823

Exercise 14-13B (30 minutes)

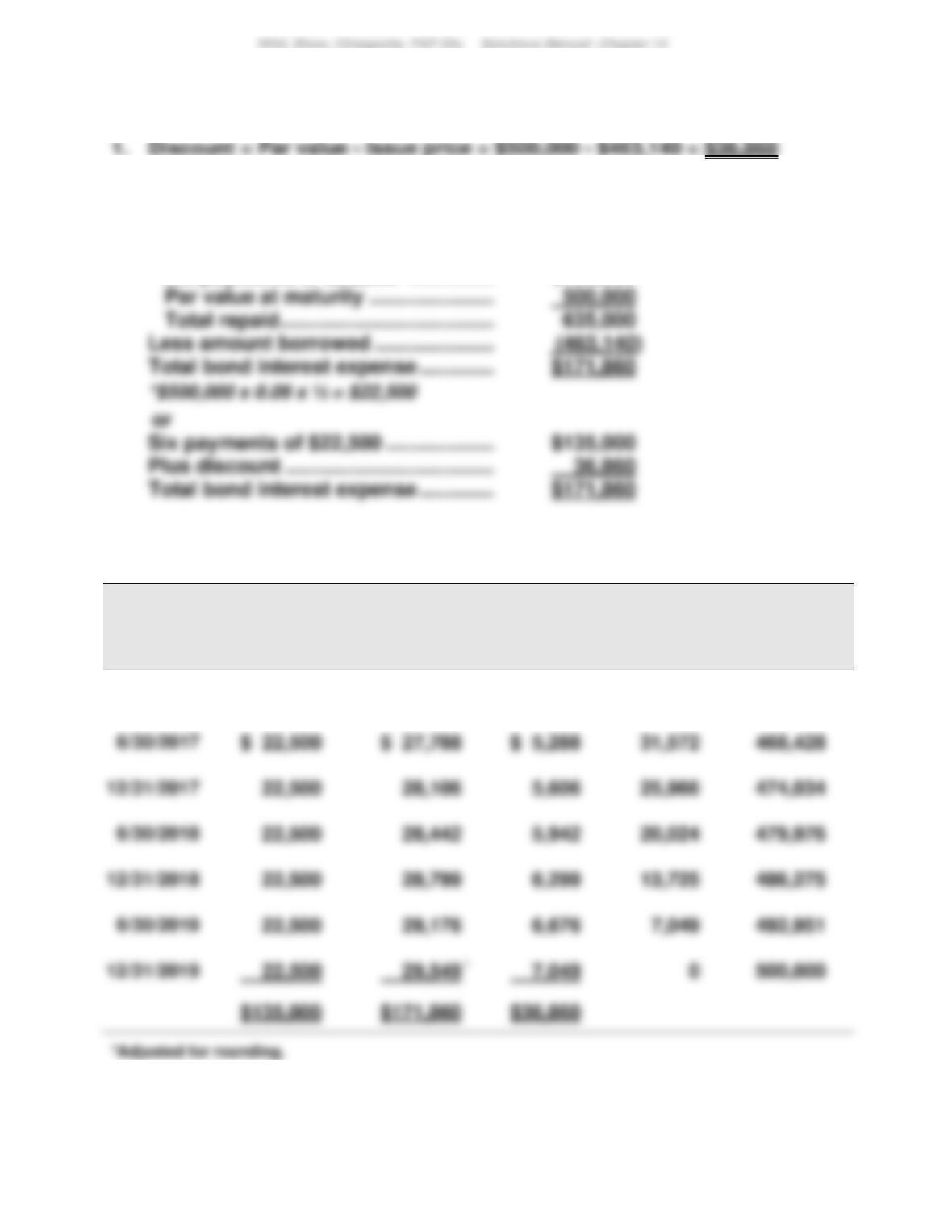

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $22,500* …………………..

$135,000

Par value at maturity …………………………

Total repaid ……………………………………….

