CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Ex. 14–26

a. Present value of $1 for 10 semiannual

periods at 6.0% semiannual rate………………………

…

0.55839

Face amount of bonds……………………………………

…

$80,000,000 $44,671,200

b. 6.0% of carrying amount of $71,167,524……………………………………

…

$ 4,270,051

c. 6.0% of carrying amount of $71,837,575*……………………………………

…

$ 4,310,255

…

d. Annual interest paid……………………………………………………………

…

$ 7,200,000

×

14-18

…

…

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Prob. 14–1A

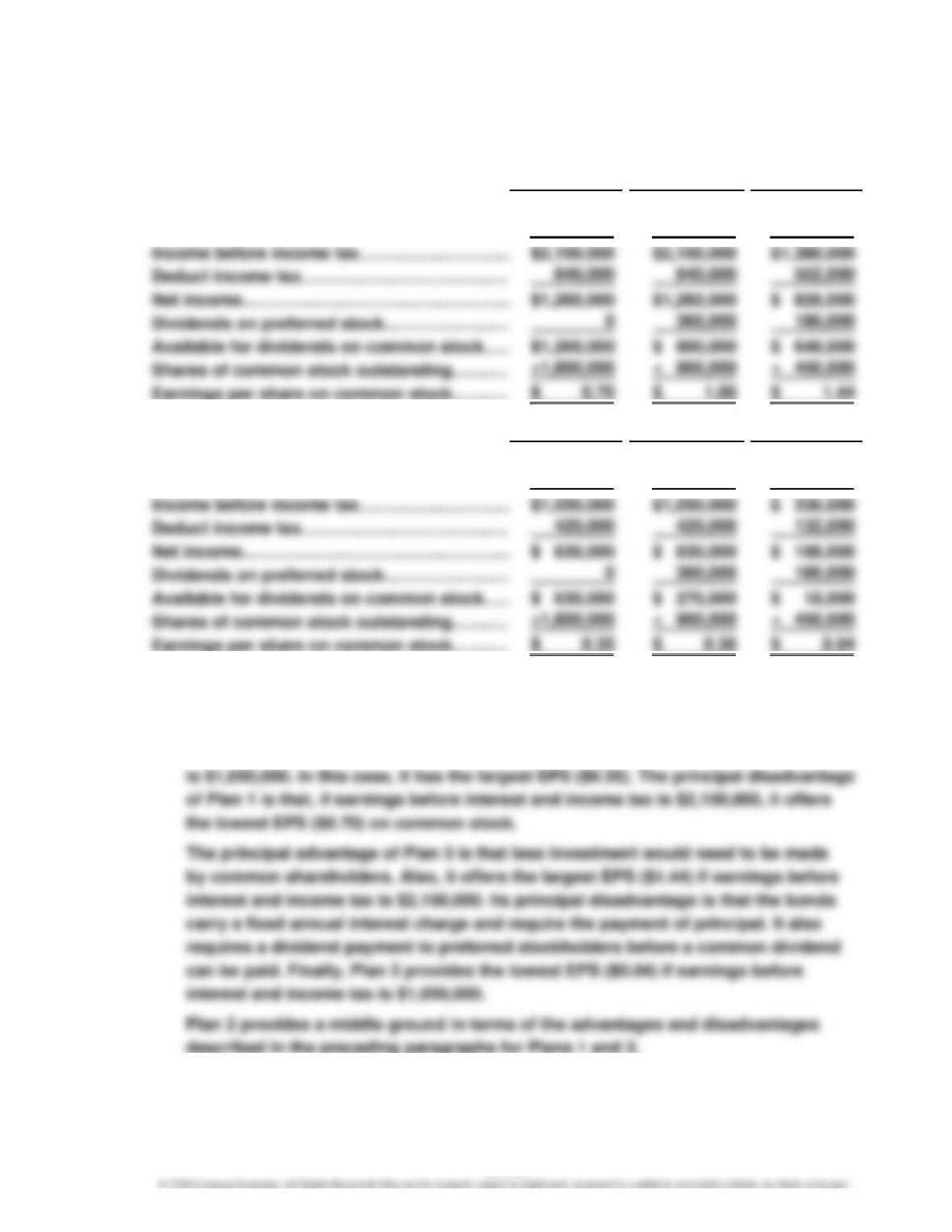

1. Plan 1 Plan 2 Plan 3

Earnings before interest and income tax……

…

$2,100,000 $2,100,000 $2,100,000

Deduct interest on bonds………………………

…

0 0 720,000

2. Plan 1 Plan 2 Plan 3

Earnings before interest and income tax……

…

$1,050,000 $1,050,000 $1,050,000

Deduct interest on bonds………………………

…

0 0 720,000

3. The principal advantage of Plan 1 is that it involves only the issuance of common

stock, which does not require a periodic interest payment or return of principal,

and a payment of preferred dividends is not required. It is also more attractive to

common shareholders than is Plan 2 or 3 if earnings before interest and income tax

