1. A company may temporarily have excess cash that is not needed for use in its current

operations. Instead of letting excess cash remain idle, most companies invest their excess

cash in temporary investments. The primary objective of investing in temporary investments

is as follows:

a. Earn interest revenue

b. Receive dividends

c. Realize gains from increases in the market price of the securities

4. An investment greater than 50% of the investee is considered to be an investment that has

control over the investee (subsidiary). Thus, the financial statements of the investee (subsidiary)

are consolidated (combined) with that of the investor (parent company).

5. A gain or loss can occur when the selling price of the bond differs from the book value of the bond.

The price of bond investments can change due to changes in the market rate of interest. If the

p

roceeds from the sale exceed the book value of the bonds, a gain is recorded.

6. Both portfolios are reported at fair value. However, changes in the fair value of trading securities

during a period are reported as an unrealized gain or loss on the income statement. For available-for-

sale securities, changes in the fair value of the securities are reported in stockholders’ equity and,

thus, are not recognized as part of net income.

7. A credit balance in Valuation Allowance for Trading Investments is subtracted from Trading

Investments (at cost). The net amount is the trading investments at fair value.

p

CHAPTER 15

INVESTMENTS

DISCUSSION QUESTIONS

CHAPTER 15 Investments

PE 15-1A

23 Investments—Aurora Company Stock 375,150

Cash 375,150

* (15,000 shares × $25 per share) + $150

10 Cash 185,900

Gain on Sale of Investments 35,840

Investments—Aurora Company Stock 150,060

* (6,000 shares × $31) – $100

** 6,000 shares × ($375,150 ÷ 15,000 shares)

PE 15-1B

12 Investments—Denver Company Stock 120,300

Cash 120,300

* (3,000 shares × $40 per share) + $300

* $0.80 per share × 3,000 shares

10 Cash 57,450

Loss on Sale of Investments 6,710

Investments—Denver Company Stock 64,160

* (1,600 shares × $36) – $150

** 1,600 shares × ($120,300 ÷ 3,000 shares)

PRACTICE EXERCISES

Nov.

June

Sept.

Jan.

*

*

**

*

*

**

CHAPTER 15 Investments

PE 15-2A

20Y7

2 Investment in Violet Company Stock 720,000

Cash 720,000

31 Cash 12,000

Investment in Violet Company Stock 12,000

* 30% × $40,000

20Y8

31 Cash 770,000

Gain on Sale of Violet Company Stock 5,000

Investment in Violet Company Stock 765,000

* $720,000 + $57,000 – $12,000

PE 15-2B

20Y4

2 Investment in Aloof Company Stock 340,000

Cash 340,000

31 Investment in Aloof Company Stock 72,000

Income of Aloof Company 72,000

Recorded 40% of Aloof Company income,

40% × $180,000.

Jan.

Jan.

Dec.

Jan.

