843

Problem 14-9AB (Concluded)

Part 3

2017

June 30

Bond Interest Expense …………………………..

7,660

Premium on Bonds Payable …………………………..

2017

Dec. 31

Bond Interest Expense …………………………..

7,646

Premium on Bonds Payable …………………………..

Part 4

As of December 31, 2019

Cash Flow

Table

Table Value*

Amount

Present Value

Par value …………………

B.1

0.8885

$250,000

$222,125

B.3

3.7171

Comparison to Part 2 Table

This present value ($252,326) equals the carrying value of the bonds in

844

Problem 14-10AB (60 minutes)

Part 1

2017

Jan. 1

Cash ……………………………………………………….

184,566

Part 2

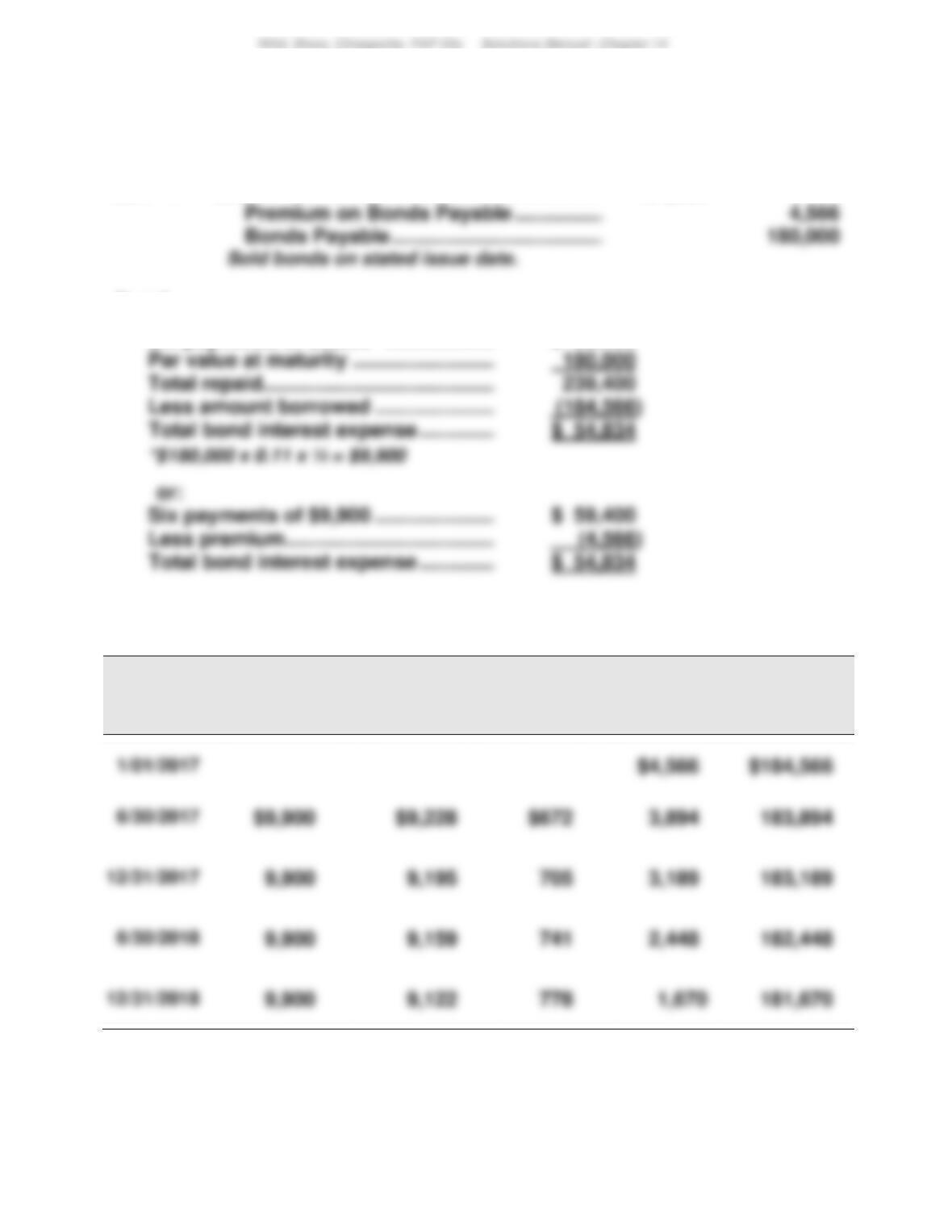

Six payments of $9,900* ………………………

$ 59,400

Par value at maturity …………………………..