PROBLEMS

14-19

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Prob. 14–2A

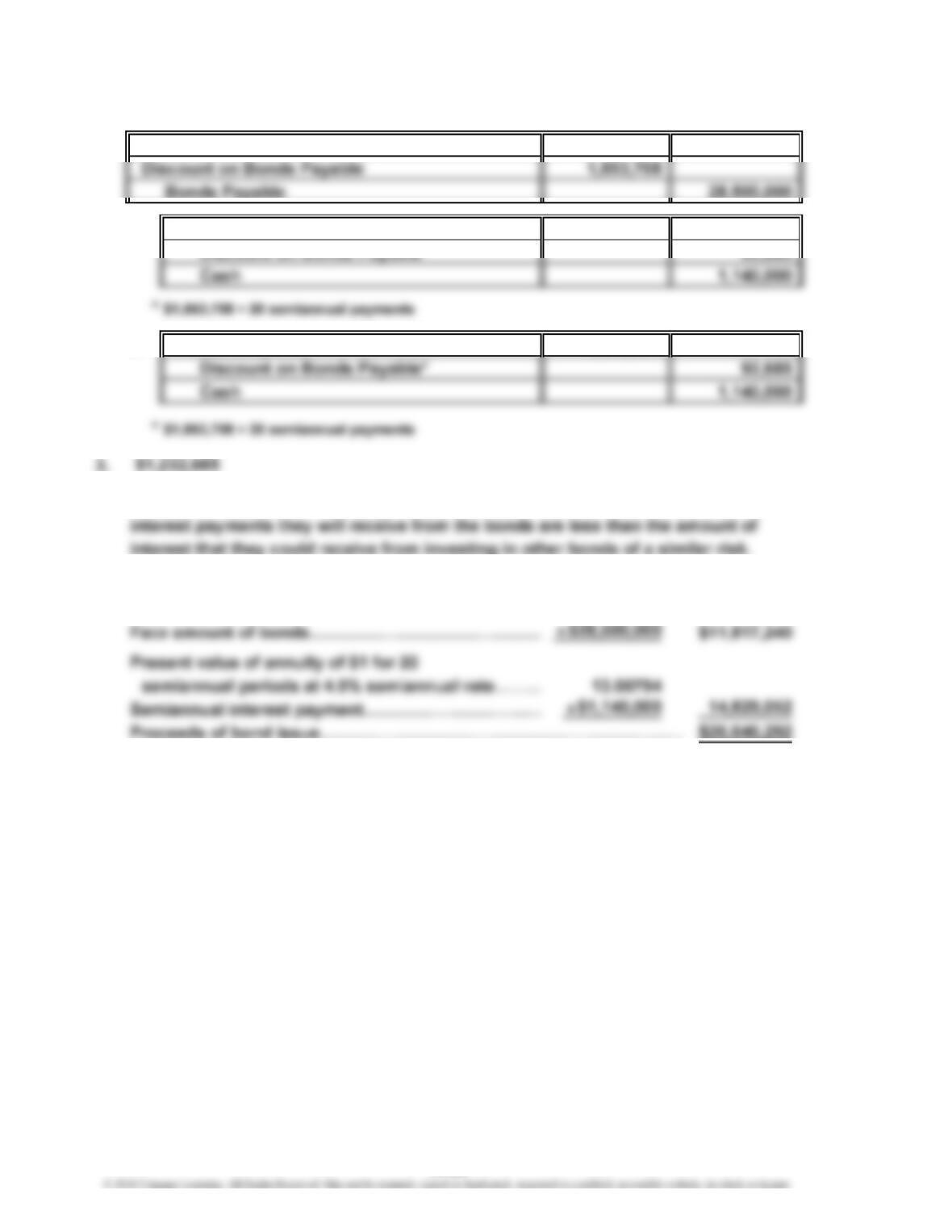

1. Cash 26,646,292

2. a. Interest Expense 1,232,685

b. Interest Expense 1,232,685

4. Yes. Investors will not be willing to pay the face amount of the bonds when the