$135,000

3. Effective interest amortization table

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[4.5% x $500,000]

(B)

Bond Interest

Expense

[6% x Prior (E)]

(C)

Discount

Amortization

[(B) – (A)]

(D)

Unamortized

Discount

[Prior (D) – (C)]

(E)

Carrying

Value

[$500,000 – (D)]

1/01/2017

$36,860

$463,140

6/30/2017

$ 27,788

6/30/2018

6/30/2019

824

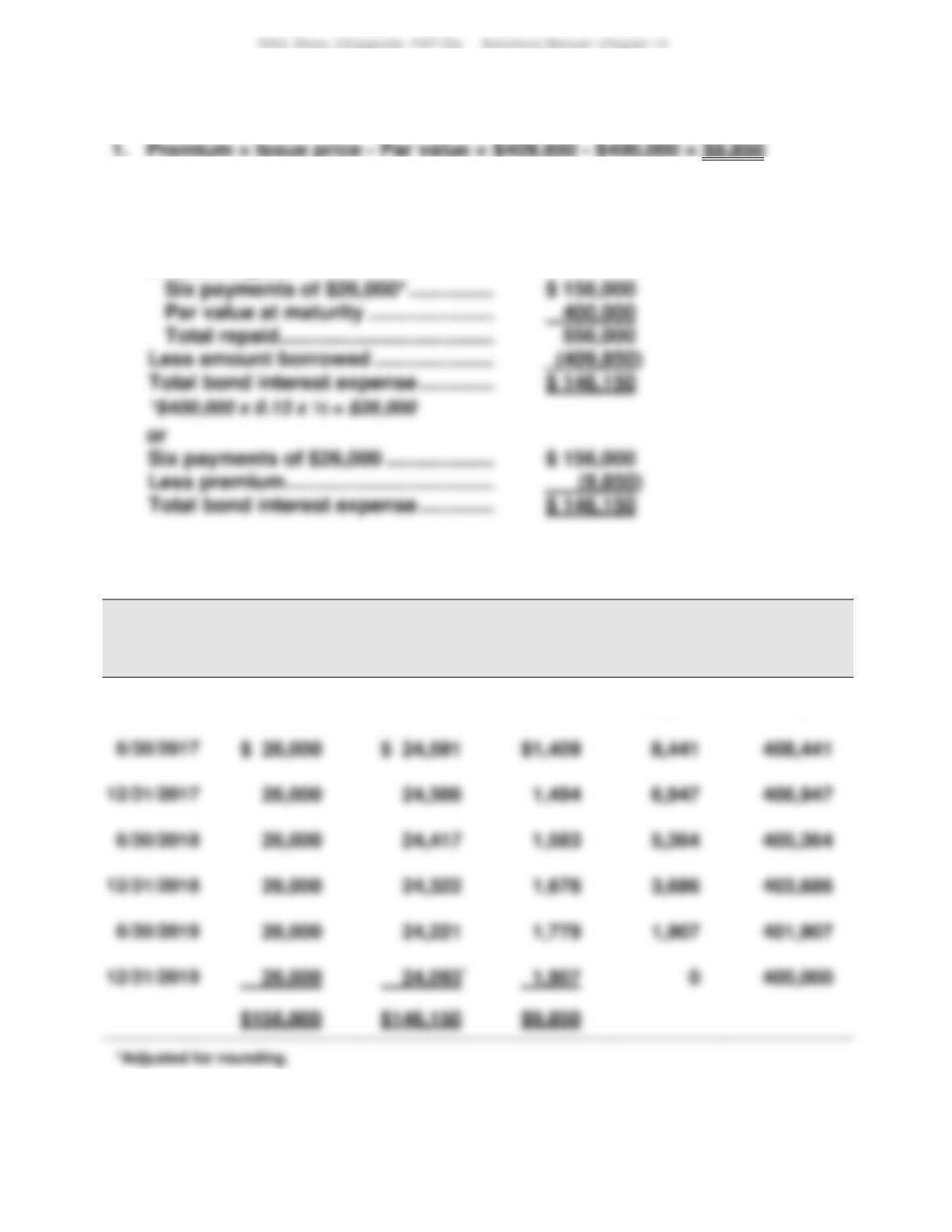

Exercise 14-14B (30 minutes)

