15–1

Chapter 15

Transfer Pricing

Learning Objectives

1. Explain the basic issues associated with transfer pricing.

2. Explain the general transfer pricing rules and understand the underlying basis for them.

3. Identify the behavioral issues and incentive effects of negotiated transfer prices, cost-based

transfer prices, and market-based transfer prices.

4. Explain the economic consequences of multinational transfer prices.

5. Describe the role of transfer prices in segment reporting.

15–2

Chapter Overview

I. WHAT IS TRANSFER PRICING AND WHY IS IT IMPORTANT?

II. DETERMINING THE OPTIMAL TRANSFER PRICE

• The Setting

• Determining Whether a Transfer Price is Optimal

• Case 1: A Perfect Intermediate Market for Wood

• Case 2: No Intermediate Market

III. OPTIMAL TRANSFER PRICE: A GENERAL PRINCIPLE

• Other Market Conditions

IV. APPLYING THE GENERAL PRINCIPLE

V. HOW TO HELP MANAGERS ACHIEVE THEIR GOALS WHILE ACHIEVING THE

ORGANIZATION’S GOALS

VI. TOP MANAGEMENT INTERVENTION IN TRANSFER PRICING

VII. CENTRALLY ESTABLISHED TRANSFER PRICING POLICIES

• Establishing a Market Price Policy

• Establishing a Cost-Basis Policy

• Alternative Cost Measures

o Full Absorption Cost-Based Transfers

o Cost-Plus Transfers

o Standard Costs or Actual Costs

• Remedying Motivational Problems of Transfer Pricing Policies

o Dual Transfer Prices

VIII. NEGOTIATING THE TRANSFER PRICE

IX. IMPERFECT MARKETS

X. GLOBAL PRACTICES

XI. MULTINATIONAL TRANSFER PRICING

XII. SEGMENT REPORTING

XIII. APPENDIX: CASE 1A PERFECT INTERMEDIATE MARKETS – QUALITY

DIFFERENCES

15–3

Chapter Outline

LO 15-1 Explain the basic issues associated with transfer pricing.

WHAT IS TRANSFER PRICING AND WHY IS IT IMPORTANT?

• Decentralization in the firm is often beneficial because it lowers information costs associated

with attempting to make decisions centrally and because the organization benefits from using

managers’ local knowledge.

o Recall that decentralization is the delegation of decision-making authority to subordinates.

• Transfer price is the value assigned to the goods or services sold or rented (transferred)

from one unit of an organization to another. Transfer price is the price at which the

transaction between the divisions is recorded.

o Because the exchange takes place within the organization, the firm has considerable

discretion in setting the transfer price.

o The profit on the sale that accrues to the selling division is the transfer price less the cost

of goods sold.

▪ The profit that will accrue to the buying division when the item is sold to an external

15–4

▪ The transfer price is not a factor in the calculation of total profit for the firm and,

therefore, does not affect corporate profit if the transaction occurs. (See Business

Application box “Transfer Pricing at Weyerhaeuser.”)