Less amount borrowed ………………………..

Six payments of $9,900 ………………………..

$ 59,400

Less premium………………………………………

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[5.5% x $180,000]

(B)

Bond Interest

Expense

[5% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$180,000 + (D)]

845

Problem 14-10AB (Concluded)

Part 4

2017

June 30

Bond Interest Expense …………………………..

9,228

Premium on Bonds Payable …………………………..

2017

Dec. 31

Bond Interest Expense …………………………..

9,195

Premium on Bonds Payable …………………………..

Part 5

2019

Jan. 1

Bonds Payable ……………………………………………………..

180,000

Premium on Bonds Payable …………………………..

1,670

Part 6

If the market rate on the issue date had been 12% instead of 10%, the bonds

would have sold at a discount because the contract rate of 11% would have been

lower than the market rate.

This change would affect the balance sheet because the bond liability would be

smaller (par value minus a discount instead of par value plus a premium). As the

846

Problem 14-11AD (35 minutes)

Part 1

Part 2

Part 3

Capital Lease Liability Payment (Amortization) Schedule

Period

Ending

Date

Beginning

Balance of

Lease

Liability

Interest on

Lease

Liability

(8%)

Reduction

of Lease

Liability

Cash

Lease

Payment

Ending

Balance of

Lease

Liability

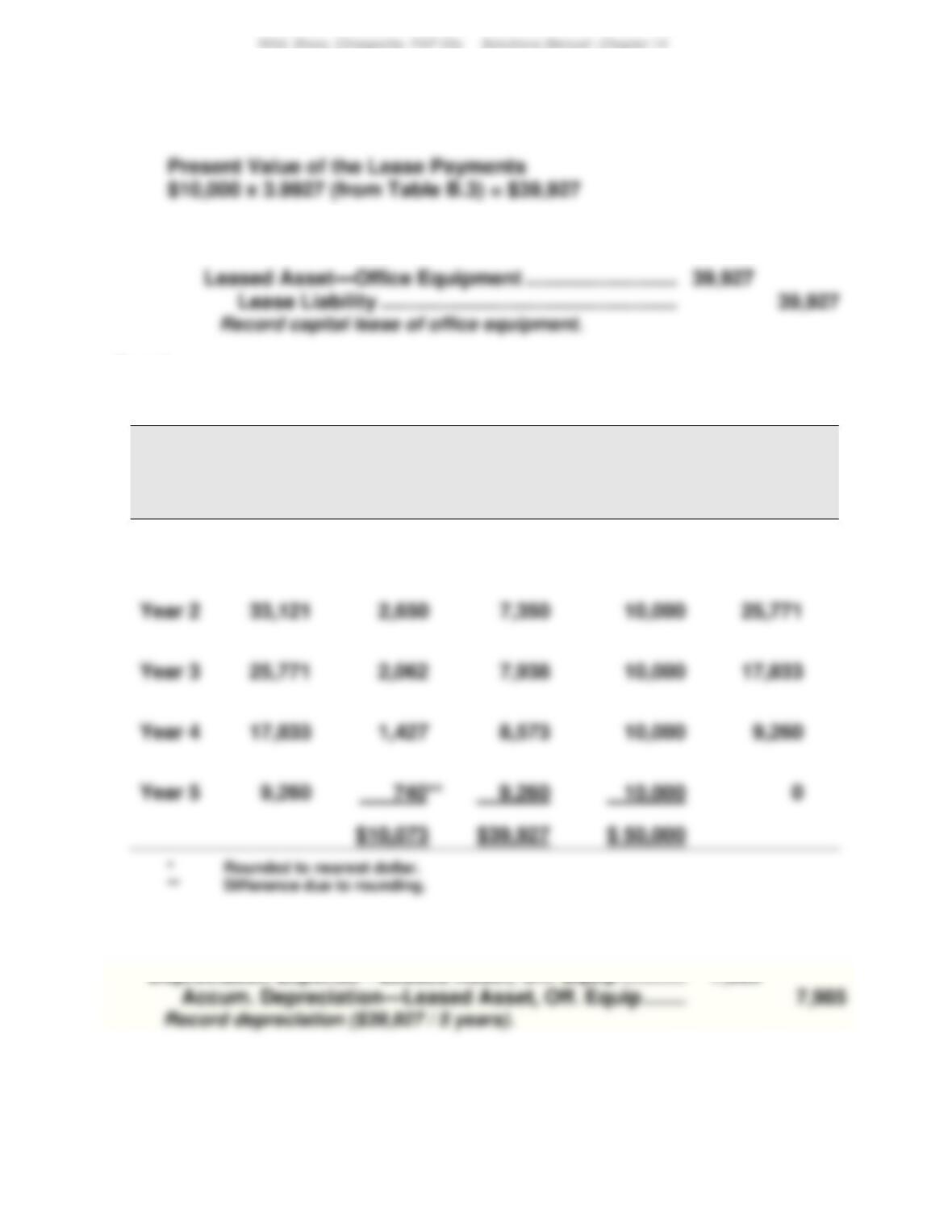

Year 1

$39,927

$ 3,194*

$ 6,806

$ 10,000

$33,121

Year 3

Year 5

Part 4

Depreciation Expense—Leased Asset, Off. Equip ……………….

7,985

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 14

847

PROBLEM SET B

Problem 14-1B (50 minutes)

Part 1

a.

Cash Flow

Table

Table Value*

Amount

Present Value

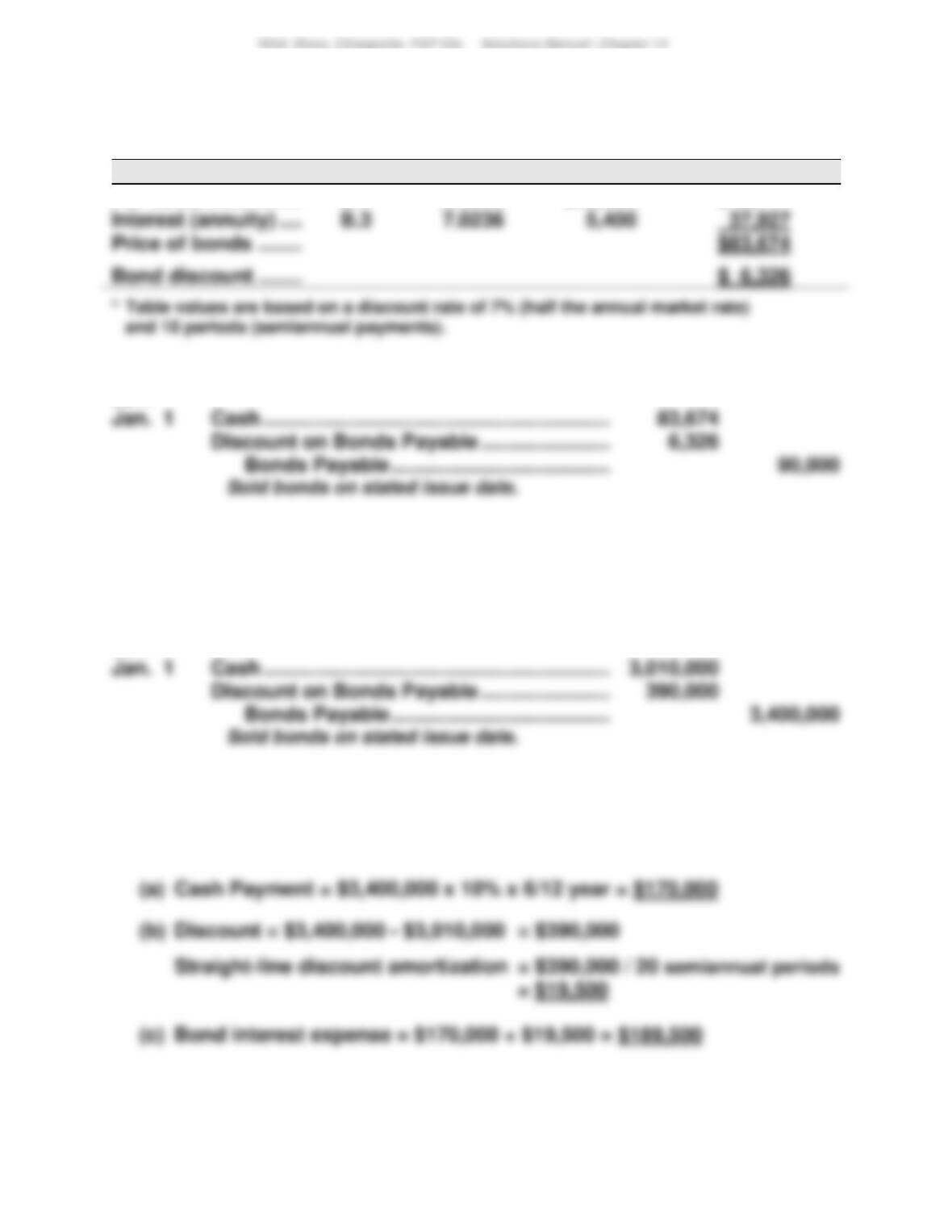

Par value ……………..

B.1

0.6139

$90,000

$55,251

b.

2017

Part 2

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value ……………..

B.1

0.5584

$90,000

$50,256

B.3

7.3601

b.

2017

B.3

7.7217

848

Problem 14-1B (Concluded)

Part 3

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value ……………..

B.1

0.5083

$90,000

$45,747

B.3

7.0236

$83,674

b.

2017

Problem 14-2B (40 minutes)

Part 1

2017

Part 2

[Note: The semiannual amounts for (a), (b), and (c) below are the same throughout

the bonds’ life because the company uses straight-line amortization.]

Problem 14-2B (Concluded)

Part 3

Twenty payments of $170,000 ………………

$3,400,000

Par value at maturity …………………………..

Total repaid ………………………………………….

Less amount borrowed ………………………..

Twenty payments of $170,000 ……………..

$3,400,000

Part 4 (Semiannual amortization: $390,000/20 = $19,500)

Semiannual

Period-End

Unamortized

Discount

Carrying

Value

1/01/2017 …………………

$390,000

$3,010,000

312,000

Part 5

2017

850

Problem 14-3B (40 minutes)

Part 1

2017

Jan. 1

Cash ……………………………………………………….

4,192,932

Part 2

Part 3

851

Problem 14-3B (Concluded)

Part 4

Semiannual

Period-End

Unamortized

Premium

Carrying

Value

1/01/2017 …………………

$792,932

$4,192,932

634,344

Part 5

2017

2017

852

Problem 14-4B (45 minutes)

Part 1

Part 2

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2017

$12,988

$332,988

853

Problem 14-4B (Concluded)

Part 3

2017

June 30

Bond Interest Expense …………………………..

13,101

2017

Dec. 31

Bond Interest Expense …………………………..

13,101

854

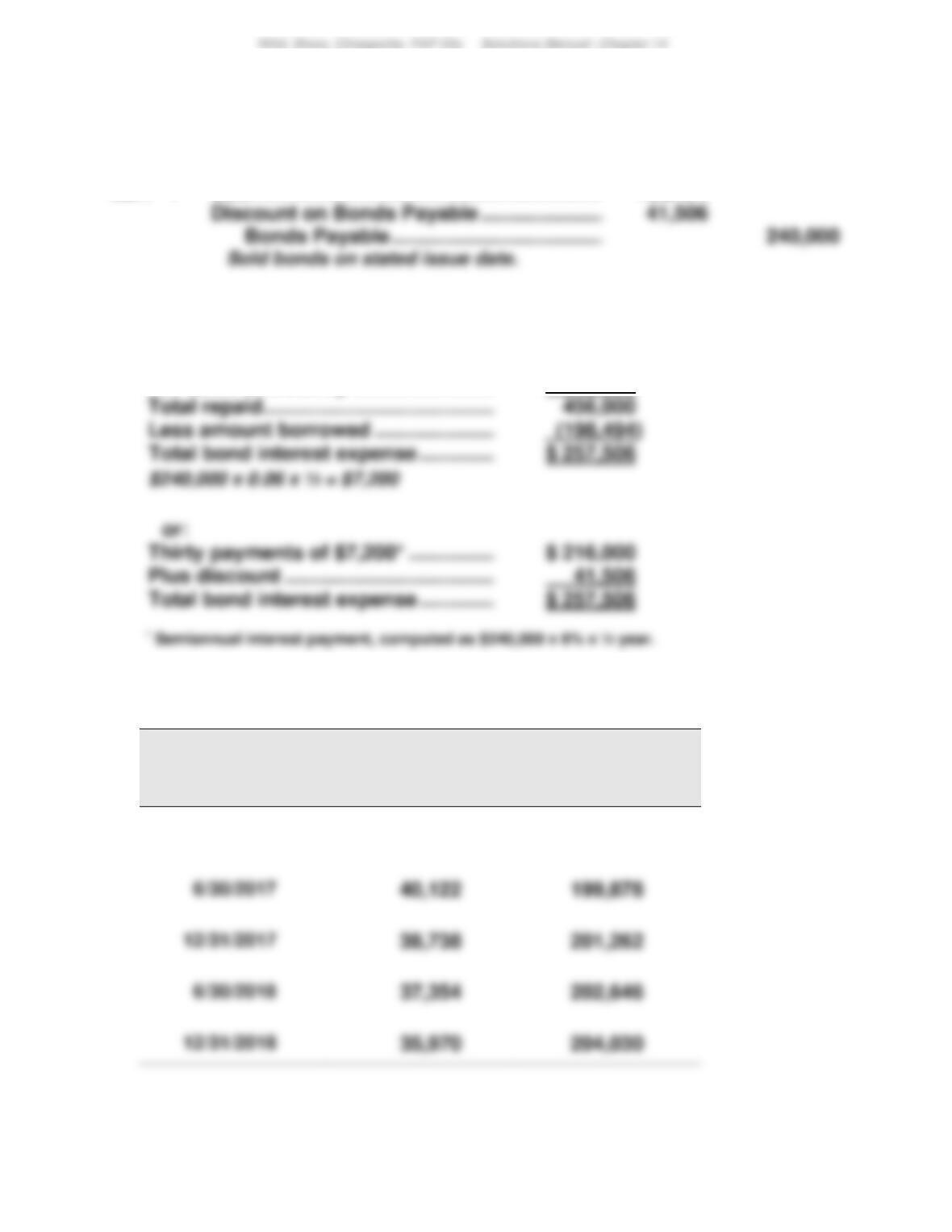

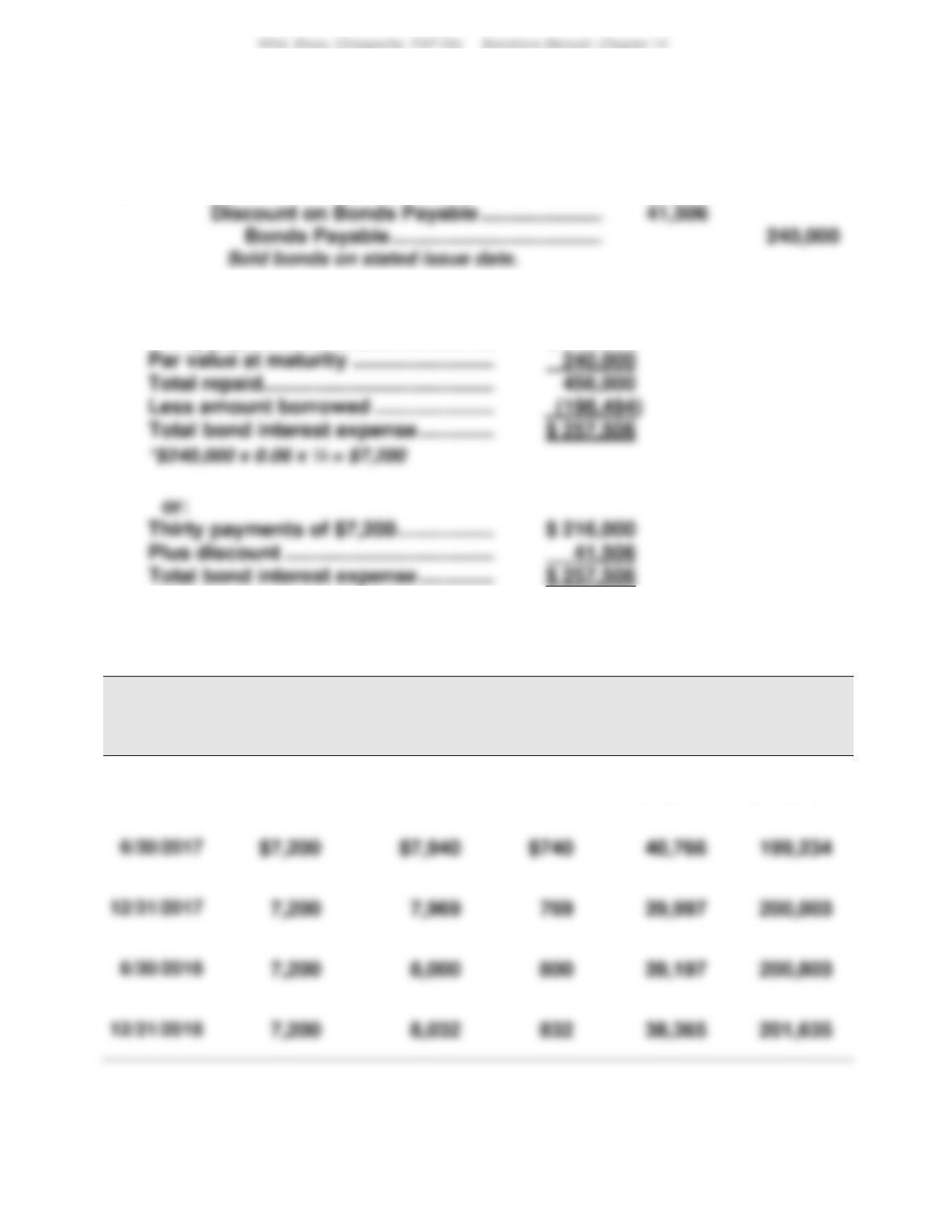

Problem 14-5B (60 minutes)

Part 1

2017

Jan. 1

Cash ……………………………………………………….

198,494

Part 2

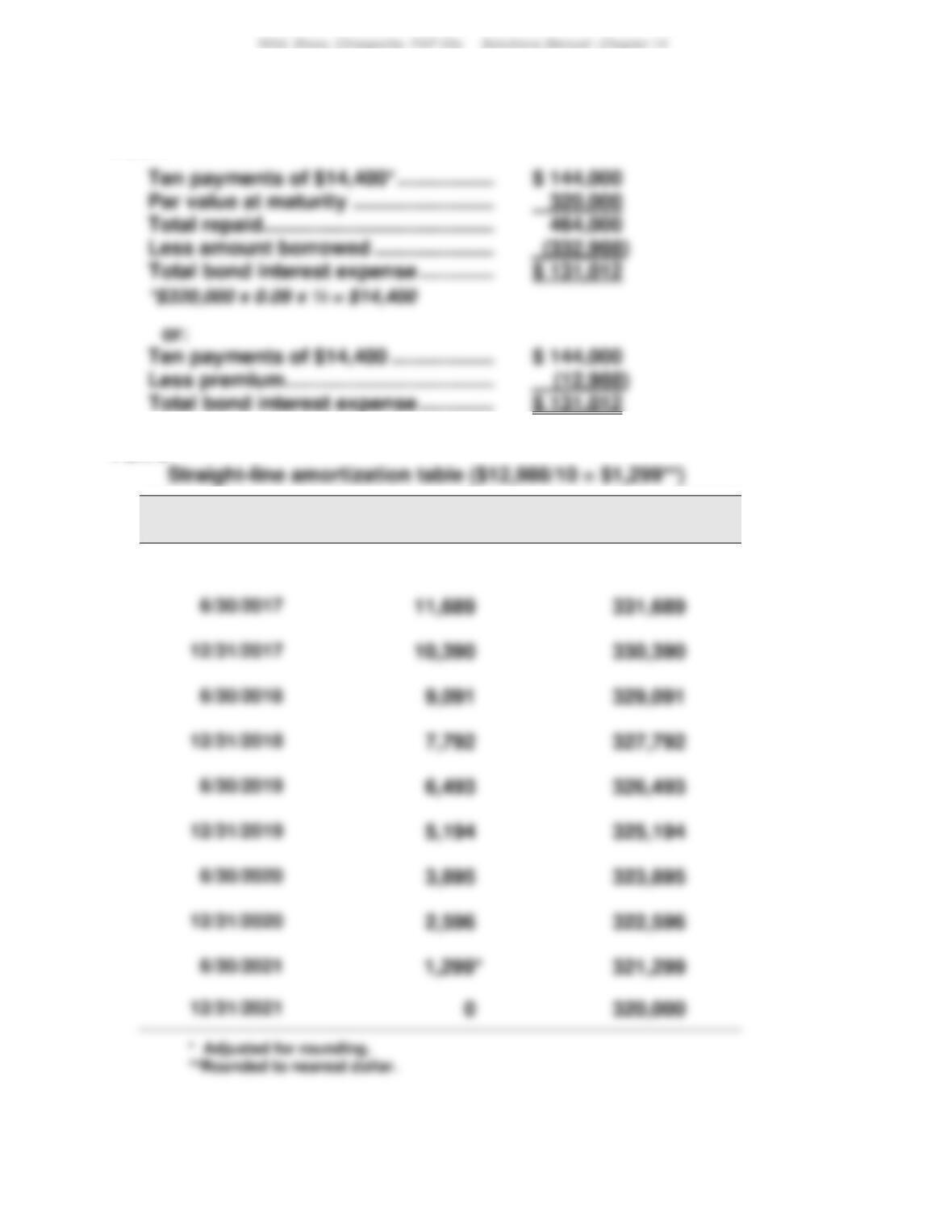

Thirty payments of $7,200* ……………………

$ 216,000

Par value at maturity …………………………..

240,000

$ 216,000

Part 3 Straight-line amortization table ($41,506/30= $1,384)

Semiannual

Interest Period-End

Unamortized

Discount

Carrying

Value

1/01/2017

$41,506

$ 198,494

6/30/2017

6/30/2018

855

Problem 14-5B (Concluded)

Part 4

2017

June 30

Bond Interest Expense …………………………..

8,584

2017

Dec. 31

Bond Interest Expense …………………………..

8,584

Notes Payable ……………………………………………………….