5. Present value of $1 for 20 semiannual

periods at 4.5% semiannual rate……………………

…

0.41464

14-20

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Prob. 14–3A

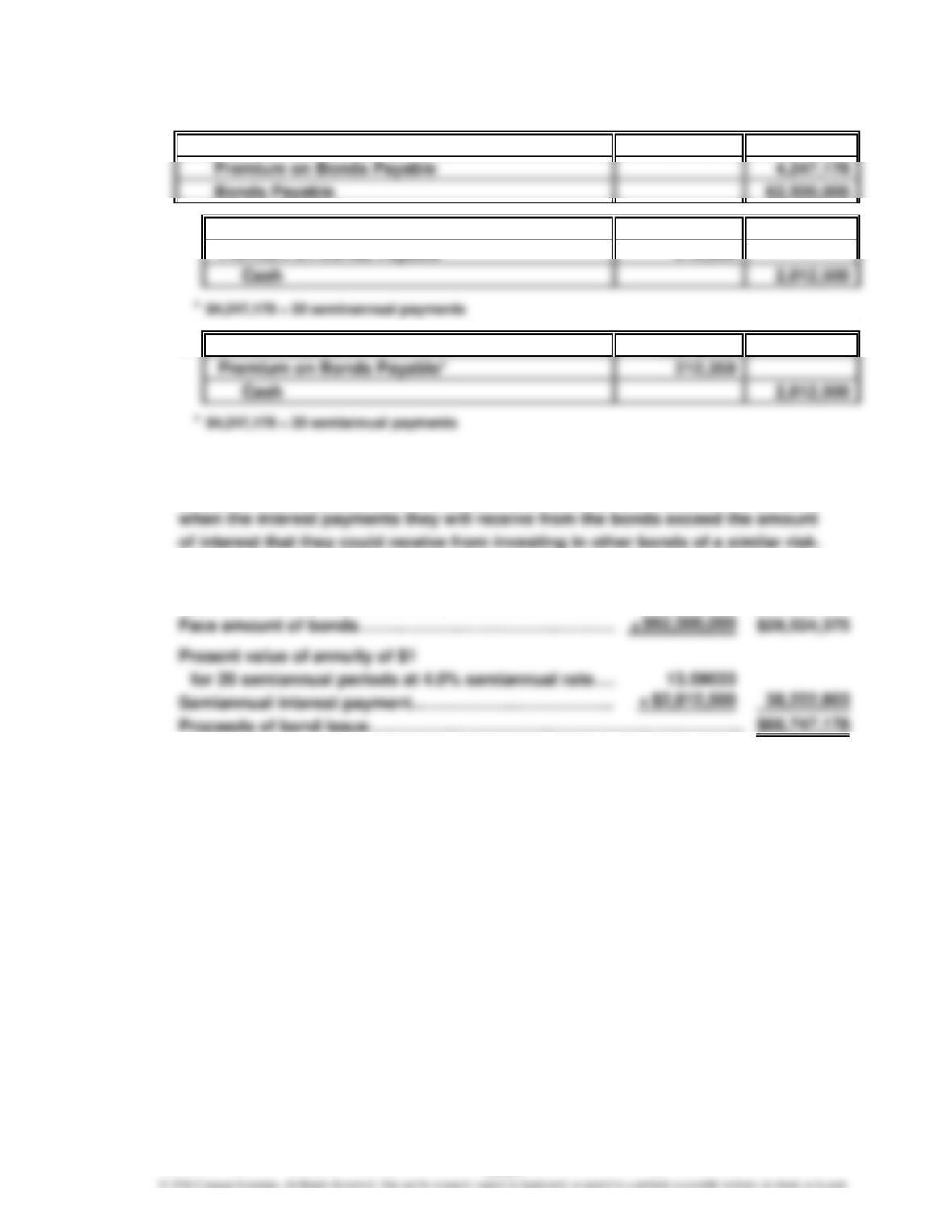

1. Cash 66,747,178

2. a. Interest Expense 2,600,141

Premium on Bonds Payable* 212,359

b. Interest Expense 2,600,141

3.