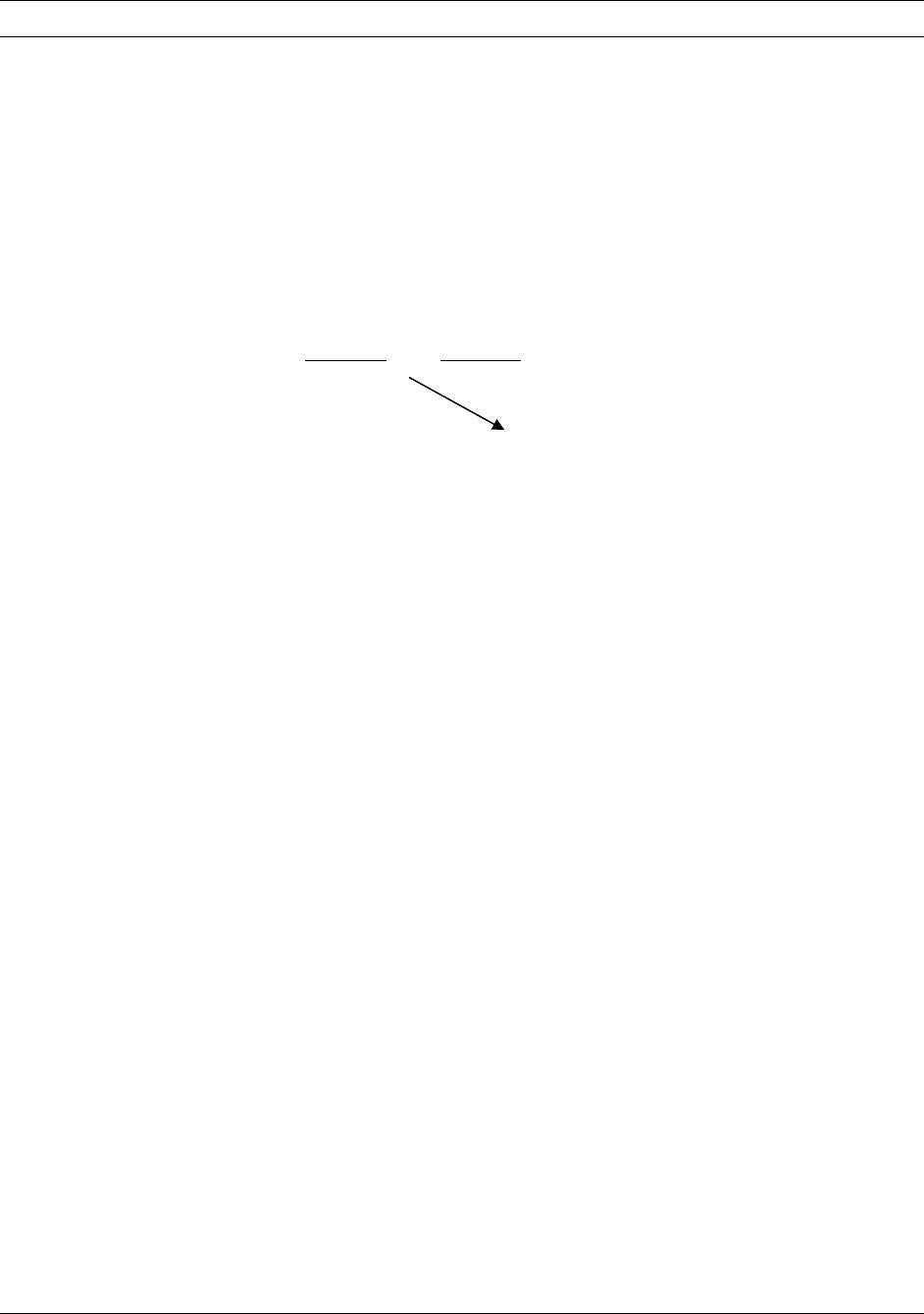

o The following diagram illustrates the relation between a selling division and a buying

division within the same organization when goods or services are exchanged internally.

The total profit calculation does not involve the transfer price used; the selling division’s

revenue from the transfer is cancelled out by the buying division’s cost for the transaction.

• What makes the transfer price important is that it affects the division managers’ decision

about whether to engage in the transaction.

o Because the managers of both the selling division and buying division are evaluated on

division profit, they consider the effect of all sales, not just sales to customers outside the

company, on their division, not company profit.

o The definition of the transfer price can affect corporate profitability.

▪ The optimal transfer price is the price that leads both division managers, each acting

in his or her own self-interest, to make decisions that are in the firm’s interest.

