859

Problem 14-8BB (Concluded)

Part 4

2017

June 30

Bond Interest Expense …………………………..

7,940

Dec. 31

Bond Interest Expense …………………………..

7,969

860

Problem 14-9BB (45 minutes)

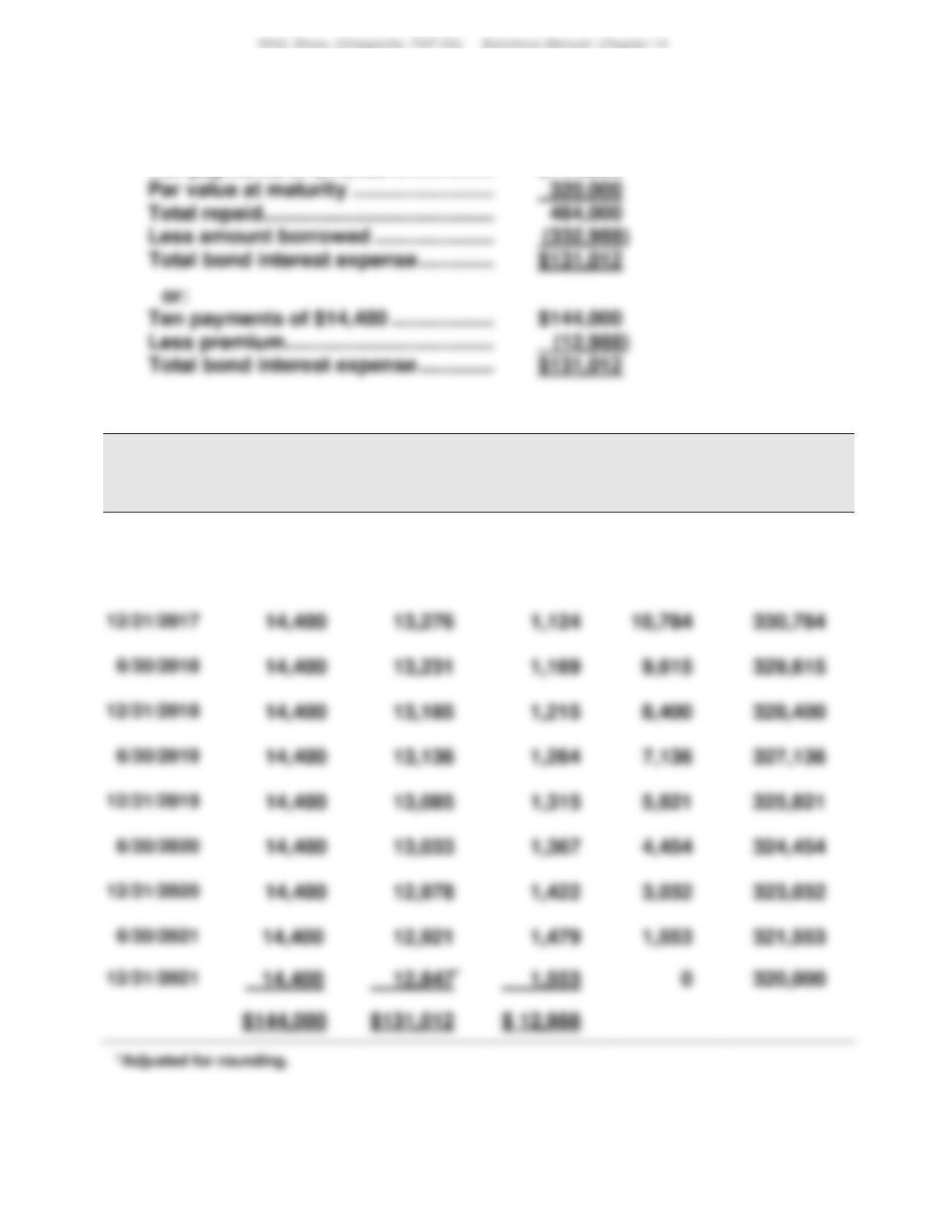

Part 1

Ten payments of $14,400 ……………………..

$144,000

Par value at maturity …………………………..

Total repaid ………………………………………….

Less amount borrowed ………………………..

Ten payments of $14,400 ……………………..

$144,000

Less premium………………………………………

Part 2

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[4.5% x $320,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$320,000 + (D)]

1/01/2017

$12,988

$332,988

6/30/2017

$ 14,400

$ 13,320

$ 1,080

11,908

331,908

6/30/2019

13,136

327,136

6/30/2021

12,921

1,553

321,553

$144,000

$131,012

861

Problem 14-9BB (Concluded)

Part 3

2017

June 30

Bond Interest Expense …………………………..

13,320

Dec. 31

Bond Interest Expense …………………………..

13,276

Part 4

As of December 31, 2019

Cash Flow

Table

Table Value*

Amount

Present Value

Par value ……………..

B.1

0.8548

$320,000

$273,536

Comparison to Part 2 Table

Except for a small rounding difference, this present value ($325,807) equals

862

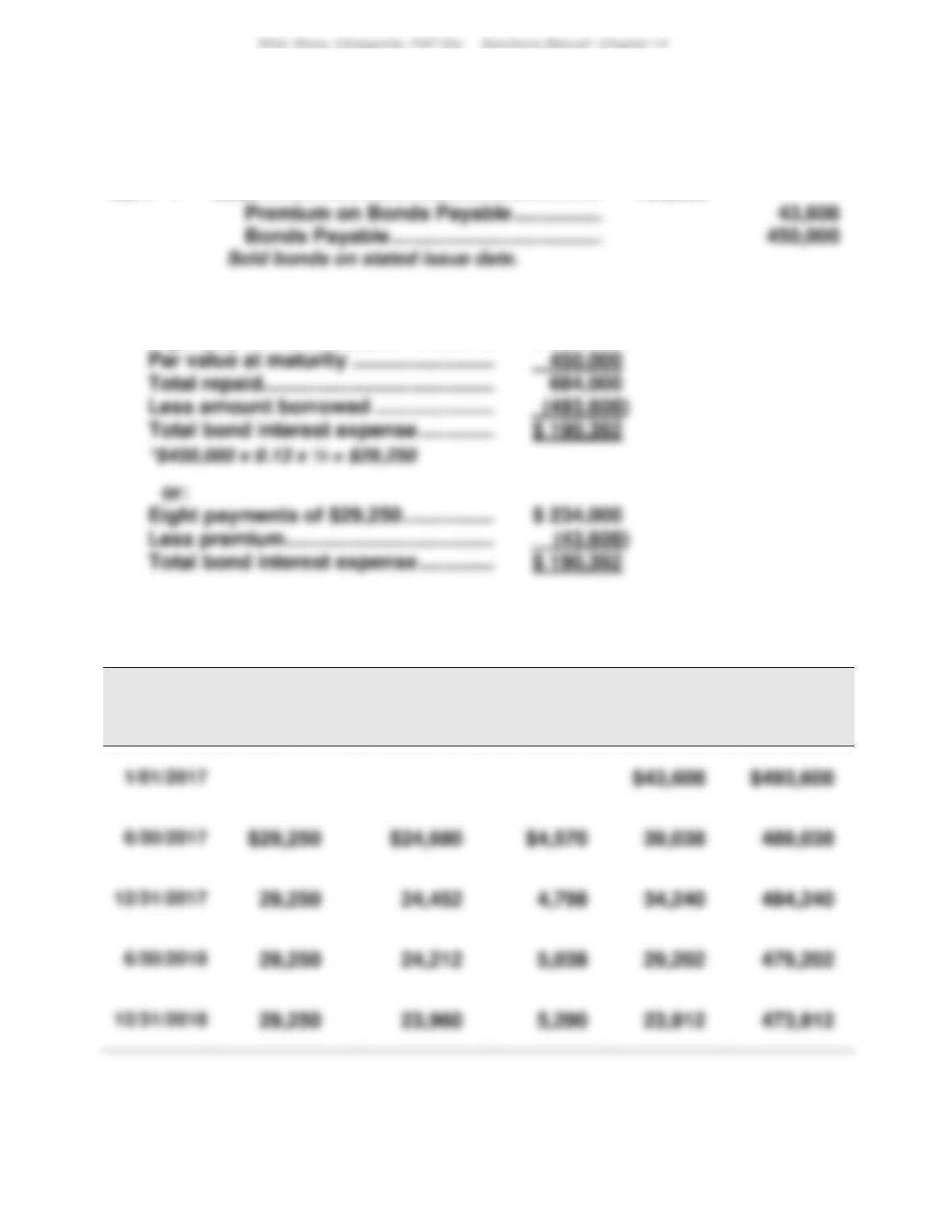

Problem 14-10BB (70 minutes)

Part 1

2017

Jan. 1

Cash ……………………………………………………….

493,608

Part 2

Eight payments of $29,250* ………………….

$ 234,000

Eight payments of $29,250 ……………………

$ 234,000

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[6.5% x $450,000]

(B)

Bond Interest

Expense

[5% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$450,000 + (D)]

863

Problem 14-10BB (Concluded)

Part 4

2017

Premium on Bonds Payable …………………………..

2017

Premium on Bonds Payable …………………………..

Part 5

Bonds Payable ……………………………………………………..

Premium on Bonds Payable …………………………..

Part 6

If the market rate on the issue date had been 14% instead of 10%, the bonds

would have sold at a discount because the contract rate of 13% would have been

864

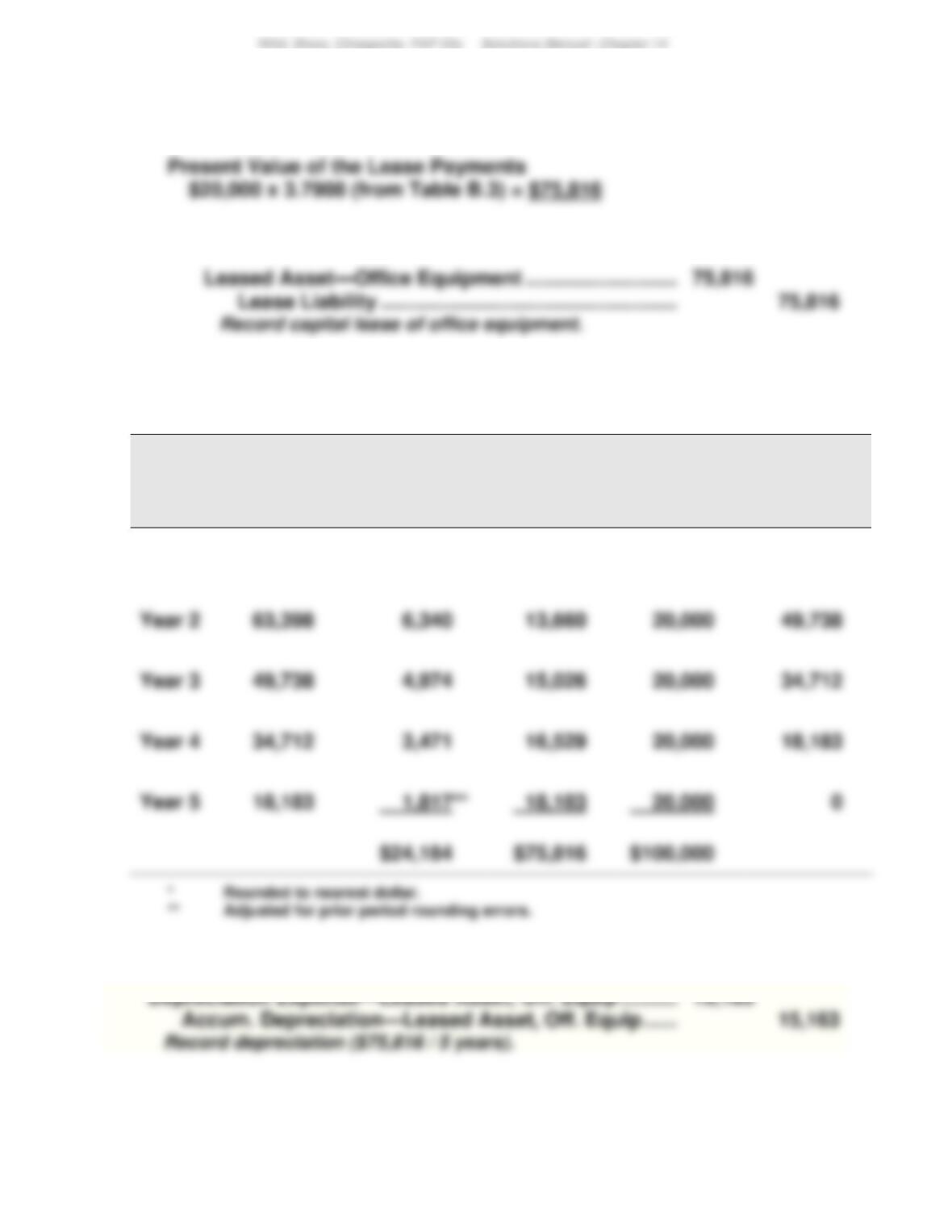

Problem 14-11BD (35 minutes)

Part 1

Part 2

Part 3

Capital Lease Liability Payment (Amortization) Schedule

Period

Ending

Date

Beginning

Balance of

Lease

Liability

Interest on

Lease

Liability

(10%)

Reduction

of Lease

Liability

Cash

Lease

Payment

Ending

Balance of

Lease

Liability

Year 1

$75,816

$ 7,582*

$12,418

$ 20,000

$63,398

Year 3

Year 5

20,000

Part 4

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 14

865

SERIAL PROBLEM — SP 14

Serial Problem — SP 14, Business Solutions (75 minutes)

Part 1

Part 2

Assume the secured loan is taken, then the percent of assets financed by:

Part 3

Santana Rey should understand the risks she is taking by borrowing funds

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 14

Reporting in Action — BTN 14-1

1. Apple reported long-term debt of $53,463 million as of September 26,

3. Assuming that Apple had $100 million carrying value of convertible

bonds that convert into 20,000 shares of stock, the following entry

would be recorded upon conversion:

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 14

867

Comparative Analysis — BTN 14-2

1. Apple’s current year debt–to-equity ratio = $171,124 / $119,355= 1.43

2. For both years, Apple’s debt–to-equity ratio is above that of the industry

average of 0.44. This implies that its debt levels are more risky than that

Ethics Challenge — BTN 14-3

1. The ethics of the Traverse County officials are questionable. The

financial impact of the leasing arrangement is the same as bond

2. Because the lease requires payments of a non-binding nature, investors

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 14

868

Communicating in Practice — BTN 14-4

MEMORANDUM

TO:

FROM:

SUBJECT:

The body of the memorandum should make the following points:

The associate is confused about the concept of a bond premium. Bonds

that sell at a premium provide the issuing company more cash than they

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 14

869

Taking It to the Net — BTN 14-5

1. Home Depot’s long-term liabilities as of January 31, 2016, follow:

2 a. These Home Depot notes offer a 5.875% interest rate. If the interest

rate for similar notes from companies with similar risk was 5.875%,

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 14

870

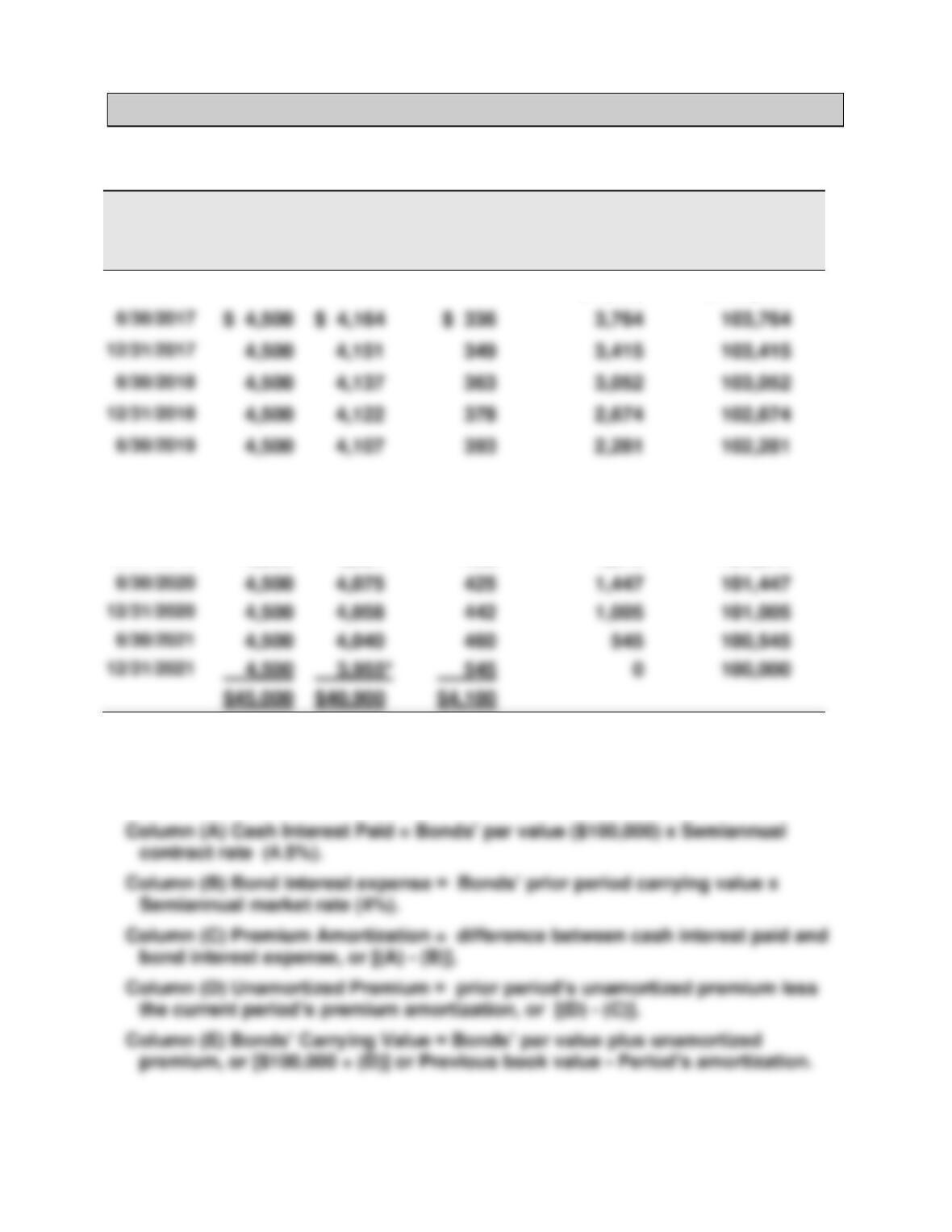

Teamwork in Action — BTN 14-6

Parts 1 and 2

Effective Interest Amortization of Bond Premium

Semi-

annual

Period-end

(A)

Cash

Interest

Paid

(B)

Bond

Interest

Expense

(C)

Premium

Amortization

(D)

Unamortized

Premium

(E)

Carrying

Value

1/01/2017

$ 4,100

$ 104,100

Since teams generally have 4 or 5 members, the team solution will likely end about

here. The remainder of the table is shown for help in answering part 3.

12/31/2019

4,500

4,091

409

1,872

101,872

4,500

4,075

1,447

101,447

4,500

4,058

1,005

101,005

100,000

*Discrepancy due to rounding.

The following computations should be articulated by team members as

each line is explained and prepared:

6/30/2017

6/30/2019

871

Teamwork in Action (Concluded)

Part 3

Without completing the table, team members should be able to project the

final number in the first column and for each of the columns (A), (D), and

(E). Specifically:

Part 4

Total Bond interest expense = Interest Paid – Premium

Part 5 List likely includes:

Similarities

Differences

columns (A), (B), and (E).

c. Computations in

will follow the same format.

c. Carrying value (E) will increase as we amortize a

a. Table column headings

a. Column (C) will be Discount Amortization and

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 14

872

Entrepreneurial Decision — BTN 14-7

Part 1

The table below reveals how the five alternative interest-bearing notes

would affect this company’s interest expense, net income, equity, and

return on equity (net income/equity):

Alternative Notes for Expansion

Current 10% Note 15% Note 16% Note 17% Note 20% Note

Income before

Part 2

The analysis in Part 1 illustrates the general rule (called “financial

leverage” or “trading on the equity”): When a company earns a higher

Wild, Shaw, Chiappetta, FAP 23e Solutions Manual: Chapter 14

Hitting the Road — BTN 14-8

Students’ answers will depend on the municipality and time period chosen

Global Decision — BTN 14-9

1. Samsung’s current year debt–to-equity ratio (in KRW millions):

2. Samsung’s debt-to–equity ratio decreased slightly from the prior year to

the current year. For the current and prior years, Samsung’s debt–to–