4. Yes. Investors will be willing to pay more than the face amount of the bonds

5. Present value of $1 for 20 semiannual

periods at 4.0% semiannual rate………………………… 0.45639

$2,600,141

14-21

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

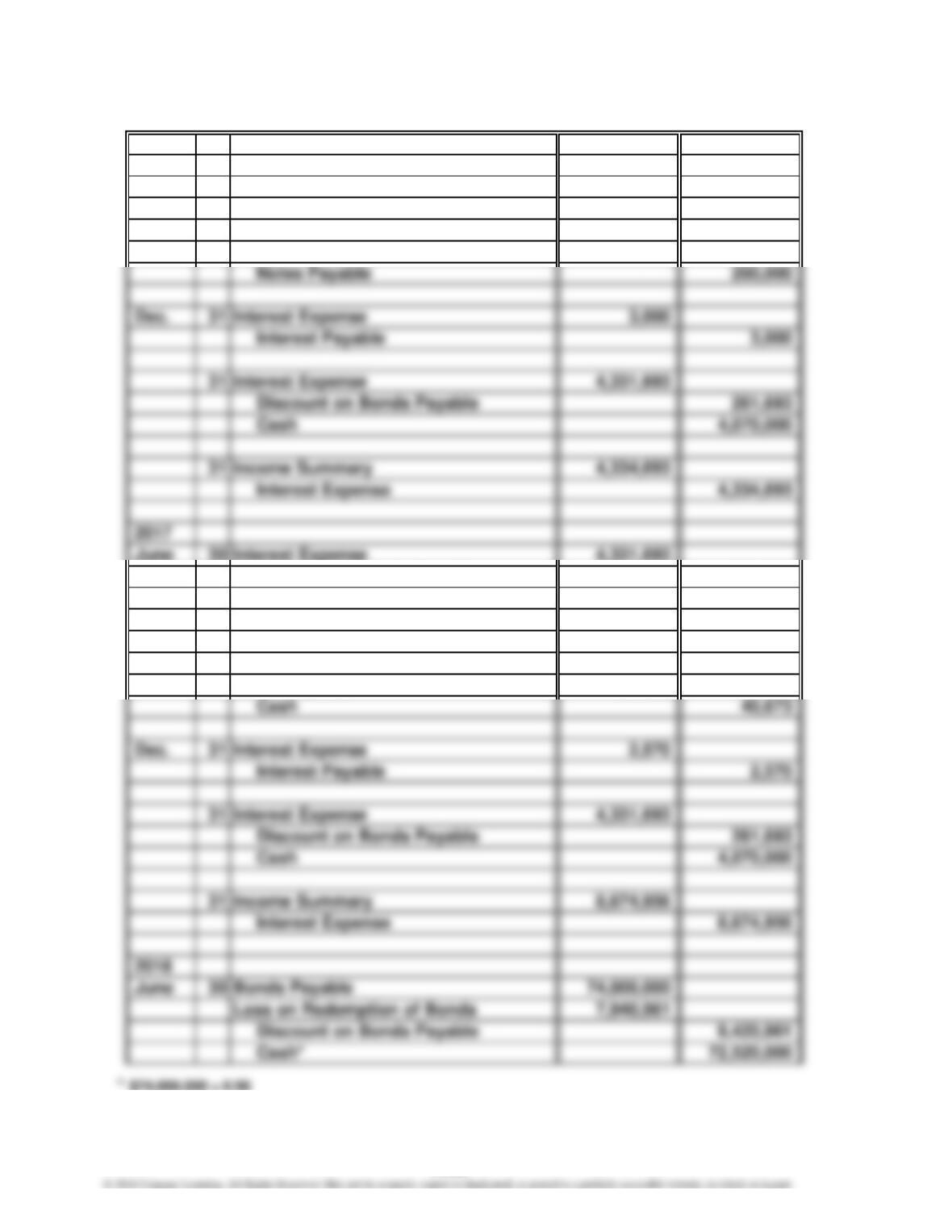

