Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Analysis of Operating Activities 441

P14-4 TO: Marta Feliz

FROM: (student’s name)

DATE: (today’s date)

SUBJECT: Pricing of new dishwasher line

With regard to pricing our new, quiet dishwasher, we will of course want

to determine what selling price will maximize return to our stockholders.

This would be the price that will maximize profit on the line through get-

ting the highest possible excess of sales revenues over variable costs.

We need to consider whether the low sound level is a sufficiently at-

tractive feature to allow us to follow a product differentiation strategy for

P14-5 A. Discount Shoes probably would be located near lower-income resi-

dential areas and in lower-cost facilities. Buildings and equipment

would not be fancy. Shoes might be stacked in metal racks by shoe

size so customers could locate merchandise for themselves. Prod-

ucts would be low cost. Designs would be those for which high de-

442 Chapter 14

Elegant Footwear probably would be located in shopping malls and

B. Relative to each other, the companies should exhibit the following:

Discount Shoes

Elegant Footwear

Sales revenues

High volume and low

Low volume and high

P14-6 Companies compete through product differentiation and cost leadership.

Product differentiation focuses on product quality and features. Cost

leadership focuses on cost control and low product prices.

(a) The products of cost leadership companies tend to be those that are

in high demand and that can be produced using standard designs.

(d) Asset turnover is likely to be higher for cost leadership companies

that attempt to generate high sales volumes.

(e) Cost leadership companies attempt to keep investment low to increase

Analysis of Operating Activities 443

P14-7

(In millions)

Dell

Apple

2004

2003

2004

2003

Profit margin (net income ÷ sales)

