14-41

14-30 (30 min.) Customer profitability in a manufacturing firm.

Antelope Manufacturing makes a component called A1030. This component is manufactured

only when ordered by a customer, so Antelope keeps no inventory of A1030. The list price is

$115 per unit, but customers who place “large” orders receive a 12% discount on price. The

customers are manufacturing firms. Currently, the salespeople decide whether an order is large

enough to qualify for the discount. When the product is finished, it is packed in cases of 10. If

the component needs to be exchanged or repaired, customers can come back within 10 days for

free exchange or repair.

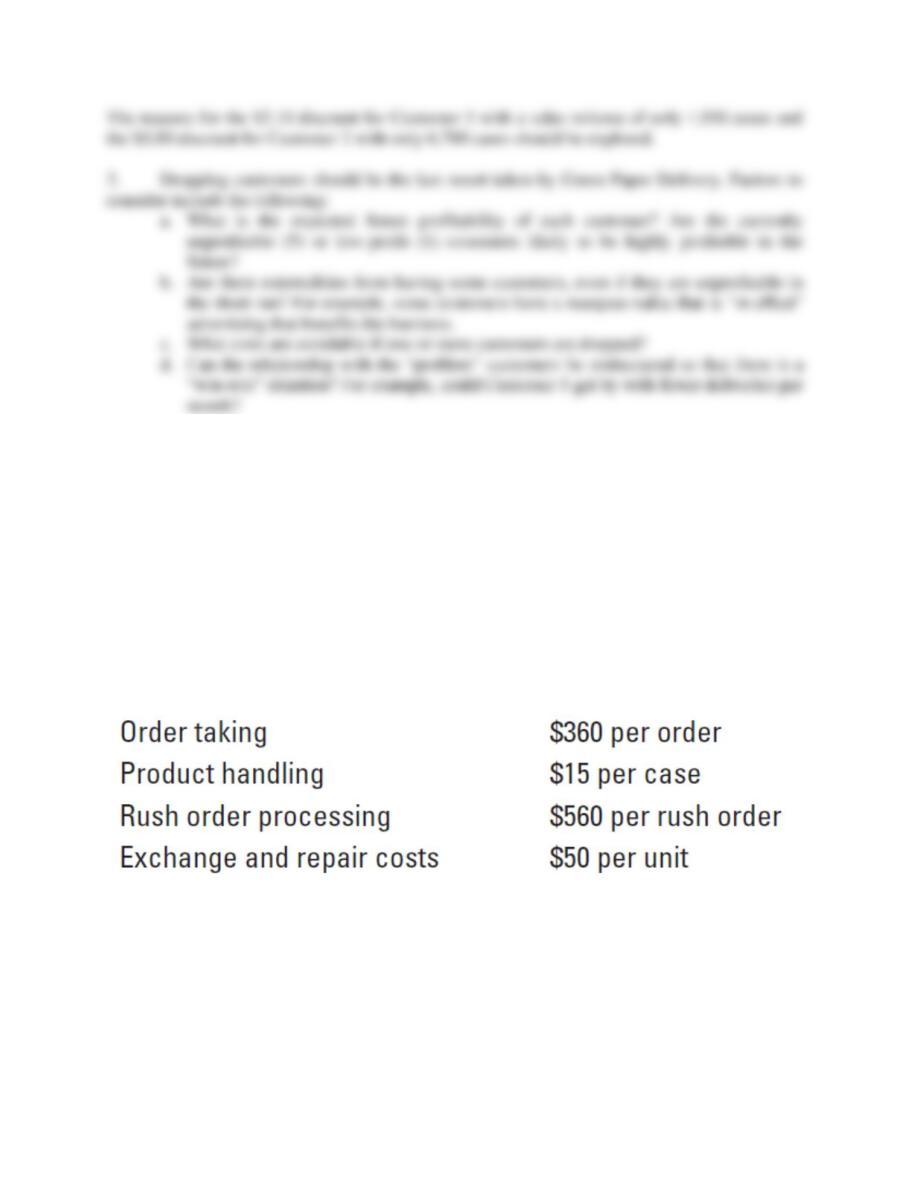

The full cost of manufacturing a unit of A1030 is $95. In addition, Antelope incurs customer-

level costs.

