CHAPTER 14

SOLUTIONS TO EXERCISES—SET B

EXERCISE 14-1B

(a) June 15 Cash Dividends (150,000 X $1) ………… 150,000

Dividends Payable …………………… 150,000

July 10 Dividends Payable ………………………….. 150,000

Cash ……………………………………….. 150,000

EXERCISE 14-2B

(a)

2016

2017

2018

Total dividend declaration

Allocation to preferred stock

Remainder to common stock

$5,000

(5,000)

$ 0

$12,000

(6,000)

$ 6,000

$28,000

(6,000)

$22,000

Remainder to common stock

$ 0

$ 3,000

$21,000

(c) Dec. 31 Cash Dividends…………………………………. 28,000

Dividends Payable ……………………… 28,000

EXERCISE 14-3B

(a) Stock Dividends (24,000* X $18) ………………………. 432,000

Common Stock Dividends Distributable

(24,000 X $10) ………………………………………. 240,000

Paid-in Capital in Excess of Par—

(b) Stock Dividends (42,000* X $20) ………………………. 840,000

Common Stock Dividends Distributable

(42,000 X $5) ………………………………………… 210,000

EXERCISE 14-4B

Before

Action

After

Stock

Dividend

After

Stock

Split

Stockholders’ equity

Paid-in capital

Common stock

In excess of par

$ 500,000

0

$ 525,000

10,000

$ 500,000

0

EXERCISE 14-5B

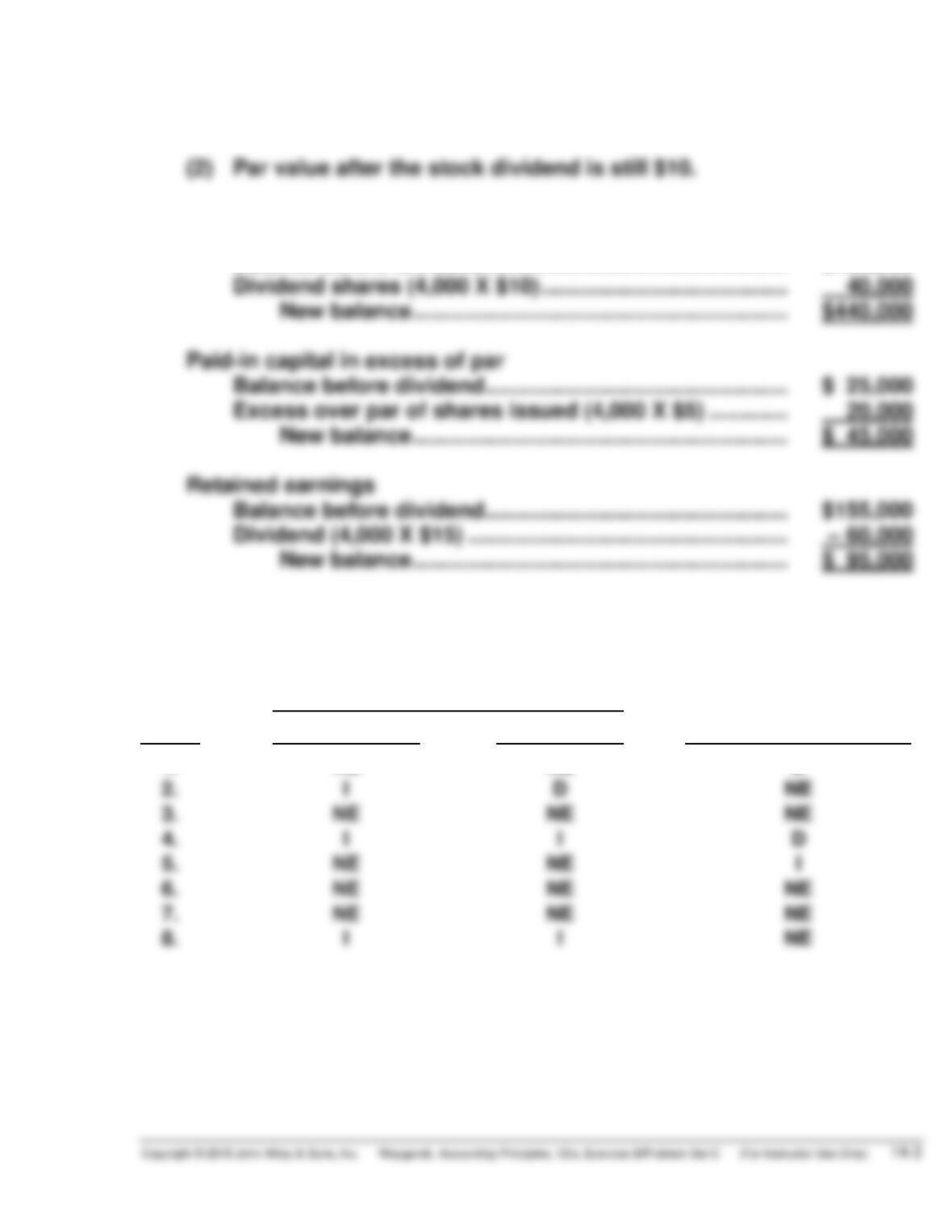

(a) (1) Par value before the stock dividend was $10.

(b) Common stock

Balance before dividend …………………………..…………….. $400,000

Dividend shares (4,000 X $10) …………………………………. 40,000

New balance ……………………………………………………. $440,000

EXERCISE 14-6B

Paid-in Capital

Item

Capital Stock

Additional

Retained Earnings

1.

2.