*

*

PE 15-3A

a. Investments—Vasquez City Bonds 420,000

Interest Receivable 6,300

Cash 426,300

*Sales proceeds ($210,000 × 99%)………………………

…

$207,900

Accrued interest……………………………………………

…

1,050

Total proceeds from sale…………………………………

…

$208,950

d. Cash 210,000

Investments—Vasquez City Bonds 210,000

PE 15-3B

a. Investments—Hotline Inc. Bonds 180,000

Interest Receivable 1,500

Cash 181,500

c. Cash 92,550

Interest Revenue 750

Gain on Sale of Investments 1,800

Investments—Hotline Inc. Bonds 90,000

…

…

…

d. Cash 90,000

Investments—Hotline Inc. Bonds 90,000

*

CHAPTER 15 Investments

PE 15-4A

PE 15-4B

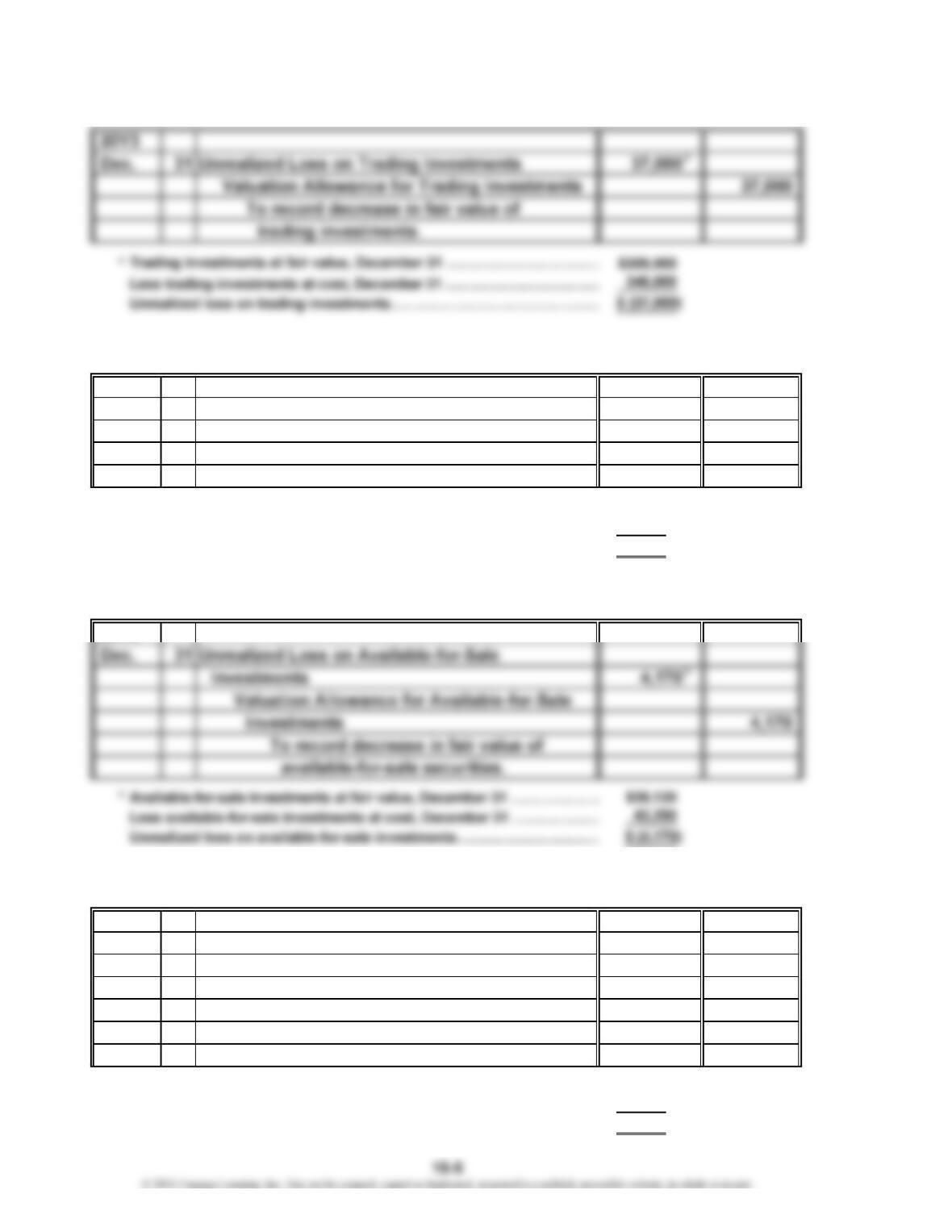

20Y9

31 Valuation Allowance for Trading Investments

Unrealized Gain on Trading Investments 6,500

To record increase in fair value of

trading investments.

*Trading investments at fair value, December 31 …………………………

…

$79,100

Less trading investments at cost, December 31 …………………………

…

72,600

Unrealized gain on trading investments……………………………………

…

$ 6,500

PE 15-5A

20Y5

PE 15-5B

20Y7

31 Valuation Allowance for Available-for-Sale

Investments

Unrealized Gain on Available-for-Sale

Investments 3,830

To record increase in fair value of

available-for-sale securities.