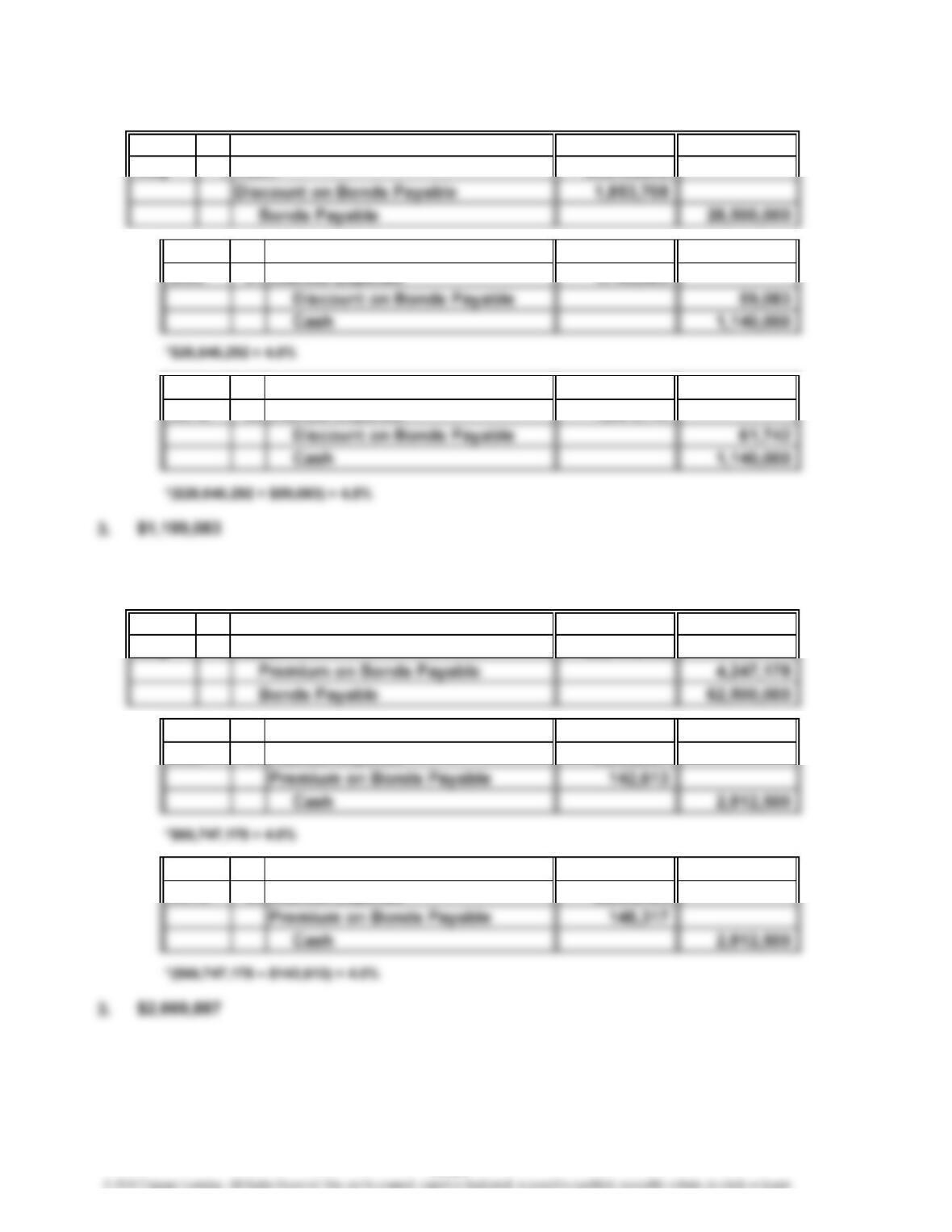

Prob. 14–4A

1.

1 Cash 63,532,267

Discount on Bonds Payable 10,467,733

Bonds Payable 74,000,000

1 Cash 200,000

Discount on Bonds Payable 261,693

Cash 4,070,000

30 Interest Expense 9,000

Interest Payable 3,000

Notes Payable 28,673

2016

July

Oct.

Sept

14-22

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

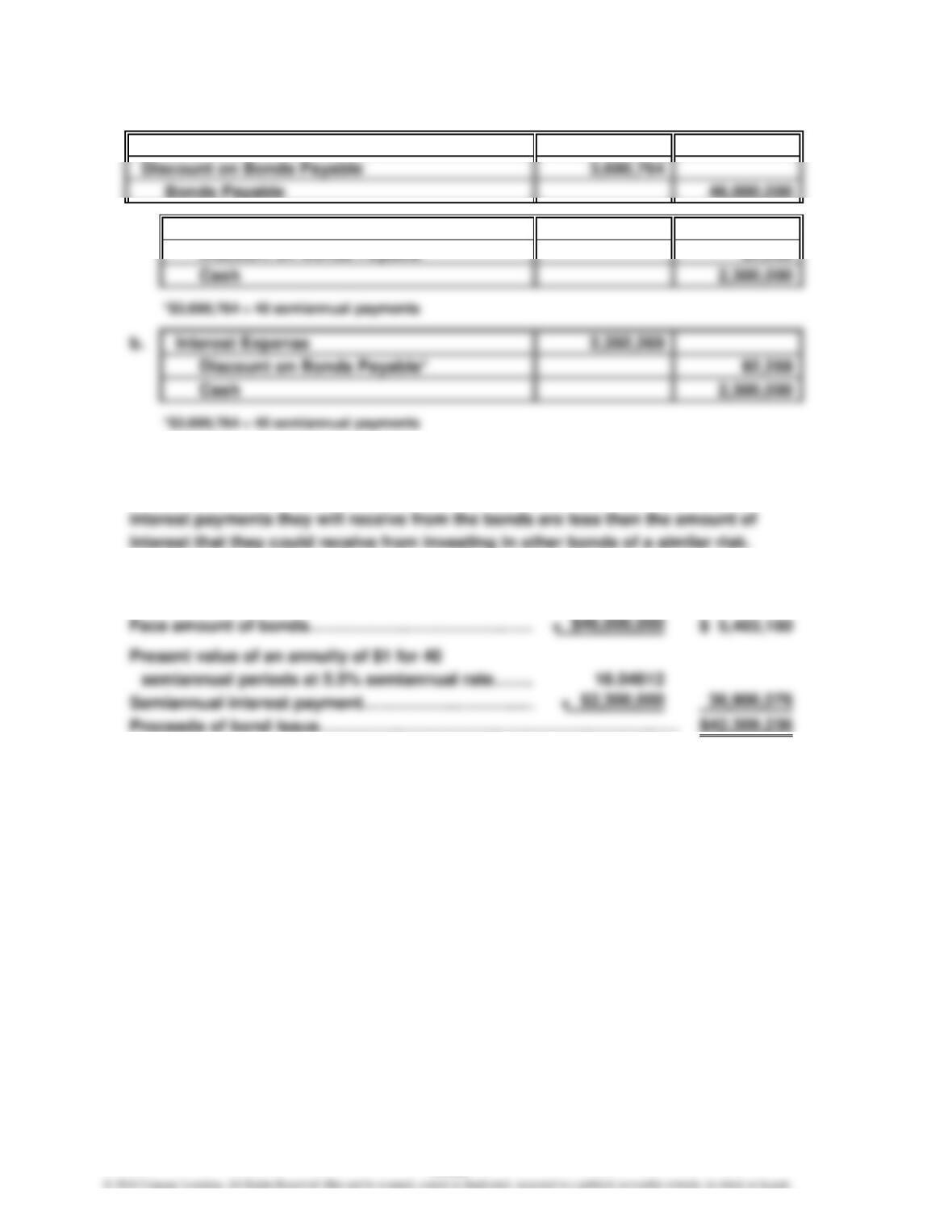

Prob. 14–4A (Concluded)

30 Interest Expense 7,710

3. Initial carrying amount of bonds……………………………………………

…

$63,532,267

Discount amortized on December 31, 2016………………………………

…

261,693

…

…

2018

Sept

14-23

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

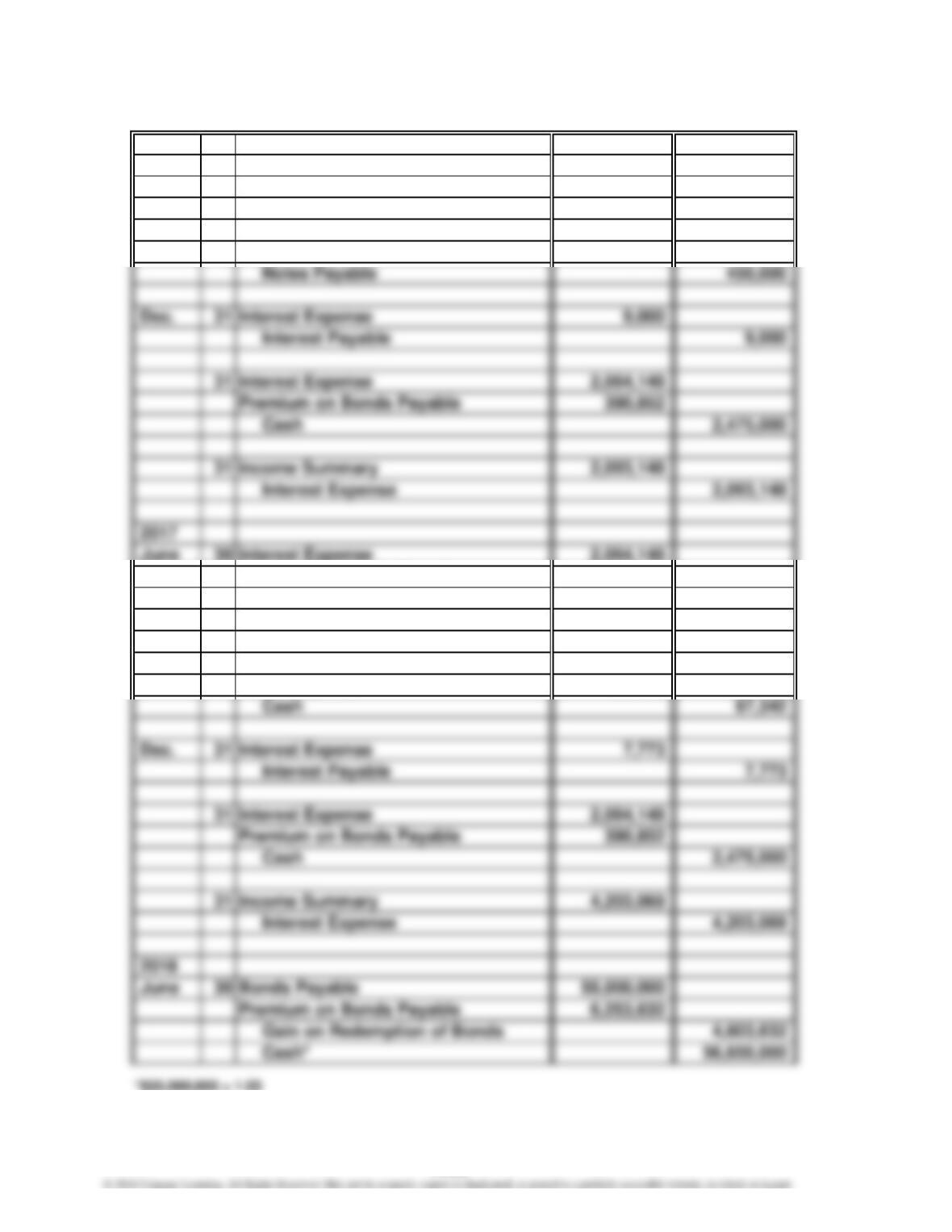

Prob. 14–5A

1. 2016

July 1 Cash 26,646,292

2. a.

31 Interest Expense* 1,199,083

b.

30 Interest Expense* 1,201,742

Prob. 14–6A

1. 2016

July 1 Cash 66,747,178

2. a.

31 Interest Expense* 2,669,887

b.

30 Interest Expense* 2,664,183

2016

Dec.

2017

June

2017

Dec.

2016

June

14-24

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Prob. 14–1B

1. Plan 1 Plan 2 Plan 3

Earnings before interest and income tax……

…

$10,000,000 $10,000,000 $10,000,000

Deduct interest on bonds………………………

…

0 0 3,600,000

Income before income tax………………………

…

$10,000,000 $10,000,000 $ 6,400,000

2. Plan 1 Plan 2 Plan 3

Earnings before interest and income tax……

…

$6,000,000 $6,000,000 $6,000,000

Deduct interest on bonds………………………

…

0 0 3,600,000

Income before income tax………………………

…

$6,000,000 $6,000,000 $2,400,000

3. The principal advantage of Plan 1 is that it involves only the issuance of

common stock, which does not require a periodic interest payment or return of

principal, and a payment of preferred dividends is not required. It is also more

attractive to common shareholders than is Plan 2 or 3 if earnings before interest

14-25

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Prob. 14–2B

1. Cash 42,309,236

2. a. Interest Expense 2,392,269

Discount on Bonds Payable*

3.

4. Yes. Investors will not be willing to pay the face amount of the bonds when the

5. Present value of $1 for 40 semiannual

periods at 5.5% semiannual rate……………………

…

0.11746

$2,392,269

92,269

14-26

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Prob. 14–3B

1. Cash 73,100,469

2. a. Interest Expense 3,494,977

b. Interest Expense 3,494,977

4. Yes. Investors will be willing to pay more than the face amount of the bonds when

5. Present value of $1 for 20 semiannual

periods at 5% semiannual rate…………………… 0.37689

14-27

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

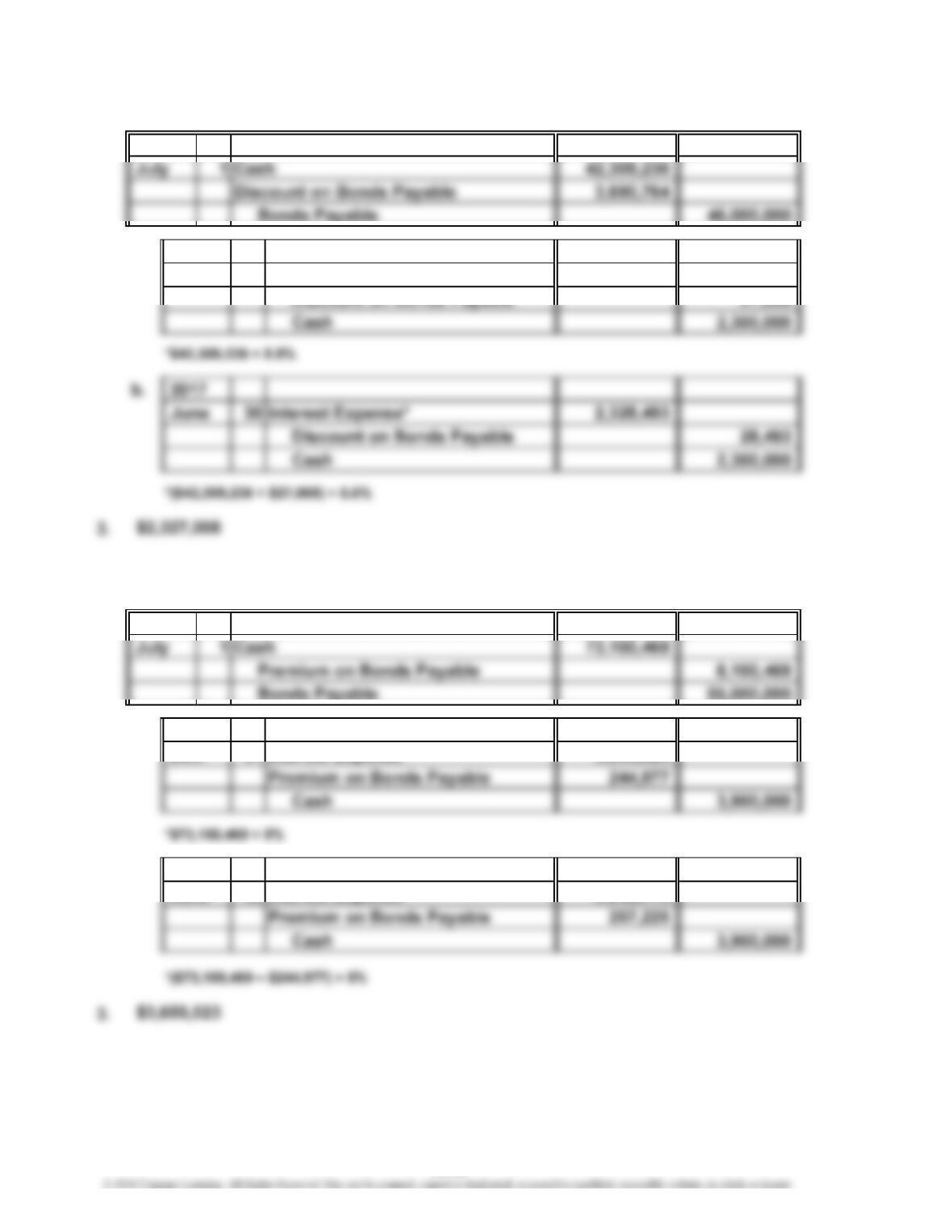

Prob. 14–4B

1.

1 Cash 62,817,040

Premium on Bonds Payable 7,817,040

Bonds Payable 55,000,000

1 Cash 450,000

Premium on Bonds Payable 390,852

Cash 2,475,000

30 Interest Expense 27,000

Interest Payable 9,000

Notes Payable 61,342

Oct.

2016

July

Sept.

14-28

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Prob. 14–4B (Concluded)

30 Interest Expense 23,320

2. a. 2016: 2,093,148

3. Initial carrying amount of bonds…………………………………………

…

$62,817,040

Premium amortized on December 31, 2016……………………………… (390,852)

2018

Sept.

14-29

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Prob. 14–5B

1. 2016

2. a.

31 Interest Expense* 2,327,008

Prob. 14–6B

1. 2016

2. a.

31 Interest Expense* 3,655,023

b.

30 Interest Expense* 3,642,775

Dec.

2016

2016

Dec.

2017

June

14-30

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

CP 14–1

GE Capital’s action was legal but caused a great public relations stir at the time.

Some quotes:

“A lot of people feel like they have been sorely used,” said one bond fund manager.

“There was nothing illegal about it, but it was nasty.”

The fund manager said that GE Capital’s decision to upsize its bond issue to $11

billion from $6 billion midway through the offering ordinarily wouldn’t have upset

bondholders.

CP 14–2

Without the consent of the bondholders, Bob’s use of the sinking fund cash to

CASES & PROJECTS

CP 14–3

Receive $100,000,000 today:

Present value of $100,000,000 today = $100,000,000

Receive $25,000,000 today, plus $9,000,000 per year for 8 years:

Present value of $25,000,000 today = $25,000,000

Present value of annual payments = $9,000,000 × 5.97130 (Present value of an

Receive $15,000,000 per year for 10 years:

Present value of annual payments = $15,000,000 × 7.02358 (Present value of an

annuity of $1 for 10 periods at 7%) = $105,353,700

CP 14–4

The primary advantage of issuing preferred stock rather than bonds is that the

preferred stock does not obligate Xentec to pay dividends, while interest on

14-32

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

CP 14–5

1.

Shares of common stock………………………………

…

400,000 950,000

Earnings before bond interest and income tax……… $5,000,000 $5,000,000

2. a. Factors to be considered in addition to earnings per share:

1. There is a definite legal obligation to pay interest on bonds, but there is

2. If the bonds are issued, there is a definite commitment to repay the

3. Present stockholders must purchase the new stock if they are to retain

their proportionate control and financial interest in the corporation.

b. Because the net income has been relatively stable in the past and anticipated

Plan 1 Plan 2

…

…

CP 14–6

$173,751 + $1,459,141

$173,751

Year 3:1. 9.4 =

14-34