2. Total bond interest expense over the life of the bonds

Amount repaid

3. Effective interest amortization table

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[6.5% x $400,000]

(B)

Bond Interest

Expense

[6% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[400,000 + (D)]

1/01/2017

$9,850

$409,850

6/30/2017

$ 26,000

6/30/2019

825

Exercise 14-15 (40 minutes)

1. Straight-line amortization table ([$100,000-$95,952]/8 = $506)

Semiannual

Period-End

Unamortized

Discount †

Carrying

Value

1/01/2017(issuance) ……….

$4,048

$95,952

6/30/2017 …………………

3,542

96,458

96,964

6/30/2018 …………………

2,530

97,470

6/30/2019 …………………

98,482

1,012

98,988

6/30/2020 …………………

99,494

826

Exercise 14-15 (Concluded)

2.

2017

June 30

Bond Interest Expense …………………………………………..

4,006

Discount on Bonds Payable …………………………..

Cash ………………………………………………………………..

Bond Interest Expense …………………………………………..

Discount on Bonds Payable …………………………..

Cash ………………………………………………………………..

Record 6 months’ interest and discount amortization.

3.

2020

Cash ………………………………………………………………..

Paid par value at maturity. (Assume interest recorded.)

Exercise 14-16 (20 minutes)

2017

Jan. 1

Cash ……………………………………………………………………..

3,400,000

Bonds Payable …………………………………………………

3,400,000

Bond Interest Expense …………………………………………..

Cash ……………………………………………………….

Paid semiannual interest. $3,400,000 x 0.09 x ½

Bond Interest Expense …………………………………………..

Cash ……………………………………………………….

2020

Bonds Payable ………………………………………………………

3,400,000

Cash ……………………………………………………….

3,400,000

827

Exercise 14-17C (10 minutes)

Exercise 14-18C (20 minutes)

1.

Leased Asset—Office Equipment ……………………………………….

41,000

2.

Depreciation Expense—Leased Asset, Office Equip ……………

Exercise 14-19C (15 minutes)

[Note: 12% / 12 months = 1% per month as the relevant interest rate.]

828

Exercise 14-20 (20 minutes)

(amounts in euros millions)

1.

Cash………………………………………………………………………

1,888

2.

Loans and Borrowings …………………………………………..

1,700

3. Heineken’s Loans and Borrowings carried a premium of €658 as of

4. The contract rate was higher than the market rate at issuance. This is

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 14

829

PROBLEM SET A

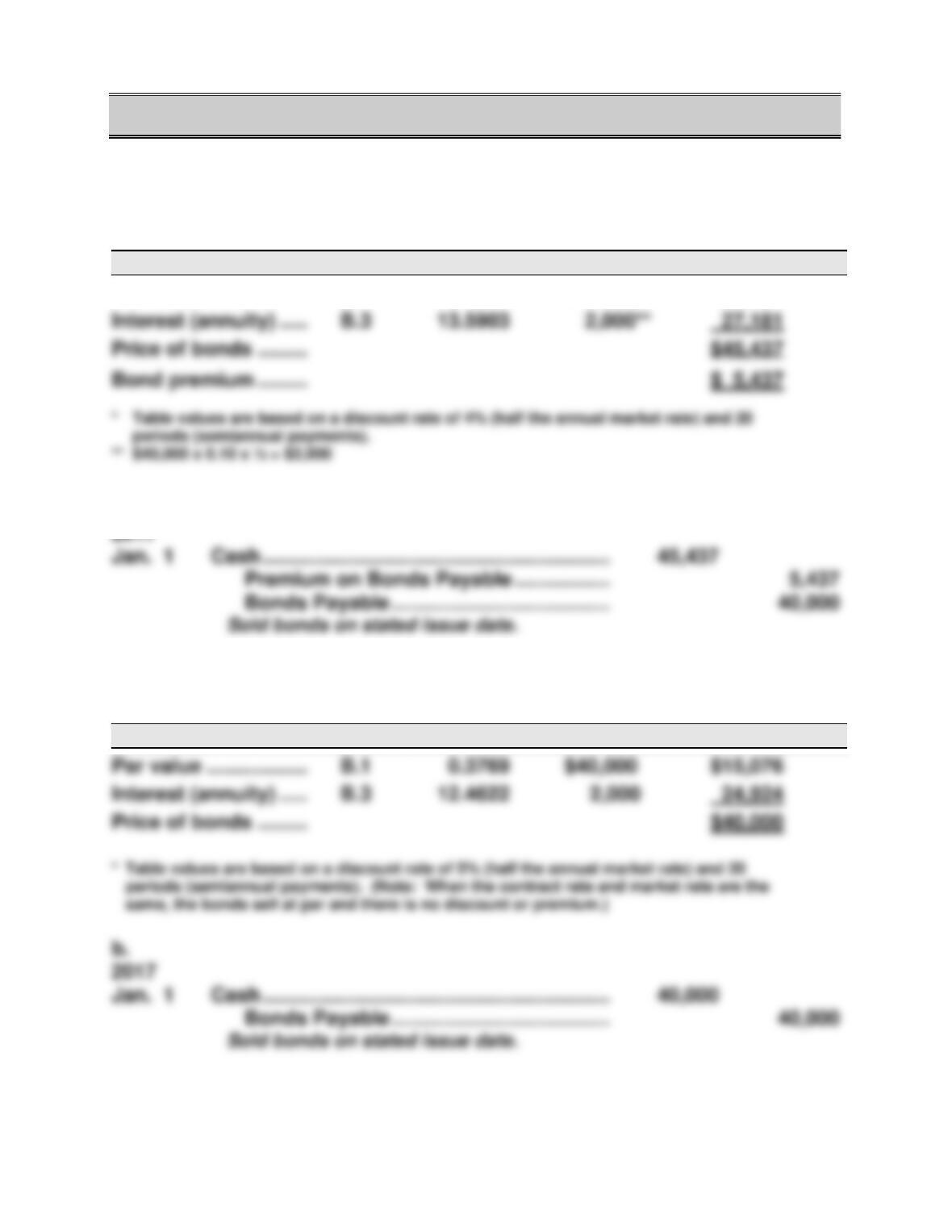

Problem 14-1A (50 minutes)

Part 1

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value …………………

B.1

0.4564

$40,000

$18,256

b.

Part 2

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value …………………

B.1

0.3769

$40,000

$15,076

B.3

B.3

830

Problem 14-1A (Concluded)

Part 3

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value ………………..

B.1

0.3118

$40,000

$12,472

B.3

$35,412

b.

2017

831

Problem 14-2A (40 minutes)

Part 1

2017

Jan. 1

Cash ……………………………………………………….

3,456,448

Part 2

[Note: The semiannual amounts for (a), (b), and (c) below are the same throughout the bonds’

life because this company uses straight-line amortization.]

Part 3

Thirty payments of $120,000 ………………..

$3,600,000

Par value at maturity …………………………..

Total repaid ………………………………………….

Less amount borrowed ………………………..

(3,456,448)

Part 4 (Semiannual amortization: $543,552/30 = $18,118.4)

Semiannual

Period-End

Unamortized

Discount

Carrying

Value

1/01/2017 …………………

$543,552

$3,456,448

6/30/2017 …………………

525,434

6/30/2018 …………………

489,198

832

Problem 14-2A (Concluded)

Part 5

2017

June 30

Bond Interest Expense …………………………………………..

138,118

Bond Interest Expense …………………………………………..

138,118

Problem 14-3A (40 minutes)

Part 1

2017

Jan. 1

Cash ……………………………………………………………………..

4,895,980

4,000,000

Part 2

(a) Cash Payment = $4,000,000 x 6% x 6/12 = $120,000

Thirty payments of $120,000 ………………..