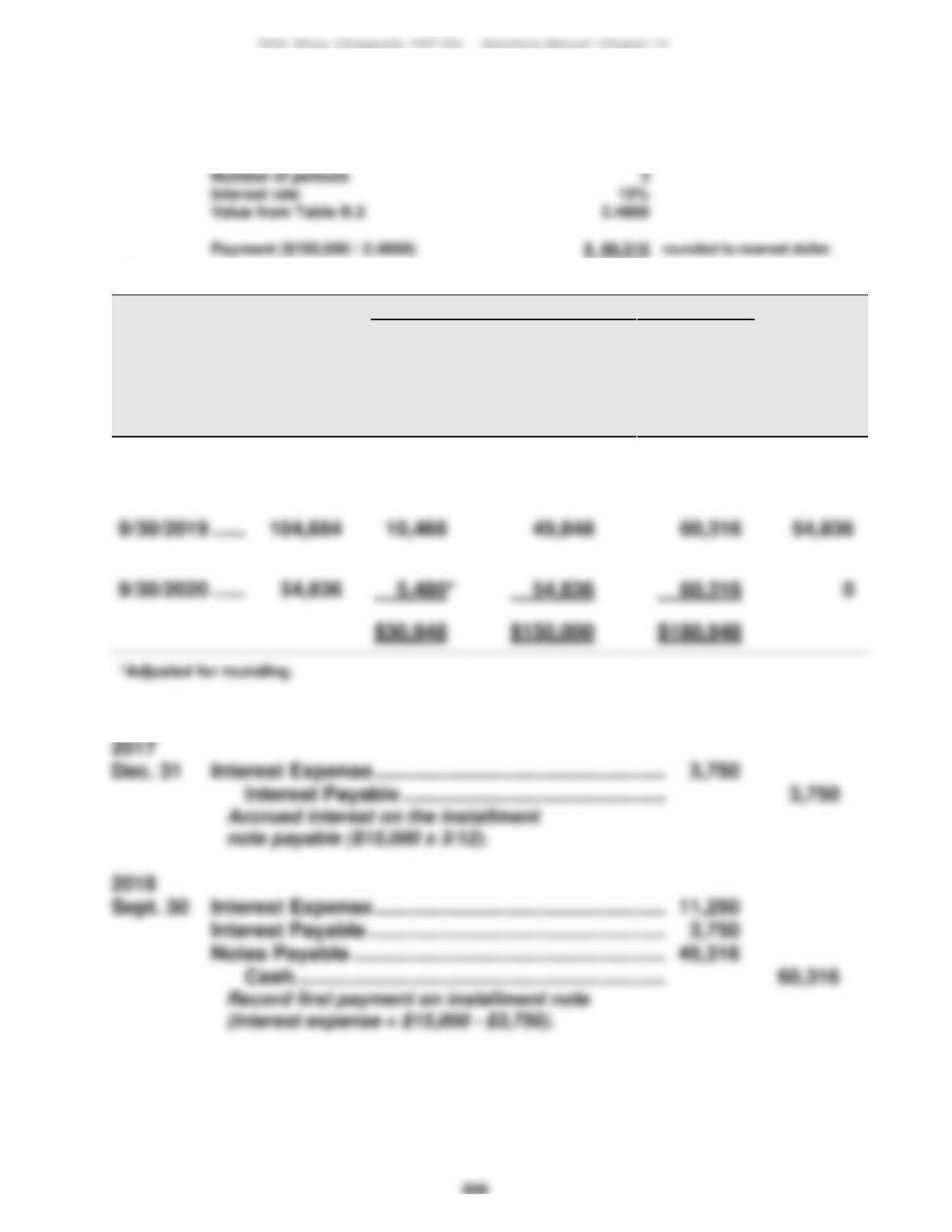

Problem 14-6B (45 minutes)

Background: Amount of Payment (given in the problem)

Note balance

$150,000

Number of periods

Interest rate

Value from Table B.3

Part 1

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[10% x (A)]

+

(C)

Debit

Notes

Payable

[(D) – (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

9/30/2018 ………….

$150,000

$15,000

$ 45,316

$ 60,316

$104,684

Part 2

857

Problem 14-7B (30 minutes)

Part 1

Atlas Company

Part 2

Bryan’s debt–to-equity ratio is much higher than that for Atlas. This implies

858

Problem 14-8BB (60 minutes)

Part 1

2017

Jan. 1

Cash ……………………………………………………….

198,494

Part 2

Thirty payments of $7,200* ……………………

$ 216,000

$ 216,000

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[3% x $240,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Discount

Amortization

[(B) – (A)]

(D)

Unamortized

Discount

[Prior (D) – (C)]

(E)

Carrying

Value

[$240,000 – (D)]

1/01/2017

$41,506

$198,494

6/30/2018