*Available-for-sale investments at fair value, December 31 ………………

…

$22,870

Less available-for-sale investments at cost, December 31 ………………

…

19,040

Unrealized gain on available-for-sale investments………………………… $ 3,830

Dec. 6,500

Dec.

3,830

*

*

…

…

…

PE 15-6A

$8.00

$100.00

Dividends per Share of Common Stock

Market Price per Share of Common Stock

Dividend Yield

= 0.08, or 8%

=

=

CHAPTER 15 Investments

Ex. 15-1

a. 22 Investments—Jupiter Co. Stock 850,680

Cash 850,680

* (34,000 shares × $25) + $680

c. 12 Cash 216,900

Gain on Sale of Investments 41,760

Investments—Jupiter Co. Stock 175,140

* (7,000 shares × $31) – $100

** ($850,680 ÷ 34,000 shares) × 7,000 shares

d. 31 Valuation Allowance for Equity

Ex. 15-2

Apr. 10 Investments—Delew Company Stock 660,220

Cash 660,220

* (11,000 shares × $60) + $220

Sept. 10 Cash 161,910

Loss on Sale of Investments 18,150

Investments—Delew Company Stock 180,060

* (3,000 shares × $54) – $90

** 3,000 shares × ($660,220 ÷ 11,000 shares)

Dec.

EXERCISES

Feb.

Nov.

*

*

**

*

*

**

CHAPTER 15 Investments

Ex. 15-3

2 Investments—Celeste Inc. Stock 99,324

Cash 99,324

* (3,100 shares × $32) + $124

7 Investments—Celeste Inc. Stock 53,256

Cash 53,256

* (1,400 shares × $38) + $56

*(4,000 shares × $41) – $100

** 3,100 shares purchased……………………………………………………

…

$ 99,324

900 shares × ($53,256 ÷ 1,400 shares)……………………………………

…

34,236

Total cost………………………………………………………………………

…

$133,560

25 Cash 310

Dividend Revenue 310

* 500 shares × $0.62

Feb.

June

Sept.

*

*

*

CHAPTER 15 Investments

Ex. 15-4

Feb. 24 Investments—Tett Co. Stock 85,150

Cash 85,150

* (1,000 shares × $85) + $150

May 16 Investments—Issacson Co. Stock 90,100

Cash 90,100

* (2,500 shares × $36) + $100

Aug. 12 Cash 24,295

Loss on Sale of Investments 2,735

Investments—Issacson Co. Stock 27,030

* (750 shares × $32.50) – $80

** 750 shares × ($90,100 ÷ 2,500 shares)

Oct. 31 Cash 240

Dividend Revenue 240

* (1,000 shares – 400 shares) × $0.40

Ex. 15-5

a. 1. Investment in Tran Corp. Stock 210,000

Income of Tran Corp. 210,000

To record 35% share of Tran Corp.

net income [$600,000 × (280,000 shares ÷

800,000 shares)].

2. Cash 140,000

Investment in Tran Corp. Stock 140,000

* 280,000 shares × $0.50

*

*

*

**

*

*

CHAPTER 15 Investments

Ex. 15-6

a.

4 Investment in Silva Company Stock 14,400,000

Cash 14,400,000

* 480,000 shares × $30 per share

2 Cash 300,000

Investment in Silva Company Stock 300,000

* $750,000 × (480,000 ÷ 1,200,000 shares)

b. Initial acquisition cost…………………………………………………………

…

$14,400,000

Equity earnings for 20Y4………………………………………………………

…

800,000

Cash dividends received………………………………………………………

…

(300,000)

Investment in Silva Company Stock balance,

December 31, 20Y4……………………………………….…………………… $14,900,000

Ex. 15-7

a.