Customer-level cost-driver rates are:

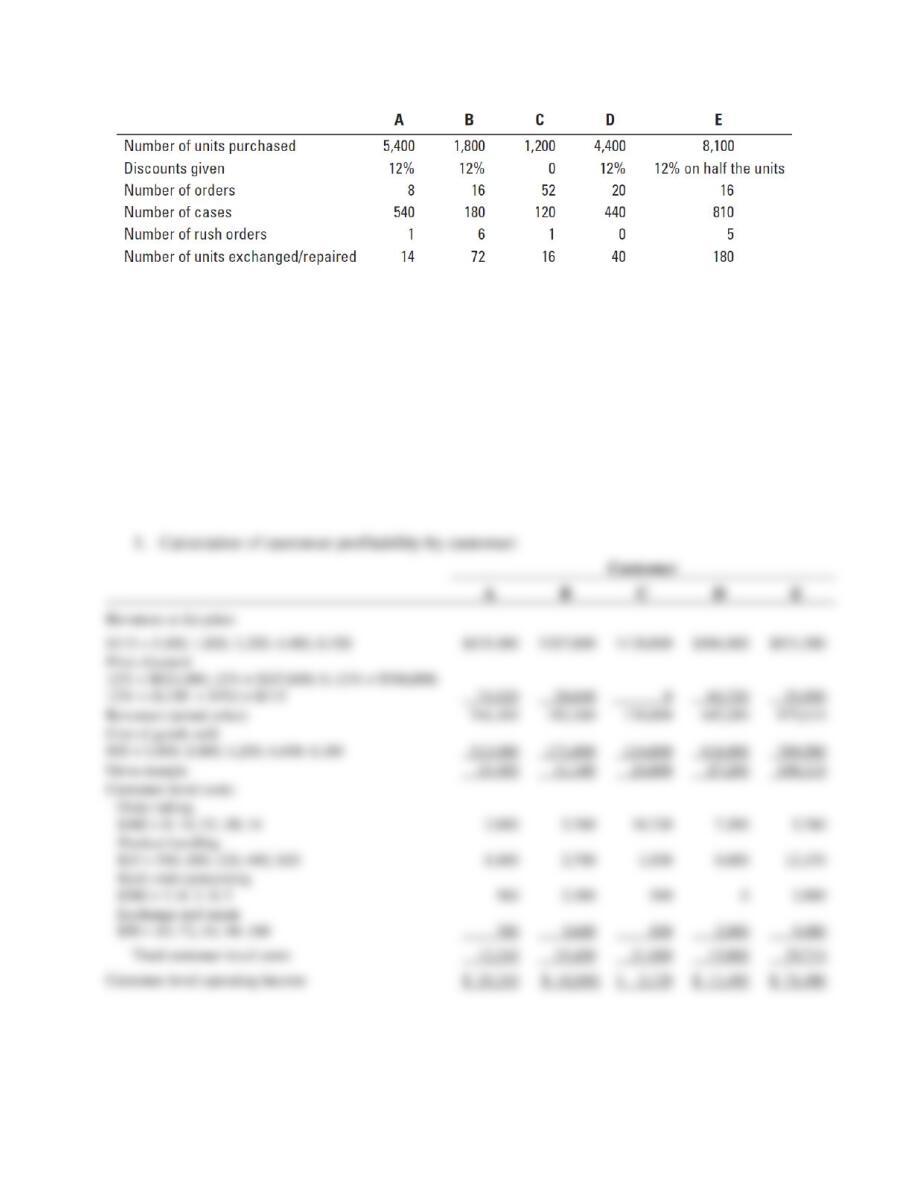

Information about Antelope’s five biggest customers follows:

14-42

All customers except E ordered units in the same order size. Customer E’s order quantity varied,

so E got a discount part of the time but not all the time.

Required:

1. Calculate the customer-level operating income for these five customers. Use the format in

Exhibit 14-3. Prepare a customer-profitability analysis by ranking the customers from most

to least profitable, as in Exhibit 14-4.

2. Discuss the results of your customer-profitability analysis. Does Antelope have unprofitable

customers? Is there anything Antelope should do differently with its five customers?

SOLUTION

14-43

14-44

14-31 (30 min.) Customer-cost hierarchy, customer profitability.

