Chapter 14 Long-Term Liabilities: Bonds and Notes 277

Group Learning Activity—Installment Notes

Ask your students to work in groups to determine the annual payment given the following conditions:

Principal amount: $30,000

Annual interest rate: 5%

Term: 3 years

Then, as an option, you can have them create an amortization schedule like the one in Exhibit 3. The

solution can be found in TM 14-14.

OBJECTIVE 5

Describe and illustrate the reporting of long-term liabilities, including bonds and notes

payable.

SYNOPSIS

Bonds payable and notes payable are reported as liabilities on the balance sheet. Any portion of these

debts that is due within one year is reported as a current liability and the remaining portion is reported as a

long-term liability. The bonds are reported at their carrying or book value. A description of the debt

should be reported in the accompanying notes.

SUGGESTED APPROACH

Use the following notes to review the presentation of bonds payable and notes payable. Refer your

students to page 656, Mornin’ Joe balance sheet presentation for liabilities, in the text for an example of a

consolidated balance sheet that illustrates many of the accounting practices covered in Chapters 7–14.

LECTURE AID—Balance Sheet Presentation of Bonds Payable and Notes

Payable

Ask your students where bonds payable and notes payable are reported on a balance sheet. Unless bonds

and/or notes are due to mature within the next year, they are listed in the Long-Term Liabilities section of

the balance sheet.

Next, ask students to write in their notes how a $100,000 bond with a $7,000 unamortized discount and

notes payable of $12,000 should appear on the balance sheet of the issuing company. After a minute,

review the following solution with your students:

Long-term liabilities:

Bond payable $100,000

Less discount 7,000

$ 93,000

Notes payable 12,000

Total long-term liabilities $105,000

278 Chapter 14 Long-Term Liabilities: Bonds and Notes

Remind your students that a premium is added to the bond payable account and that a description of the

bonds and notes should also be reported either on the face of the financial statements or in the

accompanying notes.

OBJECTIVE 6

Describe and illustrate how the number of times interest charges are earned is used to

evaluate a company’s financial condition.

SYNOPSIS

As creditors, bondholders are concerned with the company’s ability to pay its interest payments and repay

the maturity value of the bonds. Analysts assess this risk by calculating the number of times interest

charges are earned ratio. It is computed as: number of times interest charges are earned = (income before

income tax + interest expense)/interest expense. This ratio tells the number of times interest payments

could be paid out of current period earnings. This measures the company’s ability to pay its interest

payments.

Key Terms and Definitions

• Number of Times Interest Charges Are Earned – A ratio that measures creditor margin of

safety for interest payments, calculated as income before interest and taxes divided by interest

expense.

Relevant Example Exercises and Exhibits

• Example Exercise 14-9 Number of Times Interest Charges Are Earned

SUGGESTED APPROACH

The number of times interest charges are earned compares the “pool” of money available for interest

payments to a company’s interest expense. The larger the “pool,” the easier it is for a company to meet its

interest payments. The group learning activity below will help your students master this concept.

GROUP LEARNING ACTIVITY—Number of Times Interest Charges Earned

TM 14-16 lists revenue and expense data for Bates Corporation. Ask your students, working in small

groups, to compute the amount of funds available to pay interest charges. The correct answer is $10,000.

This amount is obtained by subtracting the operating expenses from the revenues. If any of your groups

answer $6,000, they have deducted income taxes. Point out that interest is a tax–deductible expense;

therefore, it is paid out of before-tax earnings. Bates’s income before taxes is $9,000.

Chapter 14 Long-Term Liabilities: Bonds and Notes 279

Next, present the formula for number of times interest charges earned:

Income Before Income Tax + Interest Expense

Interest expense

Ask your students to calculate Bates’s number of times interest charges earned. The answer is:

$9,000 + $1,000 $10,000

Number of Times Interest Charges Earned = = = 10

$1,000 $1,000

The funds available to pay interest are ten times larger than the required interest payments. Remind your

students that the number of times interest charges are earned should be compared to prior years’ data and

industry averages for a thorough assessment. A number of times interest charges are earned of ten seems

to be adequate, but if that ratio has been steadily declining or is below the ratio for other companies in the

same industry, investors could become concerned.