NE

I

NE

D

D

NE

EXERCISE 14-7B

1. Dec. 31 Retained Earnings …………………….. 50,000

Interest Expense ………………… 50,000

EXERCISE 14-8B

ZUNIGA CORPORATION

Retained Earnings Statement

For the Year Ended December 31, 2017

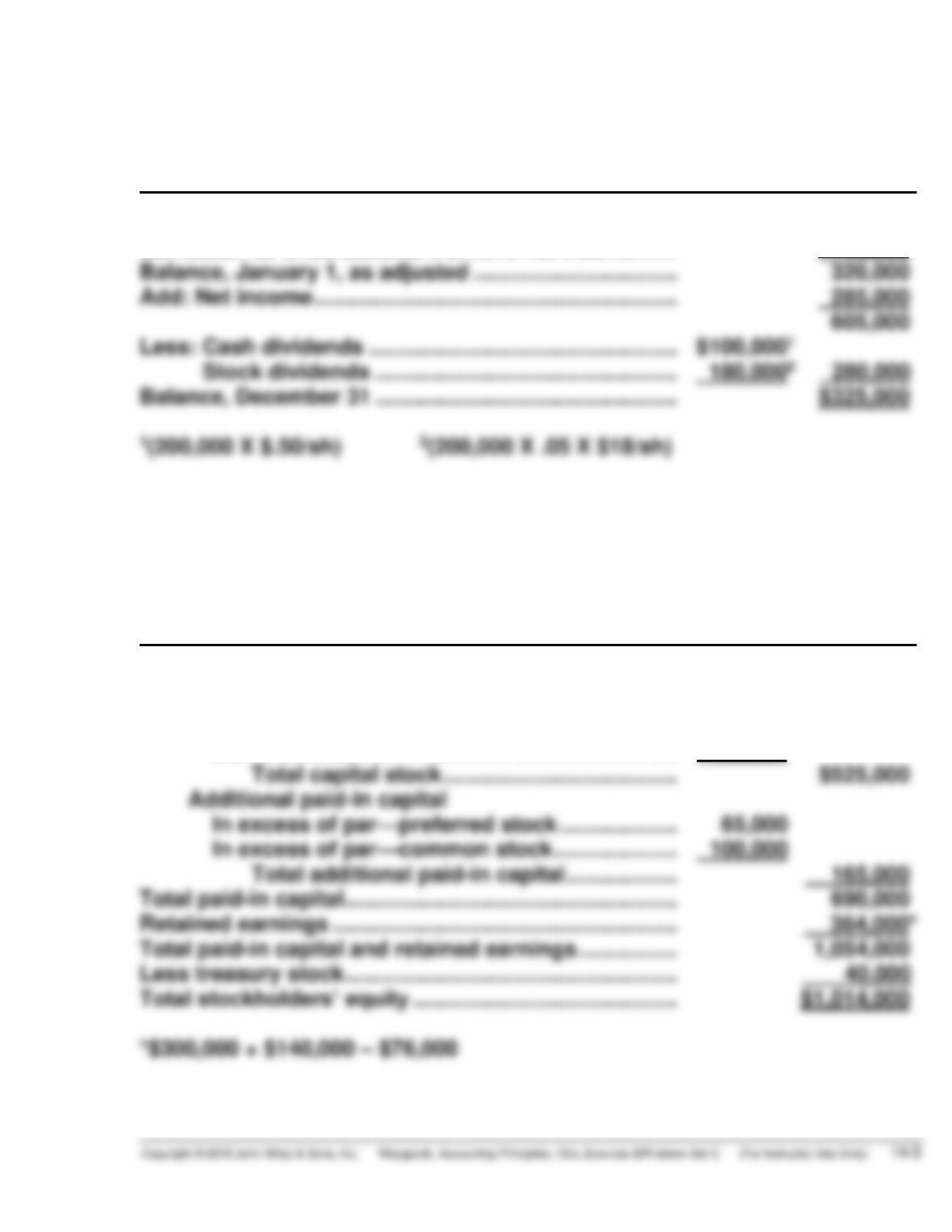

Balance, January 1, as reported ………………………… $550,000

Correction for overstatement of 2013 net

EXERCISE 14-9B

OSWALD COMPANY

Retained Earnings Statement

For the Year Ended December 31, 2017

Balance, January 1, as reported ……………………………. $310,000

Correction for understatement of 2012 net income ……. 10,000

Balance, January 1, as adjusted …………………………... 320,000

EXERCISE 14-10B

VASQUEZ COMPANY

Balance Sheet (Partial)

December 31, 2017

Paid-in capital

Capital stock

Preferred stock …………………………..…………….. $125,000

Common stock …………………………………………. 400,000

Total capital stock ……………………………….. $525,000

EXERCISE 14-11B

RAMIREZ INC.

Balance Sheet (Partial)