Total repaid ………………………………………….

Less amount borrowed ………………………..

833

Problem 14-3A (Concluded)

Part 4

Semiannual

Period-End

Unamortized

Premium

Carrying

Value

1/01/2017 …………………

$895,980

$4,895,980

Part 5

2017

June 30

Bond Interest Expense …………………………..

90,134

29,866

Bond Interest Expense …………………………..

90,134

29,866

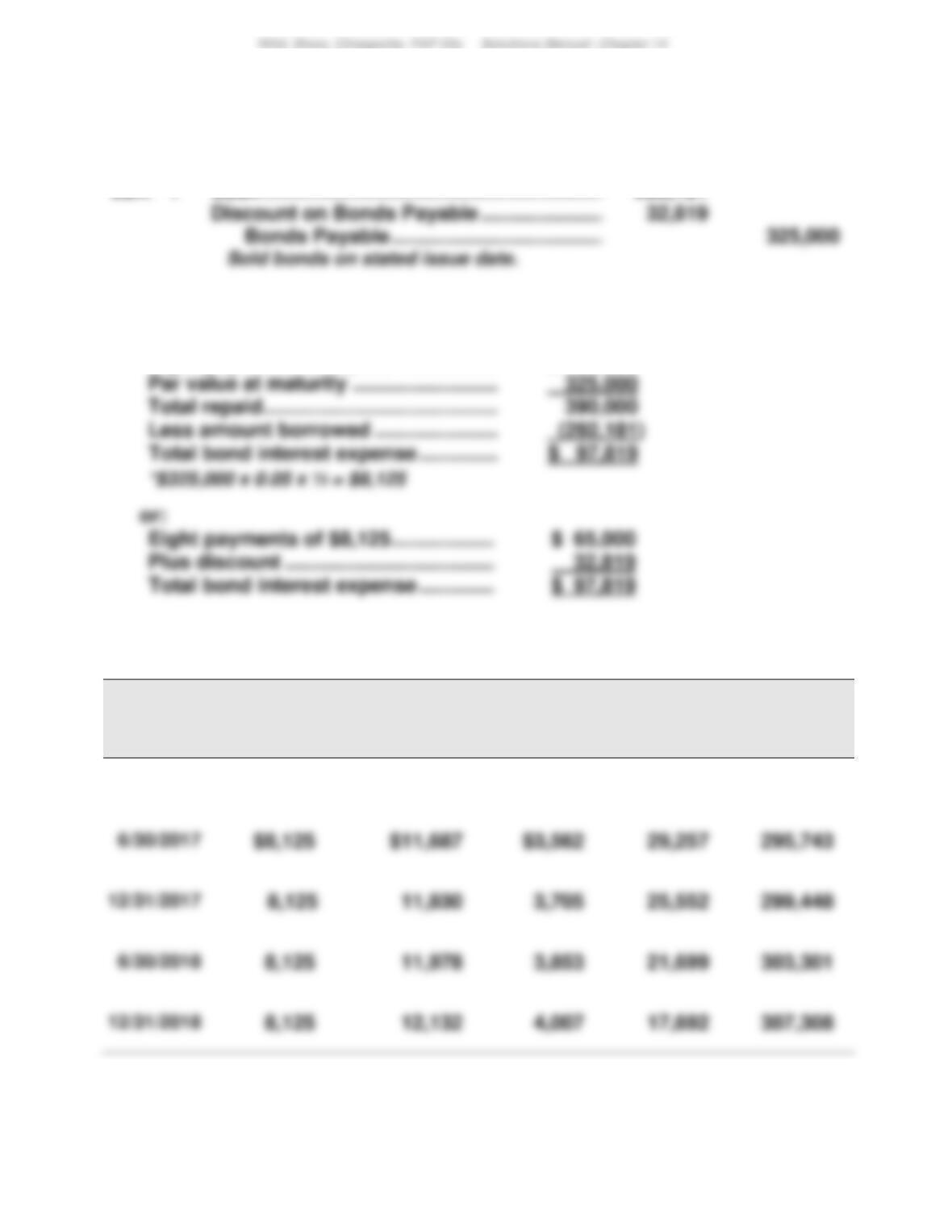

Problem 14-4A (45 minutes)

Part 1

Ten payments of $8,125* ……………………..

$ 81,250

Par value at maturity …………………………..

Total repaid ………………………………………….

Less amount borrowed ………………………..

Ten payments of $8,125 ……………………….

$ 81,250

Less premium………………………………………

Part 2

Semiannual

Interest Period–End

Unamortized

Premium

Carrying

Value

1/01/2017

$5,333

$255,333

6/30/2017

4,800

254,800

12/31/2017

4,267

254,267

6/30/2018

3,734

253,734

12/31/2018

3,201

253,201

6/30/2019

2,668

252,668

2,135

252,135

6/30/2020

1,602

251,602

12/31/2020

1,069

261,069

6/30/2021

533**

250,533

12/31/2021

0

250,000

835

Problem 14-4A (Concluded)

Part 3

2017

June 30

Bond Interest Expense …………………………..

7,592

Premium on Bonds Payable …………………………..

2017

Dec. 31

Bond Interest Expense …………………………..

7,592

Premium on Bonds Payable …………………………..

836

Problem 14-5A (60 minutes)

Part 1

2017

Jan. 1

Cash ……………………………………………………….

292,181

Part 2

Eight payments of $8,125* ……………….

$ 65,000

Par value at maturity ……………………….

325,000

(292,181)

$ 65,000

Part 3 Straight-line amortization table ($32,819/8 =$4,102*)

Semiannual

Interest Period-End

Unamortized

Discount

Carrying

Value

1/01/2017

$32,819

$292,181

837

Problem 14-5A (Concluded)

Part 4

2017

June 30

Bond Interest Expense …………………………..

12,227

Discount on Bonds Payable …………………………..

4,102

Cash ……………………………………………………….

8,125

Bond Interest Expense …………………………..

12,227

Discount on Bonds Payable …………………………..

4,102

Cash ……………………………………………………….

8,125

Part 5

If the market interest rate on the issue date had been 4% instead of 8%, the

bonds would have sold at a premium because the contract rate of 5%

would have been greater than the market rate.

838

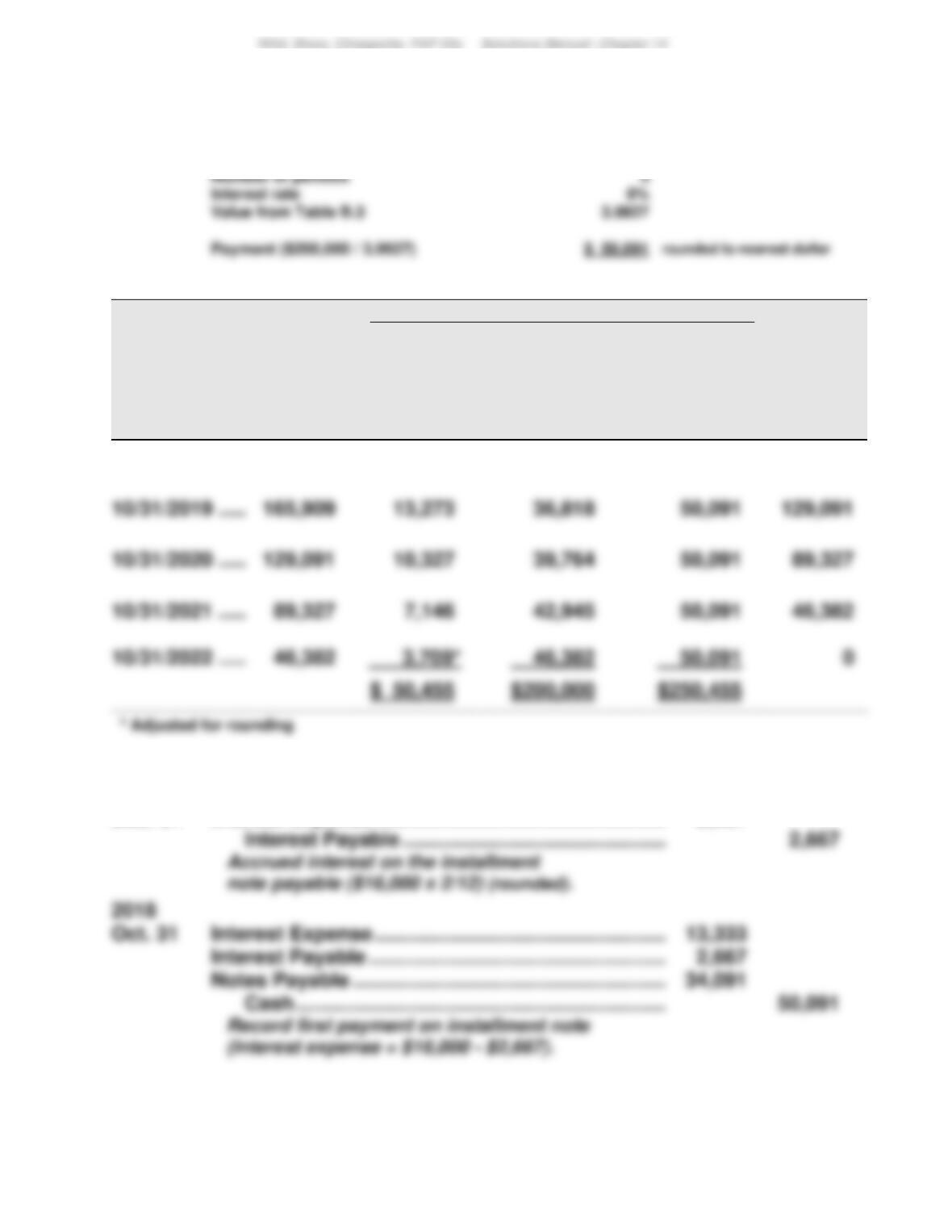

Problem 14-6A (45 minutes)

Background: Amount of Payment (given in the problem)

Note balance

$200,000

Number of periods

Interest rate

Value from Table B.3

Part 1

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[8% x (A)]

+

(C)

Debit

Notes

Payable

[(D) – (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

10/31/2018 …………

$200,000

$ 16,000

$ 34,091

$ 50,091

$165,909

$ 50,455

$200,000

$250,455

Part 2

2017

Dec. 31

Interest Expense ……………………………………………………

2,667

Interest Payable …………………………..…………………..

Interest Expense ……………………………………………………

Interest Payable …………………………………………………….

2,667

Cash ………………………………………………………………..

839

Problem 14-7A (20 minutes)

Part 1

Part 2

Scott’s debt–to–equity ratio is higher than Pulaski’s. This implies that Scott

840

Problem 14-8AB (60 minutes)

Part 1

2017

Jan. 1

Cash ……………………………………………………….

292,181

Part 2

Eight payments of $8,125* ……………….

$ 65,000

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[2.5% x $325,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Discount

Amortization

[(B) – (A)]

(D)

Unamortized

Discount

[Prior (D) – (C)]

(E)

Carrying

Value

[$325,000 – (D)]

1/01/2017

$32,819

$292,181

841

Problem 14-8AB (Concluded)

Part 4

2017

June 30

Bond Interest Expense …………………………..

11,687

2017

Dec. 31

Bond Interest Expense …………………………..

11,830

842

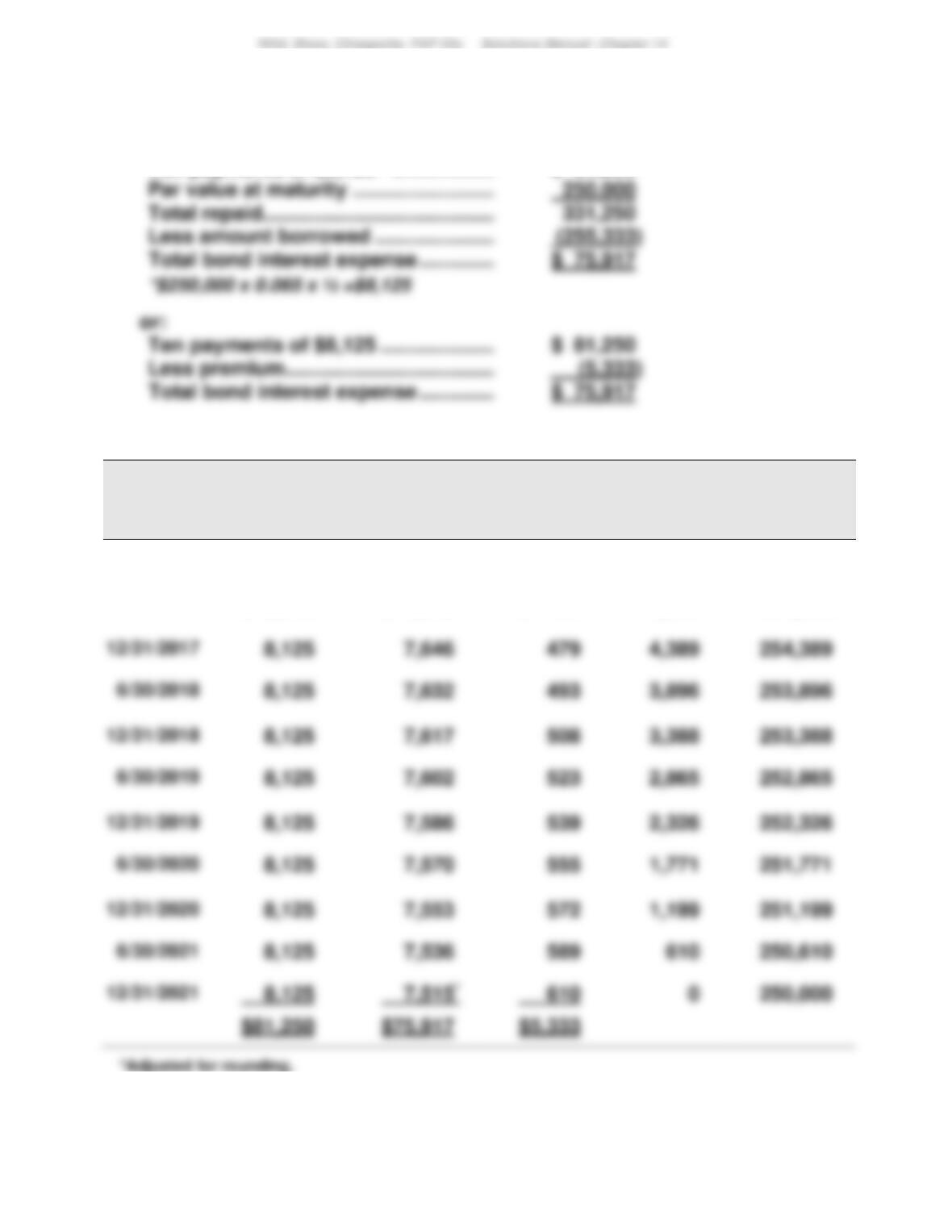

Problem 14-9AB (45 minutes)

Part 1

Ten payments of $8,125* ………………………

$ 81,250

Par value at maturity …………………………..

Total repaid …………………………………………..

Less amount borrowed …………………………

Ten payments of $8,125 ……………………….

$ 81,250

Less premium………………………………………

Part 2

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[3.25% x $250,000]

(B)

Bond Interest

Expense

[3% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$250,000 + (D)]

1/01/2017

$5,333

$255,333

6/30/2017

$ 8,125

$ 7,660

$ 465

4,868

254,868

4,389

6/30/2018

3,388

6/30/2019

2,326

6/30/2020

1,199

6/30/2021

$81,250

$75,917

*Adjusted for rounding.