APPENDIX 1—PRESENT VALUE CONCEPTS

AND PRICING BONDS PAYABLE

SYNOPSIS

Investors consider many factors when deciding what they are willing to pay for a bond. Face value,

interest, and market rate of interest are all considered. The investor may also consider the present value of

the bonds’ future cash receipts. This concept is based on the time value of money. To illustrate the present

value concept, consider that $1,000 is to be received in one year. If the market rate of interest is 10%, the

present value of that $1,000 would be $909.09 ($1,000/1.10). Exhibits 8 and 10 can be used to find the

present value of $1 and the present value of an annuity of $1 at compound interest rates. The selling price

of a bond is the sum of the present values of the face value of the bonds due at the maturity date and the

periodic interest due on the bonds. The selling price of the bond varies with the present value of the

bond’s face value at maturity, interest payments, and the market interest rate.

Key Terms and Definitions

• Annuity – A series of equal cash flows at fixed intervals.

• Future Value – The value of an asset or cash at a specified date in the future that is equivalent in

value to a specified sum today.

• Present Value – Cash to be received (or paid) in the future is not the equivalent of the same

amount of money received at an earlier date.

• Present Value of an Annuity – The sum of the present values of a series of equal cash flows to

be received at fixed intervals.

280 Chapter 14 Long-Term Liabilities: Bonds and Notes

Relevant Example Exercises and Exhibits

• Exhibit 5 – Present Value and Future Value

• Exhibit 6 – Present Value of an Amount to Be Received in One Year

• Exhibit 7 – Present Value of an Amount to Be Received in Two Years

• Exhibit 8 – Present Value of $1 at Compound Interest

• Exhibit 9 – Present Value of an Annuity

• Exhibit 10 – Present Value of an Annuity of $1 at Compound Interest

SUGGESTED APPROACH—Computation of Present Value of Bonds

Payable

This introduces students to present value concepts used to price bonds. This concept is new to most

accounting principles students, and many find it very difficult. Therefore, you may want to spend time

discussing present value in general before applying this concept to bonds.

A series of questions follow, which you can ask your class to lead into a discussion of present value.

Several Demonstration Problems showing the use of present value outside the area of bonds are also

presented. To give your students a chance to practice these concepts, assign Handout 14-1 as a group

learning activity or as homework.

This process can be overwhelming to some students, but when broken down to a simple four-step process,

it becomes manageable. The four-step process is as follows:

1. Calculate the present value of the lump sum (face value of the bond). Point out that students should

use the market rate of interest for this calculation

2. Calculate the interest payment. Use the bond interest rate for this calculation

3. Calculate the present value of the annuity (interest payment calculated in step 2). Again, use the

market rate of interest for this calculation

4. Add the PV of the lump sum (step 1) to the PV of the annuity (step 3). The results will be the present

value of the bond.

LECTURE AID—Introduction to Present Value

Present the following scenario to your class:

If I told you that I would give you $100 today or $100 one year from now, how many of

you would want the money today? What if I told you that I would give you $100 today or

$105 one year from now? How many of you would wait one year to get an extra $5? If I

offered to pay $110 one year from now, how many would wait one year for an extra $10?

What about $125 in one year? What about $150 in one year?

Ask a student who did not raise a hand when you offered $105 why he or she was not willing to wait one

year for the extra $5. Next, ask a student who did raise a hand when you offered $125 or $150 why he or

she was willing to wait one year to receive an extra $25 or $50.

Chapter 14 Long-Term Liabilities: Bonds and Notes 281

Your students’ comments should provide a good lead-in to a discussion of time value of money.