December 31, 20XX

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $5 par value,

40,000 shares authorized,

30,000 shares issued ……………… $ 150,000

Common stock, no par, $1 stated

value, 400,000 shares autho-

rized, 300,000 shares issued

and 290,000 outstanding ………… $ 300,000

Retained earnings (see Note R) ……………….. 850,000

Total paid-in capital and

retained earnings ……………. 2,894,000

EXERCISE 14-12B

(a) ENOS CORPORATION

Income Statement

For the Year Ended December 31, 2017

_______________________________________________________________

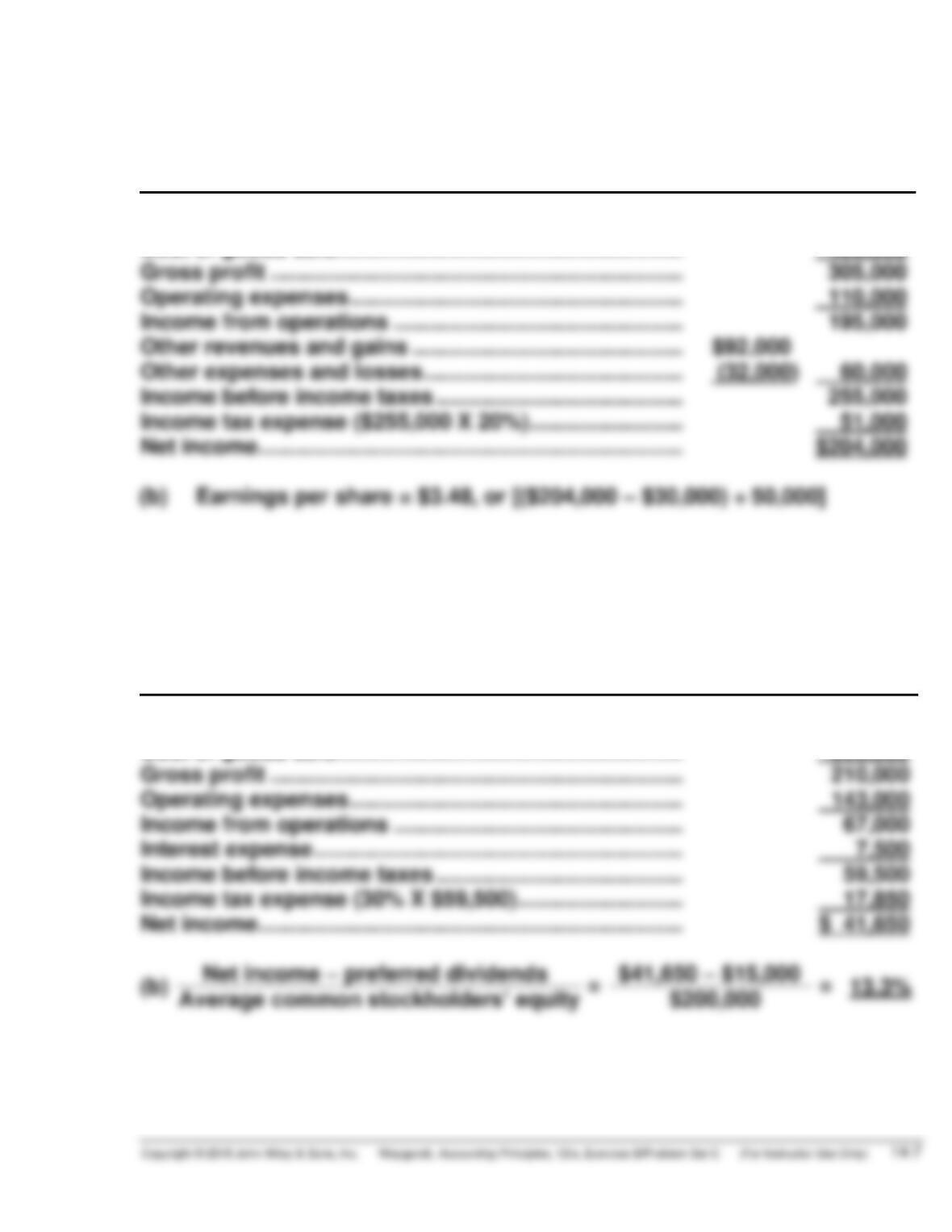

Sales revenue ………………………………………………………. $800,000

Cost of goods sold ……………………………………………….. 495,000

Gross profit …………………………………………………………. 305,000

Operating expenses ……………………………………………… 110,000

EXERCISE 14-13B

(a) MARKOWITZ CORPORATION

Income Statement

For the Year Ended December 31, 2017

_______________________________________________________________

Net sales ……………………………………………………………… $600,000

Cost of goods sold ……………………………………………….. 390,000

Gross profit …………………………………………………………. 210,000

(b)