6 Investment in Gator Co. Stock 212,000

Cash 212,000

b. Initial acquisition cost…………………………………………………………

…

$212,000

Equity loss for 20Y8……………………………………………………………

…

(19,040)

Cash dividends received………………………………………………………

…

(8,160)

Investment in Gator Co. Stock balance, December 31, 20Y8……………

…

$184,800

20Y4

July

Jan.

20Y8

Jan.

*

*

CHAPTER 15 Investments

Ex. 15-7 (Concluded)

c. Under the equity method, the investor will record its proportionate share of

the net increase (or decrease) of the book value of the investee resulting from

earnings and dividend distributions. The fair value method uses market price

Ex. 15-8

Investment in Raven Company stock, December 31, 20Y5……………………

…

Plus equity earnings in Raven Company…………………………………………

…

Less dividends received*……………………………………………………………

…

Investment in Raven Company stock, December 31, 20Y6……………………

…

$281

(in millions)

$264

25

(8)

CHAPTER 15 Investments

Ex. 15-9

a. 1 Investments—Marimar Co. Bonds 150,000

Cash 150,000

b. 1 Cash 4,500

Interest Revenue 4,500

$150,000 × 6% × 6/12.

Ex. 15-10

a.

1 Investments—Effenstein Corp. Bonds 240,000

Cash 240,000

c.

1 Cash 9,600

Interest Receivable 4,800

Interest Revenue 4,800

* $240,000 × 8% × 3/12

e.

1 Cash 150,000

Investments—Effenstein Corp. Bonds 150,000

20Y8

Oct.

Nov.

May

20Y1

Oct.

Apr.