DEMONSTRATION PROBLEM—Present Value of a Single Sum

One hundred dollars today is more valuable than $100 in the future. You can invest the $100 you have

today and end up with more than $100 in the future.

Ask your students to calculate how much money they would have in one year if they invested $100 and

earned 7 percent interest on their money. (Answer: $107)

Look at this same concept from the reverse perspective. How much money do you need to invest today to

have $100 in one year if interest rates are 7 percent? Show your students how to solve this problem with

an algebraic equation.

Let X = $ to be invested today

X + 0.07X = $100

1.07X = $100

X = $100/1.07

X = $93.46

$93.46 is the present value of receiving $100 in one year if interest rates are 7 percent.

Next, ask your students to write down the equation to determine how much they would need to invest to

have $100 in two years, assuming a 7 percent interest rate. After a minute, show them the correct formula.

X + 0.07X = 1.07X (what you will have at the end of year 1)

1.07X + 0.07(1.07X) = 1.1449X (the amount at the end of year 2)

Therefore,

1.145X = $100

X = $87.34

This calculation gets fairly complex after just two years because of the compounding of interest. Present

value tables, such as the one in Exhibit 4 in the text, were developed as a shortcut. To calculate the

amount needed today to accumulate $100 in two years at 7 percent, the present value factor from the table

for two periods at 7 percent is multiplied by $100.

$100 0.87344 = $87.34

Ask your students to use the table to find the present value of receiving $100,000 ten years from now at 7

percent.

$100,000 0.50835 = $50,835

282 Chapter 14 Long-Term Liabilities: Bonds and Notes

In simple terms, this means that $50,835 invested at 7 percent will grow to $100,000 in ten years.

Finally, ask your students to answer the following question (TM 14-8):

Assume that you have a rich uncle who dies. In his will, he leaves you with the following

option: You can have $100,000 today or $200,000 in ten years. Interest rates are 10

percent. Which should you choose?

$200,000 0.38554 = $77,108

$100,000 > $77,108, so take the $100,000 now

DEMONSTRATION PROBLEM—Present Value of an Annuity

Begin by defining an annuity. An annuity is a series of equal payments at equal intervals (for example,

$100 per year for five years). Ask students for examples of annuities. Examples include insurance and

pension annuities.

Demonstrate the need to calculate the present value of an annuity through the following scenario:

Assume that you have won a sweepstakes with a $5 million grand prize. Now you have to choose how to

take your winnings: $500,000 per year for ten years or $3 million now. If interest rates are 11 percent,

which would you choose?

To solve this problem, you need to compare the $3 million that could be yours today with what receiving

the money over ten years is worth today. In other words, you need to compute the present value of an

annuity using the table in text Exhibit 5.

To calculate the present value of an annuity:

Annuity Amount Factor from PV Table for Annuities (Exhibit 5)

$500,000 5.88923 = $2,944,615

$3,000,000 > $2,944,615, so take the $3 million today

Next, ask your students to determine whether they would want the sweepstakes prize today or over ten

years if they could earn only 6 percent interest on investments.

$500,000 7.36009 = $3,680,045

$3,000,000 < $3,680,045, so take payments over ten years

GROUP LEARNING ACTIVITY—Present Value of an Annuity

TM 14-9 contains additional annuity problems to be solved with present value concepts. One of these

problems requires students to use present value interest factors for a 20-year period. These factors can be

found in the expanded present value tables included in Appendix A of the text.

Chapter 14 Long-Term Liabilities: Bonds and Notes 283

Ask your students to solve the present value problems in small groups. TM 14-10 presents the solutions.

LECTURE AID—Pricing Bonds

The selling price of a bond is determined by the relationship between the bond’s contract interest rate and

the market interest rate when the bond is sold.

If contract rate = market rate, bond sells at face value.

If contract rate > market rate, bond sells at a premium.

If contract rate < market rate, bond sells at a discount.

When determining the present value of a bond, the following two components must be viewed separately:

1. Principal, repaid when bond matures (a single payment). Use Exhibit 4 to determine the present

value.

2. Interest payments, usually made semiannually (an annuity). Use Exhibit 5 to determine the present

value.

APPENDIX 2—EFFECTIVE INTEREST RATE

METHOD OF AMORTIZATION

SYNOPSIS

The effective interest rate method provides a constant rate of interest over the life of the bond as opposed

to the straight-line method that provides a constant amount of interest expense each period. You may use

the chart in Exhibit 11 to figure the interest expense for each period for bonds sold at a discount. Exhibit

12 shows the varying interest expense for a bond issued at a premium.

Relevant Example Exercises and Exhibits

• Exhibit 11 – Amortization of Discount on Bonds Payable

• Exhibit 12 – Amortization of Premium on Bonds Payable

Two Demonstration Problems to help you introduce effective interest amortization are provided below.

Stress that this method reports a constant rate of interest. Interest expense reported on the income

statement is always the same percentage of the beginning carrying value of any bonds. That percentage is

the market rate of interest on the date bonds were issued.

284 Chapter 14 Long-Term Liabilities: Bonds and Notes

The following comparison of the straight-line and effective interest amortization methods will help your

students distinguish between the two methods:

Straight-Line Method Constant Amount of Interest

Effective Interest Rate Method Constant Rate of Interest

Stress that the effective interest method of amortization is required by generally accepted accounting

principles. The straight-line method can be used only if the results are not materially different from the

effective interest method.

DEMONSTRATION PROBLEM—Amortizing a Bond Discount Using the

Effective Interest Method

The easiest way to amortize a bond discount correctly is to set up an amortization table with the following

headings:

Interest Interest

Paid Expense Bond

Interest (based on the (based on the Discount Unamortized Carrying

Payment contract rate) market rate) Amortization Discount Amount

For example, assume a $100,000, two-year, 11 percent bond that makes semiannual interest payments is

sold for $96,574 when the market interest rate is 13 percent. Prepare an amortization table for your

students illustrating all four interest payments. Show each calculation as you step through this table. In

addition, make the journal entries to record the first two interest payments.

5.5% 6.5% Bond

Interest Interest Interest Discount Unamortized Carrying

Payment Paid Expense Amortization Discount Amount

3,426 96,574

1 5,500 6,277 777 2,649 97,351

2 5,500 6,328 828 1,821 98,179

3 5,500 6,382 882 939 99,061

4 5,500 6,439 939 0 100,000

Journal entries:

1st payment: Interest Expense………………………… 6,277

Discount on Bonds Payable…….. 777

Cash…………………………….. 5,500

2nd payment: Interest Expense………………………… 6,328

Discount on Bonds Payable…….. 828

Cash…………………………….. 5,500

Your students may find the following hints helpful:

Chapter 14 Long-Term Liabilities: Bonds and Notes 285

1. Write the interest rate used to determine the interest expense above the column. For a bond that pays

interest semiannually, this will be one-half the effective interest rate.

2. When amortizing a discount, make sure that the carrying value of the bond increases after each

interest payment. The carrying value must be raised up to the face value by the last interest payment.

3. When recording the last interest payment, any remaining discount must be amortized.

Point out that interest expense reported on the income statement increases each year as you amortize the

bond discount. This occurs because the bond’s carrying value is increasing. You may also want to

illustrate the journal entry to repay the bond at maturity:

Bonds Payable………………………………………. 100,000

Cash ………………………………………… 100,000

There is no entry to the Discount on Bonds Payable account because it has been amortized to zero.

DEMONSTRATION PROBLEM—Amortizing a Bond Premium

The easiest way to amortize a bond premium correctly is to set up an amortization table with the

following headings:

Interest Interest

Paid Expense Bond

Interest (based on the (based on the Premium Unamortized Carrying

Payment contract rate) market rate) Amortization Premium Amount

For example, assume a $250,000, three-year, 13 percent bond that makes semiannual interest payments is

sold for $269,035 when the market interest rate is 10 percent. Start the following amortization table by

computing the premium amortized with the first two interest payments. Also, make the journal entries to

record the first two interest payments. Ask your students to complete the amortization table on their own.

6.5% 5% Bond

Interest Interest Interest Premium Unamortized Carrying

Payment Paid Expense Amortization Premium Amount

19,035 269,035

1 16,250 13,452 2,798 16,237 266,237

2 16,250 13,312 2,938 13,299 263,299

3 16,250 13,165 3,085 10,214 260,214

4 16,250 13,011 3,239 6,975 256,975

5 16,250 12,849 3,401 3,574 253,574

6 16,250 12,676 3,574 0 250,000

Journal entries:

1st payment: Interest Expense…………………… 13,452

Premium on Bonds Payable……….. 2,798

Cash……………………….. 16,250

286 Chapter 14 Long-Term Liabilities: Bonds and Notes

2nd payment: Interest Expense…………………… 13,312

Premium on Bonds Payable……….. 2,938

Cash……………………….. 16,250

When amortizing a premium, stress that the carrying value of a bond must decrease after each interest

payment. This will drive the carrying value down to the bond’s face value. The amount of interest

expense reported on the income statement decreases each year as the premium is amortized. The interest

expense is driven downward because the bond’s carrying value is decreased each year.

Handout 14-1

PRESENT-VALUE PROBLEMS

1. Compute the present value of $80,000, to be received in ten years, if the interest rate is 12

percent.

2. You’ve just accepted a contract to provide services for a client for seven years at a fee of

$6,000 per year. Find the present value of this contract, assuming that interest rates are 11

percent.

3. Ellen Saber is contemplating paying several years’ rent on her business office in advance.

By paying in advance, she can avoid a rent increase that goes into effect the first of next

year. Ellen’s rent payment is $4,800 per year. Calculate the sum that Ellen would have to

pay now in order to prepay five years of rent. Interest rates are 7 percent.

4. Craig Jones owns a computer sales and repair business. He has decided to sell maintenance

contracts with new computers that cover all repairs needed within three years of purchase.

On average, each new computer needs $100 in repairs and maintenance per year during the

first three years it is operated. (The $100 is the customer’s cost for maintenance, including

parts, labor, and Craig’s profit.) How much should Craig charge for a maintenance contract

if interest rates are 13 percent?

5. You have just won the Florida lottery, and the jackpot was $10 million! Your first major

decision is how to take your prize winnings. You can choose $1 million a year for ten years

or $5.65 million now. Which would you choose if you believe you can earn 10 percent

interest on money you invest?

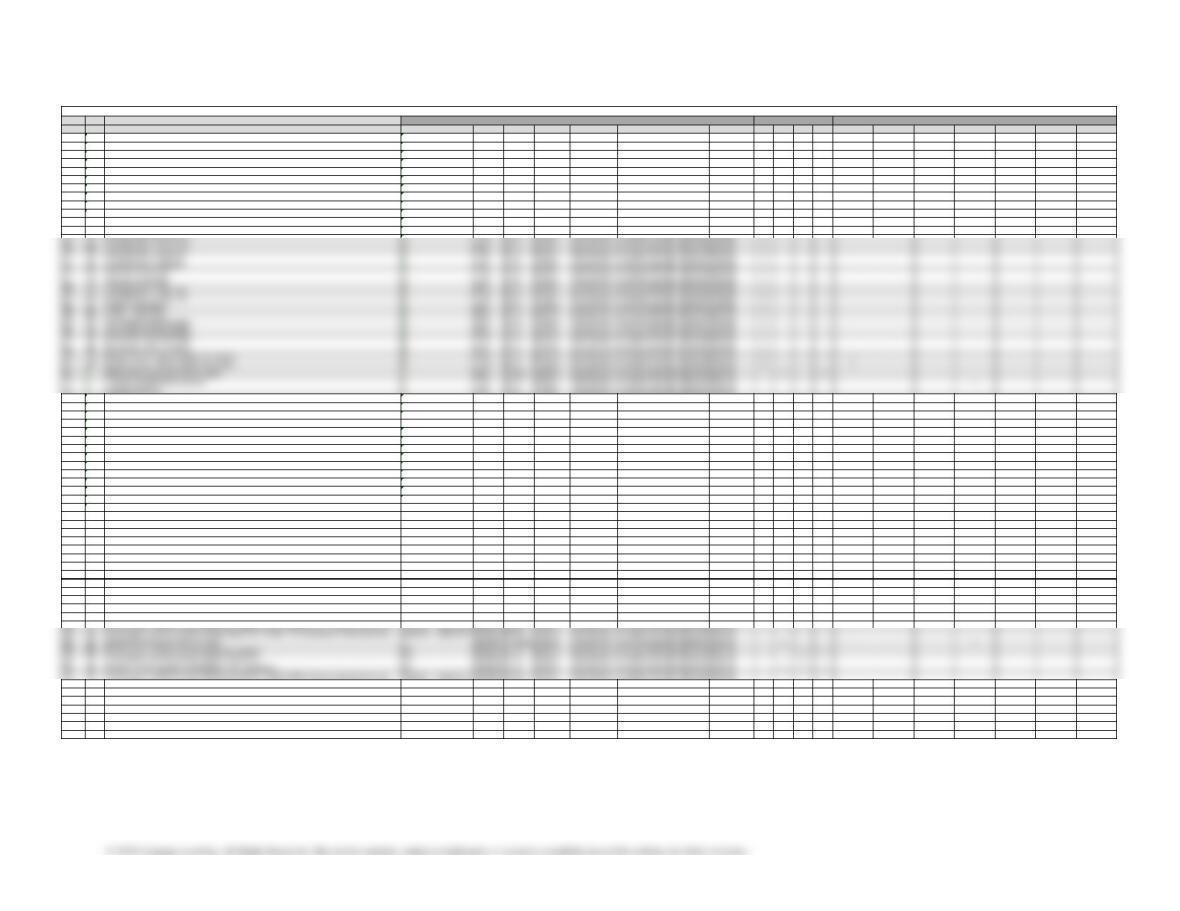

Type Item Description LO(s) Difficulty Time Est BUSPROG AICPA ACBSP – APC Bloom’s EE Excel GL SMH FAI Service Real World Writing Ethics Internet Group

DQ 1 2 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Remembering

DQ 2 2 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Remembering

DQ 3 2 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Remembering

DQ 4 2 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Remembering

DQ 5 2 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Remembering

DQ 6 2 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Remembering

DQ 7 3 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Remembering

DQ 8 3 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Remembering

DQ 9 3 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Remembering

DQ 10 4 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Remembering

PE 1A Alternative financing plans 1 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Applying x

PE 1B Alternative financing plans 1 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Applying x

EX 4 Bond price 3 Easy 10 min. Analytic Measurement Long-term Liabilities Reporting Applying x

EX 5 Entries for issuing bonds 3 Easy 10 min. Analytic Measurement Long-term Liabilities Reporting Applying x

EX 6 Entries for issuing bonds and amortizing discount by straight-line method 3 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Applying x

EX 7 Entries for issuing bonds and amortizing premium by straight-line method 2,3 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Applying x

EX 8 Entries for issuing and calling bonds; loss 3 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Applying x

EX 9 Entries for issuing and calling bonds; gain 3 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Applying x

EX 10 Entries for installment note transactions 4 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Applying x

EX 11 Entries for installment note transactions 4 Easy 10 min. Analytic Measurement Long-term Liabilities Reporting Applying x

EX 12 Entries for installment note transactions 4 Easy 15 min. Analytic Measurement Long-term Liabilities Reporting Applying x x

EX 13 Reporting bonds 5 Easy 10 min. Analytic Measurement Long-term Liabilities Reporting Applying x x

EX 14 Number of times interest charges are earned 6 Easy 10 min. Analytic Measurement Long-term Liabilities Reporting Applying x x

EX 15 Number of times interest charges are earned 6 Easy 10 min. Analytic Measurement Long-term Liabilities Reporting Applying x x

EX 16 Number of times interest charges are earned 6 Easy 10 min. Analytic Measurement Long-term Liabilities Reporting Applying x x

EX 17 Present value of amounts due Appendix 1 Easy 15 min. Analytic Measurement Long-term Liabilities Reporting Applying

EX 18 Present value of annuity Appendix 1 Moderate 15 min. Analytic Measurement Long-term Liabilities Reporting Applying

EX 19 Present value of annuity Appendix 1 Moderate 15 min. Analytic Measurement Long-term Liabilities Reporting Applying

EX 20 Present value of annuity Appendix 1 Moderate 15 min. Analytic Measurement Long-term Liabilities Reporting Applying x

EX 21 Present value of bonds payable; discount Appendix 1 Moderate 15 min. Analytic Measurement Long-term Liabilities Reporting Applying

EX 22 Present value of bonds payable; premium Appendix 1 Moderate 15 min. Analytic Measurement Long-term Liabilities Reporting Applying

EX 23 Amortize discount by interest method Appendix 2 Moderate 15 min. Analytic Measurement Long-term Liabilities Reporting Applying

EX 24 Amortize premium by interest method Appendix 2 Moderate 15 min. Analytic Measurement Long-term Liabilities Reporting Applying

EX 25 Compute bond proceeds, amortizing premium by interest method, and interest expense Appendix 1; Appendix 2 Moderate 15 min. Analytic Measurement Long-term Liabilities Reporting Applying

EX 26 Compute bond proceeds, amortizing premium by interest method, and interest expense Appendix 1; Appendix 2 Moderate 15 min. Analytic Measurement Long-term Liabilities Reporting Applying

PR 1A Effect of financing on earnings per share 1 Moderate 1.5 hours Analytic Measurement Long-term Liabilities Reporting Applying x x

PR 2A Bond discount, entries for bonds payable transactions 2,3 Moderate 1 hour Analytic Measurement Long-term Liabilities Reporting Applying x x

PR 3A Bond premium entries for bonds payable transactions 2,3 Moderate 1 hour Analytic Measurement Long-term Liabilities Reporting Applying x

PR 4A Entries for bonds payable and installment note transactions 3.4 Moderate 1 hour Analytic Measurement Long-term Liabilities Reporting Applying x x x

PR 6B Bond premium, entries for bonds payable transactions, interest method of amortizing bond premium Appendix 1; Appendix 2 Moderate 45 min. Analytic Measurement Long-term Liabilities Reporting Applying

CP 1 General Electric bond issuance 2 Easy 5 min. Ethics Industry Long-term Liabilities Reporting Analyzing x

CP 2 Ethics and professional conduct in business 2 Easy 5 min. Ethics Industry Long-term Liabilities Reporting Analyzing x

CP 3 Present values 2 Easy 10 min. Analytic Measurement Long-term Liabilities Reporting Applying x

CP 4 Preferred stock vs. bonds 1 Easy 5 min. Analytic Measurement Long-term Liabilities Reporting Understanding x

CP 5 Financing business expansion 2 Moderate 30 min. Analytic Measurement Long-term Liabilities Reporting Applying x

CP 6 Number of times interest charges are earned 6 Moderate 10 min. Analytic Measurement Long-term Liabilities Reporting Applying x

HOMEWORK CHART WITH LEARNING OUTCOMES TAGGING

TAGGING

RESOURCES

FOCUS