14–39

PROBLEM 14-58 (45 MINUTES)

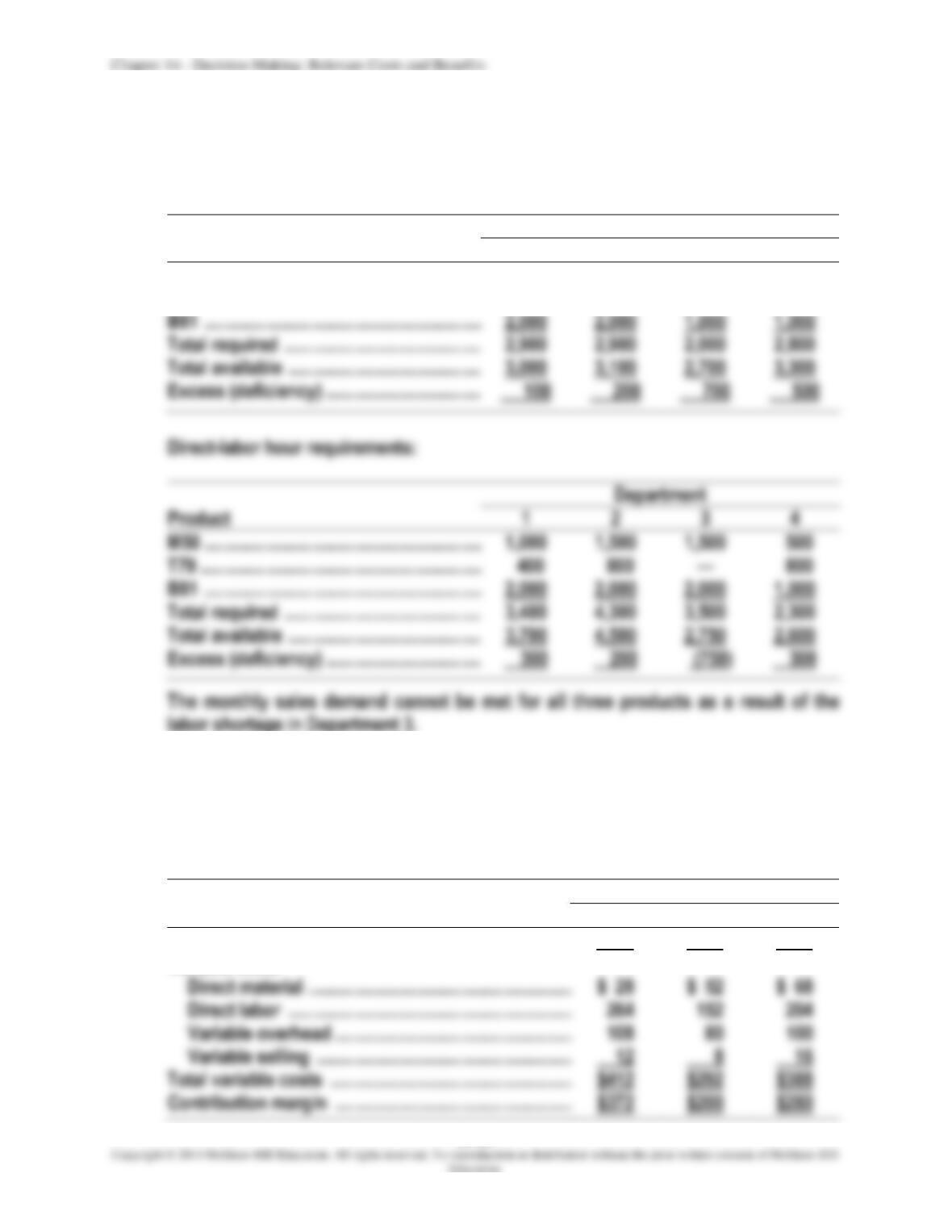

1. Machine hour requirements:

Department

Product

1

2

3

4

M50 ……………………………………………………….

500

500

1,000

1,000

T79 ……………………………………………………….

400

400

—

800

B81 ……………………………………………………….

2,000

2,000

1,000

1,000

Total required ……………………………………………………….

2,900

2,900

2,000

2,800

Total available ……………………………………………………….

3,000

3,100

2,700

3,300

Department

Product

1

2

3

4

M50 ……………………………………………………….

1,000

1,500

1,500

500

T79 ……………………………………………………….

400

800

—

800

B81 ……………………………………………………….

2,000

2,000

2,000

1,000

Total required ……………………………………………………….

3,400

4,300

3,500

2,300

Total available ……………………………………………………….

3,700

4,500

2,750

2,600

2. The goal is to maximize contribution margin. Fixed costs are not relevant. The scarce

resource is direct-labor hours (DLH) in Department 3. Oceana should first produce

the product that maximizes contribution margin per unit of the scarce resource

(DLH). In this case two products, M50 and B81, require direct-labor hours in

Department 3.

Product

M50

T79

B81

Sales price ………………………………………………………………….

$784

$492

$668

Variable costs

264

152

204

108

100

14–40

PROBLEM 14-58 (CONTINUED)

Product

Contribution

Margin

Department 3

DLH

Contribution

Margin

per DLH

M50

$372

$124

Units

Department 3

DLH

Required

Balance (DLH)

Maximum DLH available

in Department 3

2,750

Product B81 first

1,000

2,000

Product M50 second

RESULTING PRODUCTION SCHEDULE

Product

Units

Comments

M50

250

by Department 3.

Produce as much as possible to maximize

Produce as much as the constraint allows (750 ÷

3 DLH per unit). Reduced production is based on

SCHEDULE OF CONTRIBUTION MARGIN BY PRODUCT

Product

Contribution

Margin per Unit

Units

Produced

Contribution

to Profit

M50

$372

250

$ 93,000

1,000

3. To supply the additional quantities of M50 that are required, Oceana should

consider:

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–41

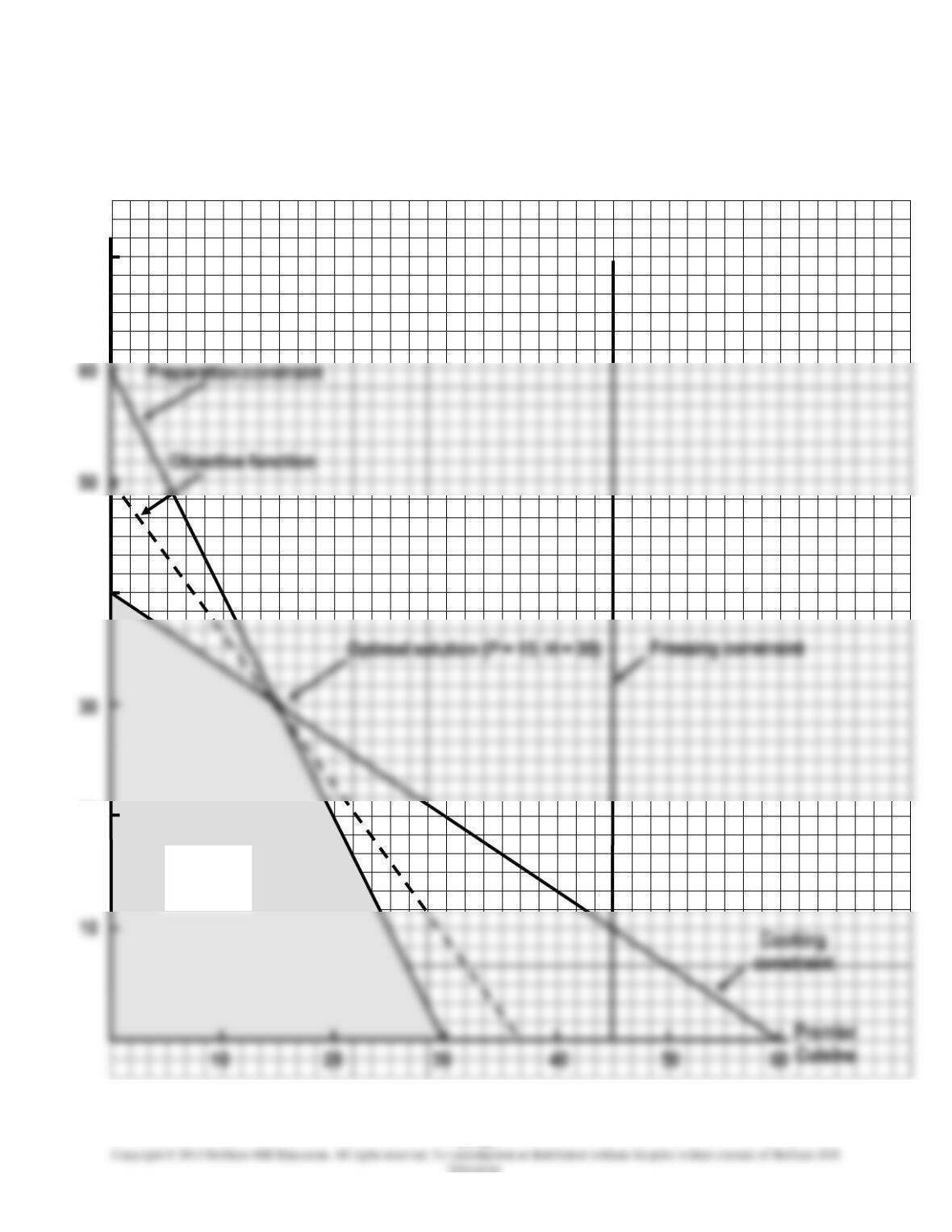

PROBLEM 14-59 (45 MINUTES)

1. The objective function and constraints that Time Saver Meals, Inc. should use to

maximize profits are as follows:

Maximize

60P + 45H

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–42

PROBLEM 14-59 (CONTINUED

2. Graph of linear program:

Haute Cuisine

60

50

70

40

30

20

10

Feasible

region

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–43

PROBLEM 14-59 (CONTINUED)

3. & 4.

Corner Points

in Feasible Region

Objective Function

Value

P = 0

H =0

($60)(0) + ($45)(0) = 0

P = 0

H = 40

($60)(0) + ($45)(40) = $1,800

P = 15

H = 30

($60)(15) + ($45)(30) = $2,250

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–44

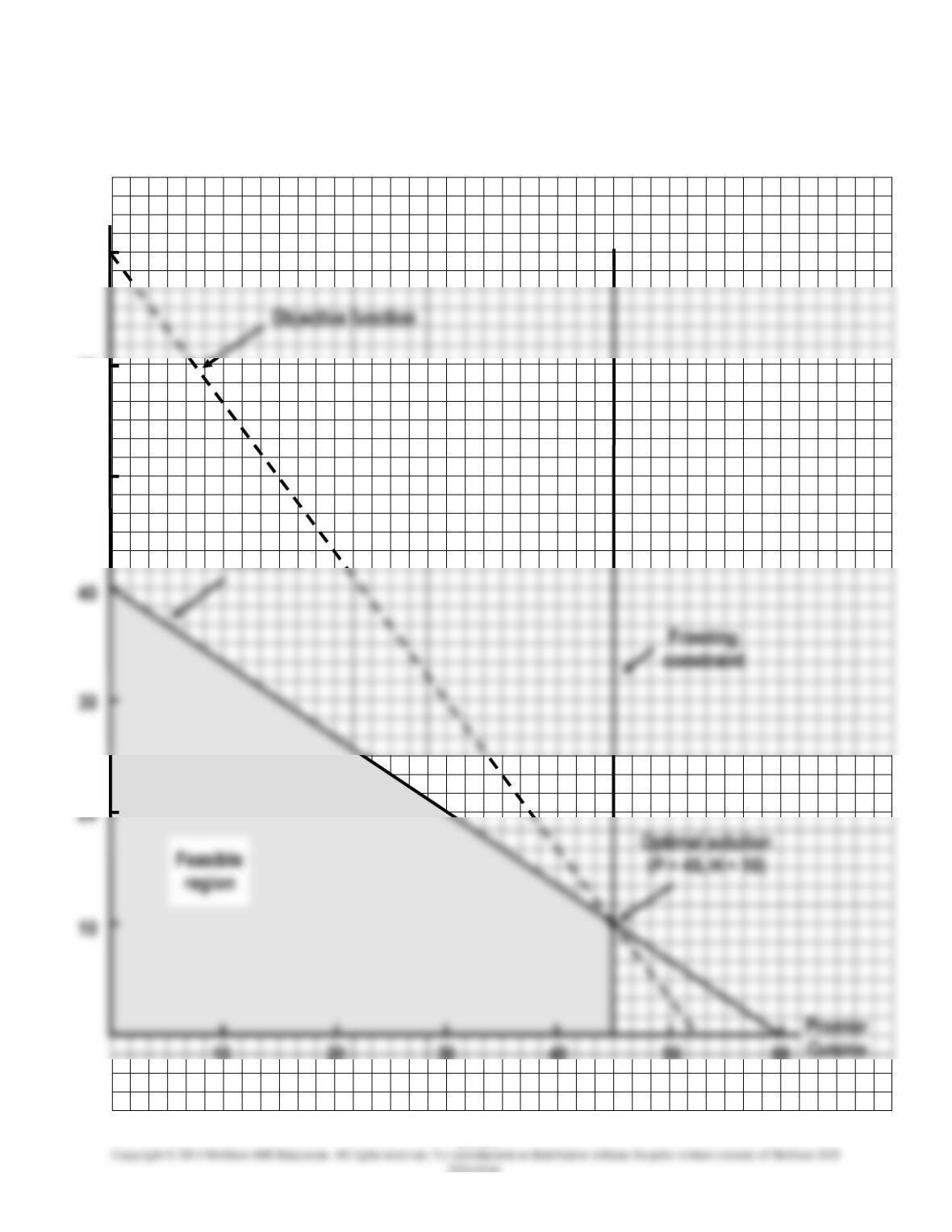

PROBLEM 14-59 (CONTINUED)

5. Graph of linear program:

Haute Cuisine

70

60

50

40

30

20

10

Cooking

constraint

10

20

30

40

50

60

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–45

PROBLEM 14-59 (CONTINUED)

Corner Points

in Feasible Region

Objective Function

Value

P = 0

H =0

($60)(0) + ($45)(0) = 0

P = 0

H = 40

($60)(0) + ($45)(40) = $1,800

P = 45

H = 10

($60)(45) + ($45)(10) = $3,150

14–46

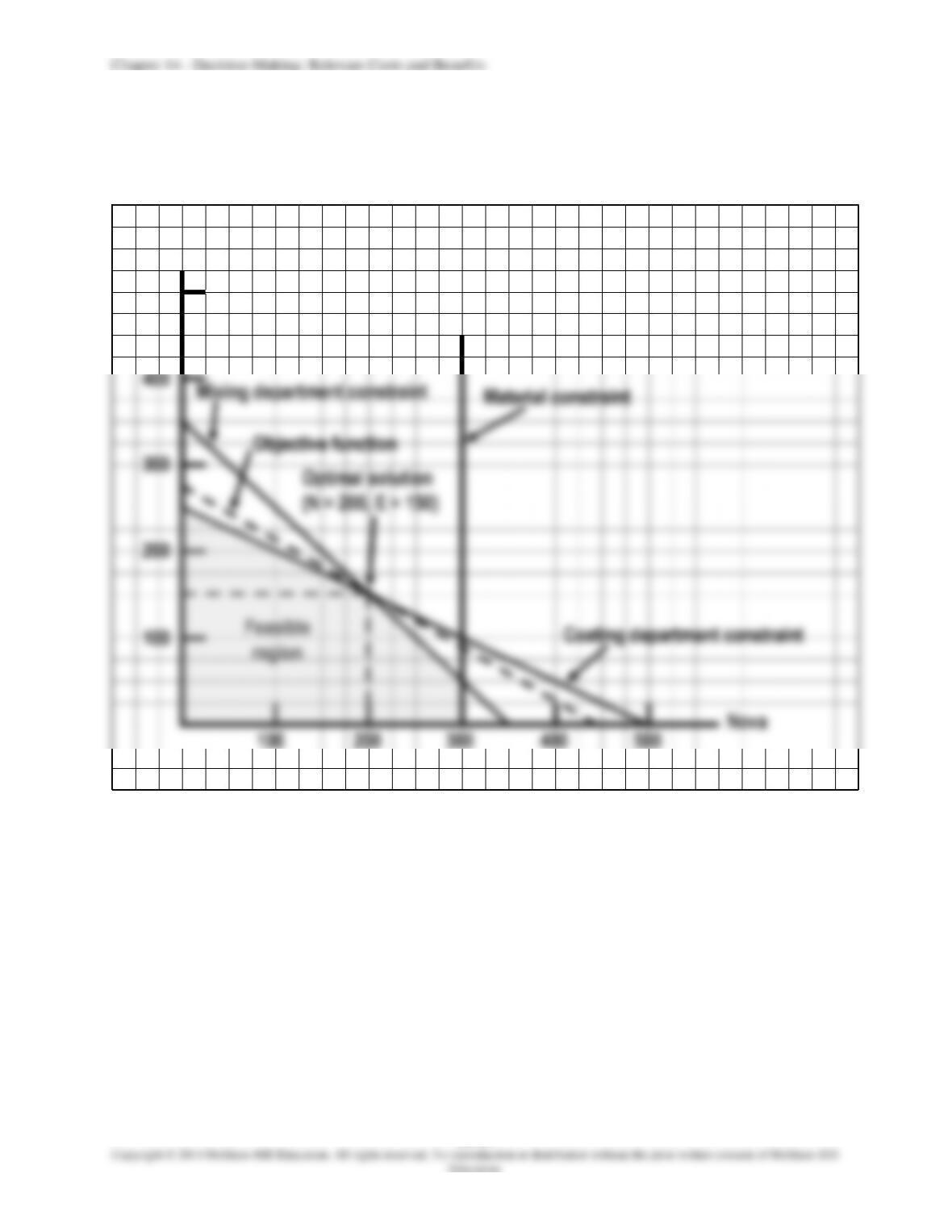

PROBLEM 14-60 (40 MINUTES)

1. In order to maximize contribution margin, the objective function and constraint

functions would be formulated as follows:

Notation:

E = number of batches of Eclipse candy bars

N = number of batches of Nova candy bars

2. The number of batches of each candy bar that should be produced to maximize

14–47

PROBLEM 14-60 (CONTINUED)

Graph of linear program:

500

300

100

200

300

100

400

500

Eclipse

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–48

PROBLEM 14-61 (50 MINUTES)

1. Linear programming (LP) is designed to determine the optimum mix when resources

are limited and can be switched or allocated among products. LP would be

2. Notation:

RL

=

Regular model in Labor Assembly

RA

=

Regular model in Automated Assembly

DL

=

Deluxe model in Labor Assembly

DA

=

Deluxe model in Automated Assembly

a. Objective function: *

*Supporting calculations (per-unit basis):

RL

RA

DL

DA

Selling price …………………………………

$90.00

$90.00

$120.00

$120.00

Less: Variable costs:

Raw material …………………………….

$44.00

$44.00

$ 57.50

$ 57.50

Plating labor ……………………………..

4.00

4.00

4.00

4.00

Assembly labor …………………………

6.00

1.20

6.00

1.20

Plating supplies ………………………..

2.50

2.50

2.50

2.50

Assembly supplies ……………………

3.00

3.00

3.00

3.00

Plating power …………………………...

2.40

2.40

2.40

2.40

Assembly power ……………………….

1.50

3.60

1.50

3.60

6.00

6.00

6.00

6.00

Total variable cost ………………………..

$69.40

$66.70

$ 82.90

$ 80.20

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–49

PROBLEM 14-61 (CONTINUED)

b. Constraints:

Direct labor (plating): .2 RL + .2 RA + .2 DL + .2 DA 30,000 hours

Direct labor (assembly): .25 RL + .05 RA + .25 DL + .05 DA 40,000 hours

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–50

SOLUTIONS TO CASES

CASE 14-62 (60 MINUTES)

1.

Memorandum

Date:

Today

To:

Maria Carlo, President, Ontario Pump Company

From:

I.M. Student

Subject:

Suggested revision of product-line income statement

2. a. The suggested discontinuance of the S-pumps would be cost effective, but the

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–51

CASE 14-62 (CONTINUED)

F-Pump

R-Pump

S-Pump

Unit selling price …………………………

$270

$600

$540

Unit variable costs

Raw material …………………………..

$51

$ 93

$150

Direct labor …………………………….

120

180

135

180

Shipping expenses ………………….

Unit contribution margin ……………..

$222

Increase (decrease) in units*

)

)

Decrease (increase) in fixed costs

)

b. Yes, the president was correct in eliminating the S-pumps. The S-pump sales

price covers only its variable cost and does not contribute anything to

Unit contribution ……………………………………………………….

14–52

CASE 14-62 (CONTINUED)

However, the president’s decisions regarding promotion expense do not seem

well conceived. The decreased promotion on the F-pump line and the increased

whether to drop the S-pump line include:

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–53

CASE 14-63 (45 MINUTES)

In order to maximize the company’s profitability, All Sports Company should purchase

1. Calculate unit contribution margins:

Purchased

Manufactured

Tackle

Boxes

Tackle

Boxes

Skate-

boards

Selling price ……………………………………………………….

$91.00

$91.00

$50.00

Less:

Contribution margin ……………………………………………………

$14.00

$33.00

$19.50

Direct-labor hours per unit ………………………………………….

*Calculation of variable overhead per unit:

Tackle boxes:

Direct-labor hours ………………………………….

$18.75 ÷ $15.00 = 1.25 hours

Overhead per direct-labor hour ………………

$12.50 ÷ 1.25 = $10.00

Total variable overhead ………………………….

$100,000 – $50,000 = $50,000

Variable overhead per hour ……………………

$50,000 ÷ 10,000 = $5.00

Skateboards:

Direct-labor hours ………………………………….

$7.50 ÷ $15.00 = .5 hours

14–54

CASE 14-63 (CONTINUED)

The optimal use of All Sports Company’s scarce resource (direct labor) is to

2. The following table shows the improvement in the company’s total contribution

The optimal use of All Sports Company’s available direct-labor hours (DLH):

Item

Quantity

DLH

per

Unit

Total

DLH

Balance

of

DLH

Unit

Contri-

bution

Total

Contri-

bution

Total hours ……………

10,000

Skateboards ………….

17,500

.50

8,750

1,250

$19.50

$341,250

Make boxes …………..

1,250

Buy boxes ……………..

Total contribution ….

$500,250

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–55

FOCUS ON ETHICS (See page 613 in the text.)

This scenario addresses the effects of a decision to outsource, and as a result, close a

department.

Edgeworth is not acting ethically in asking Mint to withhold the ABC costing analysis

data from Mello. To do so would be tantamount to deliberately risking that the company