0.064

0.060

0.033

0.011

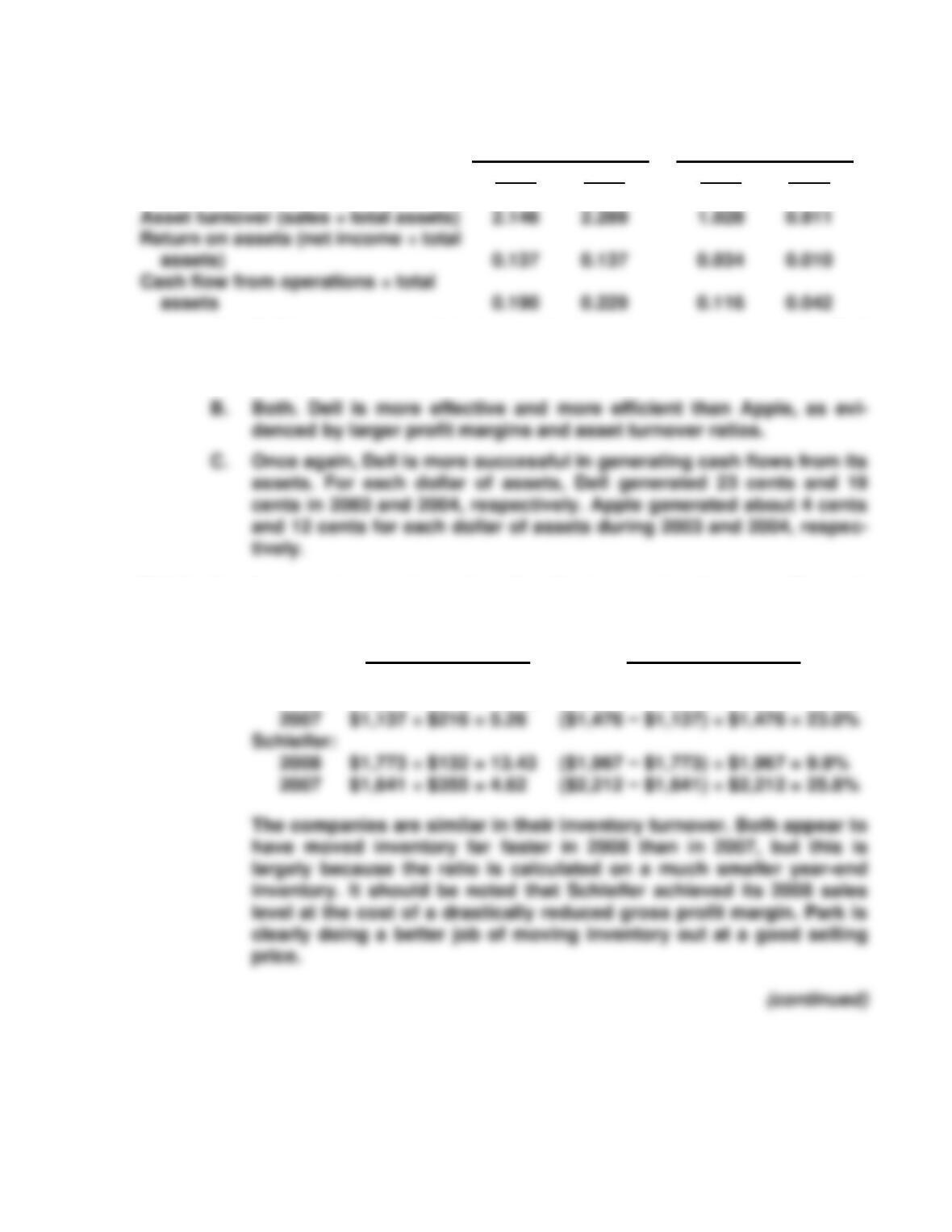

A. Dell is more successful at generating net income from its assets. Dell

produced an ROA of about 14% in both years, while Apple produced

an ROA of about 1% and 3% in 2003 and 2004, respectively.

P14-8 A. Inventory turnover (cost of goods sold ÷ inventory) and gross profit margin

[(sales − cost of goods sold) ÷ sales] are computed as follows:

Inventory turnover Gross profit margin

Park:

2008 $1,391 ÷ $115 = 12.10 ($1,811 − $1,391) ÷ $1,811 = 23.2%

444 Chapter 14

B. Receivable turnover (sales ÷ accounts receivable) can be computed

as follows:

C. Park, in 2008, generated a cash flow from operations that was about

2.6 times net income ($341 ÷ $131). The primary differences are de-

creases in inventories and increases in accounts payable, which may

B. Percentage analysis of the income statement has the following re-

sults:

2008

2007

2006

Net sales

Cost of sales

Gross income

100.00%

68.5%

31.5%

100.00%

67.7%

32.3%

100.00%

67.9%

32.1%

C. Because of increases in the cost of sales and in amortization of trade

names and goodwill, operating income (as a percentage of sales) has

decreased over the three-year period. One piece of good news is that

Analysis of Operating Activities 445

2008 had the effect of overcoming the decrease in operating income

tive, but it is only because of this one item.

D. Despite sales increases of 12.2% and 11.5% over the last two years,

P14-10 A.

Coca-Cola

PepsiCo

2004

2003

2002

2004

2003

2002

Gross profit margin

B. PepsiCo’s gross profit margin remained stable over the three-year

period, indicating production costs relative to sales have not

changed. However, PepsiCo’s operating profit margin improved dur-

446 Chapter 14

P14-11 A. Coca-Cola PepsiCo

2004 2003 2004 2003

Inventory turnover

(cost of goods sold ÷ inventory) 5.38 6.20 8.70 8.77

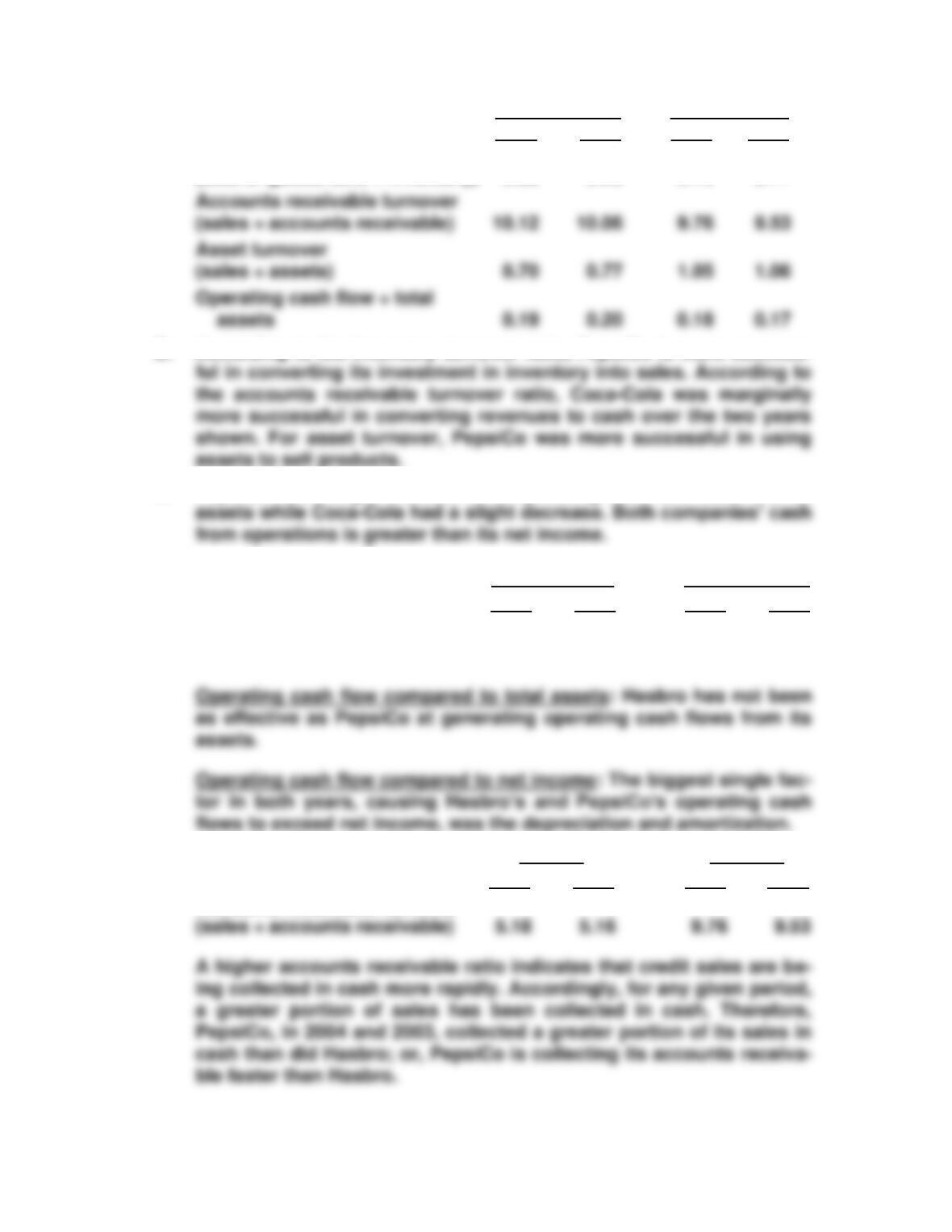

B. According to the inventory turnover ratio, PepsiCo is more success-

C. PepsiCo had a slight increase in its operating cash flow relative to its

P14-12 A. Hasbro PepsiCo

2004 2003 2004 2003

Cash flow from operations ÷ total assets 0.11 0.14 0.18 0.17

Cash flow from operations ÷ net income 1.83 2.87 1.20 1.21

B. Hasbro PepsiCo

2004 2003 2004 2003

Accounts receivable turnover

Analysis of Operating Activities 447

P14-13 A. 3M Corp. Eastman Chemical

2004 2003 2004 2003

Profit margin 0.149 0.132 0.026 −0.047

(net income ÷ sales)

3M Corp PM × ATO × FL = ROE

2004 0.149 0.966 1.995 0.288

B. According to the profit margin percentage (PM), 3M Corp. has been

P14-14 A. Given the facts presented, Big Bend is likely to be using a product

differentiation strategy, while Longbow is probably using the cost

leadership strategy. Product differentiation requires that the firm be

448 Chapter 14

B.

Year 2008 results

Big Bend

Longbow

Profit margin

9.1%

3.1%

It does appear that Big Bend relies on a high profit margin more than

C.

Year 2007 results

Big Bend

Longbow

Profit margin

(net income ÷ sales revenue)

8.7%

($3.13 ÷ $35.9)

3.0%

($5.8 ÷ $193.3)

Big Bend managed to increase its strength (profit margin) while its

D.

Return on equity

(net income ÷ equity)

Big Bend

Longbow

E. Which strategy is most successful depends on the measure chosen

to represent success. Generally, the measure used is return on equi-

ty. By that measure, the results of the two companies are equally

successful. This suggests that one strategy is not necessarily better

Analysis of Operating Activities 449

to rework their strategies. This would also include issues of operat-

ing leverage and financial leverage.

P14-15 A. Growth rates:

2004

2003

2002

2001

Average

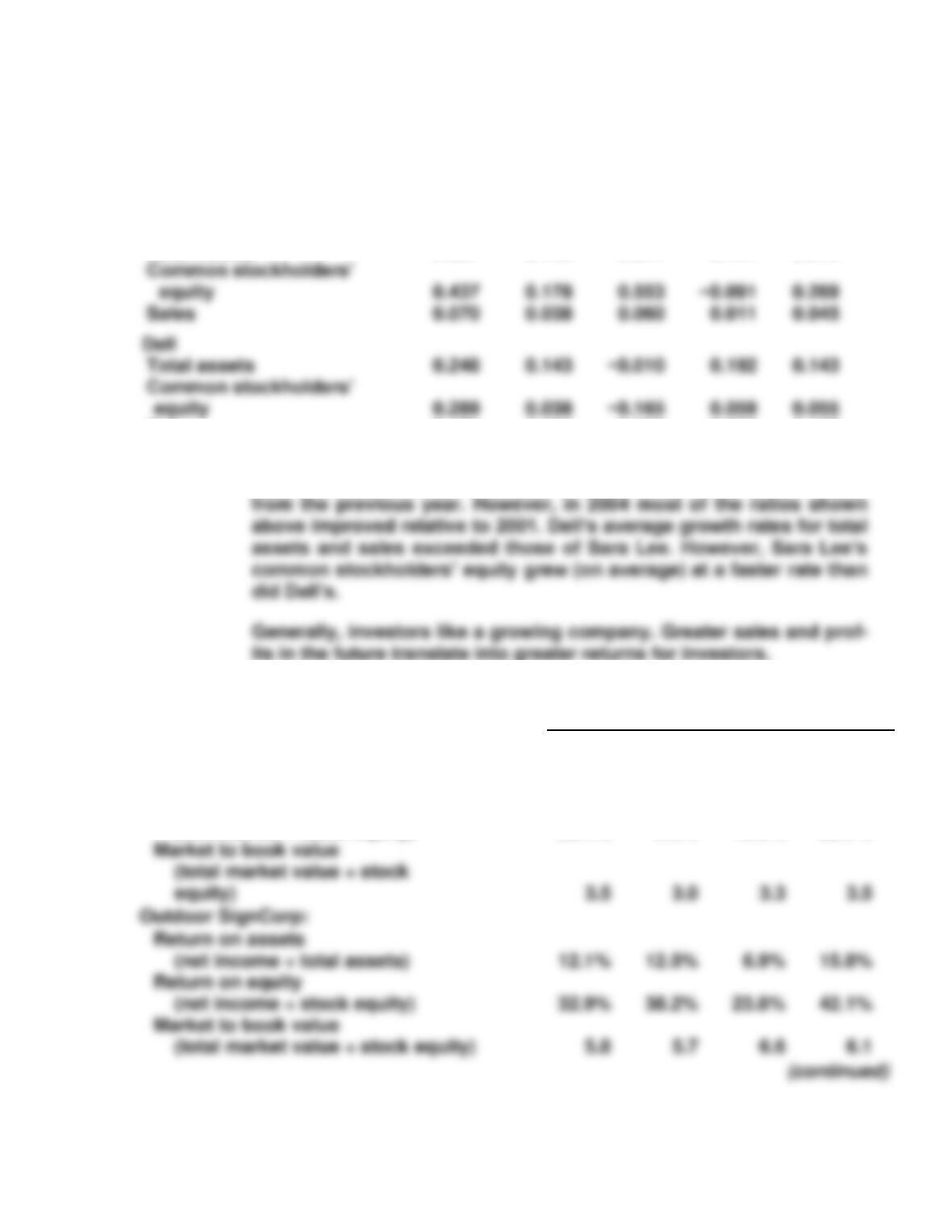

Sara Lee

Total assets

−0.037

0.128

0.347

−0.124

0.079

Sales

0.171

0.136

−0.023

0.262

0.137

B. Both companies report wide fluctuations in their growth rates over

the periods evaluated. During 2002, all of Dell’s changes declined

P14-16 A.

2008

2007

2006

2005

Billboards–R–Us:

Return on assets

(net income ÷ total assets)

6.5%

1.7%

6.5%

7.6%

Return on equity

(net income ÷ stock equity)

20.4%

6.0%

19.8%

22.5%

450 Chapter 14

B. Outdoor SignCorp’s return on assets has been significantly higher

P14-17 A.

John, Inc.

Roberta Company

2008

2007

2008

2007

1. Profit margin

7%

($57 ÷ $825)

5%

($37 ÷ $770)

4%

($14 ÷ $352)

9%

($30 ÷ $330)

6. Inventory

turnover

3.9

($540 ÷ $139)

3.7

($504 ÷ $136)

2.9

($250 ÷ $85)

3.0

($216 ÷ $71)

7. Return on as-

sets

3%

($57 ÷ $1,630)

2%

($37 ÷ $1,530)

2%

($14 ÷ $850)

4%

($30 ÷ $765)

Analysis of Operating Activities 451

B. This table identifies which company had the better value for each ra-

tio during each year.

Company with better ratio value

2008 2007

1. Profit margin John Roberta

2. Gross profit margin John same

C. Change from 2007 to 2008

John Roberta

1. Profit margin improvement decline

2. Gross profit margin no change decline

D. Overall, John Company had the better performance during the period

P14-18 Financial statements give only a partial view of a business entity, but that

part is very important. The statements summarize the effects of past

transactions. Statements have evolved as a relatively efficient way of giv-

ing the decision maker a summarized, approximate view of the financial

affairs of the company.

452 Chapter 14

However, statements are limited as tools for predicting the future of a

company. They are summaries; they report on the past; they make exten-

A supplier’s ability to remain in business and avoid cash flow prob-

lems might be indicated by its ability to generate cash from operations.

The operating section of the cash flows statement reports on this for a

given period. The income statement can be viewed as an estimate of the

P14-19 A. Measurement rules determine which attributes of the transformation

process are entered into the accounting system. They involve both

amounts and timing. Reporting rules determine the type and format of

information reported in financial statements for external users.

B. Measurement and reporting rules help to make financial statements

Analysis of Operating Activities 453

E. It is easier to establish standards on a national basis than on a

P14-20

Financial Analysis

Comparison

December 31, 2008

The Book

Wermz

Book Farm

Special Editions

Sales

$6,230,000

$20,584,000

$4,896,200

Cost of goods sold

3,426,500

13,390,200

2,153,100

Gross profit

2,803,500

7,193,800

2,743,100

Gross profit margin

0.4500

0.3495

0.5603

Operating profit margin

0.1041

0.0962

0.1820

Return on assets

0.0530

0.0643

0.0740

Financial leverage

1.6685

1.9821

1.4287

Return on equity

0.0884

0.1274

0.1057

1. Cost leadership Book Farm: low profit margin and high asset

(inventory) turnover

(continued)

4. Financial leverage Financial leverage is beneficial to all of the

P14-21

1

2

3

4

5

6

7

8

9

10

CASES

C14-1 A. and B.

General Mills

Microsoft

Procter & Gamble

2004

2003

2004

2003

2004

2003

General Mills’ profit margin, turnover, and return on assets all im-

proved from 2003 to 2004. The company’s profit margin and ROA are

C.

2004

2003

Receivables turnover

10.96

10.72

Inventory turnover

6.19

5.65

Gross profit margin

0.405

0.419

General Mills’ receivables turnover and inventory turnover improved

Analysis of Operating Activities 455

D.

2004

2003

Return on equity

0.201

0.220

E. Lists of estimated items could include depreciation and amortization

C14-2 A. Net Income 30 Weeks 25 Weeks

Revenues: $1,300 × 50 units ×

30 or 25 weeks $ 1,950,000 $ 1,625,000

Maintenance and operating costs:

$200 × 50 units × 52 weeks (520,000) (520,000)

Management costs (250,000) (250,000)

Cash flow from operating activities 1,180,000 855,000

Required reinvestment (200,000) (200,000)

Cash flow to investors $ 980,000 $ 655,000

* Other assets = $5,500,000 = $4,000,000 for buildings + $250,000 for

456 Chapter 14

B. Present value assuming 30-week average rental:

Present value of 10 periods of $980,000

discounted at 10% = $980,000 × 6.14457 = $ 6,021,679

C. Operating results are particularly sensitive to operating leverage in

D. If the condominiums rent for 30 weeks per year, on average, as ex-

C14-3 A. Expected Minimum

Sales $ 1,000,000 $ 700,000

CGS −300,000 −210,000

Wages −100,000 −100,000

Analysis of Operating Activities 457

PV Beg. Int. Exp. Payment Principal PV End

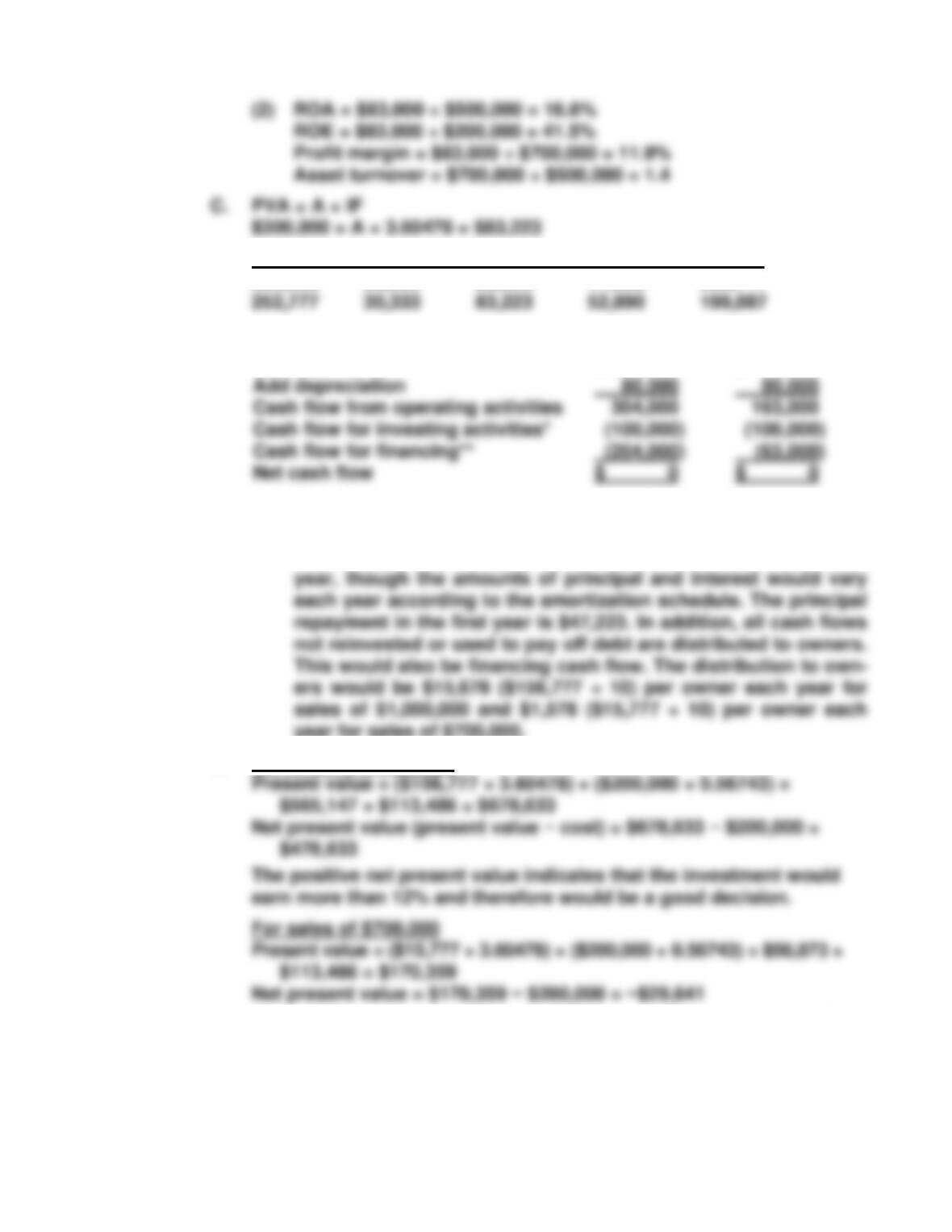

300,000 36,000 83,223 47,223 252,777

D. Cash Flow from Operating Activities

Net income $ 224,000 $ 83,000

* The $100,000 or reinvestment is in the cash flow statement as

investing cash flow.

** Total payments for principal and interest would be $83,223 each

year for sales of $700,000.

E. For sales of $1,000,000

The negative net present value indicates that the investment would

earn less than 12% and therefore would not be a good decision.

(continued)

458 Chapter 14

F. The company’s expected earnings and cash flows are sufficient to

justify the investment. The investment is risky because of the high

potential variability of sales and because of the financial leverage. If