Chapter 14 – Decision Making: Relevant Costs and Benefits

14-1

CHAPTER 14

Decision Making: Relevant Costs and Benefits

ANSWERS TO REVIEW QUESTIONS

14-1 The seven steps in the decision-making process are as follows:

Clarify the decision

14-2 The managerial accountant’s role in the decision-making process is to participate as

14-3 A quantitative analysis is expressed in numerical terms. A qualitative analysis

14-4 A decision model is a simplified representation of the choice problem. Unnecessary

14-5 The result of a quantitative analysis is that one alternative is preferred over the next–

best alternative by some numerical amount, such as profit. The amount by which the

best alternative dominates the second-best alternative establishes a “price” on the

Chapter 14 – Decision Making: Relevant Costs and Benefits

14-2

14-6 Relevant information is pertinent to a decision problem. Accurate information is

precise. Timely information is available to the decision maker in time to make the

14-7 Two important criteria that must be satisfied in order for information to be relevant

are as follows:

14-8 The book value of an asset is its acquisition cost less its accumulated depreciation.

14-9 The book value of inventory, like the book value of any asset, is not a relevant cost.

14–10 Managers sometimes exhibit a behavioral tendency to inappropriately consider a

sunk cost in making a decision, because they believe that their original decision to

14–11 An example of an irrelevant future cost is a cost that will occur in the future but does

14-3

14–12 An opportunity cost is the potential benefit given up when the choice of one action

14–13 People often exhibit a behavioral tendency to ignore or downplay the importance of

14–14 If a firm has excess production capacity, there is no opportunity cost to the

acceptance of a special order. On the other hand, if the firm is already at capacity

14–15 In a differential-cost analysis, the decision maker determines the difference in each

14–16 In making a decision about adding or dropping a product line, the decision maker

14–17 A joint production process is one in which the processing of a common input results

in two or more distinct products known as joint products. A special decision that

14–18 The allocated joint processing costs are irrelevant when making a decision as to

14–19 The proper approach to making a production decision when limited resources are

14-4

14–20 The contribution margin per unit of scarce resource is a product’s unit contribution

margin divided by the number of units of the scarce resource required to produce

14–21 Sensitivity analysis may be used to cope with uncertainty in decision making by

14–22 There is an important link between decision making and managerial performance

evaluation, because managers typically make decisions that maximize their

14–23 Four potential pitfalls in decision making that represent common errors are the

following:

14–24 Unitized fixed costs can cause errors in decision making because the fixed cost per

14–25 Sunk costs are irrelevant in decision making because they have already occurred in

Chapter 14 – Decision Making: Relevant Costs and Benefits

14-5

14–26 This remark fails to recognize the fact that the identification of relevant information

14–27 The concepts underlying a relevant-cost analysis remain valid both in an advanced

manufacturing environment and in a situation where activity-based costing is used.

14–28 Five ways to relax a bottleneck constraint are as follows:

• Working overtime at the bottleneck operation.

Chapter 14 – Decision Making: Relevant Costs and Benefits

14-6

SOLUTIONS TO EXERCISES

EXERCISE 14-29 (25 MINUTES)

Students’ answers to this exercise will vary widely. The following illustration is set in a

QUANTITATIVE ANALYSIS

1. Clarify the decision problem: The first step was to clarify the problem. Was the

perceived slow response time real or merely a perception by the residents of the

neighborhood? What was the average response time for emergency vehicles to the

area? Were proper procedures being followed? What was the condition of the roads,

bridges, and traffic lights on the route to the neighborhood in question?

2. Specify the criterion: The City Council decided that some type of action was

3. Identify the alternatives: The city engineer identified the following alternatives:

4. Develop a decision model: The decision model consisted of a computer program that

14-7

EXERCISE 14-29 (CONTINUED)

5. Collect the data: The data needed for the decision model included employee

QUALITATIVE CONSIDERATIONS

The computer model indicated that either alternative would satisfy the criterion of

reducing emergency response times by five minutes, and that the positioning of emergency

6. Make a decision: The City Council decided to build a satellite fire and rescue station.

EXERCISE 14-30 (20 MINUTES)

FLIGHT ROUTE DECISION

Revenues and Costs

Under Two Alternatives

(a)

Nonstop

Route*

(b)

With Stop

In San

Francisco*

(c)

Differential

Amount†

Passenger revenue ……………………………………….