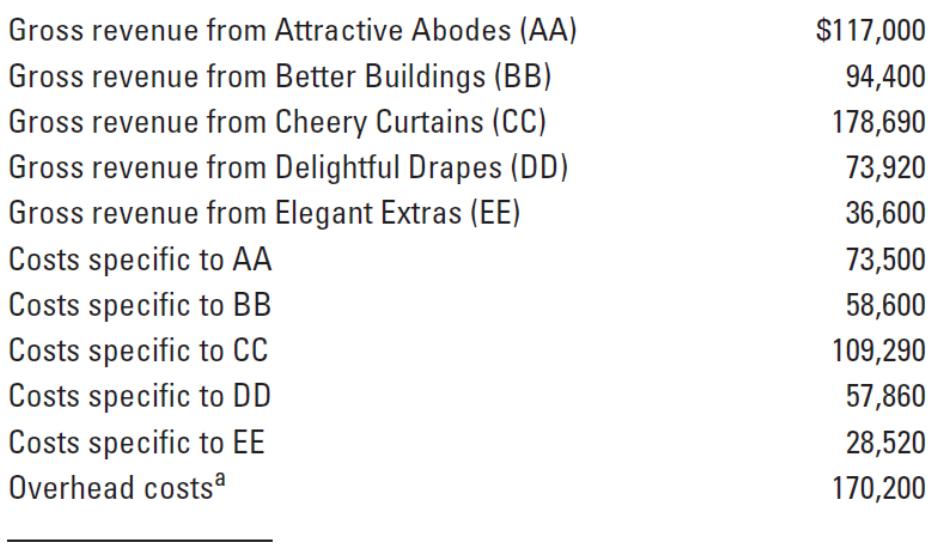

Denise Nelson operates Interiors by Denise, an interior design consulting and window treatment fabrication business. Her business is

made up of two different distribution channels, a consulting business in which Denise serves two architecture firms (Attractive

Abodes and Better Buildings) and a commercial window treatment business in which Denise designs and constructs window

treatments for three commercial clients (Cheery Curtains, Delightful Drapes, and Elegant Extras). Denise would like to evaluate the

profitability of her two architecture firm clients and three commercial window treatment clients, as well as evaluate the profitability of

each of the two channels and the business as a whole. Information about her most recent quarter follow:

aDenise has determined that 25% of her overhead costs relate directly to her architectural business, 40% relate directly to her window

treatment business, and the remainder are general in nature.

On the revenues indicated above, Denise gave a 10% discount to Attractive Abodes in order to lure it away from a competitor and

gave a 5% discount to Elegant Extras for advance payment in cash.

14-45

Required:

1. Prepare a customer-cost hierarchy report for Interiors by Denise, using the format in Exhibit 14-6.

2. Prepare a customer-profitability analysis for the five customers, using the format in Exhibit 14-4.

3. Comment on the results of the preceding reports. What recommendations would you give Denise?

SOLUTION

14-46

14-47

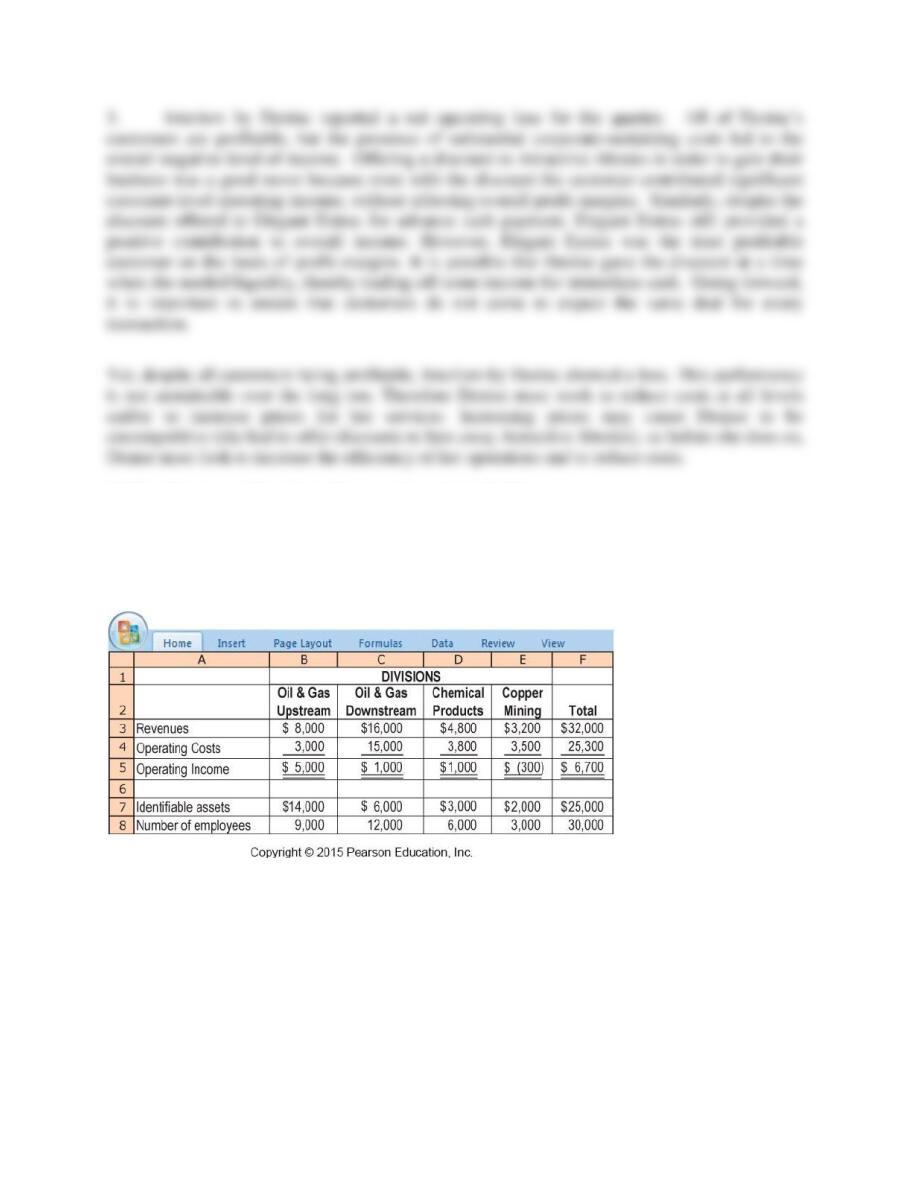

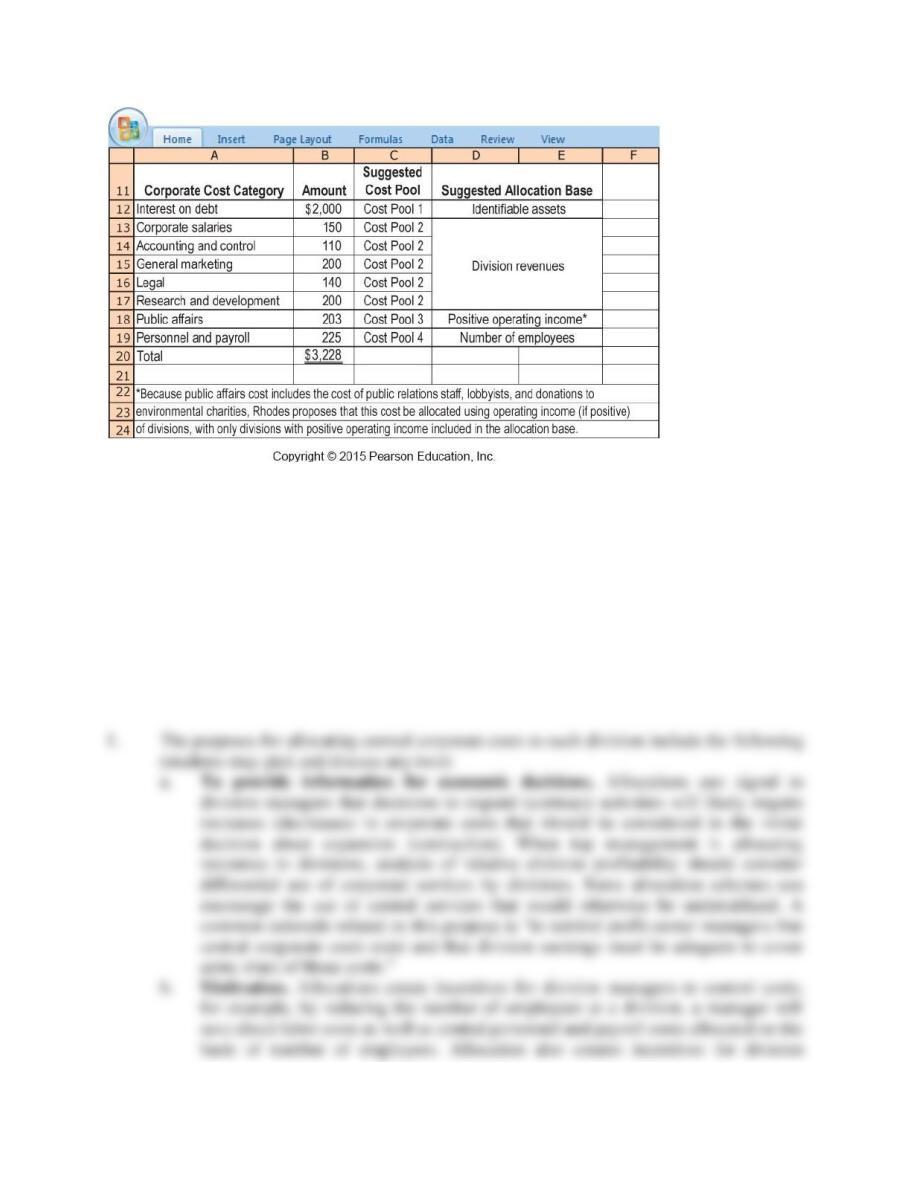

14-32 (40 min.) Allocation of corporate costs to divisions.

Dusty Rhodes, controller of Richfield Oil Company, is preparing a presentation to senior

executives about the performance of its four divisions. Summary data (dollar amounts in

millions) related to the four divisions for the most recent year are as follows:

Under the existing accounting system, costs incurred at corporate headquarters are collected in a

single cost pool ($3,228 million in the most recent year) and allocated to each division on the

basis of its actual revenues. The top managers in each division share in a division-income bonus

pool. Division income is defined as operating income less allocated corporate costs.

Rhodes has analyzed the components of corporate costs and proposes that corporate costs be

collected in four cost pools. The components of corporate costs for the most recent year (dollar

amounts in millions) and Rhodes’ suggested cost pools and allocation bases are as follows:

14-48

Required:

1. Discuss two reasons why Richfield Oil should allocate corporate costs to each division.

2. Calculate the operating income of each division when all corporate costs are allocated based

on revenues of each division.

3. Calculate the operating income of each division when all corporate costs are allocated using

the four cost pools.

4. How do you think the division managers will receive the new proposal? What are the

strengths and weaknesses of Rhodes’ proposal relative to the existing single-cost-pool

method?

SOLUTION

14-49

14-50

14-51

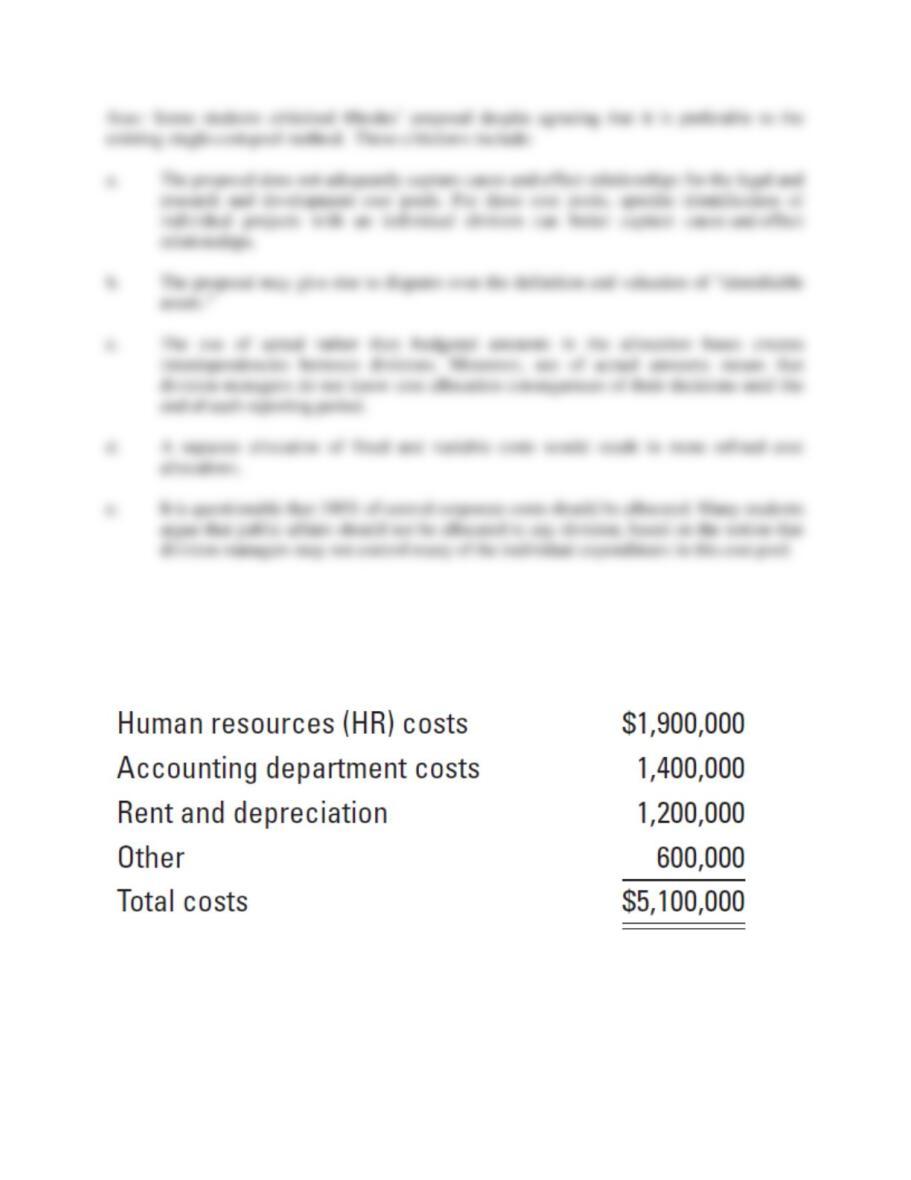

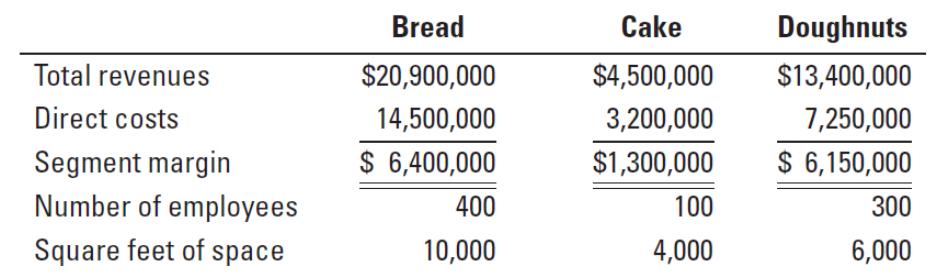

14-33 (30 min.) Cost allocation to divisions.

Forber Bakery makes baked goods for grocery stores and has three divisions: bread, cake, and

doughnuts. Each division is run and evaluated separately, but the main headquarters incurs costs

that are indirect costs for the divisions. Costs incurred in the main headquarters are as follows:

The Forber upper management currently allocates this cost to the divisions equally. One of the

division managers has done some research on activity-based costing and proposes the use of

different allocation bases for the different indirect costs—number of employees for HR costs,

total revenues for accounting department costs, square feet of space for rent and depreciation

costs, and equal allocation among the divisions of “other” costs. Information about the three

divisions follows:

14-52

Required:

1. Allocate the indirect costs of Forber to each division equally. Calculate division operating

income after allocation of headquarter costs.

2. Allocate headquarter costs to the individual divisions using the proposed allocation bases.

Calculate the division operating income after allocation. Comment on the allocation bases

used to allocate head- quarter costs.

3. Which division manager do you think suggested this new allocation. Explain briefly. Which

allocation do you think is “better?”

14-53

SOLUTION

14-54

14-34 (30 min.) Cost-hierarchy income statement and allocation of corporate, division,

and channel costs to customers.

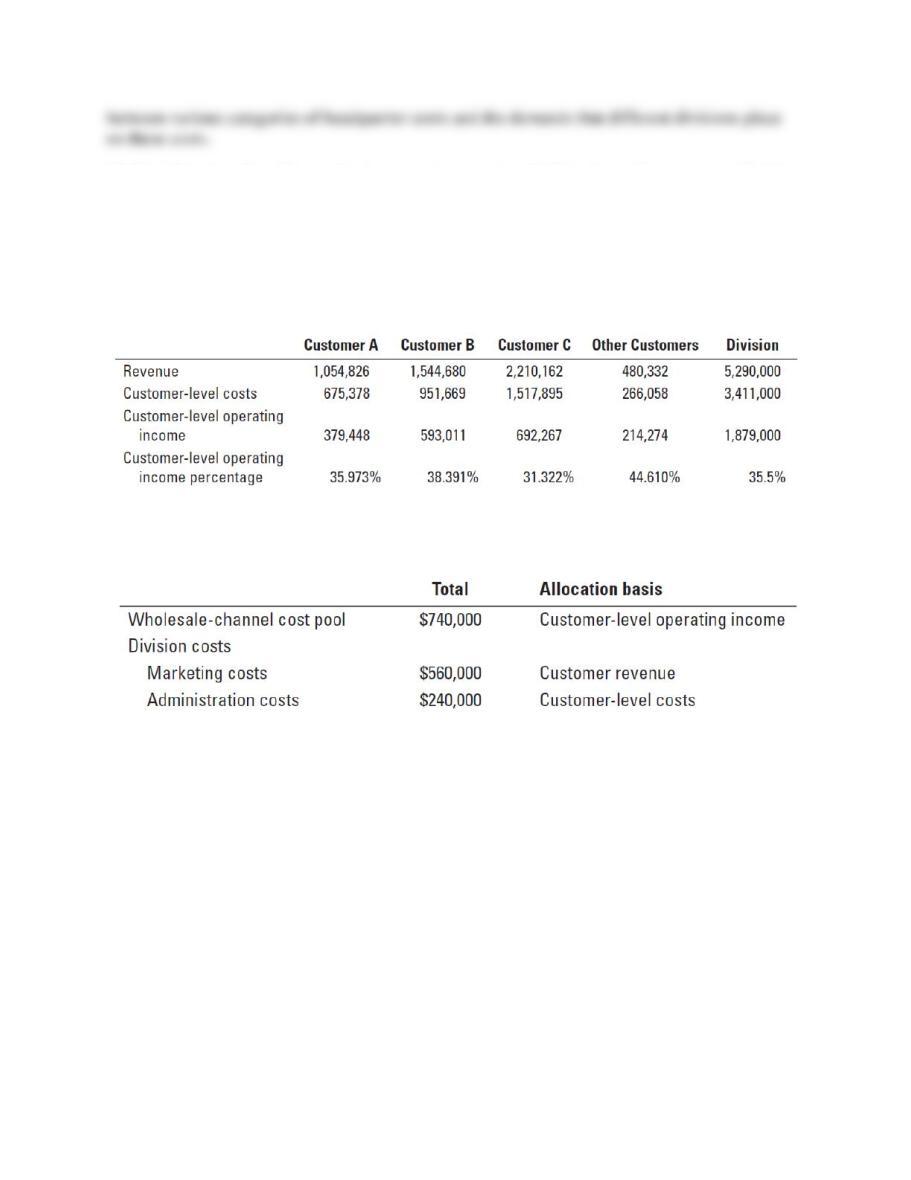

Rod Manufacturing Company produces metal rods for their customers. Its wholesale division is

the focus of our analysis.

Management of the company wishes to analyze the profitability of the three key customers in

the division and has gathered the following information.

The company allocates wholesale channel costs to customers based on one cost pool and division

costs based on two cost pools as follows. Customer actions do not influence these costs.

Required:

1. Calculate customer profitability as a percentage of revenue after assigning customer-level

costs, distribution-channel costs, and division costs. Comment on your results.

2. What are the advantages and disadvantages of Rod Manufacturing allocating wholesale-

channel and division costs to customers?