Net income – preferred dividends

=

$41,650 – $15,000

=

13.3%

Average common stockholders’ equity

$200,000

EXERCISE 14-14B

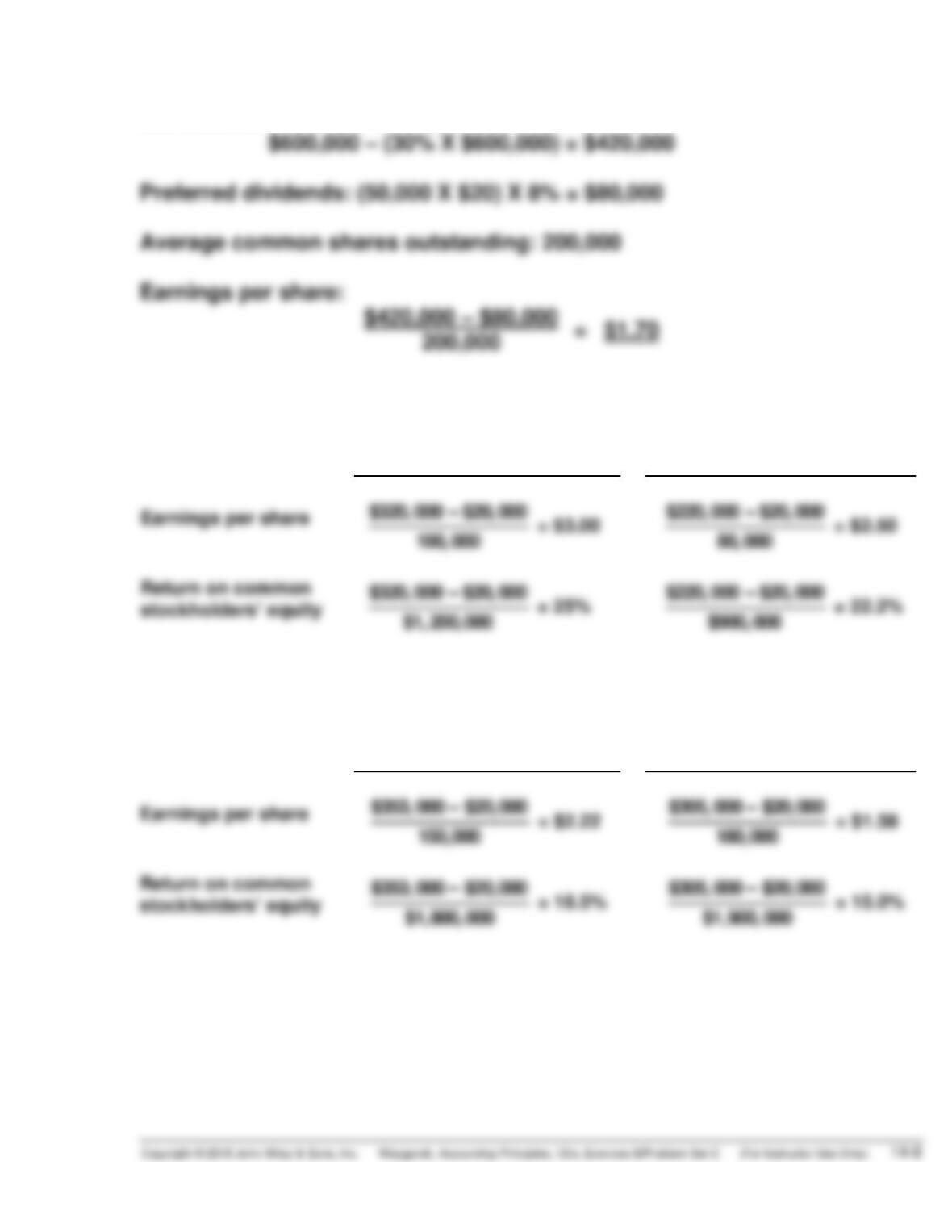

Net income: $2,000,000 – $1,400,000 = $600,000;

$600,000 – (30% X $600,000) = $420,000

EXERCISE 14-15B

2017

2016

Earnings per share

$320,000 –$20,000

100,000

= $3.00

$220,000 –$20,000

80,000

= $2.50

$320,000 –$20,000

= 25%

$220,000 –$20,000

= 22.2%

EXERCISE 14-16B

2017

2016

Earnings per share

$353,000 –$20,000

150,000

= $2.22

$305,000 –$20,000

180,000

= $1.58

$353,000 –$20,000

$305,000 –$20,000

EXERCISE 14-17B

(a)

$286,000 –$16,000

100,000

= $2.70

SOLUTIONS TO PROBLEMS—SET C

PROBLEM 14-1C

(a) Jan. 15 Cash Dividends (100,000 X $1) …………. 100,000

Dividends Payable ……………………. 100,000

May 15 Common Stock Dividends

Distributable ……………………………….. 150,000

Common Stock (15,000 X $10) …… 150,000

31 Income Summary …………………………….. 250,000

Retained Earnings ……………………. 250,000

Retained Earnings …………………………... 215,000

Cash Dividends ………………………… 215,000

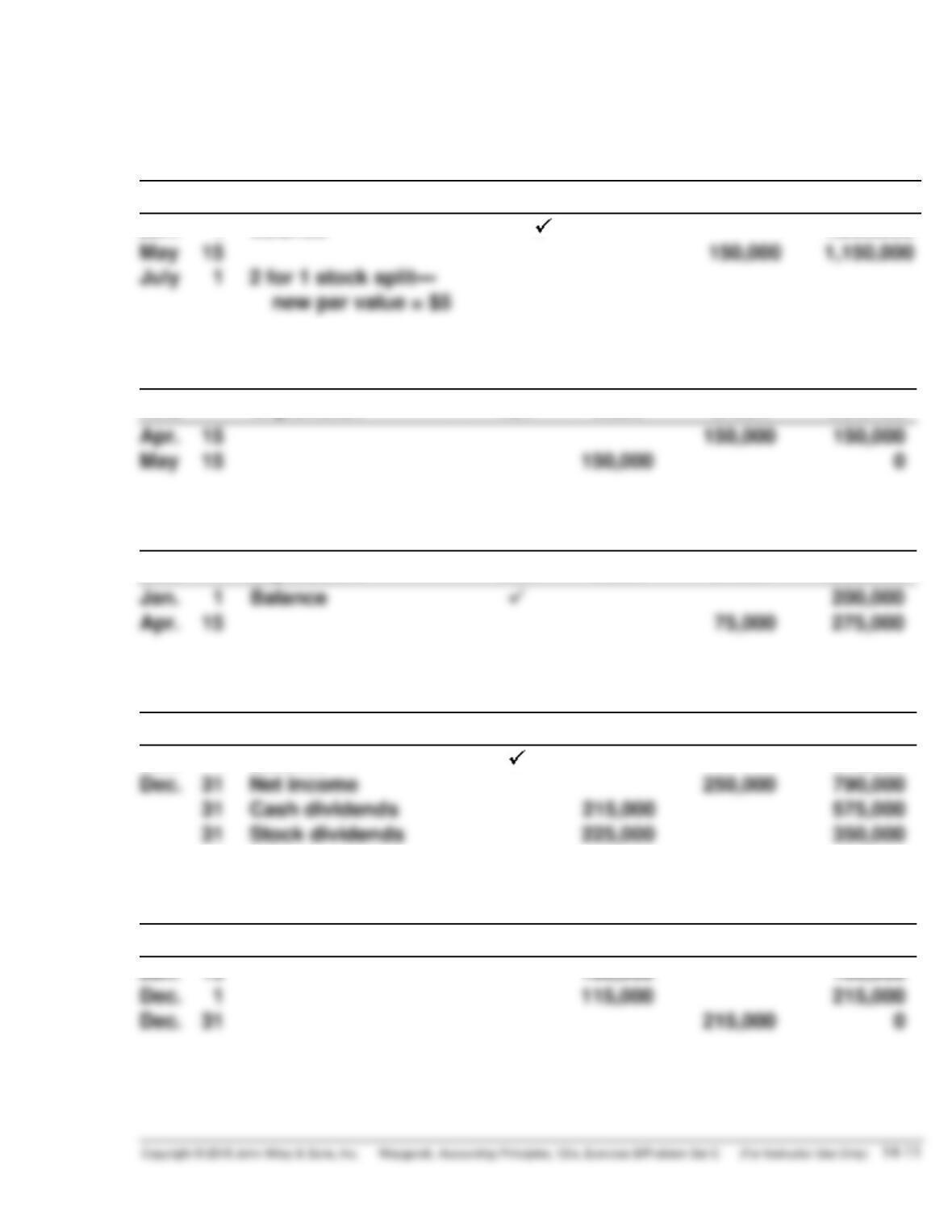

PROBLEM 14-1C (Continued)

(b)

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

May 15

July 1

Balance

2 for 1 stock split—

new par value = $5

150,000

1,000,000

1,150,000

Apr. 15

150,000

150,000

0

Paid-in Capital in Excess of Par—Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Apr. 15

Balance

75,000

200,000

275,000

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Cash dividends

250,000

790,000

350,000

Jan. 1

Balance

540,000

Cash Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 15

Dec. 1

100,000

115,000

100,000

215,000

Dec. 31

215,000

0

PROBLEM 14-1C (Continued)

Stock Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 15

225,000

225,000

(c) GLADOW CORPORATION

Balance Sheet (Partial)

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

Common stock, $5 par value, 230,000

shares issued and outstanding…………… $1,150,000

PROBLEM 14-2C

(a) July 1 Cash Dividends

[($800,000 ÷ $10) X $.50] ………………. 40,000

Dividends Payable …………………… 40,000

Aug. 1 Accumulated Depreciation ……………… 72,000

Retained Earnings …………………… 72,000

15 Cash Dividends (5,000 X $7) ……………. 35,000

Dividends Payable …………………… 35,000

(b)

Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

500,000

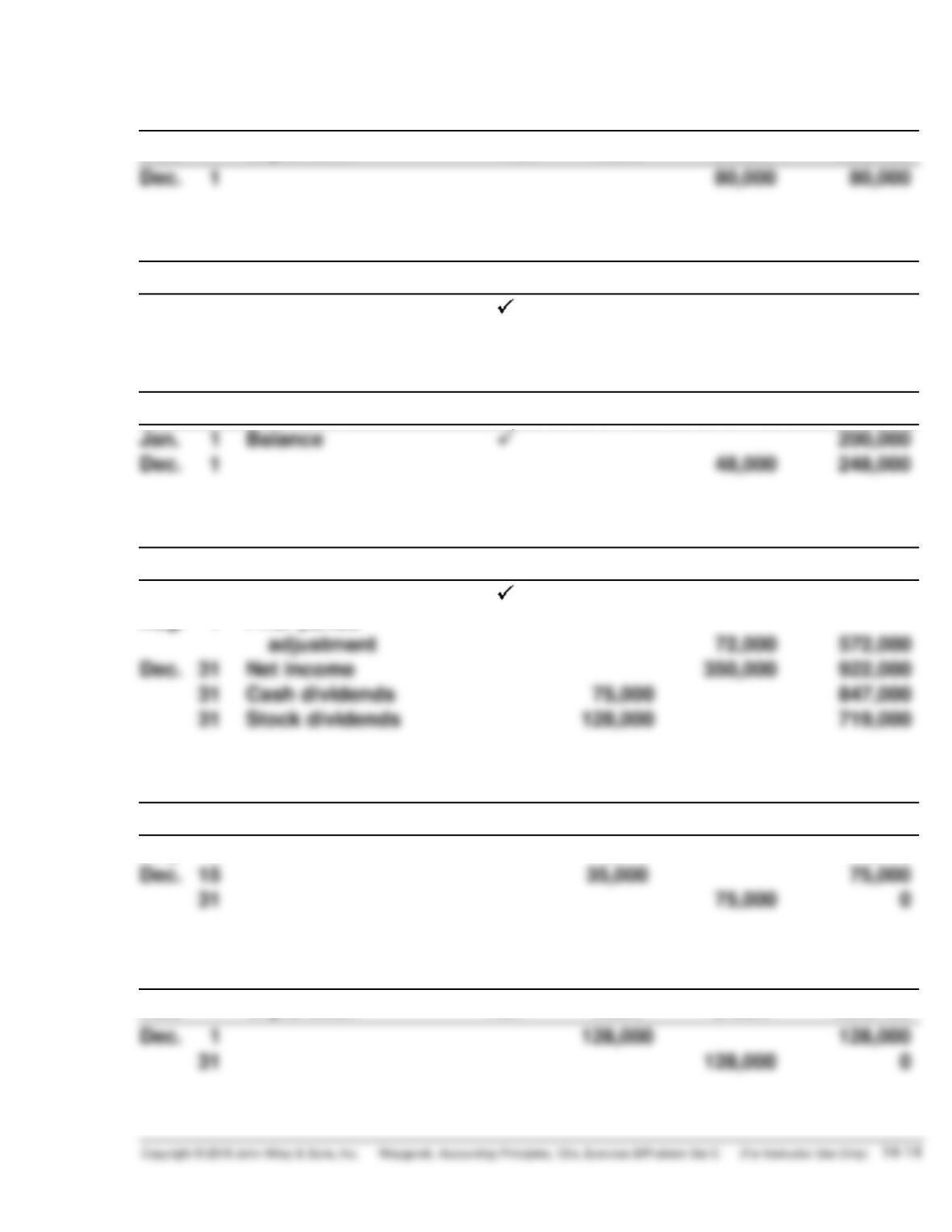

PROBLEM 14-2C (Continued)

Common Stock Dividends Distributable

Date

Explanation

Ref.

Debit

Credit

Balance

Dec. 1

80,000

80,000

Paid-in Capital in Excess of Par—Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

100,000

Paid-in Capital in Excess of Par—Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Balance

200,000

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Cash dividends

75,000

128,000

Jan. 1

Aug. 1

Balance

Prior period

adjustment

72,000

500,000

572,000

Cash Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

31

0

July 1

40,000

40,000

Stock Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

Dec. 1

31

128,000

128,000

128,000

0

PROBLEM 14-2C (Continued)

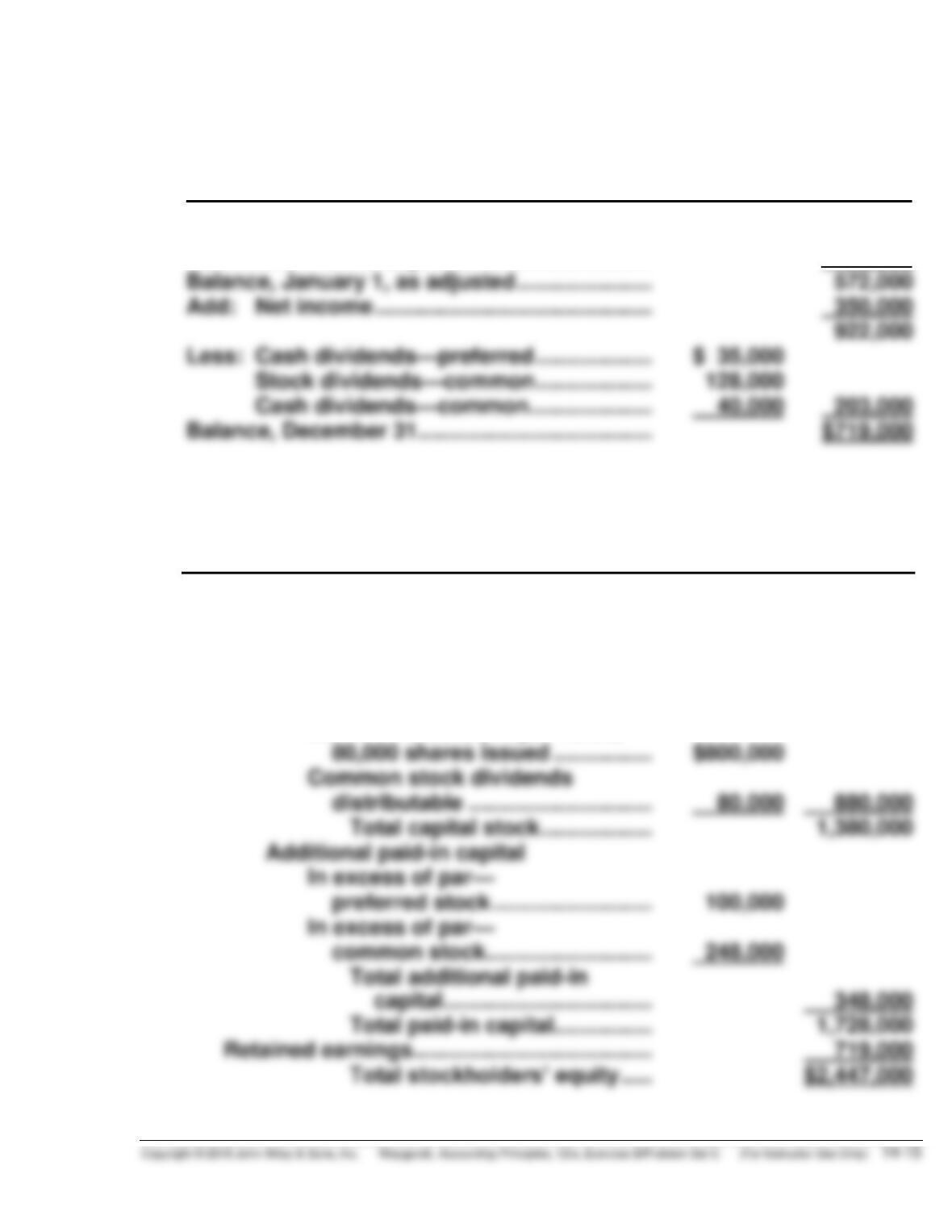

(c) COREA, INC.

Retained Earnings Statement

For the Year Ended December 31, 2017

Balance, January 1, as reported …………………. $500,000

Correction of 2013 depreciation …………………. 72,000

Balance, January 1, as adjusted …………………. 572,000

(d) COREA, INC.

Balance Sheet (Partial)

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

7% Preferred stock, $100 par

value, 5,000 shares issued ……. $ 500,000

Common stock, $10 par value,

80,000 shares issued ……………. $800,000

Common stock dividends

common stock ……………………… 248,000

Total additional paid-in

capital ……………………………. 348,000

Total paid-in capital……………. 1,728,000

Retained earnings………………………………… 719,000

Total stockholders’ equity ….. $2,447,000

PROBLEM 14-3C

(a)

Retained Earnings

Dec. 31 Stock Dividend 360,000

Dec. 31 840,000

Nov. 1 Cash Dividend 600,000

Jan. 1 Balance 2,450,000

(b) MERANDO CORPORATION

Retained Earnings Statement

For the Year Ended December 31, 2017

Balance, January 1 ………………………………….. $2,450,000

Add: Net income ……………………………………. 840,000

3,290,000

(c) MERANDO CORPORATION

Partial Balance Sheet

December 31, 2017

____________________________________________________________

Stockholders’ equity

Paid-in capital

Capital stock

6% Preferred stock, $100

par value, noncumulative,

callable at $125, 20,000

shares authorized, 10,000

PROBLEM 14-3C (Continued)

MERANDO CORPORATION (Continued)

Additional paid-in capital

In excess of par—

preferred stock …………………. $ 200,000

Retained earnings (see Note A) …………. 2,330,000

Total stockholders’

(d) Total dividend ……………………………………………………………… $600,000

Allocated to preferred stock—current year only …………….. 60,000

Remainder to common stock ………………………………………… $540,000

PROBLEM 14-4C

(a) TOWERS CORPORATION

Partial Balance Sheet

March 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

(b) TOWERS CORPORATION

Partial Balance Sheet

June 30, 2017

Stockholders’ equity

Paid-in capital

Capital stock

(c) TOWERS CORPORATION

Partial Balance Sheet

September 30, 2017

Stockholders’ equity

Paid-in capital

Capital stock

PROBLEM 14-4C (Continued)

(d) TOWERS CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

PROBLEM 14-5C

Preliminary analysis (in thousands)—NOT REQUIRED

Common

Stock

Common Stock

Dividends

Distributable

Retained

Earnings

Total

Balance, Jan. 1

$3,000

$400

$1,200

$4,600

1. Issued 100,000

shares for stock

dividend

400

(400)

0

200

200

140

140

dividend

Balance, Dec. 31

$3,600

$1,440

$5,040

PAGE INC.

Stockholders’ Equity Section of Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock