453

CHAPTER 14

PERFORMANCE EVALUATION FOR

DECENTRALIZED OPERATIONS

CLASS DISCUSSION QUESTIONS

1. In a cost center, the department manager is

responsible for and has authority over costs

only. In a profit center, the manager’s re-

sponsibility and authority extend to costs

and revenues.

3. The difference in budget performance re-

ports prepared for department supervisors

and plant managers is the amount of detail

provided to each. The departmental supervi-

sors require considerable detail to control

costs. The report for the plant managers

would contain more summarized cost data

for the various departments.

4. A cost center manager is not responsible for

making decisions concerning sales or the

amount of fixed assets invested in the cen-

ter.

6. The major shortcoming of using income from

operations as a measure of investment cen-

ter performance is that it ignores the amount

of investment committed to each center.

Since investment center managers also con-

8. A division of a decentralized company could

be considered the least profitable, even

though it earned the largest amount of in-

come from operations, when its rate of re-

turn on investment is the lowest. In this situ-

from operations per dollar invested.

10. North Division. The North Division will return

38 cents (38%) on each dollar of invested

assets, while the South and Midwest divi-

sions will return only 30 cents (30%) and 22

cents (22%), respectively. Thus, in expand-

ing operations, the North Division should be

given priority over the South and Midwest

divisions.

11. A balanced scorecard can indicate the un-

derlying causes of financial performance

from innovation and learning, customer, in-

courage each division manager to work in

the best interests of the company. Thus,

transfer prices should encourage managers

to transfer goods between divisions if the

overall company income can be increased.

454

EXERCISES

E14–1

a. (a) $140,000 (g) $275,000

(b) $150,750 (h) $285,325

Schedules of supporting calculations (answers in italics; the solution requires

working from the department level, up to the plant level, then to the vice president

of production level):