14-55

SOLUTION

14-56

14-57

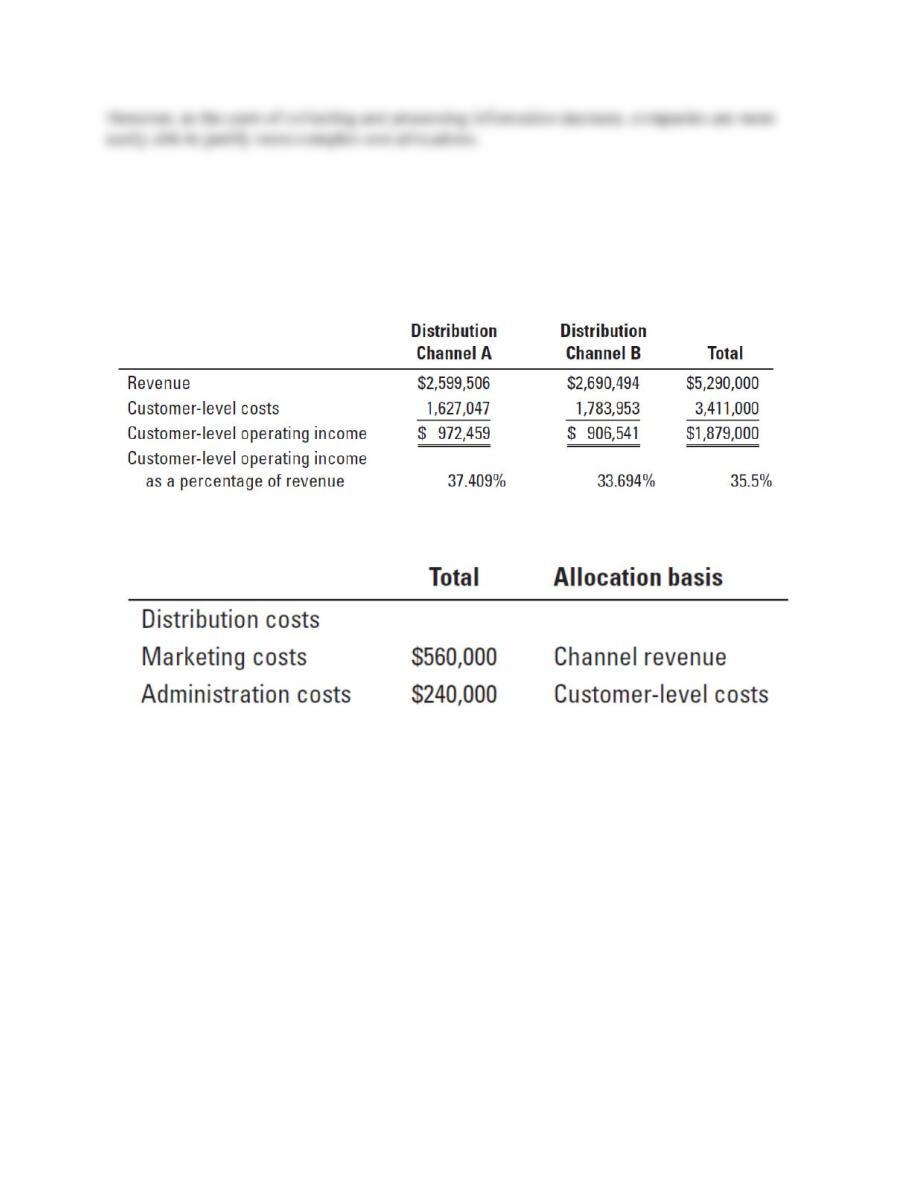

14-35 (30 min.) Cost-hierarchy income statement and allocation of corporate, division, and

channel costs to customers.

Basic Boards makes keyboards that are sold to different customers in two main distribution

channels. Recently, the company’s profitability has decreased. Management would like to

analyze the profitability of each channel based on the following information:

The company allocates distribution costs to the two channels as follows:

Based on a special study, the company allocates corporate costs to the two channels based on the

corporate resources demanded by the channels as follows: Distribution Channel A, $440,000,

and Distribution Channel B, $500,000. If the company were to close a distribution channel, none

of the corporate costs would be saved.

Required:

1. Calculate the operating income for each distribution channel as a percentage of revenue after

assigning customer-level costs, distribution costs, and corporate costs.

2. Should Basic Boards close down any distribution channel? Explain briefly.

3. Would you allocate corporate costs to divisions? Why is allocating these costs helpful? What

actions would it help you take?

14-58

SOLUTION

14-59

14-36 (60 min.) Variance analysis, sales-mix and sales-quantity variances.

Houston Infonautics, Inc., produces handheld Windows CE™-compatible organizers. Houston

Infonautics markets three different handheld models: PalmPro is a souped-up version for the

executive on the go, PalmCE is a consumer-oriented version, and PalmKid is a stripped-down

version for the young adult market. You are Houston Infonautics’ senior vice president of

marketing. The CEO has discovered that the total contribution margin came in lower than

budgeted, and it is your responsibility to explain to him why actual results are different from the

budget. Budgeted and actual operating data for the company’s third quarter of 2014 are as

follows: