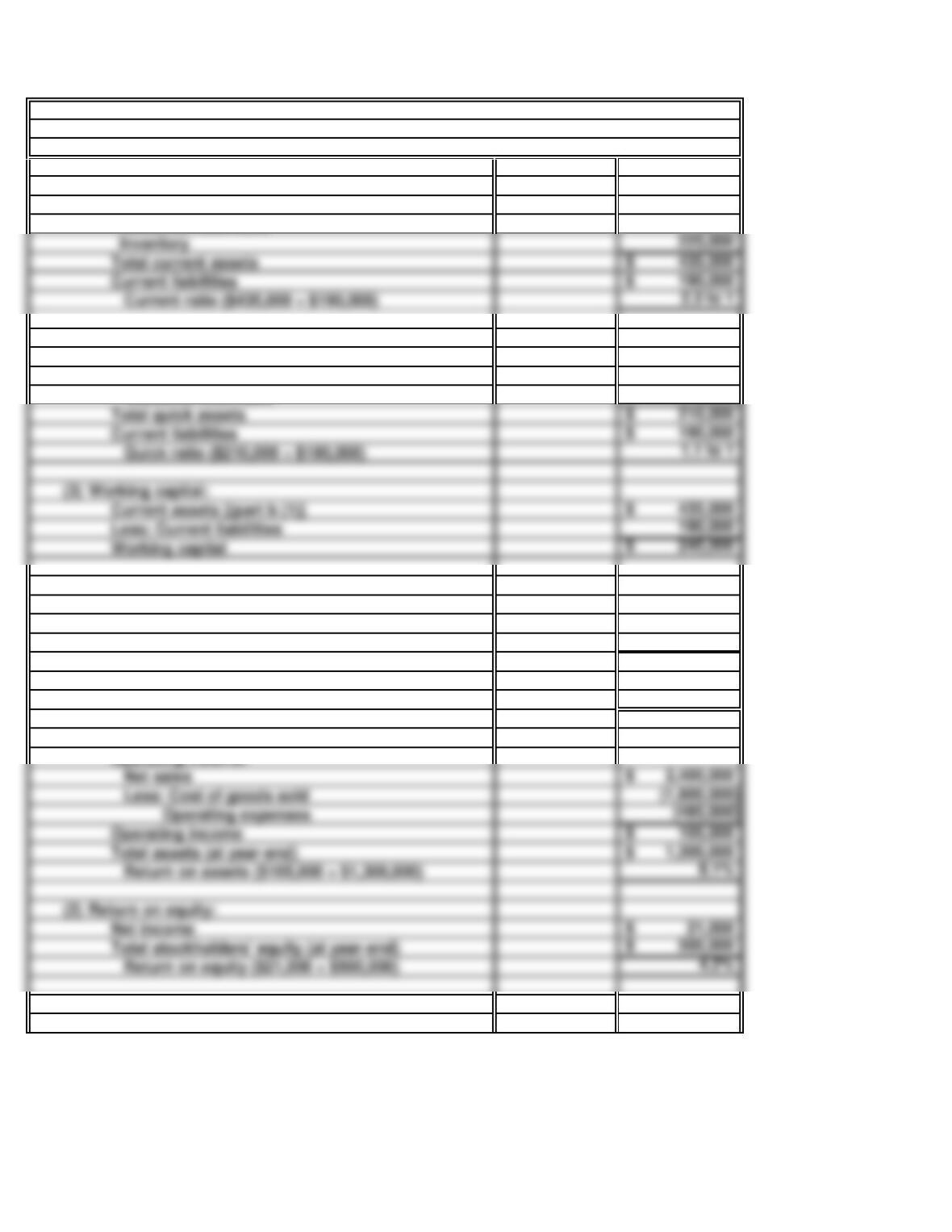

25 Minutes, Easy

(Dollars in

Millions)

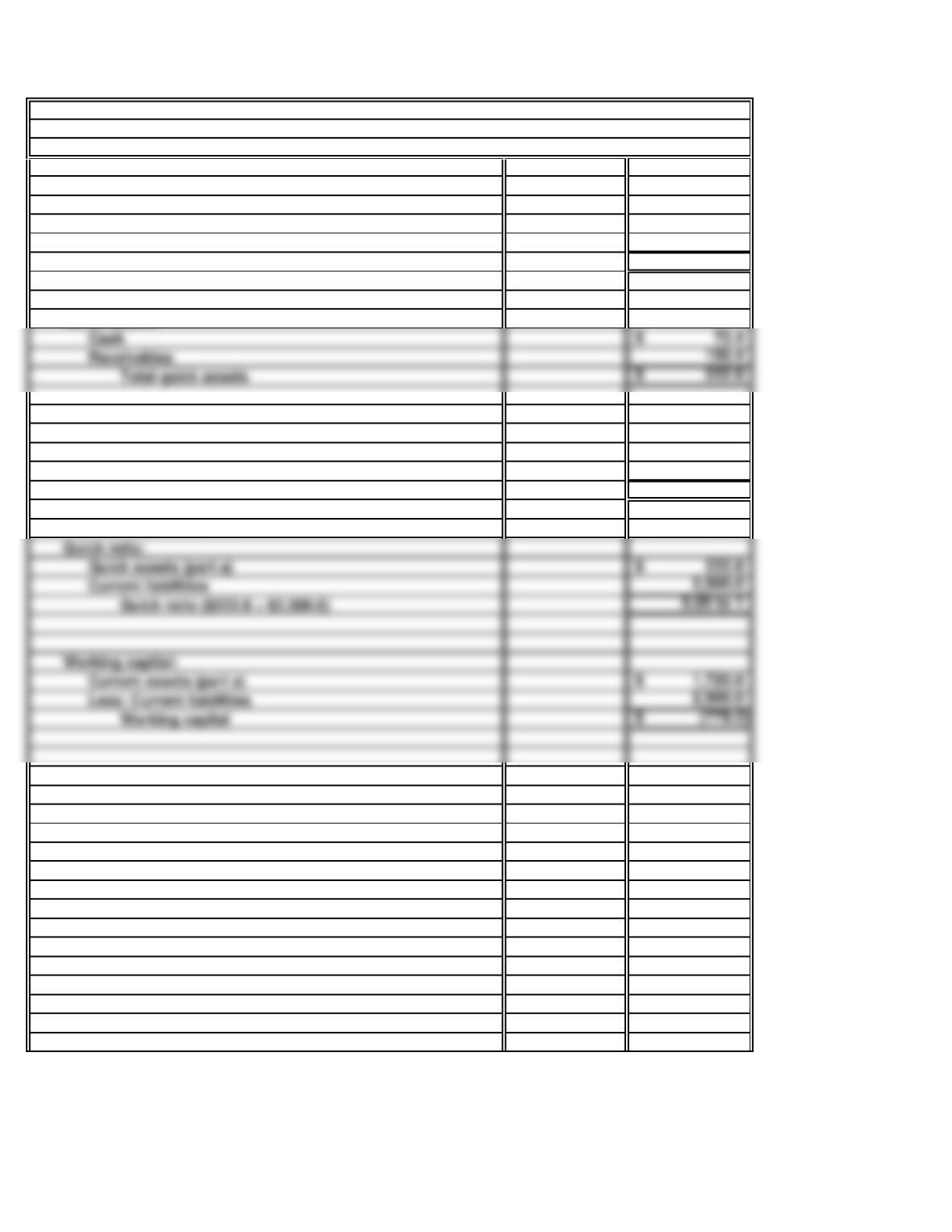

a. Current assets:

(

Cash 72.4$

Receivables 150.4

Merchandise inventories 1,400.0

Prepaid expenses 98.0

Total current assets 1,720.8$

Quick assets:

b. Current ratio:

(

Current assets (part a) 1,720.8$

Current liabilities 2,500.0

Current ratio ($1,720.8 ÷ $2,500.0) 0.69 to 1

Quick ratio:

(

Quick assets (part a) 222.8$

Working capital:

(

Current assets (part a) 1,720.8$

PROBLEM 14.4B

CHEZO, INC.

(

Receivables 150.4

Total quick assets 222.8$

d.

e.

In evaluating Chezo’s liquidity, it would be useful to review the company’s financial position

PROBLEM 14.4B

CHEZO, INC. (concluded)

Due to characteristics of the industry, cheese stores tend to have smaller amounts of current

35 Minutes, Medium

(Dollars in

Thousands)

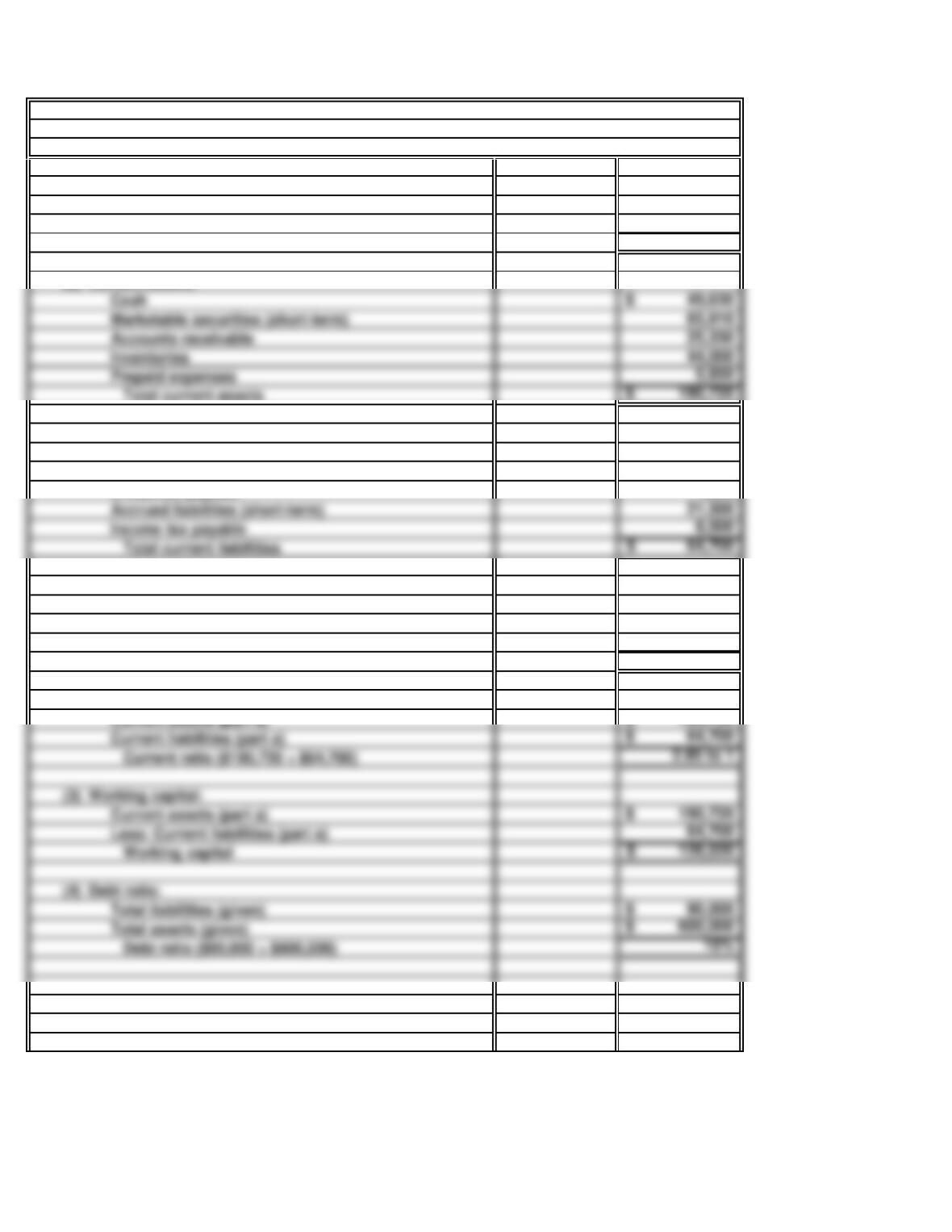

a. (1) Quick assets:

(

(

Cash 49,630$

Marketable securities (short-term) 65,910

Accounts receivable 25,330

Total quick assets 140,870$

(2) Current assets:

Total current assets 190,720$

(3) Current liabilities:

(

(

Notes payable to banks (due within one year) 28,000$

Accounts payable 4,900

Dividends payable 1,800

Accrued liabilities (short-term) 21,500

Income tax payable 8,500

Total current liabilities 64,700$

b. (1) Quick ratio:

(

Quick assets (part a) 140,870$

Current liabilities (part a) 64,700

Quick ratio: ($140,870 ÷ $64,700) 2.18 to 1

(2) Current ratio:

Current assets (part a) 190,720$

Current liabilities (part a) 64,700$

(

(

Current assets (part a) 190,720$

Less: Current liabilities (part a) 64,700

Working capital 126,020$

(4) Debt ratio:

Total liabilities (given) 90,000$

Total assets (given) 600,000$

PROBLEM 14.5B

SWEET AS SUGAR, INC.

(

(

Marketable securities (short-term) 65,910

Accounts receivable 25,330

Prepaid expenses 5,850

c. (1)

(2)

(3)

From the viewpoint of stockholders, Sweet as Sugar may appear overly liquid. Current

PROBLEM 14.5B

SWEET AS SUGAR, INC. (concluded)

From the viewpoint of short-term creditors, Sweet as Sugar appears highly liquid. Its

Long-term creditors should feel relatively secure. Not only is the company highly liquid,

45 Minutes, Strong

b. (1) Current ratio:

(

(

Current assets:

Cash 35,000$

Accounts receivable 175,000

(2) Quick ratio:

(

(

Quick assets:

Cash 35,000$

Accounts receivable 175,000

Total quick assets 210,000$

Current liabilities 190,000$

Quick ratio ($210,000 ÷ $190,000) 1.1 to 1

(3) Working capital:

(

(

Current assets [(part b (1)] 435,000$

Less: Current liabilities 190,000

Working capital 245,000$

(4) Debt ratio:

(

Total liabilities

Total assets 1,300,000$

Less: Total stockholders’ equity 500,000

Total liabilities 800,000$

Total assets 1,300,000$

Debt ratio ($800,000 ÷ $1,300,000) 61.5%

d. (1) Return on assets:

Operating income:

Net sales 2,400,000$

Less: Cost of goods sold (1,800,000)

Operating income 105,000$

(

(

Total assets (at year-end) 1,300,000$

Return on assets ($105,000 ÷ $1,300,000) 8.1%

Net income 21,000$

Total stockholders’ equity (at year-end) 500,000$

Return on equity ($21,000 ÷ $500,000) 4.2%

PROBLEM 14.6B

HAMILTON STORES

Parts a, c, e, and f appear on the following page.

Inventory 225,000

Total current assets 435,000$

Current liabilities 190,000$

Current ratio ($435,000 ÷ $190,000) 2.3 to 1

a.

c.

e.

f. (1)

(2)

PROBLEM 14.6B

HAMILTON STORES (concluded)

In the statement of cash flows, amounts are reported on a cash basis, whereas in the income

statement, they are reported under the accrual basis. Apparently $8,000 of the interest

By traditional measures, the company’s current ratio (2.3 to 1) and quick ratio (1.1 to 1)

appear quite adequate. The company also generates a positive cash flow from operating

The 8.1% return on assets is adequate by traditional standards. However, the 4.2% return on

equity is very low. The problem arises because of Hamilton Stores’ relatively large interest

expense, which is stated as $80,000 for the year.

At year-end, Hamilton Stores has total liabilities of $800,000 ($1,300,000 total assets less

61.5% is high for American industry. Also, debt is continuing to rise. During the current

Long-term creditors do not appear to have a high margin of safety. The debt ratio of

If the current year is typical, Hamilton Stores can not continue its $24,000 annual

dividend. In the current year, investing activities consumed more than the net cash flow

25 Minutes, Medium

(Dollar Amounts

in Thousands)

b. Working capital:

(1) Beginning of year ($43,000 – $54,000) (11,000)$

(2) End of year ($82,000 – $75,000) 7,000$

d. (1) Return on average total assets:

c.

e.

Rochester’s management appears to be utilizing the company’s resources in more than a

PROBLEM 14.7B

ROCHESTER CORPORATION

c. and e.

Rochester’s short-term debt-paying ability appears to be improving. In the course of the year,

(1) Beginning of year ($43,000 ÷ $54,000) 0.80 to 1

25 Minutes, Medium

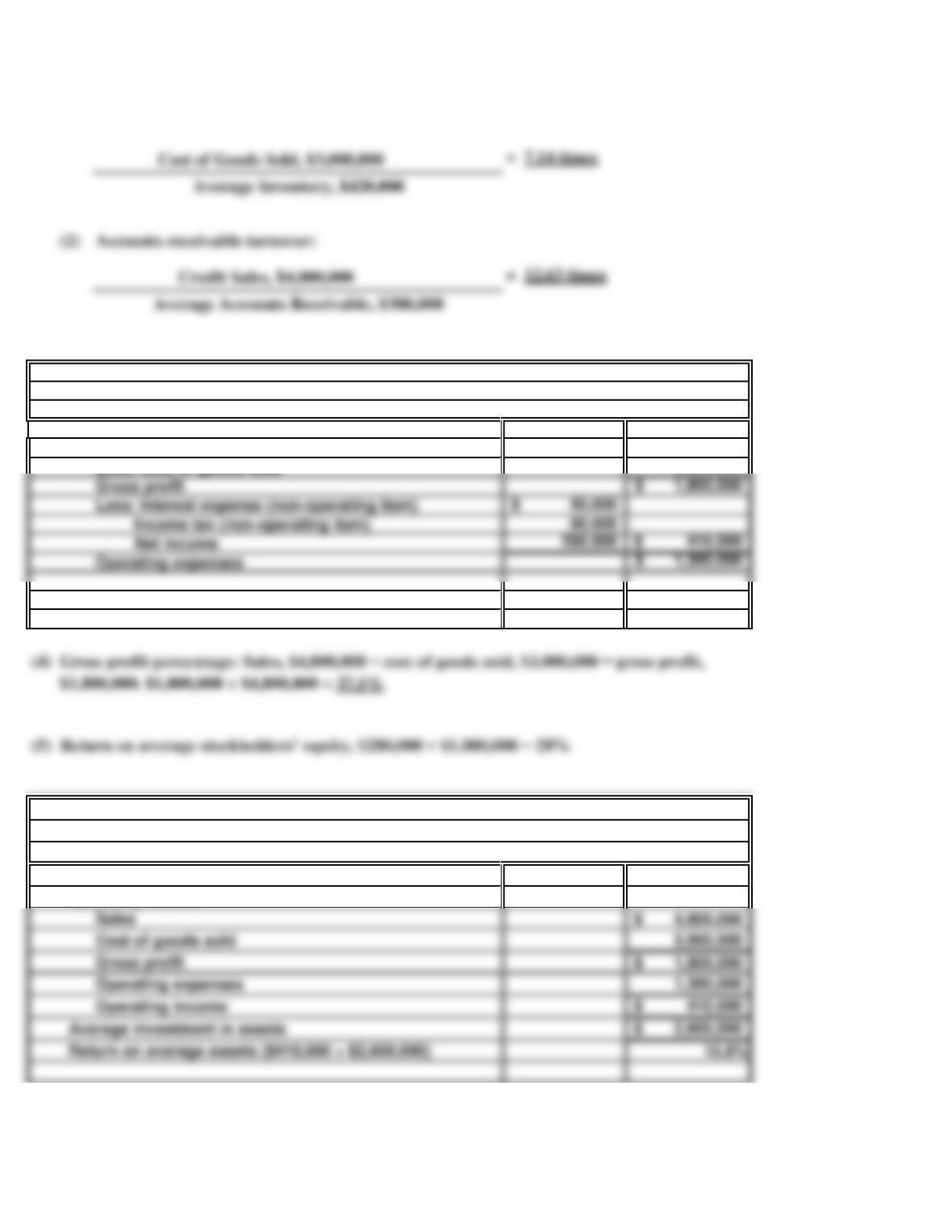

a. (1) Inventory turnover:

(3) Total operating expenses:

Sales 4,800,000$

Less: Cost of goods sold 3,000,000

Gross profit 1,800,000$

(6) Return on average assets:

Operating income:

PROBLEM 14.8B

SOLAR SYSTEMS, INC.

b.

Obtaining the loan will be desirable to stockholders because the return on average assets

PROBLEM 14.8B

SOLAR SYSTEMS, INC. (concluded)

35 Minutes, Medium

a.

THIS THAT

STAR STAR

(1) Working capital:

($95,000 + $100,000 + $50,000 – $120,000) 125,000$

($47,000 + $90,000 + $160,000 – $110,000) 187,000$

(3) Quick ratio:

($95,000 + $100,000) ÷ $120,000 1.63 to 1

($47,000 + $90,000) ÷ $110,000 1.25 to 1

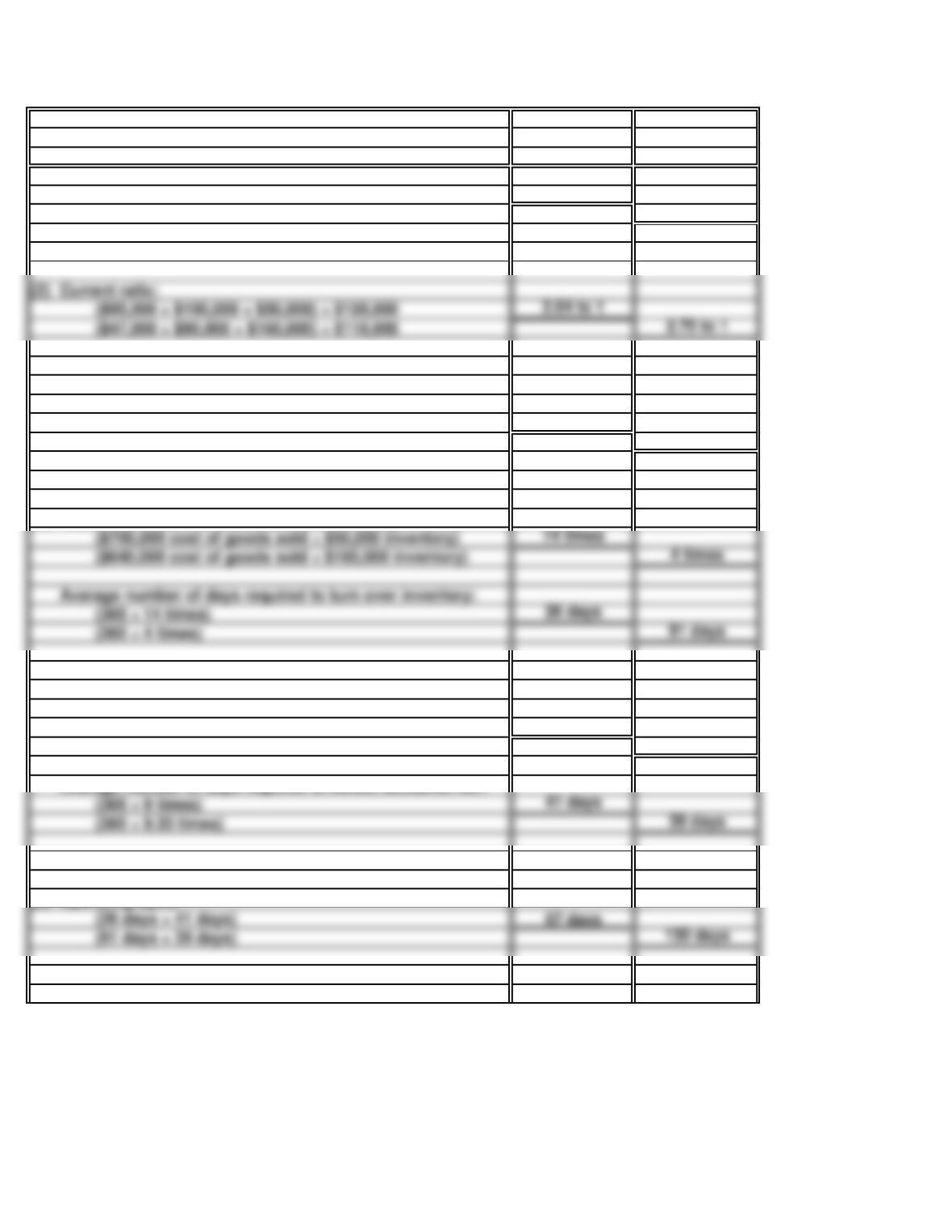

(4) Number of times inventory turned over during the year:

($700,000 cost of goods sold ÷ $50,000 inventory) 14 times

($640,000 cost of goods sold ÷ $160,000 inventory) 4 times

Average number of days required to turn over inventory:

(365 ÷ 14 times) 26 days

(365 ÷ 4 times) 91 days

(5) Number of times accounts receivable turned over:

($900,000 credit sales ÷ $100,000 accounts receivable) 9 times

($840,000 credit sales ÷ $90,000 accounts receivable) 9.33 times

Average number of days required to collect accounts rec.:

(365 ÷ 9 times) 41 days

(365 ÷ 9.33 times) 39 days

(6) Operating cycle:

(26 days + 41 days) 67 days

(91 days + 39 days) 130 days

PROBLEM 14.9B

THIS STAR, INC. AND

THAT STAR, INC.

(2) Current ratio:

($95,000 + $100,000 + $50,000) ÷ $120,000 2.04 to 1

($47,000 + $90,000 + $160,000) ÷ $110,000 2.70 to 1

b.

PROBLEM 14.9B

THIS STAR, INC. AND THAT STAR, INC. (concluded)

Although THAT Star, Inc., has a larger dollar amount of working capital and a higher

current ratio, THIS Star, Inc. has the higher-quality working capital. The quality of working

capital is determined by the nature of the current assets comprising the working capital and

25 Minutes, Medium

a.

b.

c.

Holcomb computed the 350% increase in fourth-quarter profits by comparing the fourth-

quarter profits of 2018 to those of the third quarter. The computation is:

SOLUTIONS TO CRITICAL THINKING CASES

HOLIDAY GREETING CARDS

CASE 14.1

The 350% increase in fourth-quarter profits, developed by comparing fourth-quarter profits

to those of the third quarter, is misleading because of the cyclical nature of Holiday Greeting

The appropriate computation of the percentage change in Holiday’s fourth-quarter earnings

for 2018 is a decrease of 10%, computed as follows:

15 Minutes, Easy

Nebraska The

Steak Ranch Stockyards

a. $75,000 $24,000

Current liabilities ………………………………………..

$30,000 $30,000

b.

c.

Nebraska Steak Ranch would become as good a credit risk as The Stockyards if West

personally guarantees the loan to the corporation. This essentially removes the difference in

risk that the bank would be taking in loaning to the two companies.

Based solely upon the financial data presented here, neither restaurant appears to be a good

Considering the form of business organization, however, The Stockyards appears to be the

better credit risk. The reason is that this business is organized as a sole proprietorship. A loan

to this business is actually a loan to its owner, Joe West, because he is personally liable for the

Note to instructor: It is a common practice for wealthy individuals to organize businesses as

corporations for the specific purpose of limiting the owner’s personal liability.

CASE 14.2

THIRD NEBRASKA BANK

Current assets …………………………………………..

$45,000

($75,000 ÷ $30,000) ………………………………..

($24,000 ÷ $30,000) ………………………………..

a. (1)

(2)

(3)

b.

CASE 14.3

NASHVILLE DO-IT-YOURSELF

25 Minutes, Strong

Decrease. Offering customers a cash discount to speed up the collection of accounts

Note to instructor: This concept can be illustrated by assuming that all of the current liabilities were

paid. In this case, some current assets would remain, current liabilities would be reduced to zero,

and the current ratio would be infinite.

by the same amount. This tends to force the current ratio closer to 1 to 1 which, for

Nashville Do-It-Yourself Centers, would be a decline. In essence, purchasing inventory on

account has the opposite effect of paying current liabilities, discussed in part (1).

Decrease. Purchasing inventory on account increases current assets and current liabilities

Increase. Paying current liabilities reduces current assets and current liabilities by the

purchases of equipment or expenditures for repairs or maintenance, will improve the current

One means of improving the current ratio is to increase current assets without increasing

current liabilities. This could be done by selling noncurrent assets, by borrowing cash on a long-

term basis, or by the owners investing cash in the business. The increase in the current ratio

would be magnified if the proceeds from these transactions were used to reduce current

liabilities.

No time estimate, Strong

ETHICS, FRAUD & CORPORATE GOVERNANCE

Board Expertise — It is typically advantageous if board members have experience serving on the

CASE 14.4

Compensation committee — Companies should have a separate committee of the board to handle

Board structure — Shareholder activists prefer boards where directors stand for reelection each

Although there are many possible “solutions” to this case, depending on the companies that

students choose for analysis, students should talk about most of these factors in evaluating the

quality of a company’s board of directors.

Board composition — The board of directors should be comprised of a majority of independent

Nominating committee — Companies should have a separate committee of the board to handle

EVALUATING CORPORATE GOVERNANCE QUALITY

CASE 14.4

(concluded)

EVALUATING CORPORATE GOVERNANCE QUALITY

Chairman/CEO Separation — Shareholder activities prefer that the same individual who serves

the independent members of the board.

Response to Shareholder Proposals — Shareholders are able to put forth proposals for vote at

Board Attendance — A board cannot be effective if it never meets or if directors fail to attend the

meetings that are held. An effective board should normally meet at least six times per year, and

No time estimate, Strong

Current ratio

c.

Ease of transferring information and applying it to analytical techniques.

Availability of extensive amounts of information from a single source.

Technology-based access and ease of storing and printing information.

Again, student responses will likely vary, but reasons for the popularity of the Internet for

receiving financial information include the following:

Timeliness and ease and frequency with which information can be updated.

CASE 14.5

Student responses will vary, but they should indicate an understanding that companies have

unique operating characteristics, and understanding those before diving into financial

Because students can choose both the company and the ratios they compute, no set answer

can be given for this question. The following are probably the ratios in the categories of

liquidity and profitability that are most likely to be selected by students:

EVALUATING LIQUIDITY AND PROFITABILITY

Liquidity

INTERNET

a.

b.

Quick ratio

Inventory turnover

Receivables turnover

Profitability