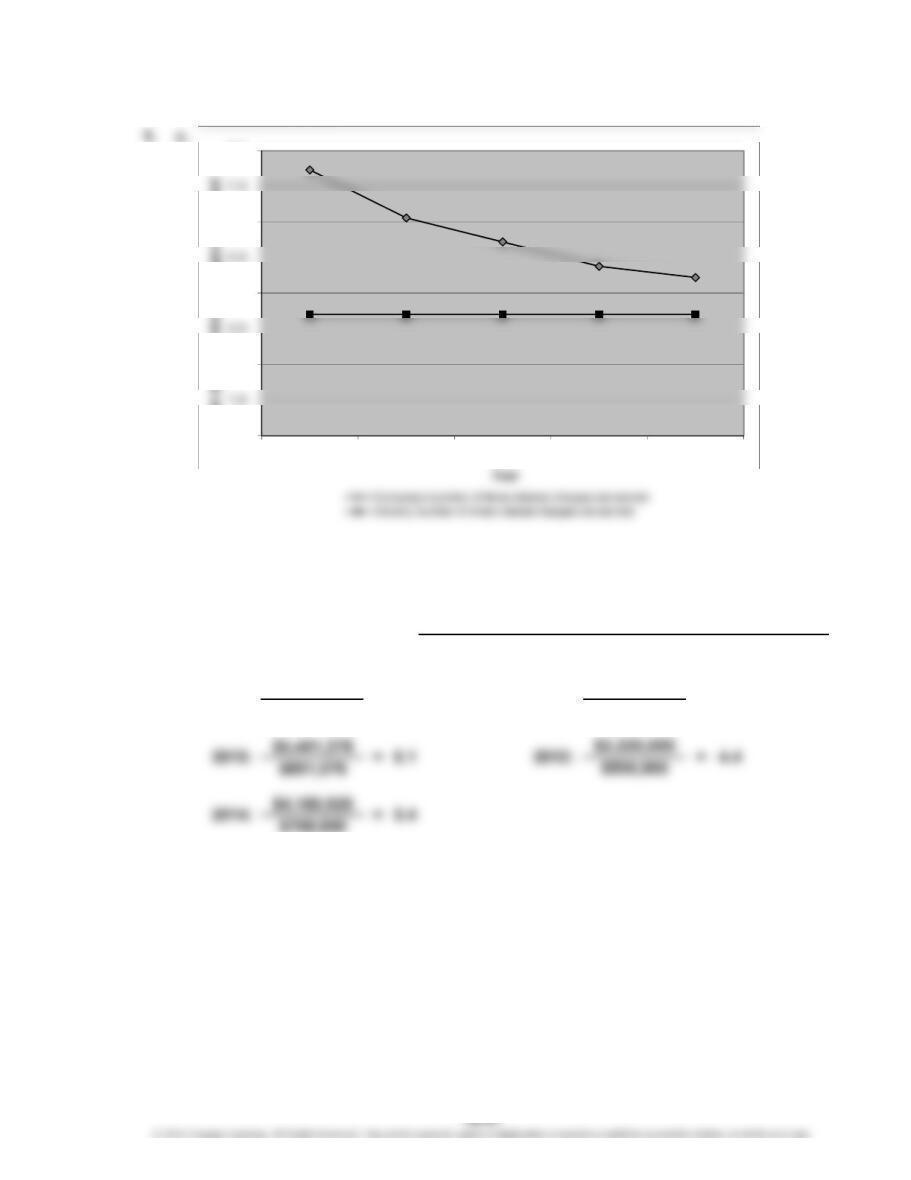

Prob. 15–5B

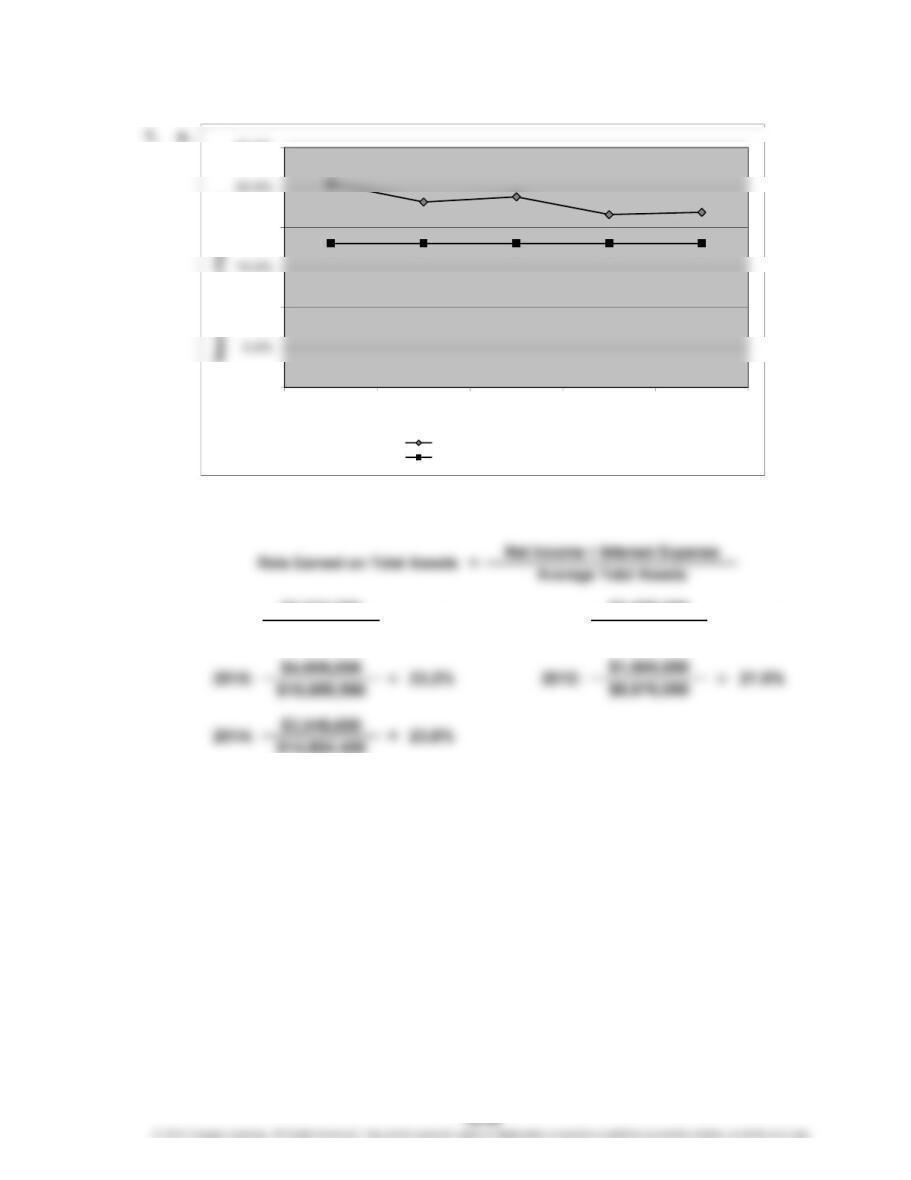

$6,623,780

$25,988,665

2013: $2,458,000

21.6%

25.5%2016: =

=

$11,370,240

0.0%

10.0%

20.0%

30.0%

2016 2015 2014 2013 2012

Year

Company’s rate earned on total assets

Industry rate earned on total assets

CHAPTER 15 Financial Statement Analysis

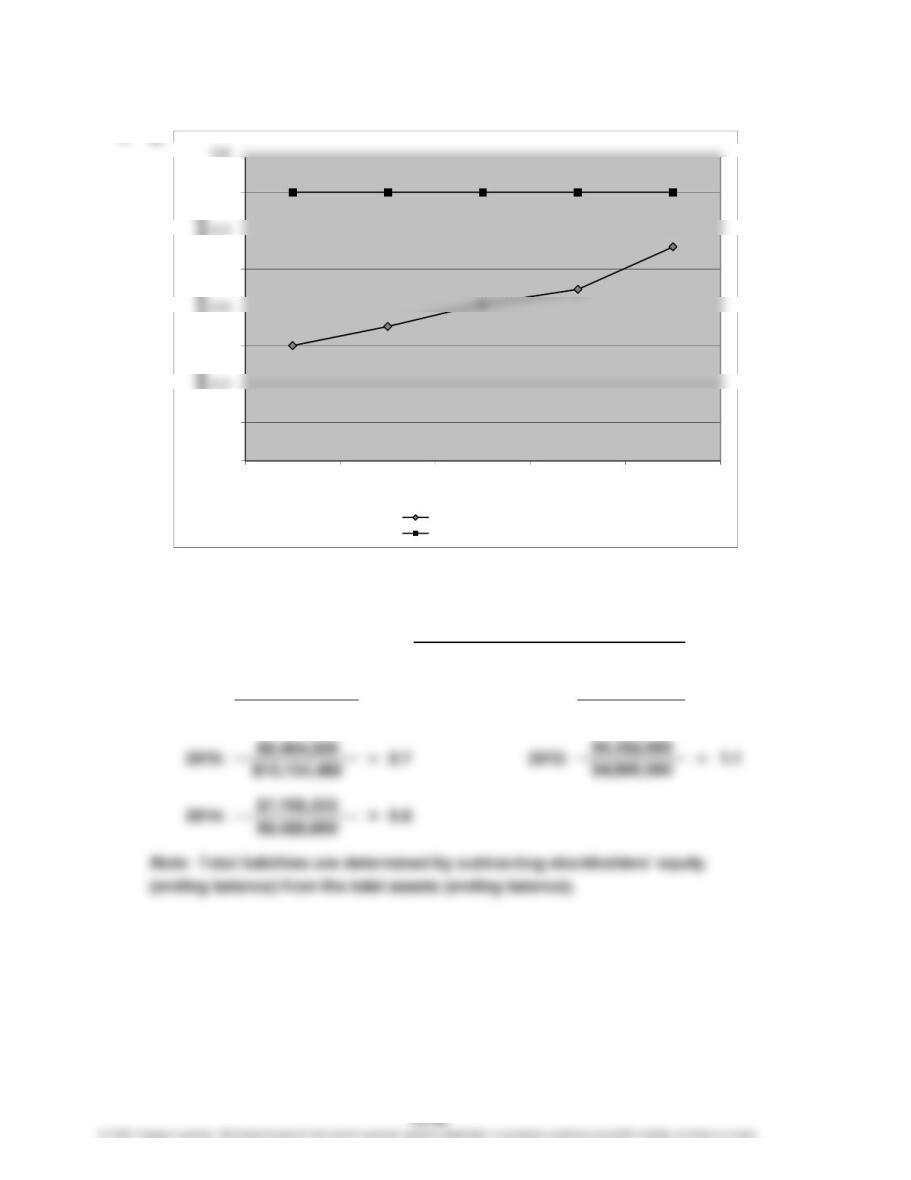

Prob. 15–5B (Continued)

1. b.

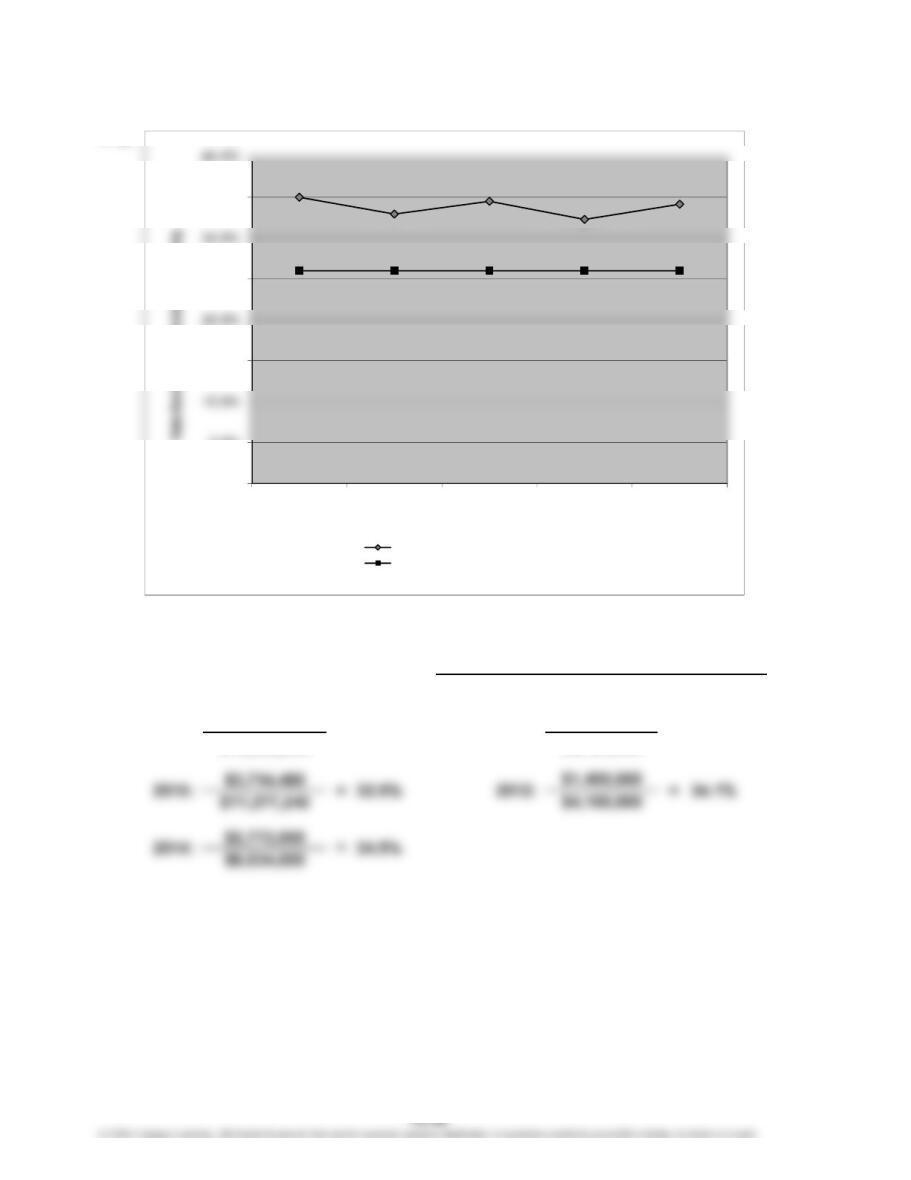

$5,571,720

$15,920,340

Rate Earned on

Stockholders’ Equity

35.0%

=Average Total Stockholders’ Equity

Net Income

2013: $1,848,000

$5,724,000

2016:

=

32.3%=

0.0%

5.0%

15.0%

25.0%

35.0%

2016 2015 2014 2013 2012

Year

Company’s rate earned on stockholders’ equity

Industry rate earned on stockholders’ equity

CHAPTER 15 Financial Statement Analysis

Prob. 15–5B (Continued)

$7,849,352

$1,052,060

7.5

=

Number of Times

Interest Charges Are Earned

Net Income + Income Tax Expense + Interest Expense

Interest Expense

=2013:2016:

=

4.8

$2,899,600

$610,000

0.0

2.0

4.0

6.0

8.0

2016 2015 2014 2013 2012

Number of Times Interest Charges Are Earned

CHAPTER 15 Financial Statement Analysis

Prob. 15–5B (Continued)

1. d.

$10,672,291

$18,706,200

0.62016:

Ratio of Liabilities to

Stockholders’ Equity =

=

0.9

Total Liabilities

Total Stockholders’ Equity

$5,940,480

$6,648,000

=

2013:

0.0

0.2

0.6

1.0

1.4

2016 2015 2014 2013 2012

Ratio of Liabilities to Stockholders’ Equity

Year

Company’s liabilities to equity

Industry liabilities to equity

CHAPTER 15 Financial Statement Analysis

Prob. 15–5B (Concluded)

2. Both the rate earned on total assets and the rate earned on stockholders’ equity

are above the industry average for all five years. The rate earned on total assets is

actually improving gradually. The rate earned on stockholders’ equity exceeds the

CHAPTER 15 Financial Statement Analysis

Fiscal Fiscal

2012 2011

Total current liabilities…………………………………

…

3,926.0 3,882.0

Working capital………………………………………

…

$ 9,700.0 $ 7,963.0

b. Total current assets……………………………………

…

$13,626.0 $11,845.0

c. Cash………………………………………………………… $ 3,337.0 $ 2,317.0

Short-term investments…………………………………

…

2,628.0 1,440.0

÷ Total current liabilities……………………………

…

3,926.0 3,882.0

…

End of year……………………………………………

…

3,117.0 3,132.0

Total………………………………………………………… $ 6,249.0 $ 6,270.0

Average (Total ÷ 2)………………………………………

…

3,124.5 3,135.0

…

Average daily sales (Sales ÷ 365)…………………

…

69.4 63.9

…

End of year……………………………………………

…

3,434.0 3,222.0

Total……………………………………………………

…

$ 6,656.0 $ 5,937.0

…

NIKE, INC., PROBLEM

CHAPTER 15 Financial Statement Analysis

Fiscal Fiscal

2012 2011

g. Inventory (average)………………………………………

…

$ 3,328.0 $ 2,968.5

Cost of goods sold………………………………………

…

14,279.0 13,183.0

Average daily cost of goods sold………………………

…

39.1 36.1

Number of days’ sales in inventory (Average

inventory ÷ Average daily cost of goods sold)……

…

85.1 82.2

Plus interest expense*……………………………………

…

23.0 31.0

Total……………………………………………………… $ 2,508.0 $ 2,254.0

Total assets:

Beginning of year……………………………………… $15,465.0 $14,998.0

End of year……………………………………………… 17,584.0 15,465.0

Total……………………………………………………… $33,049.0 $30,463.0

Average total assets………………………………………

…

16,524.5 15,231.5

Rate earned on total assets

[(Net income + Interest expense) ÷

Average total assets]…………………………………

…

15.2% 14.8%

*See Nike Note 6.

NIKE, INC., PROBLEM (Continued)

CHAPTER 15 Financial Statement Analysis

…

2. Before reaching definitive conclusions, each measure should be compared with

past years, industry averages, and similar firms in the industry.

45.0. Thus, it takes the company less than two months to collect its

accounts receivable from credit sales. These numbers should be

compared to their competitors, industry averages, and Nike’s credit

policy to draw definitive conclusions.

f. and g. The results of these two analyses show a very slight decrease in

inventory turnover and an increase in the number of days’ sales in

inventory. Both trends are small. Inventory management is critical to

Nike, so this indicates a favorable trend.

h. The margin of protection to creditors remained decreased slightly. Overall, Nik

e

provides sound protection to its creditors.

i. These analyses indicate that the effectiveness in the use of assets to generate

revenues was very similar in both years.

NIKE, INC., PROBLEM (Concluded)

CHAPTER 15 Financial Statement Analysis

CP 15–1

This position does not allow the shareholders to take advantage of leverage. As a

result, the return on shareholders’ equity cannot be improved by using debt. In

CP 15–2

Josh is concerned about the inventory and accounts receivable levels because he must

determine their value. Inventory that cannot be sold (or sold at a large discount) or

accounts receivable that cannot be collected must be written down to reflect their

CASES & PROJECTS

CHAPTER 15 Financial Statement Analysis

CP 15–3

Dell Inc. Apple Inc.

Sales 100.0% 100.0%

Cost of sales 78.6% 56.1%

Gross profit 21.4% 43.9%

The common-sized analysis indicates that Dell and Apple are very different computer

companies. Dell’s income from operations was 5.3% of sales, while Apple’s was 35.3% o

f

sales. There is a 30 percentage point difference between the two companies. What

explains this difference? The gross profit for Dell was 21.4% of sales, which is fairly

are 14.2% of sales. Apple has larger research expenses as a percent of sales. It attempts

to sell a unique array of products to a wide audience. This requires significant research

and development. Dell’s R&D was 1.9% of sales, while Apple’s was 2.2% of

DELL INC. AND APPLE INC.

Common-Sized Statements

CHAPTER 15 Financial Statement Analysis

CP 15–4

$3,064.7

$6,821

$2,799.9

44.9%

Year 3: =

Year 3: $3,064.7 + $782.8

$52,237

a.

= 7.4%

Rate Earned on Total Assets = Net Income + Interest Expense

Average Total Assets

CHAPTER 15 Financial Statement Analysis

CP 15–4 (Continued)

$1.79

$79.27

$80.48

$61.18

$79.27

$80.48

$61.18

2.

Market Price per Share of Common Stock

2.3%

Year 3: =

e.

=Price-Earnings Ratio

=

Average Liabilities

Average Stockholders’ Equity

Ratio of Average Liabilities to Average

Stockholders’ Equity

Earnings per Share

CHAPTER 15 Financial Statement Analysis

CP 15–4 (Concluded)

3. Deere & Co.’s profitability, as measured by earnings per share, has improved

significantly during the three-year period presented. The rates earned on total

assets and total stockholders’ equity have also improved significantly during this

CHAPTER 15 Financial Statement Analysis

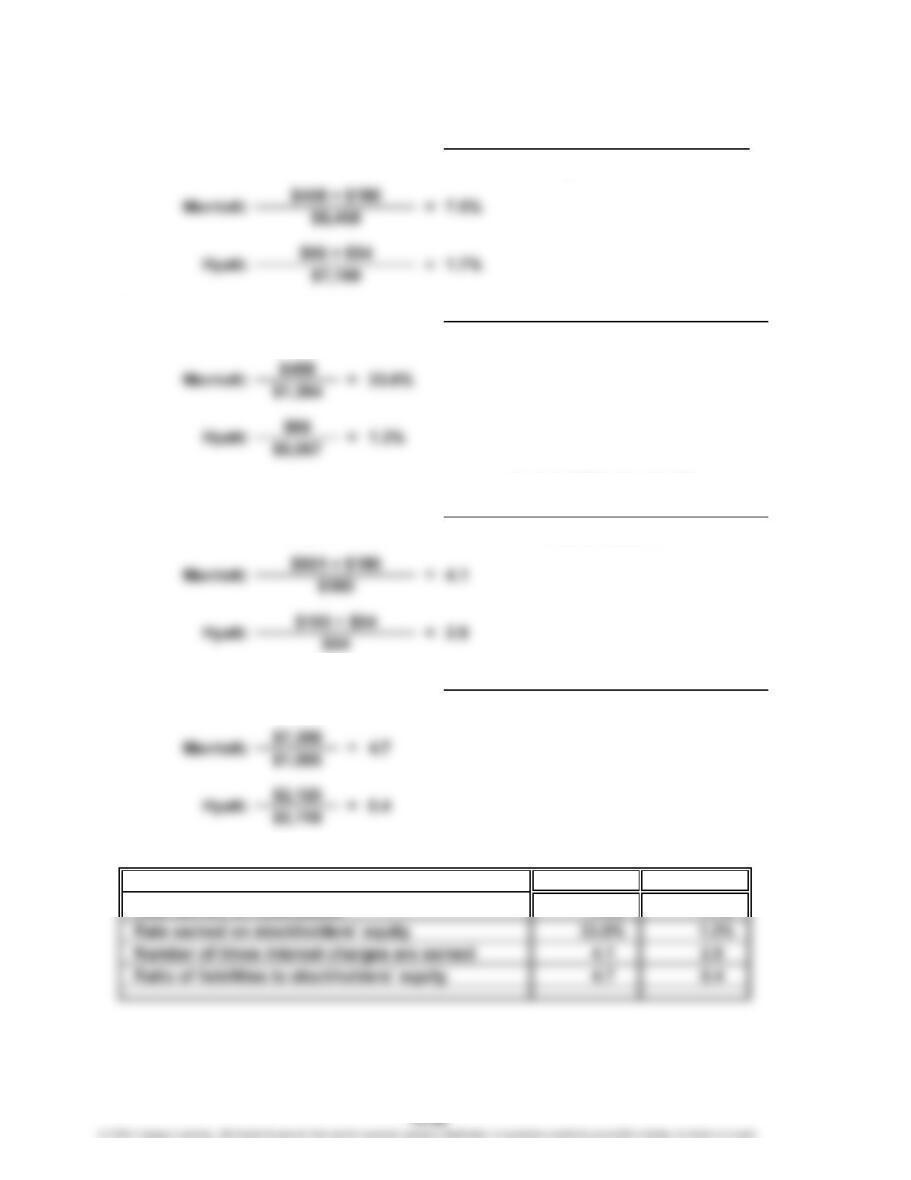

CP 15–5

b.

c.

d.

Summary Table:

Marriott Hyatt

Rate earned on total assets 7.5% 1.7%

=Total Liabilities

Total Stockholders’ Equity

=

Income Before Income Tax

+ Interest Expense

1.

Ratio of Liabilities to

Stockholders’ Equity

a.

Number of Times Interest

Charges Are Earned

Interest Expense

Rate Earned on Total Assets

Rate Earned on

Stockholders’ Equity

=Net Income + Interest Expense

Average Total Assets

=Net Income

Average Total Stockholders’ Equity

CHAPTER 15 Financial Statement Analysis

CP 15–5 (Concluded)

2. Marriott has a higher rate earned on total assets (7.5% vs. 1.7%), and a higher

rate on stockholders’ equity (33.6% vs. 1.3%), compared to Hyatt. Hyatt’s weaker

performance relative to Marriott appears to be due to its weak earnings relative