E14–21

a.

Operations from

Income sing‘Manufactur

Retina in Increase

=

Price

Market

–

Unit per Cost

Variable

×

dTransferre

Units

$225,000 = ($75 – $66) × 25,000

Price

Transfer

dTransferre

Units

This is the amount the Aircraft Division saves by purchasing from the Elec-

tronic Division at an internal price that is lower than the market price.

c.

Operations from Income

sDivision‘ )(Supplying

Electronic the in Increase

=

Price

Transfer

–

Unit per Cost

Variable

×

dTransferre

Units

$150,000 = ($72 – $66) × 25,000

This is the amount the Electronic Division earns by using available excess

capacity to produce and sell products above variable cost to the Aircraft Divi-

sion.

472

PROBLEMS

P14–1

1. SNEED INDUSTRIES COMPANY

Budget Performance Report—Director, Crane Division

For the Month Ended August 31, 20Y6

Over Under

2. The customer service and marketing salaries are significantly over budget.

The director should investigate the cause of these results. One possibility is

that the company is having an increase in sales, requiring greater marketing

473

P14–2

1.

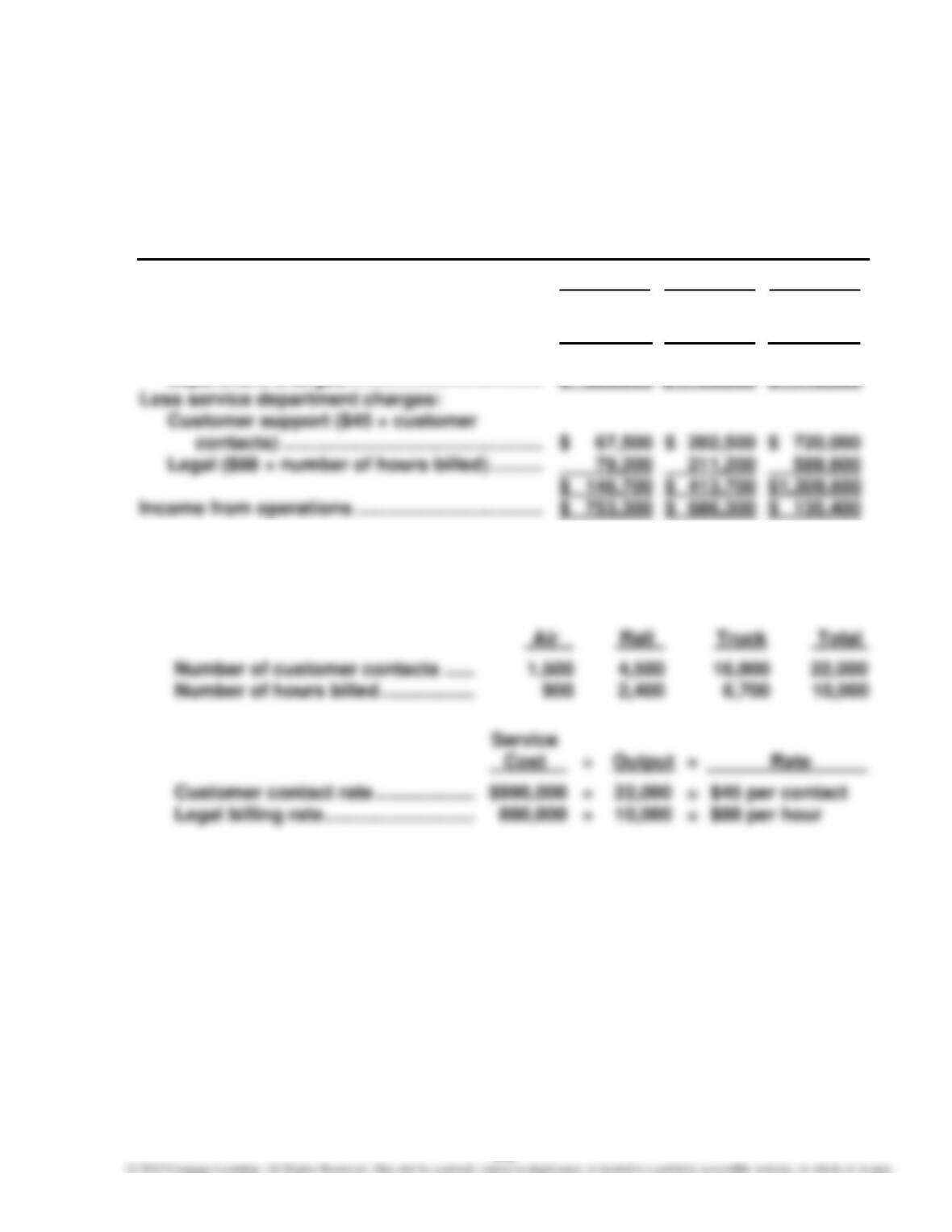

A-ONE FREIGHT INC.

Divisional Income Statements

For the Quarter Ended December 31, 20Y3

Air Rail Truck

Revenues …………………………………………………… $5,000,000 $6,000,000 $9,000,000

Operating expenses ……………………………………. 4,100,000 4,900,000 7,555,000

Income from operations before service

department charges ………………………………. $ 900,000 $1,100,000 $1,445,000

Supporting schedules:

Service department charge rates for the two service departments, Customer

Support and Legal, are determined as follows:

Note: The Shareholder Relations Department and general corporate officers’ sala-

ries are not controllable by division management and thus are not included in

determining division income from operations.

474

P14–2, Concluded

2. The CEO evaluates the three divisions using income from operations as a

percent of revenues (profit margin). This measure is calculated for the three

divisions as follows:

3. To: CEO

The method used to evaluate the performance of the divisions should be

reevaluated. The present method identifies the amount of income from opera-

tions per dollar of earned revenue. However, this company requires a signifi-

cant investment in fixed assets and distribution facilities. In addition, the

amount of assets may not be related to the revenue earned. For example,

475

P14–3

1.

PASTRY INC.

Divisional Income Statements

For the Year Ended April 30, 20Y7

Frozen

Breakfast Cookies Desserts

Division Division Division

Income from operations ………………… $ 3,168,000 $1,026,000 $ 5,994,000

2.

Investment

on Return of Rate

= Profit Margin × Investment Turnover

Investment

on Return of Rate

=

Sales

Operations from Income

×

AssetsInvested

Sales

Breakfast Division: ROI =

0$19,800,00

$3,168,000

×

0$18,000,00

0$19,800,00

= 16.0% × 1.10

= 17.6%

0$33,300,00

$5,994,000

0$27,750,00

0$33,300,00

3. Per dollar of invested assets, the Frozen Desserts Division is the most profit-

able of the three divisions. Assuming that the rates of return on investments

do not change in the future, an expansion of the Frozen Desserts Division will

476

P14–4

1.

Investment

on Return of Rate

= Profit Margin × Investment Turnover

Investment

on Return of Rate

2.

AMAZING RIDES INC.—JET SKI DIVISION

Estimated Income Statements

For the Year Ended December 31, 20Y2

Proposal 1 Proposal 2 Proposal 3

Sales ……………………………………………… $12,000,000 $12,000,000 $ 9,720,000

Cost of goods sold …………………………. 7,464,000 6,720,000 5,800,000

477

P14–4, Concluded

3.

Investment

on Return of Rate

= Profit Margin × Investment Turnover

Investment

on Return of Rate

=

Sales

Operations from Income

×

AssetsInvested

Sales

0$12,000,00

$1,416,000

0$12,000,00

0$12,000,00

Proposal 2: ROI =

0$12,000,00

$2,160,000

×

0$16,000,00

0$12,000,00

= 18.0% × 0.75

= 13.5%

0$10,800,00

$9,720,000

4. Proposal 2 would yield a rate of return on investment of 13.5%.

5. Rate of Return on Investment = Profit Margin × Required Investment Turnover

12% = 14% × Required Investment Turnover

478

P14–5

1.

MONTANA BIKE COMPANY

Divisional Income Statements

For the Year Ended December 31, 20Y9

On-Road Off-Road

Bike Bike

Division Division

Sales ………………………………………………………….. $10,500,000 $8,000,000

2.

Investment

on Return of Rate

= Profit Margin × Investment Turnover

Investment

on Return of Rate

=

Sales

Operations from Income

×

AssetsInvested

Sales

Off-Road Bike Division: ROI =

$8,000,000

$840,000

×

$5,000,000

$8,000,000

= 10.5% × 1.6

P14–5, Concluded

4. On the basis of income from operations, the On-Road Bike Division generated

$420,000 ($1,260,000 – $840,000) more income from operations than did the

Off-Road Bike Division. However, income from operations does not consider

the amount of invested assets in each division.

480

P14–6

1. No. When unused capacity exists in the supplying division (the GPS Systems

2. The GPS Systems Division’s income from operations would increase by

$300,000:

Operations from Income sDivision‘

)(Supplying

Systems GPS in Increase

=

Price

Transfer

–

Unit per Cost

Variable

×

dTransferre

Units

$300,000 = ($52 – $40) × 25,000

Operations from Income sDivision‘

Price

Transfer

dTransferre

Units

By purchasing from the GPS Systems Division, the Communication Systems

Division saves $8 ($60 – $52) per unit on its purchases.

Pendray Scientific Inc.’s total income from operations would increase by

$500,000:

481

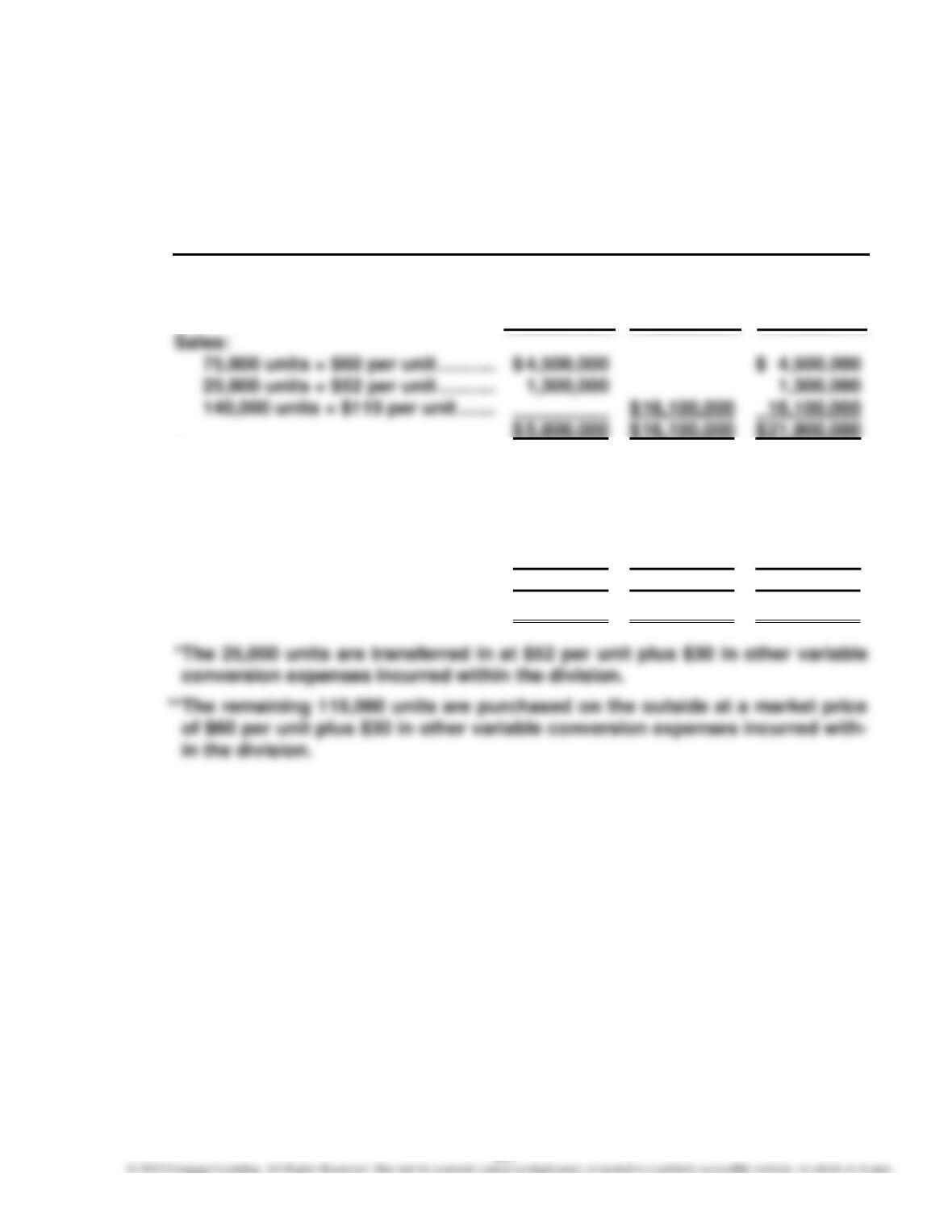

P14–6, Continued

3.

PENDRAY SCIENTIFIC INC.

Divisional Income Statements

For the Year Ended December 31, 20Y5

GPS Communication

Systems Systems Total

Expenses:

Variable:

100,000 units × $40 per unit ….. $ 4,000,000 $ 4,000,000

25,000 units × $82* per unit …… $ 2,050,000 2,050,000

115,000 units × $90** per unit .. 10,350,000 10,350,000

Fixed ………………………………………. 250,000 500,000 750,000

Total expenses …………………….. $ 4,250,000 $ 12,900,000 $ 17,150,000

Income from operations ……………….. $ 1,550,000 $ 3,200,000 $ 4,750,000

482

P14–6, Concluded

4. The GPS Systems Division’s income from operations would increase by

$225,000:

Operations from Income sDivision’

)(Supplying

Systems GPS in Increase

=

Price

Transfer

–

Unit per Cost

Variable

×

dTransferre

Units

$225,000 = ($49 – $40) × 25,000

Operations from Income sDivision’

g)(Purchasin Systems

ionCommunicat in Increase

=

Price

Market

–

Price

Transfer

×

dTransferre

Units

$275,000 = ($60 – $49) × 25,000

Operations from Income s‘Scientific

Pendray in Increase

=

Price

Market

–

Unit per Cost

Variable

×

dTransferre

Units

$500,000 = ($60 – $40) × 25,000

The increase in total company income from operations is also equal to the

sum of the increases in the division incomes from operations.

483

CASES

Case 14–1

This scenario is a negotiation between two divisions. Newt is not behaving unethically

by attempting to get a good price from the Optic Lens Division. Also, he is not behav-

ing unethically because he refuses market price. This may not seem “fair,” but price

negotiation is a very typical business activity and is part of Newt’s job. It would be un–

Case 14–2

The department head is responsible for the quantity of service, but not the source of

the service (i.e., not the price). Most accountants would hold the department head re–

sponsible for the cost by transferring the cost of the brochures to the Customer Ser–

vice Department, even though the price is 15% higher than could be obtained from the

outside. This may not seem fair, but it does control the use of internal services to

some degree. If there were no internal transfer price, departments would view the Pub–

Case 14–3

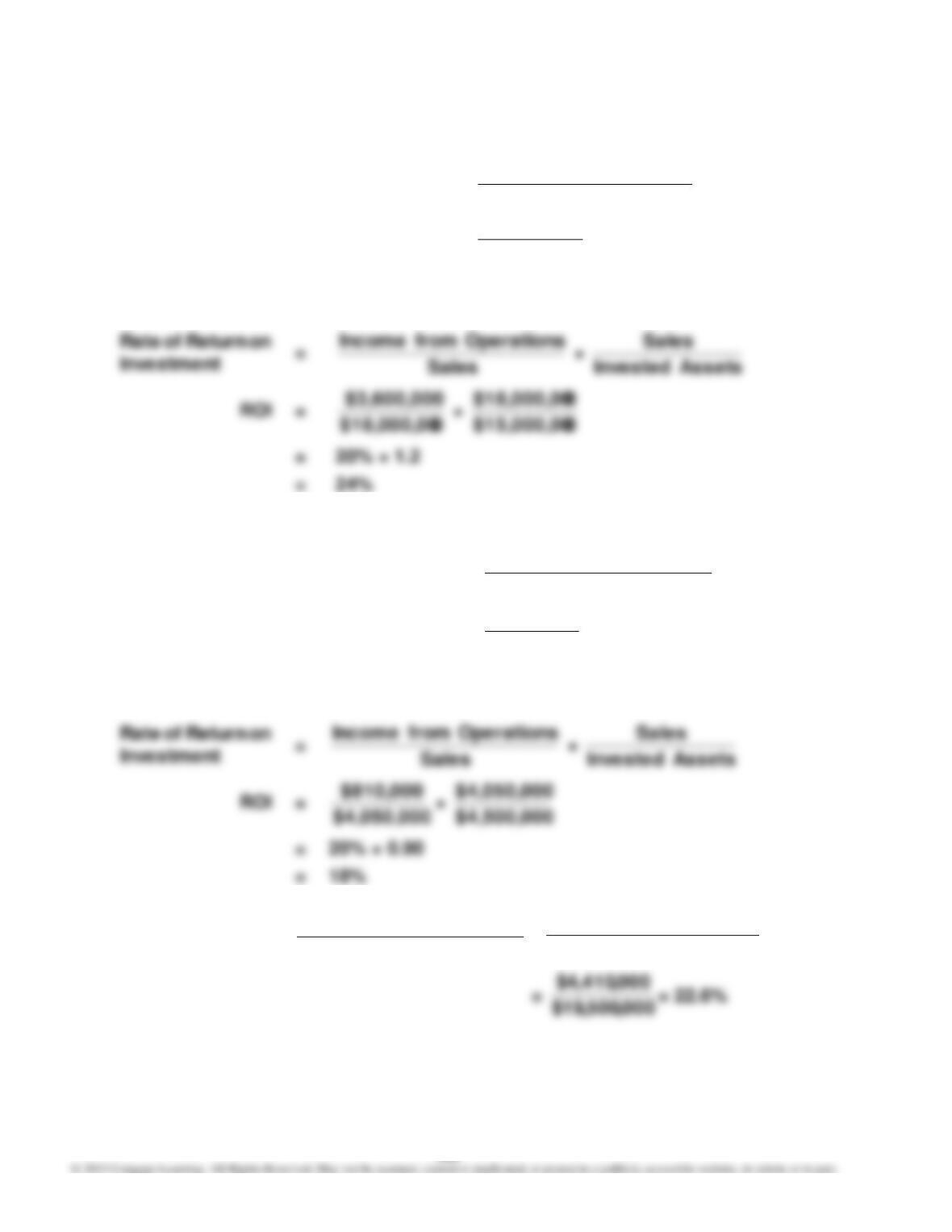

1. The rate of return on invested assets is computed as follows:

Cereal Produce Snacks

2. Not all projects that have greater than a 10% rate of return would be accepted.

This is because any project that is accepted between the 10% minimum and

their existing ROI would cause their ROI to drop. This is true because of aver-

3.

Investment

on Return of Rate

=

AssetsInvested

Operations from Income

=

000,000,5$ + 000,000,8$ + 000,500,4$

000,080,1$ + 000,960$ + 000,432$

=

000,500,17$

000,472,2$

= 14.1%

4. There are two approaches to improving Dixie Foods’ overall rate of return of

14.1%: (1) improving the profit margin or (2) improving the investment turno-

ver. The profit margin for all three divisions is as follows:

Cereal 8% ($432,000 ÷ $5,400,000)

Produce 6% ($960,000 ÷ $16,000,000)

Case 14–4

1.

20Y6 20Y7 20Y8

Profit margin …………………………………….. 30% 35% 40%

Computations:

2.

20Y6 20Y7 20Y8

Investment turnover ………………………….. 1.5 1.0 0.7

Computations:

20Y6: $3,000,000 ÷ $2,000,000 = 1.5

3.

20Y6 20Y7 20Y8

Rate of return on investment …………….. 45% 35% 28%

Computations:

20Y6: $900,000 ÷ $2,000,000 = 45%

4. Hal is concerned about the Laser Division because the return on investment ap–

pears to be deteriorating over the 20Y6–20Y8 operating periods. This is happening

even though the profit margin is increasing over this time period. In order for this to

occur, the investment turnover must be dropping, which is the case in part (2).

486

Case 14–5

1. Rate of Return on Investment =

AssetsInvested

Operations from Income

ROI =

0$15,000,00

$3,600,000

= 24%

or

0$18,000,00

$3,600,000

0$15,000,00

2. $100,000 (10 × $10,000 = $100,000, where 10 = 24% – 14%)

3. Rate of Return on Investment =

Assets Invested

Operations from Income

ROI =

$4,500,000

$810,000

= 18%

or

$4,050,000

$810,000

4.

Investment

on Return of Rate

=

Assets Invested

Operations from Income

=

000,500,4$ + 000,000,15$

000,810$ + 000,600,3$

487

Case 14–5, Concluded

5. Even though the addition of the new product line would increase the overall

company rate of return on investment, its addition would decrease the

6. Use of residual income as a performance measure and as the basis for grant-

ing bonuses would motivate division managers to accept investment oppor-

tunities that exceed a minimum rate of return. If the minimum rate of return

was set at 14%, the overall company average rate of return, any investment

opportunity whose rate exceeded 14% would be viewed as acceptable. If this

Projected income from operations of new product line ……….. $810,000

Minimum amount of desired income from operations

($4,500,000 × 14%) ………………………………………………………… 630,000

Residual income from new product line ……………………………… $180,000

The manager’s bonus could then be calculated as a percent of residual in-

come. In this case, a bonus equal to 6.7% of residual income would achieve a

bonus similar to the initial plan:

488

Case 14–6

This activity is designed to introduce students to two very popular divisional

performance measurement approaches, the balanced scorecard and economic

value added (EVA). Both methods are getting very strong support in corporate

America. The two consulting firms’ home pages provided in this activity have

financial measure that is strongly oriented to maximizing wealth to the share-

holder. Hopefully, the students will recognize EVA as a specific application of the

residual income concept. EVA’s strength is in its simplicity and its apparent

association with wealth maximization (share values). It is interesting to note that

the two methods flow from two different philosophies. The balanced scorecard

takes a multiple stakeholder perspective, while EVA is taking a stockholder