20Y2

*

CHAPTER 15 Investments

Ex. 15-11

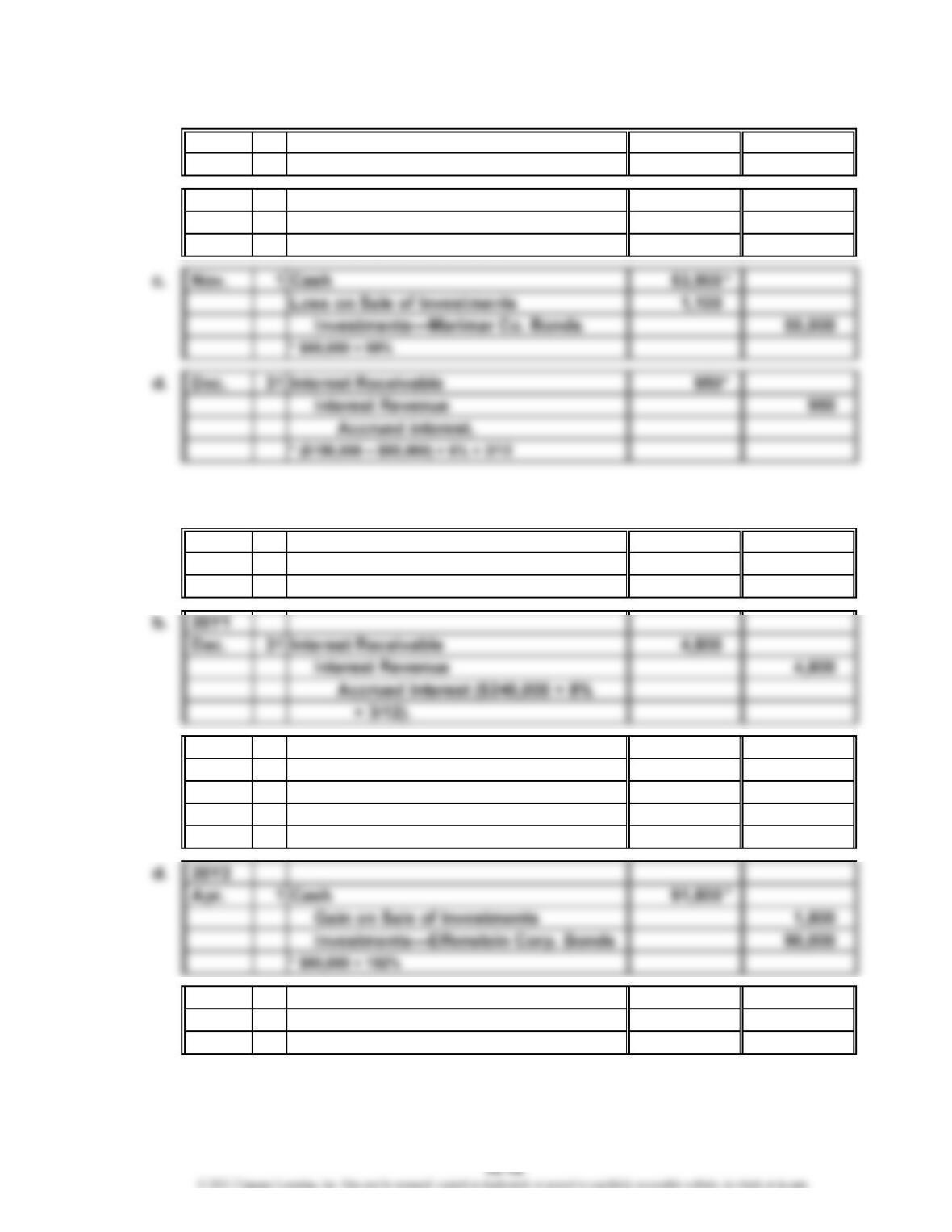

a.

11 Investments—Lumpkin County Bonds 360,000

Interest Receivable 2,400

Cash 362,400

* $360,000 × 6% × 40 ÷ 360

c. 31 Cash 88,450

Loss on Sale of Investments 2,000

Interest Revenue 450

Investments—Lumpkin County Bonds 90,000

*Bond sale ($90,000 × 0.98)………………………………… $88,200

Accrued interest ($90,000 × 6% × 30 ÷ 360)……………

…

450

Less brokerage commission……………………………

…

(200)

Total proceeds………………………………………………

…

$88,450

Investments—Lumpkin County Bonds 270,000

May

Year 1

Oct.

*

*

CHAPTER 15 Investments

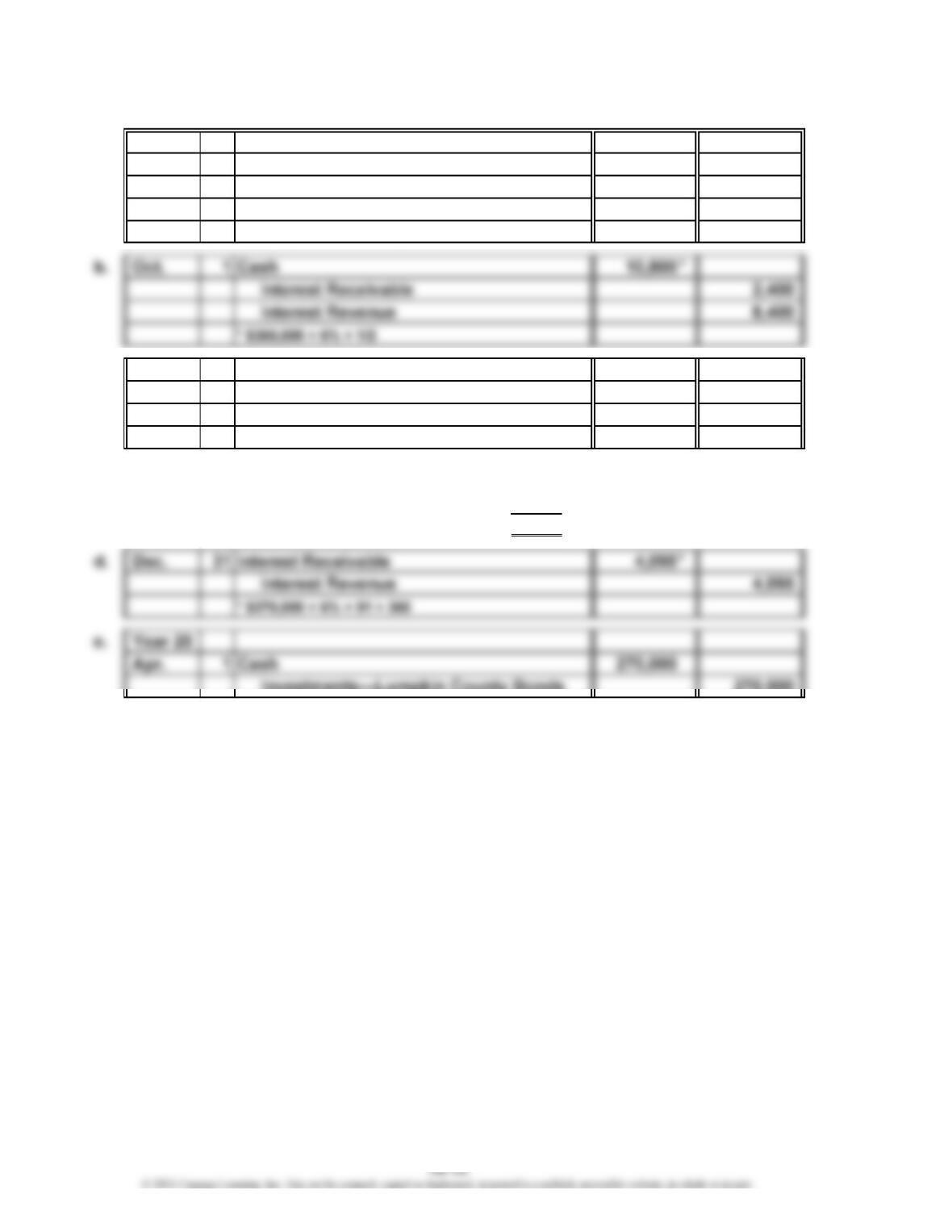

Ex. 15-12

a. 31 Investments—Government Bonds 75,000

Interest Receivable 375

Cash 75,375

* $75,000 × 6% × 30 ÷ 360

30 Cash 34,650

Loss on Sale of Investments 700

Interest Revenue 350

Investments—Government Bonds 35,000

*Bond sale ($35,000 × 98%)………………………………

…

$34,300

Accrued interest ($35,000 × 6% × 60/360)……………

…

350

Total proceeds from sale…………………………………

…

$34,650

c. 1 Cash 40,000

Investments—Government Bonds 40,000

Ex. 15-13

Interest earned

(

Februar

y

1 to Jul

y

1

)

1

…………………………………………… $2,500

Interest earned on sold bonds

(

Jul

y

1 to October 1

)

2

…………………………

…

500

Interest earned on remainin

g

bonds

(

Jul

y

1 to December 31

)

3

……………… 2,000

Total interest earned during the year……………………………………………

…

$5,000

July

Jan.

Aug.

*

*

CHAPTER 15 Investments

Ex. 15-14

a. {$35,000 [from (c)] – $29,000 [from (b)]}

b. [$17,000 – $(12,000)]

c. ($245,000 – $210,000)

d. ($144,000 – $12,000)

Ex. 15-15

a.

24 Trading Investments—Raiders Inc. 551,000

Cash 551,000

b. The unrealized gain or unrealized loss on trading investments is reported

on the income statement as Other Revenue (or a separate item if significant).

Unrealized losses would be deducted in determining net income, while

unrealized gains would be added in determining net income.

c. The unrealized gain on available-for-sale investments of $58,000 would be

reported as an addition to stockholders’ equity on the balance sheet. The

debit balance of Valuation Allowance for Available-for-Sale Investments of

$58,000 would be added to the balance of the investments account of

$551,000 to report the fair value of $609,000 on the balance sheet.

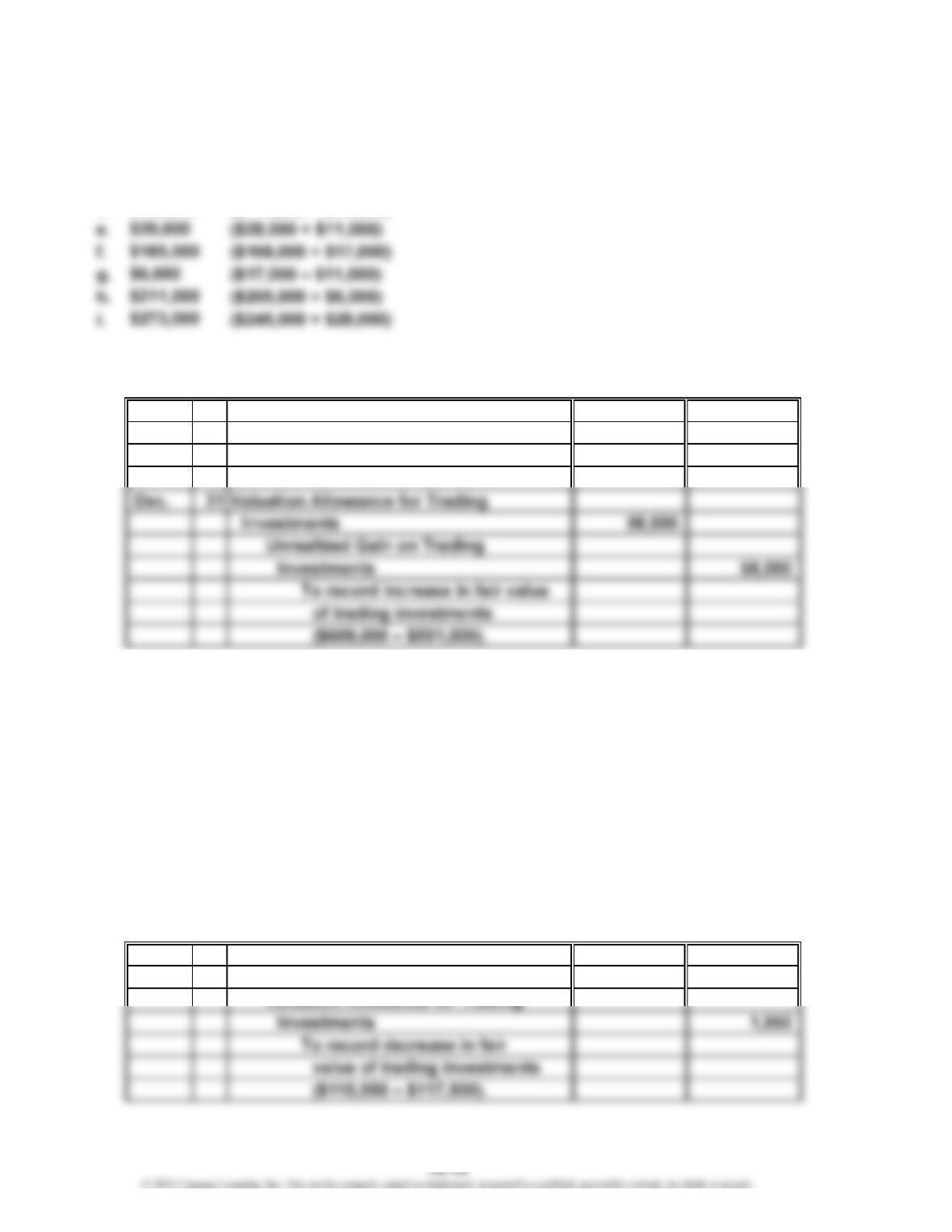

Ex. 15-16

a.

31 Unrealized Loss on Trading Investments 1,950

20Y3

Dec.

$6,000

$29,000

$35,000

Feb.

$132,000

20Y7

CHAPTER 15 Investments

Ex. 15-16 (Concluded)

b.

10 Trading Investments—Carroll Inc. 34,900

Cash

c.

31 Valuation Allowance for Trading

Investments 24,550

* Since the Valuation Allowance for Trading Investments has an “unadjusted” credit balance of

$1,950 on December 31, 20Y4, $1,950 must be added to arrive at an “adjusted” balance of

$22,600 ($175,000 – $117,500 – $34,900) on December 31, 20Y4.

d. $175,000; the fair value of the trading investments, which is the sum of the

trading investments account of $152,400 and the valuation account of $22,600.

Ex. 15-17

* $337,500 – $320,000, as determined from the following schedule:

Issuing Company Cost

Arden Enterprises Inc. ……………………………………………………… $150,000

French Broad Industries Inc. ………………………………………………

…

66,000

Pisgah Construction Inc. …………………………………………………… 104,000

Total………………………………………………………………………… $320,000

b. There would be no adjusting entry for December 31, 20Y6, if the fair value of

the portfolio of securities is unchanged from December 31, 20Y5. This is

34,900

$170,000

Dec.

20Y4

May

20Y4

Fair Value

Dec. 31, 20Y5

71,500

96,000

$337,500

CHAPTER 15 Investments

Ex. 15-17 (Concluded)

c.

31 Valuation Allowance for Available-for-

Sale Investments 2,500

Unrealized Gain on Available-

d.

31 Unrealized Loss on Available-for-Sale

Investments 7,500

Valuation Allowance for Available-

for-Sale Investments

Ex. 15-18

Ex. 15-19

a. Current: Dividend Yield = $1.68 ÷ $101.57 = 1.65%

Previous: Dividend Yield = $1.56 ÷ $85.95 = 1.82%

b. Dividends per share increased in the current year from the previous year. The

dividend yield, however, decreased from 1.82% in the previous year to 1.65% in the

current year. This decrease is a result of a decrease in the dividend relative to stock

price. Microsoft provides a small return to the shareholder in terms of a dividend

yield and an additional return in terms of price appreciation of the stock.

Ex. 15-20

7,500

Dividend Yield Cash Dividends per Share of Common Stock

Market Price per Share of Common Stock

20Y6

Dec.

2.1%

=

=$198.01

$4.19 =

20Y6

Dec.

CHAPTER 15 Investments

Appendix Ex. 15-21

Net income

Other comprehensive income (loss):

Valur Co.

For the Year Ended December 31, 20Y8

$210,000

CHAPTER 15 Investments

Prob. 15-1A

1.

1 Investments—Caldwell Inc. Stock 375,075

Cash 375,075

* (7,500 shares × $50 per share) + $75

31 Cash 1,500

Dividend Revenue 1,500

* (7,500 shares – 4,500 shares) × $0.50

Nov. 15 Cash 152,910

Gain on Sale of Investments 2,880

Investments—Caldwell Inc. Stock 150,030

* (3,000 shares × $51 per share) – $90

** 3,000 shares × ($375,075 ÷ 7,500 shares)

PROBLEMS

20Y2

Feb.

*

*

*

**

CHAPTER 15 Investments

Prob. 15-1A (Concluded)

1 Trading Investments—Fuller Inc. 125,000

Cash 125,000

14 Cash 30,000

Gain on Sale of Investments 5,000

2.

Current assets:

Trading investments (at cost) $226,000

3. Unrealized gains or losses are reported on the income statement, often as

“Other Revenue (Losses).” For 20Y2, Rios Co. would have reported an

unrealized loss of $6,000 as “Other Losses.” For 20Y3, Rios Co. would have

Rios Co.

Oct.

Balance Sheet (selected items)

December 31, 20Y3

20Y3

Apr.

*

**