MERIDIAN COMPANY

Budget Performance Report—Vice President, Production

For the Month Ended June 30, 20Y4

Plant Budget Actual Over Budget Under Budget

MERIDIAN COMPANY

Budget Performance Report—Plant Manager, Peoria, Illinois

For the Month Ended June 30, 20Y4

Department Budget Actual Over Budget Under Budget

455

E14–1, Concluded

MERIDIAN COMPANY

Budget Performance Report—Supervisor, Condenser Assembly

For the Month Ended June 30, 20Y4

Department Budget Actual Over Budget Under Budget

Factory wages $ 30,000 $ 33,400 $ 3,400

b. MEMO

To: Darla Pennington, President of Meridian Company

The Peoria, Illinois, plant has experienced a $10,325 budget overrun, while the

Waco, Texas, plant has experienced a budget surplus of $1,800 and the Or-

lando, Florida, plant experienced a small overrun of $2,000. The budget of the

E14–2

STATHAM CONSTRUCTION COMPANY

Divisional Income Statements

For the Year Ended November 30, 20Y3

Residential Industrial

Division Division

Net sales ………………………………………………………………….. $ 2,300,000 $ 5,750,000

Cost of goods sold …………………………………………………… 1,450,000 3,450,000

E14–3

Expense Activity Bases

a. Accounts Receivable Number of invoices, number of customers

b. Central Purchasing Number of requisitions, number of purchase

orders

E14–4

a. 6 e. 8

E14–5

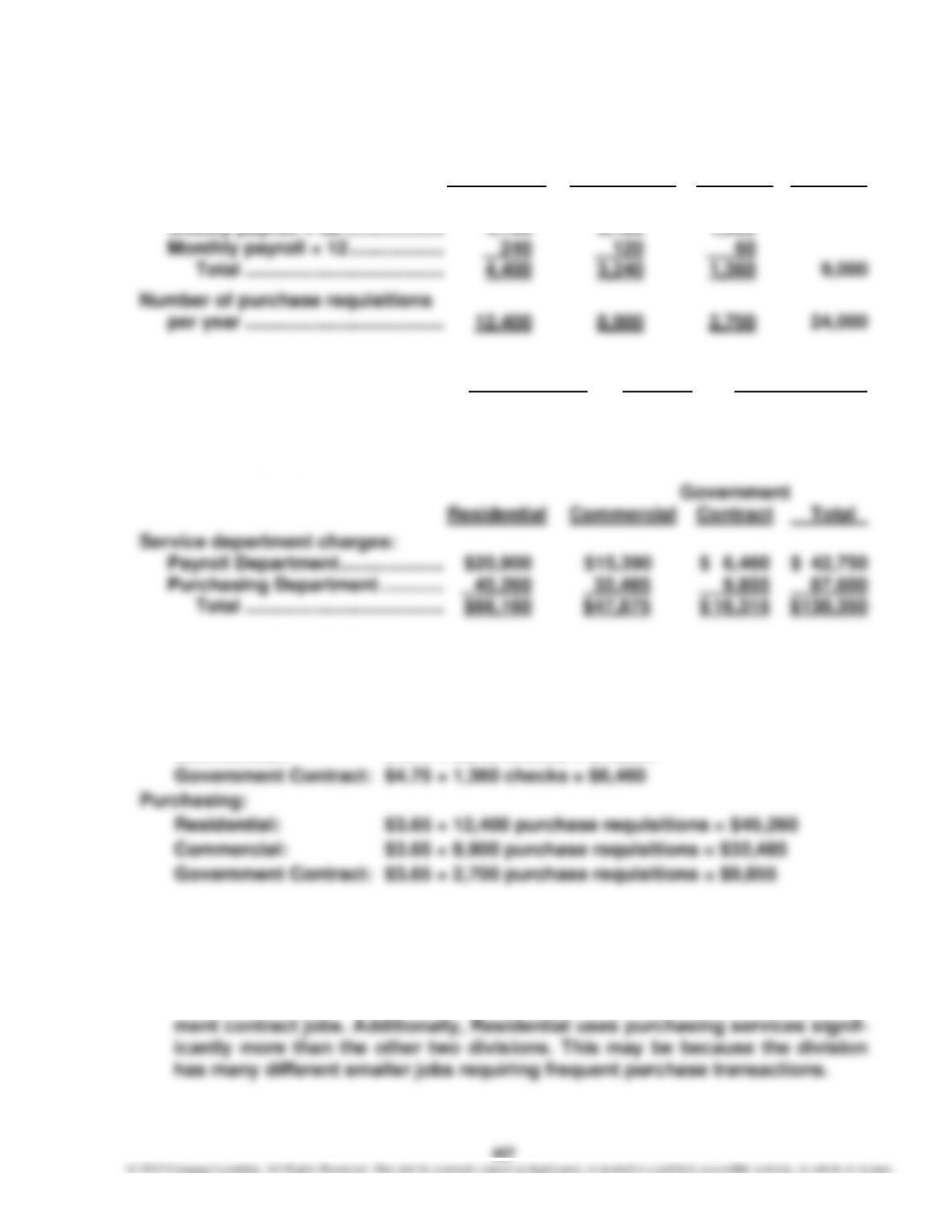

a. Government

Residential Commercial Contract Total

Number of payroll checks:

b. Service Dept. Activity Charge

Cost ÷ Base = Rate

Service department charge rates:

Payroll Department ……………….. $42,750 ÷ 9,000 = $4.75 per check

Purchasing Department ………… $87,600 ÷ 24,000 = $3.65 per req.

The service department charges are determined by multiplying the service

department charge rate by the activity base for each division as shown below.

Payroll:

Residential: $4.75 × 4,400 checks = $20,900

Commercial: $4.75 × 3,240 checks = $15,390

c. Residential’s service department charge is higher than the other two divi-

sions because Residential is a heavy user of service departments. Residential

has many employees on a weekly payroll, which translates into a larger num-

ber of check-issuing transactions. This may be because residential jobs are

less productive per labor hour, compared to larger commercial and govern-

458

E14–6

a. Help desk:

calls 5,000

$135,000

= $27.00 per call

b. February charges to the Electronics sector:

Help desk: (2,000 employees × 60% × 100% × 0.45) × $27.00 per call = $14,580

Network center: [(2,000 employees × 60% × 100%) + 80] × $48.40 per device =

$61,952

459

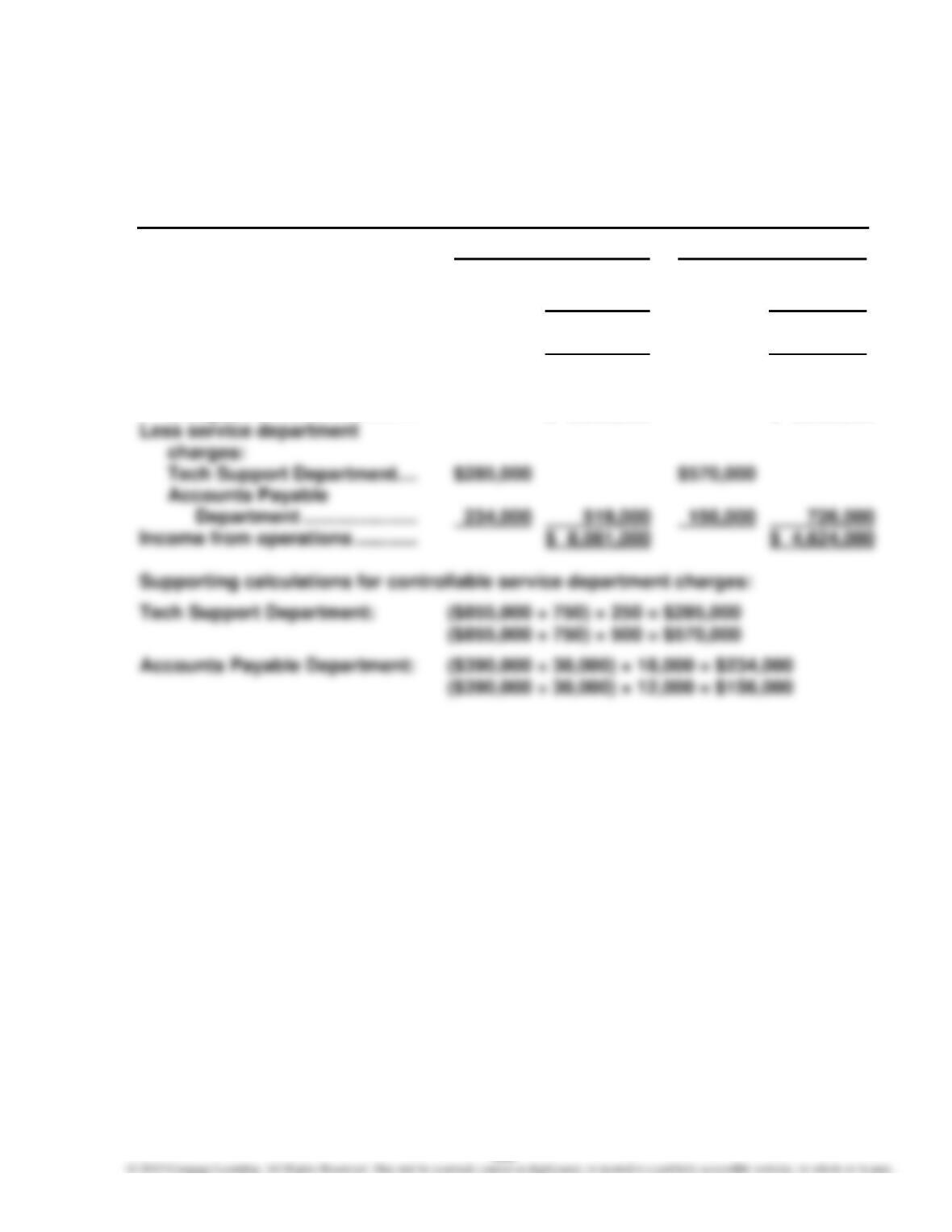

E14–7

POWER SPORTS COMPANY

Divisional Income Statements

For the Year Ended December 31, 20Y7

Wholesale Division Retail Division

Revenues ……………………………… $24,600,000 $13,750,000

Cost of goods sold ……………….. 14,500,000 8,000,000

Gross profit ………………………….. $ 10,100,000 $ 5,750,000

Operating expenses ………………. 1,500,000 400,000

Income from operations

before service department

charges ………………………….... $ 8,600,000 $ 5,350,000

460

E14–8

a. The reported income from operations does not accurately measure perfor-

mance because the service department charges are based on revenues. Rev-

enues are not associated with the profit center manager’s use of the service

greater than the Cargo Division.

b.

PANDA AIRLINES INC.

Divisional Income Statements

For the Year Ended April 30, 20Y9

Passenger Division Cargo Division

Revenues ……………………………… $7,500,000 $5,000,000

Operating expenses ……………… 4,500,000 2,700,000

Income from operations

Note 1: Passenger Division, ($500,000 ÷ 800 personnel trained) × 600

Cargo Division, ($500,000 ÷ 800 personnel trained) × 200

Note 2: Passenger Division, ($350,000 ÷ 5,000 flights) × 4,000

Cargo Division, ($350,000 ÷ 5,000 flights) × 1,000

461

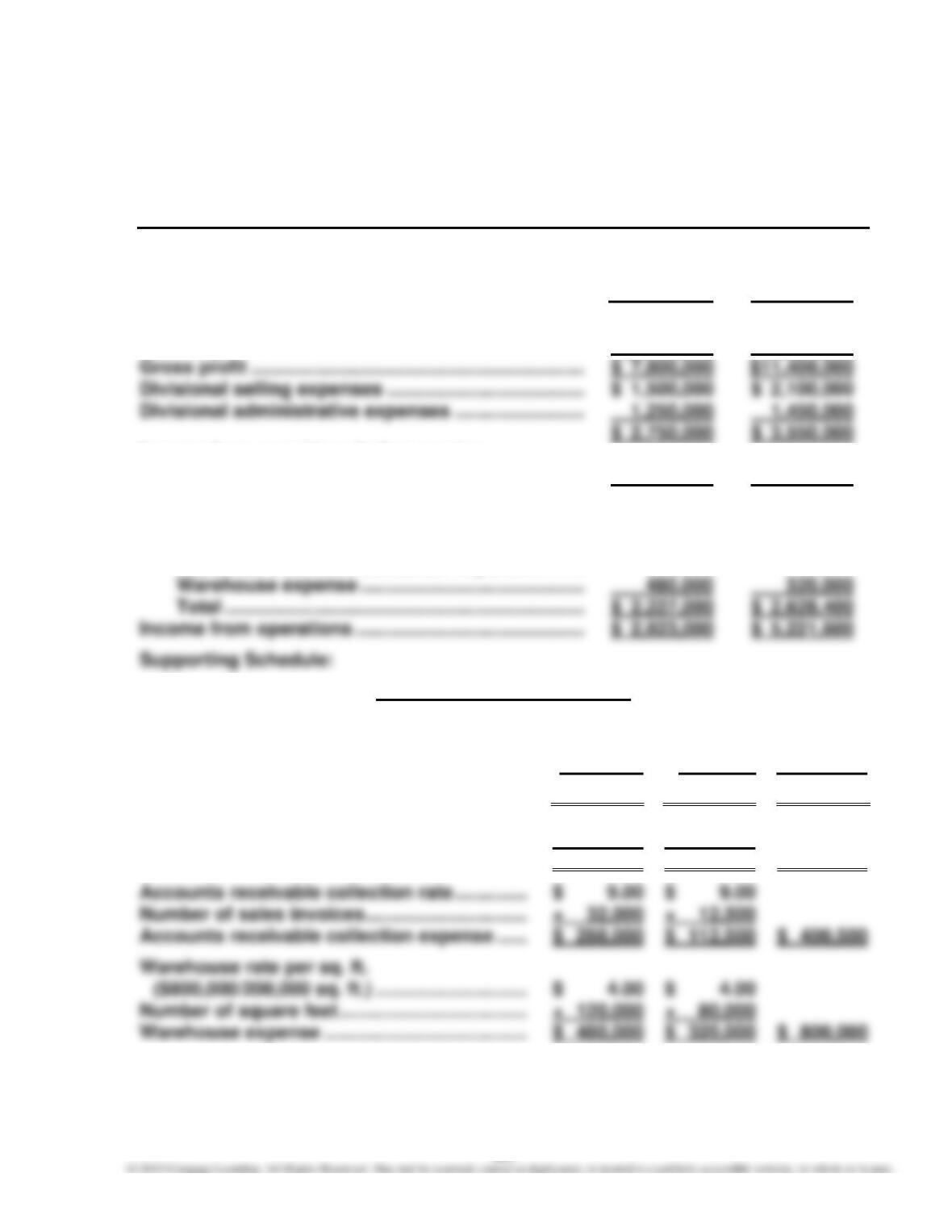

E14–9

ON-DEMAND SPORTS CO.

Divisional Income Statements

For the Year Ended November 30, 20Y1

Action Team

Sports Sports

Division Division

Sales ………………………………………………………………… $18,500,000 $30,600,000

Cost of goods sold ……………………………………………. 10,700,000 19,200,000

Income from operations before service

department charges…………………………………….. $ 5,050,000 $ 7,850,000

Less service department charges:

Advertising expense ……………………………………. $ 1,200,000 $ 1,800,000

Transportation expense ………………………………. 259,000 395,900

Accounts receivable collection expense ………. 288,000 112,500

Service Department Charges

Action Team

Sports Sports

Division Division Total

Advertising expense ………………………………… $1,200,000 $1,800,000 $3,000,000

Transportation rate per bill of lading ………… $ 18.50 $ 18.50

Number of bills of lading ………………………….. × 14,000 × 21,400

Transportation expense …………………………... $ 259,000 $ 395,900 $ 654,900

462

E14–10

a. Sporting Goods Division: 18% ($540,000 ÷ $3,000,000)

E14–11

a.

Sporting Health

Goods Club School

Division Division Division

Income from operations ……………………… $540,000 $418,000 $455,000

Minimum amount of income from

operations:

463

E14–12

a. 1.50 = 12% ÷ 8%

E14–13

a.

Investment

on Return of Rate

= Profit Margin × Investment Turnover

Investment

on Return of Rate

b. The profit margin would increase from 16% to 17%, the investment turnover

would remain unchanged, and the rate of return on investment would in-

crease from 19.2% to 20.4%, as shown below.

Investment

on Return of Rate

= Profit Margin × Investment Turnover

Investment

on Return of Rate

464

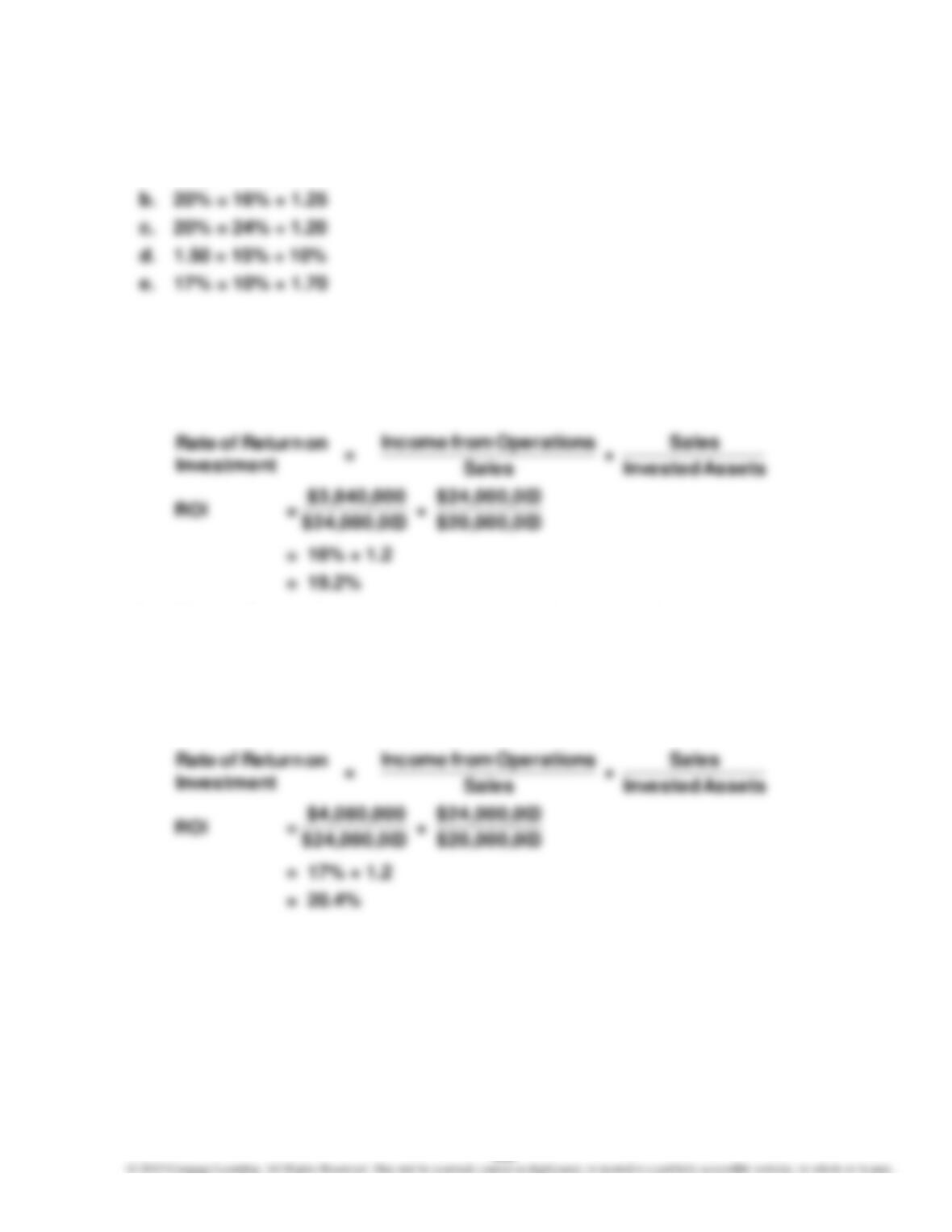

E14–14

a. Rate of Return on Investment =

Revenues

Operations from Income

×

AssetsInvested

Revenues

Media Networks:

$19,436

$6,619

×

$28,660

$19,436

$12,920

$1,902

$12,920

Studio Entertainment:

$5,825

$722

×

$12,928

$5,825

= 12.4% × 0.45

= 5.6% (rounded)

$3,252

$5,016

b. The four sectors are different from each other. Media Networks combines a

good profit margin of 34.1% with a low investment turnover of 0.68 to yield

E14–15

a. 16% ($400,000 ÷ $2,500,000)

b. $300,000 ($2,500,000 × 12%)

c. $100,000 ($400,000 – $300,000)

466

E14–16

a. (a) $1,200,000 ($6,000,000 × 20%)

(b) $7,500,000 ($1,200,000 ÷ 16%)

(c) 0.8 (16% ÷ 20%) or ($6,000,000 ÷ $7,500,000)

(d) $12,600,000 ($1,512,000 ÷ 12%)

(l) 1.5 ($5,250,000 ÷ $3,500,000)

b. California Division: $450,000 [$1,200,000 – ($7,500,000 × 10%)]

Midwest Division: $612,000 [$1,512,000 – ($9,000,000 × 10%)]

Northwest Division: $825,000 [$1,925,000 – ($11,000,000 × 10%)]

Texas Division: $490,000 [$840,000 – ($3,500,000 × 10%)]

467

E14–17

a. Rate of Return on Investment =

Revenues

Operations from Income

×

AssetsInvested

Revenues

North American—Full Service:

$5,450

$2,358

$382

International:

ROI =

$1,278

$175

×

$1,026

$1,278

= 13.7% × 1.25 = 17.1% (rounded)

$1,673

N. American— N. American—

b. Full Service Limited Serv. International Luxury

Income from

operations …………. $351 $382 $175 $ 74

E14–17, Concluded

c. The North American—Limited Service segment has the highest return on in–

vestment of 76.8% due to a strong investment turnover of 4.74, which may be a

result of more franchise operations in this segment.

469

E14–18

Although there is some judgment in classifying each of these measures, the fol-

lowing represents our assessment with explanations:

Average cardmember spending Customer—demonstrates the useful-

ness of the card to the customer.

Number of Internet features Internal process (or innovation)—shows

new process investments in a new

channel.

Number of merchant signings Customer—the larger the number of

merchants that honor the card, the more

valuable it is to cardholders.

Number of card choices Customer—more choices are more valu-

able to customers.

470

E14–19

a. UPS wanted a performance measurement system that would focus more on

the underlying drivers, or levers, of financial success. It believed that focus-

ing on the financial numbers by themselves would not reveal how financial

objectives were to be achieved, especially with new demands coming from

would straight financial numbers.

b. The employee sentiment number is common in service businesses. The

employees are the face of the company to the customer. If employees feel

poorly about the organization, or if they feel that they don’t make a difference,

E14–20

a.

Operations from

Income sing‘Manufactur

Retina in Increase

=

Price

Market

–

Unit per Cost

Variable

×

dTransferre

Units

$225,000 = ($75 – $66) × 25,000

Price

Market

dTransferre

Units