$240,000

$258,000

$(18,000

)

Landing fee in San Francisco ………………………..

-0-

(5,000

)

5,000

Use of airport gate facilities …………………………..

-0-

(3,000

)

3,000

Flight crew cost …………………………………………….

(2,000

)

(2,500

)

Fuel ……………………………………………………………..

)

)

3,000

Meals and services ……………………………………….

)

)

14-8

EXERCISE 14-31 (15 MINUTES)

The owner’s analysis incorrectly includes the following allocated costs that will be incurred

regardless of whether the ice cream counter is operated:

Utilities ……………………………………………………………………………………………………….

$ 4,350

Depreciation of building ………………………………………………………………………………

4,500

Total …………………………………………………………………………………………………………..

$14,850

It is possible that closing the ice cream counter might save a portion of the utility

cost, but that is doubtful.

A better analysis follows:

Sales ………………………………………………………………………………………

$67,500

Less: Cost of food …………………………………………………………………..

Gross profit …………………………………………………………………………….

Less: Operating expenses

Wages of counter personnel ……………………………………….

$18,000

Paper products ……………………………………………………………

Depreciation of counter equipment and furnishings* …….

3,750

Total ……………………………………………………………………………

Profit on ice cream counter

$ 9,750

EXERCISE 14-32 (15 MINUTES)

1.

(a) $11,100 allocation of rent on factory building: Irrelevant, since Toon Town Toy

Chapter 14 – Decision Making: Relevant Costs and Benefits

14-9

EXERCISE 14-33 (15 MINUTES)

(a) $51,000 salary of Packaging Department manager: Irrelevant, since this manager will

(b) $66,000 salary of Cutting Department manager if a new person must be hired:

The following comparison may help to clarify the analysis:

ANNUAL SALARY COST INCURRED BY TOON TOWN TOY COMPANY

If Packaging

Department

is Kept

If Packaging

Department

is Eliminated

Salary of newly hired person to manage the

Total ……………………………………………………………..

Salary of the person currently managing the

*Continues to manage Packaging Department.

†Moves to Cutting Department position.

Additional comment:

There are many possible reasons why it might cost Toon Town Toy Company more

to hire a new Cutting Department manager than to transfer a current employee to the

14–10

EXERCISE 14-34 (15 MINUTES)

1.

The owner’s reasoning probably reflects the following calculation:

Savings in annual operating expenses if old pizza oven is replaced ………………

)

)

3.

Correct analysis:

Savings in annual operating expenses if old pizza oven is replaced ………………

Acquisition cost of new oven, which will be operable for one year ………………..

)

Net benefit from replacing old pizza oven …………………………………………………….

EXERCISE 14-35 (30 MINUTES)

Answers will vary depending on the company and activity chosen. There are many trade-

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–11

EXERCISE 14-36 (15 MINUTES)

1.

Relevant data:

Current sales value for unmodified parts ……………………………………………………..

$ 7,000

Sales value for modified parts ……………………………………………………………………..

Modification costs ……………………………………………………………………………………

Irrelevant data:

Current book value of inventory …………………………………………………………………..

This is a sunk cost. It will not affect any future course of action.

2.

There are two alternatives for disposing of the obsolete parts: (a) sell in

unmodified condition or (b) modify and then sell.

(a) Benefit if parts are sold without modification ………………………………………….

$ 7,000

(b) Sales value for modified parts ………………………………………………………………..

Less: Cost of modification …………………………………………………………………….

Net benefit if parts are sold after being modified ……………………………………..

Conclusion: Modify the parts and then sell them.

EXERCISE 14-37 (15 MINUTES)

Dear (president’s name):

We recommend against processing banolide into kitrocide. The incremental cost of

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–12

EXERCISE 14-38 (20 MINUTES)

Sales revenue for one jar of silver polish ………………………………….

$8.00

Less: Sales revenue for 1/4 pound of Grit 337 ………………………….

Incremental revenue from further processing …………………………...

$7.00

Incremental costs of further processing:

$1.40

EXERCISE 14-39 (15 MINUTES)

1.

The relevant cost of the theolite to be used in producing the special order is the

(a) 21,750p sales value: Discussed in requirement (1).

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–13

EXERCISE 14-40 (20 MINUTES)

1.

The relevant cost of genatope is calculated as follows:

*Additional cost incurred on the next order of genatope as a result of

Cost of replacing the 1,000 kilograms to be used in the special order

(b) 1,000 kilograms to be used in the special order: Relevant, as shown in

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–14

EXERCISE 14-41 (10 MINUTES)

The most profitable product is the one that yields the highest contribution margin per unit

of the scarce resource, which is direct labor. We do not know the amount of direct-labor

time required per unit of either product, but we do know that Beta requires six times as

14–15

EXERCISE 14-42 (15 MINUTES)

1. Decision variables:

2. Objective function:

3. Constraints:

(a) Direct-labor time constraint: .25X + 1.5Y 11,000

14–16

EXERCISE 14-43 (30 MINUTES)

1. (a) Notation: X denotes the quantity of zanide produced per day

Y denotes the quantity of kreolite produced per day

(b) Contribution margin:

Zanide

Kreolite

Price ……………………………………………………….

Unit variable cost ……………………………………………………….

Maximize

24X + 42Y

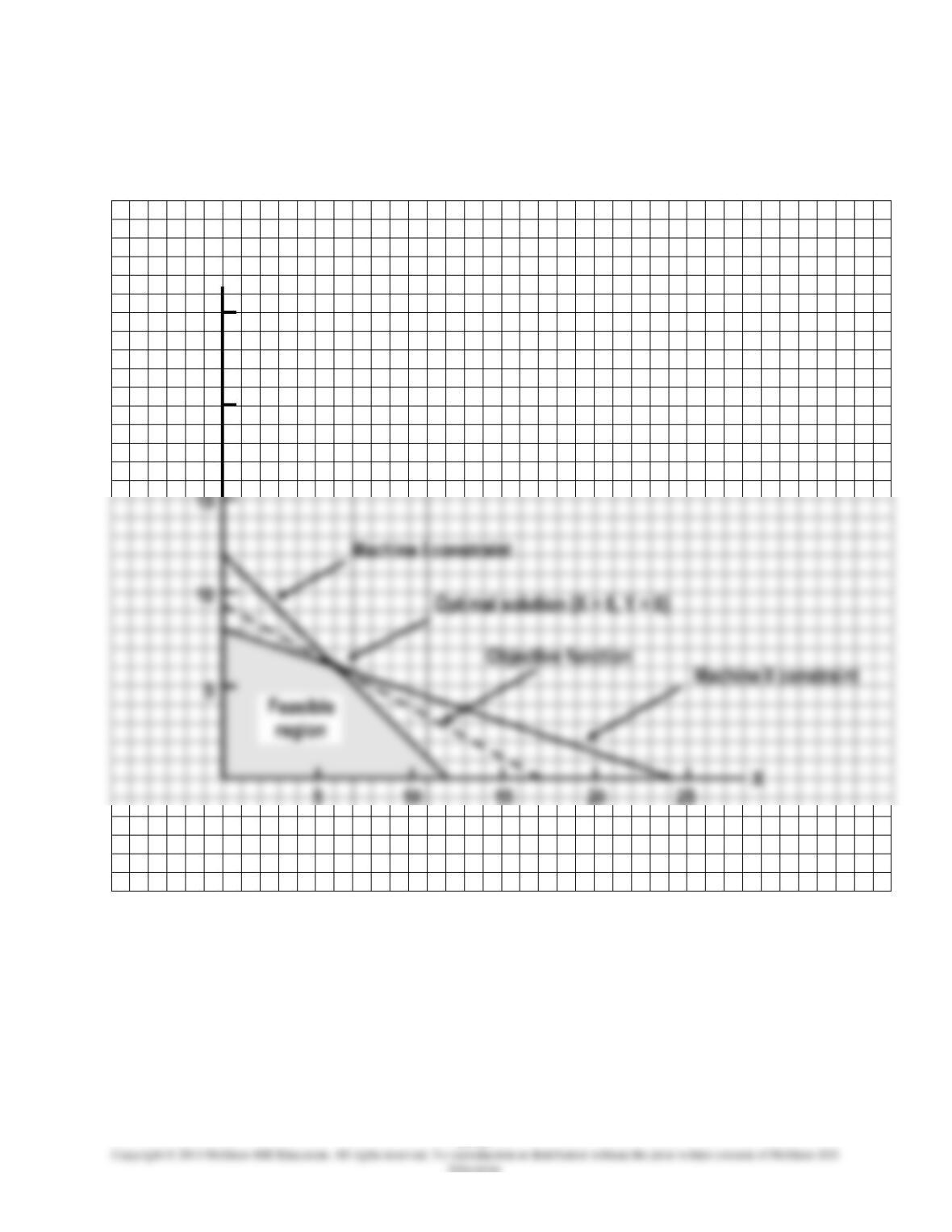

2. Graphical solution: See next page.

Corner points in feasible region:

Objective function value:

X = 0

Y = 0

$ 0

X = 0

Y = 8

X = 6

Y = 6

X = 12

Y = 0

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–17

EXERCISE 14-43 (CONTINUED)

Graphical solution:

Y

25

15

5

X

Machine I constraint

Optimal solution (X = 6, Y = 6)

Objective function

Machine II constraint

20

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–18

SOLUTIONS TO PROBLEMS

PROBLEM 14-44 (25 MINUTES)

1. Contemporary Trends will be worse off by $6,400 if it discontinues wallpaper sales.

Paint and

Supplies

Carpeting

Wallpaper

Sales……………………..

$190,000

$230,000

$ 70,000

Less: Variable costs….

56,000

Contribution margin….

$ 76,000

$ 69,000

$ 14,000

If wallpaper is closed, then:

Loss of wallpaper contribution margin……

$(14,000)

Remodeling…………………………………….

(6,200)

Added profitability from carpet sales*……

32,500

Fixed cost savings ($22,500 x 40%)……….

9,000

Decreased contribution margin from paint

Increased advertising………………………..

Income (loss) from closure…………………

$ (6,400)

2. This cost should be ignored. The inventory cost is sunk (i.e., a past cost that is not

3. The Internet- and magazine-based firms likely have several advantages:

• These companies probably carry little or no inventory. When a customer places

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–19

PROBLEM 14-44 (CONTINUED)

PROBLEM 14-45 (50 MINUTES)

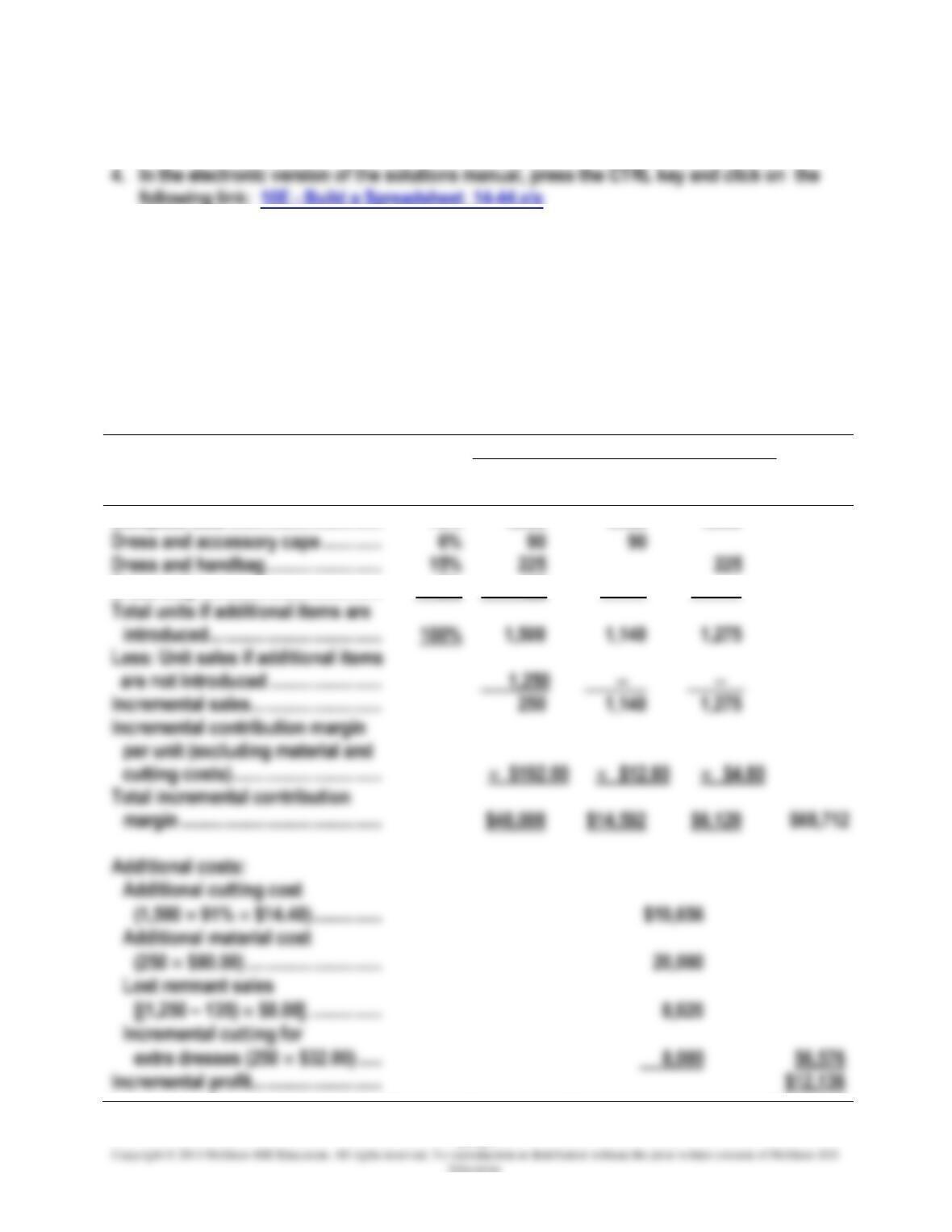

1. Sets result in a 20% increase, or 1,500 dresses (1,250 1.20 = 1,500).

Total Number of

Percent

of Total

Dresses

Accessory

Capes

Handbags

Total

Complete sets …………………………...

70%

1,050

1,050

1,050

Dress and accessory cape ………….

Dress and handbag …………………….

15%

Dress only …………………………………

9%

135

Total units if additional items are

1,500

1,140

1,275

Less: Unit sales if additional items

1,250

—

Incremental sales ……………………….

1,140

1,275

$48,000

$14,592

$6,120

$68,712

Additional costs:

Chapter 14 – Decision Making: Relevant Costs and Benefits

14–20

2. Qualitative factors that could influence the company’s management team in its

decision to manufacture matching accessory capes and handbags include:

PROBLEM 14-45 (CONTINUED)

• company image of a dress manufacturer versus a more extensive supplier of

PROBLEM 14-46 (25 MINUTES)

1.

Blender

Food

Processor

Unit cost if purchased from an outside supplier …………………………..

$60

$114

Incremental unit cost if manufactured:

$18

$48

Unit cost savings if manufactured …………………………………………………….

$12

Machine hours required per unit ……………………………………………………….

Cost savings per machine hour if manufactured

$12