CHAPTER 14

Analysis of Operating Activities

THINKING BEYOND THE QUESTION

How do operations create value for our business?

Good business decisions require reliable and timely information about

business activities. Accounting is the source of much of that information.

QUESTIONS

Q14-1 Generally, in this situation, one would expect that profits would increase

by a rate greater than the increase in sales. Since a large portion of the

Q14-2 Generally, in this situation, one would expect that profits would increase

by about the same rate as the increase in sales. Perhaps marginally fast-

Q14-3 Frankly, no. A product differentiation strategy is typically built around

enhancing the product. By imbuing the product with additional features

or value it is expected that customers will pay more. A successful prod-

424 Chapter 14

Q14-4 In general, one would expect this company to pursue a cost leadership

strategy. The products are identical chemically, and unless the firm can

add value by quicker delivery or in some other way, it is unlikely that

Q14-5 The facts of this situation suggest a classic product differentiation strat-

egy. New products are invented and introduced quickly. Because they are

Q14-6 The cost leadership strategy involves selling products at a low sales

price relative to competitors. The low prices result in low profit margins.

Q14-7 A cost leader must control its costs to permit it to keep its prices low and

still earn a profit. Economies of scale are important. Economies of scale

are achieved when a company can maintain sufficiently high volumes to

take advantage of operating leverage and reduce unit costs. A cost leader

Analysis of Operating Activities 425

Q14-8 The major reason for a price decrease would be the increase in sales vol-

ume that would tend to follow. However, a price decrease will decrease the

Q14-9 Normally, cash flow from operations will be significantly higher than net

income. Although net income is an estimate of the cash that is eventually

to flow because of the period’s operations, net income includes deduc-

tions for noncash expenses such as depreciation and amortization. The

Q14-10 Trends of net income and net cash flow from operations depend on the

length and nature of the operating cycle. Changes in income and cash flow

may occur at about the same time in a company with a short cycle. Cash

flow changes may lag behind income for a company with large, slowly col-

426 Chapter 14

Q14-11 Yes, there probably is a connection between cash flow problems and the

low turnover of both inventory and receivables. Low rates of turnover

Q14-12 The value of stock is the present value of expected future cash flows that

will be derived from it. Growth results in an increase in future cash flows

and, therefore, increases present value. Variability of earnings indicates

Q14-13 Return on assets measures the relationship between net income and total

investment. It reveals the average return on each dollar of assets, regard-

Q14-14 Financing decisions involve the capital structure of a company. They in-

volve the extent to which the company will use debt and equity financing.

This is related to whether financial leverage is used. Investing decisions

involve the type of assets the company will acquire, as well as changes in

Analysis of Operating Activities 427

EXERCISES

E14-2 Strategy

A B C

Unit price $ 7 $ 9 $ 7

Estimated sales in units × 200,000 × 135,000 × 300,000

E14-3 The financial objective here would be to minimize the loss on the concert,

thus minimizing the amount that must be raised through contributions.

The losses would be as follows:

Ticket price $ 12 $ 15 $ 20

E14-4 Unit Price: $100 $125 $160

Estimated sales, in units 200,000 160,000 125,000

428 Chapter 14

E14-5 Company A’s profit margin indicates that it realizes only $0.05 of net in-

come for each $1 of sales it earns. This low profit margin suggests that

Company B seems to be completely different from A. Company B keeps

Company C, according to the profit margin, realizes $0.25 of net income

All companies are equally profitable as measured by their 30% return on

assets.

E14-6 Profit margin, asset turnover, and return on assets are provided below for

Home Depot, Microsoft, and Procter & Gamble.

Home Depot

Microsoft

Procter &

Gamble

Analysis of Operating Activities 429

E14-7 Profit margin, asset turnover, and return on assets are provided below for

Hershey Foods and Wrigley.

Hershey Foods

Wrigley

Profit margin (net income ÷ sales)

13.34%

13.51%

Asset turnover (sales ÷ assets)

1.152

Return on assets (margin × turnover)

15.56%

15.57%

E14-8 Calculation of the components of return on assets will give some clues to

operating strategy.

Pat’s Place:

Henry’s Hangout:

430 Chapter 14

Return on assets is similar for the two restaurants. But Pat’s has a higher

profit margin and lower asset turnover, suggesting a product differentia-

E14-9 Profit margin, asset turnover, and return on assets are provided below for

Southwest and Delta airlines.

Southwest Airlines

Delta Air Lines

2004

2003

2004

2003

Profit margin (net income ÷ sales)

4.79%

7.44%

−34.65%

−5.49%

0.688

Return on assets (margin × turnover)

2.76%

4.47%

−23.84%

−2.98%

E14-10 a.

2008

2007

2006

Profit margin

18.7%

($1,683 ÷ $9,000)

14.2%

($852 ÷ $6,000)

9.6%

($288 ÷ $3,000)

Asset turnover

44.9%

56.3%

81.3%

($3,000 ÷ $3,692)

Average daily cost of

Fixed asset turnover

Analysis of Operating Activities 431

b. The company’s profit margin has almost doubled over the three

years, indicating more emphasis on a product differentiation strate-

E14-11 a.

Fasani Enterprises

Thunderbird

Corporation

2008

2007

2008

2007

b. Fasani is better at generating cash from assets. Net income can be

c. A major difference between net income and cash flow for both firms

is the noncash expenses of depreciation and amortization. In addi-

E14-12 a. Disney’s earnings improved slightly from 2002 to 2003, and signifi-

cantly between 2003 and 2004. Cash flows from operating activities

followed a similar pattern.

(continued)

432 Chapter 14

b. It should not be surprising that differences exist between net earn-

ings and net cash from operating activities. Timing differences be-

E14-13

Federated

Wal-Mart

2004

2003

2004

2003

Inventory turnover

2.98

2.83

7.5

7.3

Accounts receivable turnover

4.573

Gross profit margin

Operating profit margin

E14-14 1. Gross profit margin = Gross profit ÷ Sales revenue

= $25,000 ÷ $50,000

= 50%

Analysis of Operating Activities 433

E14-15 Inventory turnover = Cost of goods sold ÷ Inventory

An increased inventory turnover means that either cost of goods sold

went up or inventory went down. While an increase in cost of goods sold

is an increase in an expense (which is not usually a good thing), it is posi-

Gross profit margin = Gross profit ÷ Operating revenues and

Operating profit margin = Operating income ÷ Operating revenues

If the gross profit margin is high, it reflects the fact that the company is

434 Chapter 14

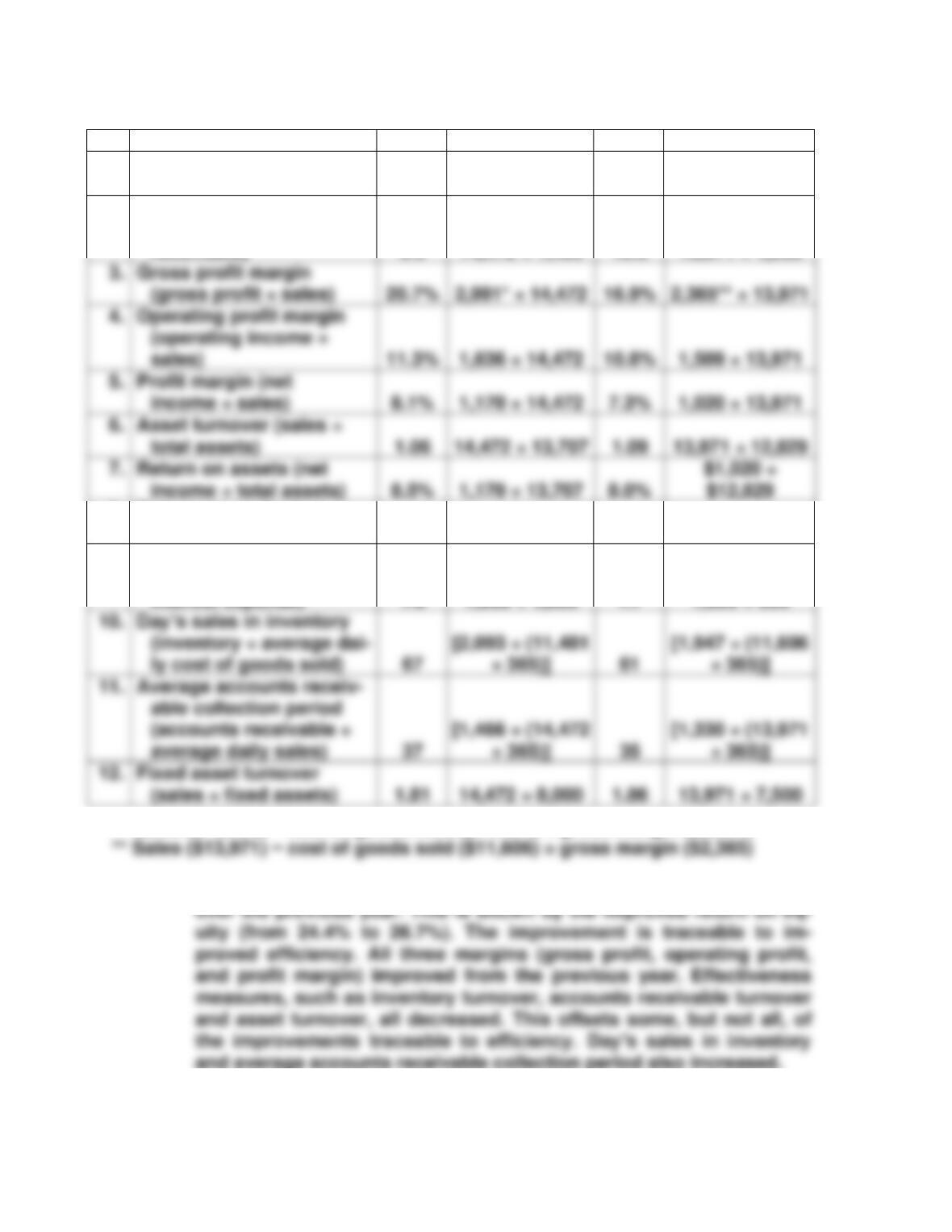

E14-16 a.

Ratio

2008

Calculation

2007

Calculation

1.

Inventory turnover

(CGS ÷ inventory)

5.5

11,481 ÷ 2,093

6.0

11,606 ÷ 1,947

2.

Accounts receivable turn-

over (sales ÷ accounts

receivable)

9.9

14,472 ÷ 1,466

10.5

13,971 ÷ 1,330

8.

Return on equity (net

income ÷ SE)

26.7%

1,170 ÷ 4,386

24.4%

1,020 ÷ 4,180

9.

Times interest earned (in-

come before taxes ÷

interest expense)

1.6

1,636 ÷ 1,000

1.7

1,509 ÷ 900

able collection period

(accounts receivable ÷

average daily sales)

Fixed asset turnover

(sales ÷ fixed assets)

1.81

14,472 ÷ 8,000

1.86

13,971 ÷ 7,500

* Sales ($14,472) − cost of goods sold ($11,481) = gross margin ($2,991)

b. Overall, the company’s financial performance improved somewhat

and average accounts receivable collection period also increased.

E14-17

3.

Gross profit margin

(gross profit ÷ sales)

20.7%

16.9%

2,365** ÷ 13,971

4.

Operating profit margin

(operating income ÷

sales)

11.3%

1,636 ÷ 14,472

10.8%

1,509 ÷ 13,971

5.

Profit margin (net

8.1%

1,170 ÷ 14,472

7.3%

1,020 ÷ 13,971

6.

Asset turnover (sales ÷

1.06

14,472 ÷ 13,707

1.09

7.

Return on assets (net

income ÷ total assets)

8.5%

1,170 ÷ 13,707

8.0%

Analysis of Operating Activities 435

Missing item

Amount

Solution

a.

Accounts

receivable

$1,846

Sales ÷ accts receivable turnover

($10,377 ÷ 5.62)

b.

Inventory

$871

CGS ÷ inventory turnover

($6,226 ÷ 7.15)

c.

Total assets

$6,918

Add together all asset amounts

E14-18 Return on assets: $16,593 ÷ $750,330 = 2.2%

E14-19 a. i. 18.7% ($5,049 ÷ $27,000)

ii. 0.449 ($27,000 ÷ $60,108)

(continued)

$1,050

e.

Total liabilities &

equity

$6,918

Must be same amount as total

g.

Rent expense

$980

Must first determine total ex-

$2,206

Income taxes

$681

Income before taxes × 35%

($1,945 × 35%)

Net income

$1,264

Income before taxes − taxes

k.

Return on equity

Net income ÷ total equity

436 Chapter 14

b. Return Profit Asset Financial

On equity = margin × turnover × leverage

E14-20 a.

McDonald’s

Wendy’s

2004

2003

2004

2003

Profit margin (net income ÷ sales)

0.12

0.09

0.01

0.07

Asset turnover (sales ÷ total assets)

0.68

0.66

1.14

1.01

Return on assets (net income ÷ total assets)

0.08

0.06

0.02

0.08

Financial leverage (total assets ÷ equity)

1.96

2.16

1.86

1.78

Return on equity (net income ÷ equity)

0.16

0.12

0.03

0.13

b. Overall, as measured by size of profits (dollars of net income) and to-

tal assets, McDonald’s is a much larger company. The two compa-

Analysis of Operating Activities 437

E14-21

Attribute

Magnitude

of Attribute

Expected

Company Value

Asset growth

Debt to assets

Dividend payout*

High

Low

Low

High

High

High

E14-22 Accounting Information

c Asset turnover

e Financial leverage

p Growth in assets

E14-23 a. Measurement units—Dollar values are used to measure the elements

(assets, liabilities, equity, revenues, and expenses) listed in the fi-

nancial statements.

438 Chapter 14

c. Accrual basis—Accounts receivable usually stands for revenues that

have been earned and recorded (and therefore accrued) but for

Also note, under GAAP, the recognition of revenues and expenses is

on an accrual basis. Thus, the income statement items all reflect the

accrual basis.

e. Matched—Cost of sales is matched with sales revenue so that the

PROBLEMS

P14-1 A.

Caterpillar

Kellogg

Eli Lilly

Profit margin (net income ÷ sales)

0.07

0.09

0.13

Asset turnover (sales ÷ total assets)

0.70

0.89

0.56

Return on assets (net income ÷ total assets)

0.05

0.08

0.07

Return on equity (net income ÷ equity)

0.27

0.39

0.17

Leverage

5.77

4.78

2.28

B. Caterpillar, Kellogg, and Eli Lilly are in three very different industries.

P14-2 A. Profit margin (net income ÷ operating revenues)

Colony: $180 ÷ 1,360 = 13.2%

Analysis of Operating Activities 439

Fixed asset turnover (operating revenues ÷ fixed assets)

Colony: $1,360 ÷ 1,400 = 0.97

Vernon: 9.0% × 1.05 = 9.5%

B. Colony appears to charge higher prices for its products than Vernon.

It earns more for each dollar of sales (13.2¢ for Colony versus 9¢ for

Colony earns a higher net income than Vernon, but each company

earns the same return on assets. Therefore, neither company is more

C. Revenues, expenses, and assets determine the return on assets.

Revenues depend on sales price and volume sold. There are two

ways to increase revenues (and increase effectiveness): (1) raise

440 Chapter 14

P14-3 A. Strategy

1 2 3

Selling price per case $ 29.00 $ 31.00 $ 34.00

Estimated monthly sales (cases) × 11,000 × 12,000 × 7,500

B. Long Life Pricing and Operating Strategy

By (student name)

Long Life is evaluating three possible selling strategies for its cereal:

1. Selling to supermarkets at $29 per case and spending a minimum

The average case of competitors’ cereals of the size we will sell is

priced at $30 to grocery stores. Thus, the first option is based on

cost leadership; our very healthy cereal would be priced slightly be-