15–5

▪ If business unit profitability is used to measure performance, by return on investment

(ROI) or economic value added (EVA), the transfer price will affect the evaluation of

the unit and the unit manager.

o Example 1: It costs the selling division $20 to produce one unit of a component which, if

transferred to the buying division, requires additional work costing $45 and can be sold to

outside customers for $100 per unit of the finished product. Assume that the transfer

price in question is TP. Then

Selling division’s profit (S) = TP – $20.

Buying division’s profit (B) = $100 – TP – $45.

Total profit for the firm = (TP – $20) + ($100 – TP – $45) = $35.

LO 15-2 Explain the general transfer pricing rules and understand the

underlying basis for them.

DETERMINING THE OPTIMAL TRANSFER PRICE

• The Setting

o The transfer price is a device to motivate managers to act in the best interests of the

company.

15–6

Selling Division

Goods or services

Buying Division

Final Market

Transfer price

Intermediate

Market

• Determining Whether a Transfer Price is Optimal

o There is a simple test, an application of the differential profitability analysis (discussed in

Chapter 4) to determine whether the calculated transfer price is optimal.

• If the answer to the first question is “yes,” the answers to questions 2 and 3 must

also be “yes” or the transfer price is not optimal. If the answer to the first question

is “no,” the answer to either question 2 or 3 (or both) must be “no” or the transfer

price is not optimal.

o Example 2 (Revised from Example 1): It costs the selling division $60 to produce one

unit of a component which, if transferred to the buying division, requires additional work

costing $45 and can be sold to outside customers for $100 per unit of the finished product.

Assume that the transfer price in question is TP. Then

Selling division’s profit (S) = TP – $60

15–7

o In determining the optimal transfer price, the important issue is the nature of the

intermediate market where the goods are being transferred. Two cases are considered:

▪ A perfect intermediate market, and

• Case 1: A Perfect Intermediate Market for Wood

o The product being sold in a perfect market is not differentiated by quality, service, or

other characteristics.

o The parties in a perfect market are “price takers.”

o Given the optimal transfer price, the two division managers acting independently will

make the transfer that the corporate staff would set if it had all the information that the

division managers have. (See Business Application box “Transfer Pricing in State-Owned

Enterprises.”)

▪ With an efficient transfer pricing system like this, when external markets (both

intermediate and final) change, there is no need to change the transfer price policy.

• Case 2: No Intermediate Market

o If there is no intermediate market for the goods being transferred, or the company has

15–8

▪ To be the optimal transfer price in general, it cannot depend on the current external

price.

o Example 3 (Revised from Example 1): It costs the selling division $20 (variable cost only)

to produce one unit of a component which, if transferred to the buying division, requires

additional work costing $45 and can be sold to outside customers for $100 per unit of the

finished product. There is no intermediate market for the component in question.

The selling division’s fixed cost is not a factor because it is unavoidable (therefore not

differential). The selling division will not accept a transfer price below $20, the variable

cost per unit.

Given the final market price of $100 and the additional cost of $45 to make the

component salable, the buying division will not pay more than $55 for the part.

OPTIMAL TRANSFER PRICE: A GENERAL PRINCIPLE

• The transfer price that is optimal represents the value of the goods being transferred to the

buying division at the transfer point.

o A general principle on setting the transfer price that leads managers to make decisions in

the firm’s best interests is:

15–9

• Other Market Conditions

o Case in Which Wood Division Is at Capacity

In the case of a perfect intermediate market, the value to the buying division is equal to

what it can be sold for in the intermediate market (i.e., intermediate market price).

o Imperfect Intermediate Markets

▪ If there is no intermediate market, there is no opportunity cost and the only cost is the

variable, or outlay cost. The transfer price should be set accordingly.

APPLYING THE GENERAL PRINCIPLE

• The general principle can be easily applied with the following two general rules when

establishing a transfer price.

o If an intermediate market exists, the optimal transfer price is the market price.

15–10

LO 15-3 Identify the behavioral issues and incentive effects of negotiated

transfer prices, cost-based transfer prices, and market-based

transfer prices.

HOW TO HELP MANAGERS ACHIEVE THEIR GOALS WHILE ACHIEVING THE

ORGANIZATION’S GOALS

• A conflict can occur between a company’s interests and the divisional manager’s interests

when transfer price-based performance measures are used.

o The general transfer pricing rules are easy to state but difficult to apply in practice.

o There are three general approaches to this type of problem in a decentralized organization:

▪ Direct intervention by top management

o Direct intervention by top management

▪ If the transfer is an extraordinarily large order, or if internal transfers are rare, direct

intervention could be the best solution to the problem.

▪ The disadvantages of direct intervention are that:

TOP MANAGEMENT INTERVENTION IN TRANSFER PRICING

• A transfer pricing policy should allow divisional autonomy yet encourage managers to

pursue corporate goals consistent with their division goals. The policy should also consider

the performance evaluation system used and the impact that alternative transfer prices will

have on managerial performance evaluation.

15–11

CENTRALLY ESTABLISHED TRANSFER PRICING POLICIES

• Establishing a Market Price Policy

o Market price-based transfer pricing is a transfer pricing policy that sets the transfer

price at the market price or at a small discount from the market price.

o Two general guidelines for market price-based transfer pricing are:

o Externally based market prices are generally considered the best basis for transfer pricing

when a competitive market exists for the product and when market prices are readily

available.

▪ Usually, there are differences between products produced internally and those that

can be purchased from outsiders, such as costs, quality, or product characteristics.

• Establishing a Cost-Basis Policy

o A cost-based transfer pricing policy should adhere to the following rule:

15–12

▪ The general rule is optimal for the company, but it does not benefit the selling

division for an internal transfer in the below-capacity case.

▪ When a measure of differential or variable cost, or market price is not available,

companies usually use full absorption costs as the transfer price.

• Alternative Cost Measures

o Full Absorption Cost-Based Transfers

▪ Full absorption cost has some advantages:

• These costs are available in the company’s records.

o Cost-Plus Transfers

▪ Cost-plus transfer pricing is a transfer pricing policy based on a measure of cost

(full costing or variable costing, actual or standard cost) plus an allowance for profit.

o Standard Costs or Actual Costs

▪ To promote responsibility in the selling division and to isolate variance within

divisions, standard costs are generally used as a basis for transfer pricing in cost-

based systems.

15–13

▪ A selling division whose transfers are almost all internal is usually organized as a cost

center.

o Dual Transfer Prices

▪ Dual transfer pricing is a transfer pricing system that charges the buying division

with costs only and credits the selling division with cost plus some profit allowance.

The difference could be accounted for in a specialized centralized account.

To encourage internal transfers, the company decides to implement a dual transfer

pricing system in which the buying division is charged for the $20 cost while the

selling division is credited with a $3 profit allowance. On a per-unit basis,

Selling Division:

Accounts Receivable – Buying Division

20

Intercompany Sales in Excess of Assigned Costs

3

Intercompany Sales

23

Intercompany Cost of Goods Sold

20

Finished Goods

20

Buying Division:

Inventory

20

15–14

▪ Disadvantages of dual price system are:

• It also tends to remove some of the performance evaluation value because both

managers benefit and the difference in the central account is ignored.

NEGOTIATING THE TRANSFER PRICE

• Negotiated transfer pricing is a system that arrives at the transfer prices through negotiation

between managers of buying and selling divisions.

o The managers involved in negotiation should act in much the same way as the managers

of independent firms.

o The major advantage to negotiated transfer pricing is that it preserves the autonomy of

the division managers.

o Two disadvantages of negotiated transfer pricing are:

▪ A great deal of management effort may be consumed in the negotiating process.

15–15

IMPERFECT MARKETS

• Transfer pricing can be quite complex when selling and buying divisions cannot sell and buy

all they want in perfectly competitive markets.

o In some cases, there may be no outside market at all. In others, the market price could

depend on how many units the divisions want to buy or sell on the market.

GLOBAL PRACTICES

• The authors of surveys of corporate practices (summarized in Exhibit 15.5) report that nearly

45 percent of the U.S. companies surveyed use a cost-based transfer pricing system, 33

percent use a market price–based system, and 22 percent use a negotiated system. Similar

results have been found for companies in Canada and Japan.

o Generally, when negotiated prices are used, they are between the market price at the

upper limit and some measure of cost at the lower limit.

▪ No transfer pricing policy applied in practice is likely to dominate all others.

LO 15-4 Explain the economic consequences of multinational transfer prices.

MULTINATIONAL TRANSFER PRICING

• In international (or interstate) transactions, transfer prices may affect tax liabilities, royalties,

and other payments because of different laws in different countries (or states or provinces).

15–16

o Management control considerations suggest that the transfer price reflect the value of the

goods or services being transferred.

LO 15-5 Describe the role of transfer prices in segment reporting.

SEGMENT REPORTING

• The FASB requires companies engaged in different lines of business to report certain

information about segments that meet FASB’s technical requirements (Statement of

Financial Accounting Standards No.131, “Disclosure about segment of an enterprise and

related information”).

o The principal items that must be disclosed about each segment include:

▪ Segment revenue, from both internal and external customers

▪ Interest revenue and expense

▪ Segment operating profit or loss

15–17

Appendix: Case 1a Perfect Intermediate Markets – Quality Differences

APPENDIX: CASE 1A PERFECT INTERMEDIATE MARKETS – QUALITY

DIFFERENCES

• The case of perfect intermediate markets is not interesting because there is really little

opportunity for managerial discretion.

• Example 5 (Revised from Example 1): It costs the selling division $20 to produce one unit of

a component which, if transferred to the buying division, requires additional work costing

$45 and can be sold to outside customers for $100 per unit of the finished product.

15–18

Matching

A.

Cost-plus transfer pricing

D.

Negotiated transfer pricing

B.

Dual transfer pricing

E.

Transfer price

C.

Market price-based transfer pricing

_____ 1. The value assigned to the goods or services sold or rented (transferred) from one unit

of an organization to another.

_____ 2. A system that arrives at the transfer prices through negotiation between managers of

buying and selling divisions.

_____ 3. A transfer pricing system that charges the buying division with costs only and credits

the selling division with cost plus some profit allowance.

_____ 4. A transfer pricing policy that sets the transfer price at the market price or at a small

discount from the market price.

_____ 5. A transfer pricing policy based on a measure of cost (full costing or variable costing,

actual or standard cost) plus an allowance for profit.

15–19

Matching Answers

Multiple Choice

1. A transfer price:

a. Is the value assigned to the goods or services sold from one unit of an organization to

another.

b. Represents a cost to the selling division.

c. Will affect the company’s total profits.

d. Is the same as the market price.

2. A market is perfect if:

a. The buyers can buy at any quantity without affecting the price.

b. The sellers can sell at any quantity without affecting the price.

c. The parties in the market are price takers.

d. All of the above.

3. Which of the following statements is not correct?

a. If an intermediate market exists, the optimal transfer price is the market price.

b. If no intermediate market exists, the optimal transfer price should be the outlay cost for

producing the goods.

c. If the selling division is operating at capacity and there is a market for the goods being

transferred, the variable cost of the goods should be used.

d. If the selling division is operating at capacity and there is no intermediate market, then

the opportunity cost depends on the cost of adding capacity.

4. When should the top management intervene in setting the transfer price?

a. The transfer is an extraordinarily large order.

b. Internal transfers are rare.

c. Internal transfer benefits the company but the division managers cannot agree on a price.

d. All of the above.

5. The selling division sells all it can produce at $18 per unit. The contribution margin lost due

to internal transfer is $6 per unit. What is the outlay cost per unit?

a. $24

b. $18

c. $6

d. $12

Use the following information to answer questions 6 and 7:

The selling incurs variable cost of $2 per unit. The buying division incurs additional $5 per unit

and sells the final product for $15 per unit.

15–21

6. If there is no intermediate market and the selling division is not operating at capacity, what is

the optimal transfer price?

a. $15

b. $7

c. $5

d. $2

7. What is the company’s profit per unit?

a. $12.

b. $8.

c. $7.

d. $5.

Use the following information to answer questions 8 through 9:

A manufacturing company has two divisions: Motor and Pump. The Motor Division produces an

intermediate good, which is a motor that can be used as an input for the Pump Division. The

Motor Division also sells the motors in the open market. The Pump Division assembles the parts

together to make water pumps which are sold to the consumers. The Pump Division needs an

average of 10,000 motors every year. A transfer price based on the variable cost is mandated.

Motor

Division

Pump

Division

Market selling price

$20

Selling price

$80

Variable cost

12

Variable cost (other than the motor)

30

Contribution margin

$ 8

Variable cost of the motor

(purchased from an outside supplier)

19

Contribution margin

$31

8. If the Motor Division has no excess capacity, what is the net result of the variable cost-based

transfer pricing policy?

a. A gain of $2 per unit

b. A loss of $1 per unit

c. $0

d. There is not enough information to determine the net result.

9. If the Motor Division has available capacity to handle the Pump Division’s demand, what is

the net result of the variable cost-based transfer pricing policy?

a. A gain of $7 per unit

b. A gain of $4 per unit

c. A loss of $7 per unit

d. A loss of $2 per unit

10. Segment reporting:

a. Is required by FASB.

b. Must disclose segment revenue, interest revenue and expense, segment operating profit or

loss, identifiable segment assets, and so on.

c. Applies to foreign operations.

d. All of the above.

11. Which of the following is suitable to deal with problems as a result of transfer price-based

performance measures being adopted?

a. Direct intervention by top management

b. Centrally established transfer price policy

c. Negotiated transfer prices

d. All of the above

12. Which of the following statements is incorrect?

a. A transfer pricing policy should allow divisional autonomy.

b. Market prices, if available, are considered the best basis for transfer pricing.

c. A seller operating at capacity should transfer at the differential cost of production.

d. Full-absorption costs are higher than variable costs.

15–23

Multiple Choice Answers

15–24

Demonstration Problem 1

A manufacturing company has two divisions: Motor and Pump. The Motor Division produces an

intermediate good, motors, which can be used as an input for the Pump Division. The Motor

Division also sells the motors in the open market. The Pump Division secures the motors from

either the Motor Division or an outside supplier and assembles the parts together to make water

pumps which are sold to the consumers. The Pump Division needs an average of 10,000 motors

every year.

The following information is available.

Motor

Division

Pump

Division

Selling price

$20

Selling price

$80

Variable cost

12

Variable cost (other than the motor)

30

Contribution margin

$ 8

Variable cost of the motor

(purchased from an outside supplier)

19

Contribution margin

$31

Required:

1. Discuss the possible transfer prices under each of the following independent situations.

2. The Motor Division sells all it can produce (80,000 motors) to the outside customers.

3. The Motor Division can produce 80,000 motors but sells only 65,000 motors to the outsider

customers.

4. The Pump Division requires a customized version of the motors that only the Motor Division

can supply. The variable cost for the Motor Division would be $22 per motor. The Motor

Division is running at capacity.

5. The Pump Division requires a customized version of the motors that only the Motor Division

can supply. The variable cost for the Motor Division would be $22 per motor. The Motor

Division has the excess capacity to handle the Pump Division’s demand.

15–25

Demonstration Problem 1 – Solution

Part 1

Since the Motor Division is operating at capacity, the only transfer price that is acceptable is the

Part 2

Since the Motor Division has excess capacity, it will accept a price that at least covers the

Part 3

Since the Motor Division is operating at capacity, it will not accept any price less than $30,

Part 4

15–26

Demonstration Problem 2

(Revised from Demonstration Problem 1)

A manufacturing company has two divisions: Motor and Pump. The Motor Division produces an

intermediate good, motors, which can be used as an input for the Pump Division. The Pump

Division assembles the parts together to make water pumps which are sold to the consumers. The

Pump Division needs an average of 10,000 motors every year.

The following information is available.

Motor

Division

Pump

Division

Selling price

?

$80

Variable manufacturing cost

12

30

Transferred-in cost

?

Variable overhead

2

15

Fixed overhead

3

9

Required:

Calculate divisional operating income and total operating income given the following

independent transfer pricing policies.

1. Market-based transfer price of $20 per motor.

2. Cost-based transfer price at 105% of the full absorption cost per motor.

3. Negotiated transfer price of $18.5 per motor.

4. The Motor Division receives the transfer price at 105% of the full absorption; the Pump

Division pays only the variable manufacturing cost.

15–27

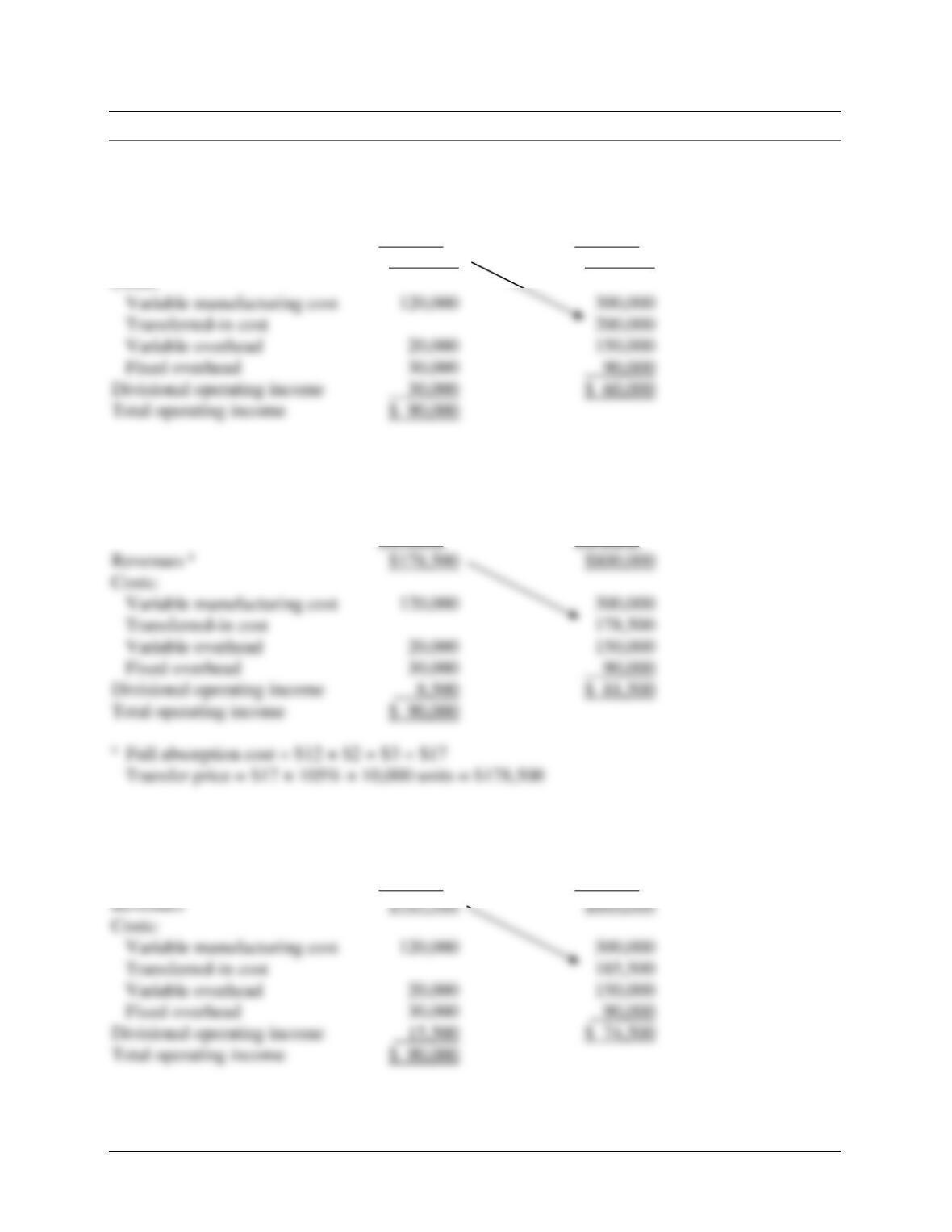

Demonstration Problem 2 – Solution

Part 1

Motor

Division

Pump

Division

Revenues a

$200,000

$800,000

Part 2

Motor

Division

Pump

Division

Revenues a

$178,500

$800,000

Costs:

Variable manufacturing cost

Transferred-in cost

Variable overhead

Fixed overhead

90,000

Divisional operating income

$ 81,500

Total operating income

$ 90,000

Part 3

Motor

Division

Pump

Division

Costs:

Variable manufacturing cost

Transferred-in cost

Variable overhead

Fixed overhead

Divisional operating income

$ 74,500

Total operating income

$ 90,000

Costs:

Variable manufacturing cost

Transferred-in cost

Variable overhead

Fixed overhead

90,000

Divisional operating income

30,000

$ 60,000

Total operating income

$ 90,000

Demonstration Problem 2 – Solution, continued

Part 4

Motor

Division

Pump

Division

Revenues

$178,500

$800,000

Costs:

Variable manufacturing cost

Transferred-in cost

Variable overhead

Fixed overhead

90,000

Divisional operating income

$140,000

Total operating income

15–29

Demonstration Problem 3

(Revised from Demonstration Problem 2)

A manufacturing company has two divisions: Motor and Pump. The Motor Division is located in

a low tax country (Tax rate = 25%) and produces an intermediate good, motors, that can be used

as an input for the Pump Division. The Pump Division is located in a high tax country (Tax rate

= 40%) and assembles the parts together to make water pumps which are sold to the outside

customers. The Pump Division needs an average of 10,000 motors every year. The following

information is available.

Motor

Division

Pump

Division

Selling price

?

$80

Variable manufacturing cost

12

30

Transferred-in cost

?

Variable overhead

2

15

Fixed overhead

3

9

Required:

Calculate divisional operating income and total operating income and discuss tax implications,

given the following independent transfer pricing policies.

1. Market-based transfer price of $20 per motor.

2. Cost-based transfer price at 105% of the full absorption cost per motor.

3. Negotiated transfer price of $18.5 per motor.

Demonstration Problem 3 – Solution, continued

Market-Based

Transfer Price

@ $20

Cost-Based

Transfer Price

@ $17.85

Negotiated

Transfer Price

@ $18.5

Motor Division

Revenues

$200,000

$178,500

$185,500

Costs:

Variable manufacturing cost

120,000

120,000

120,000

Variable overhead

20,000

20,000

20,000

Fixed overhead

30,000

30,000

30,000

Divisional income before tax

$ 30,000

$ 15,500

Income tax (25%)

7,500

3,875

Divisional income

$ 22,500

$ 11,625

Pump Division

Revenues

$800,000

$800,000

$800,000

Costs:

Variable manufacturing cost

300,000

300,000

300,000

Transferred-in cost

Variable overhead

150,000

150,000

150,000

Fixed overhead

90,000

90,000

90,000

Divisional income before tax

$ 60,000

$ 74,500

Income tax (40%)

24,000

32,600

29,800

Divisional income

$ 48,900

$ 44,700

Total income

$ 58,500

$ 55,275

$ 56,325