CHAPTER 14

SOLUTIONS TO EXERCISES—SET B

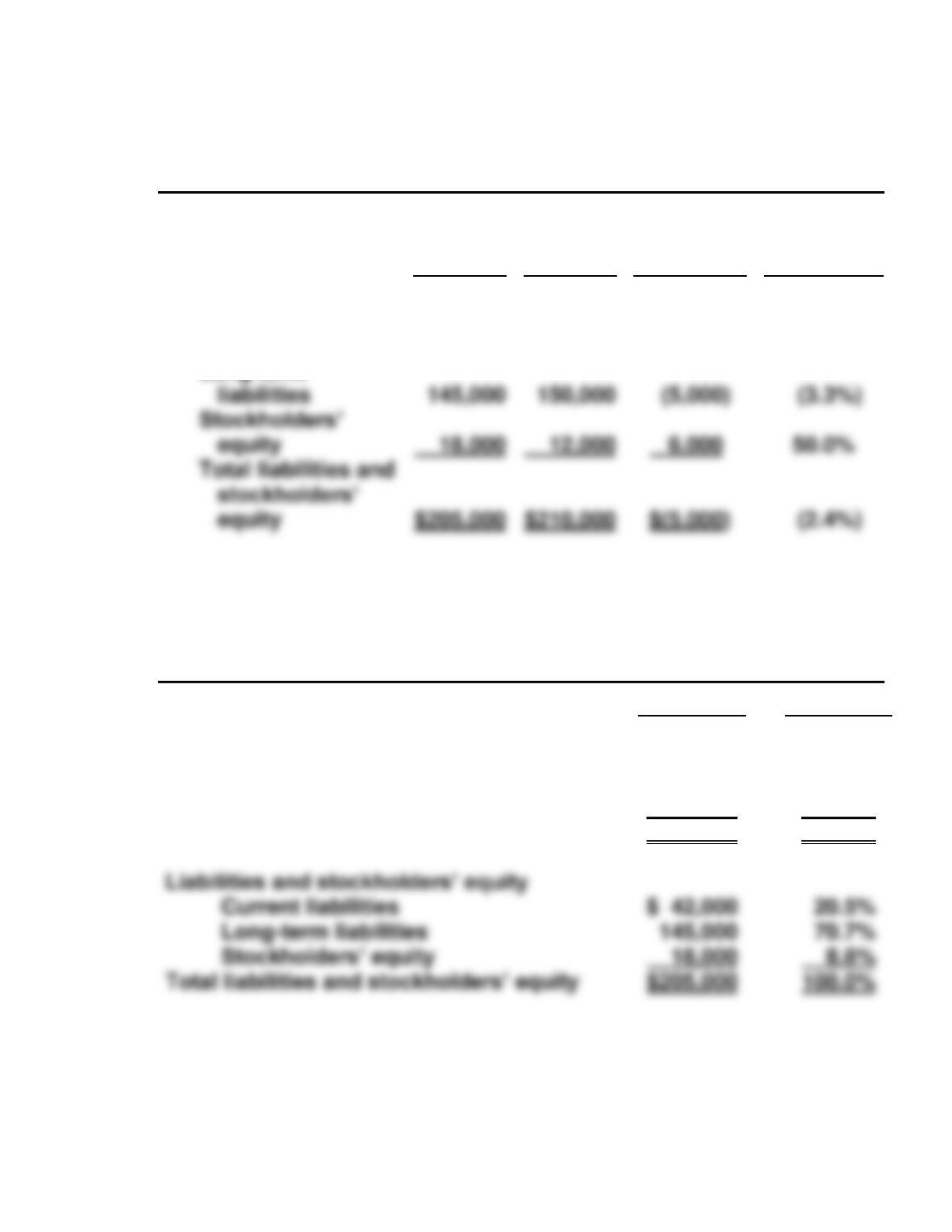

EXERCISE 14-1B

LARRS INC.

Condensed Balance Sheets

December 31

Increase or (Decrease)

2017

2016

Amount

Percentage

Assets

Current assets

$150,000

$100,000

($50,000

(50.0%)

Liabilities

Total liabilities

Stockholders’ Equity

Common stock, $1 par

Retained earnings

Total stockholders’

161,000

135,000

115,000

150,000

( 46,000

(40.0%)

(10.0%)

Total assets

EXERCISE 14-2B

SWENSON CORPORATION

Condensed Income Statements

For the Year Ended December 31

2017

2016

Amount

Percent

Amount

Percent

Sales revenue

Cost of goods sold

$750,000

450,000

100.0%

60.0%

$600,000

400,000

100.0%

66.7%

EXERCISE 14-3B

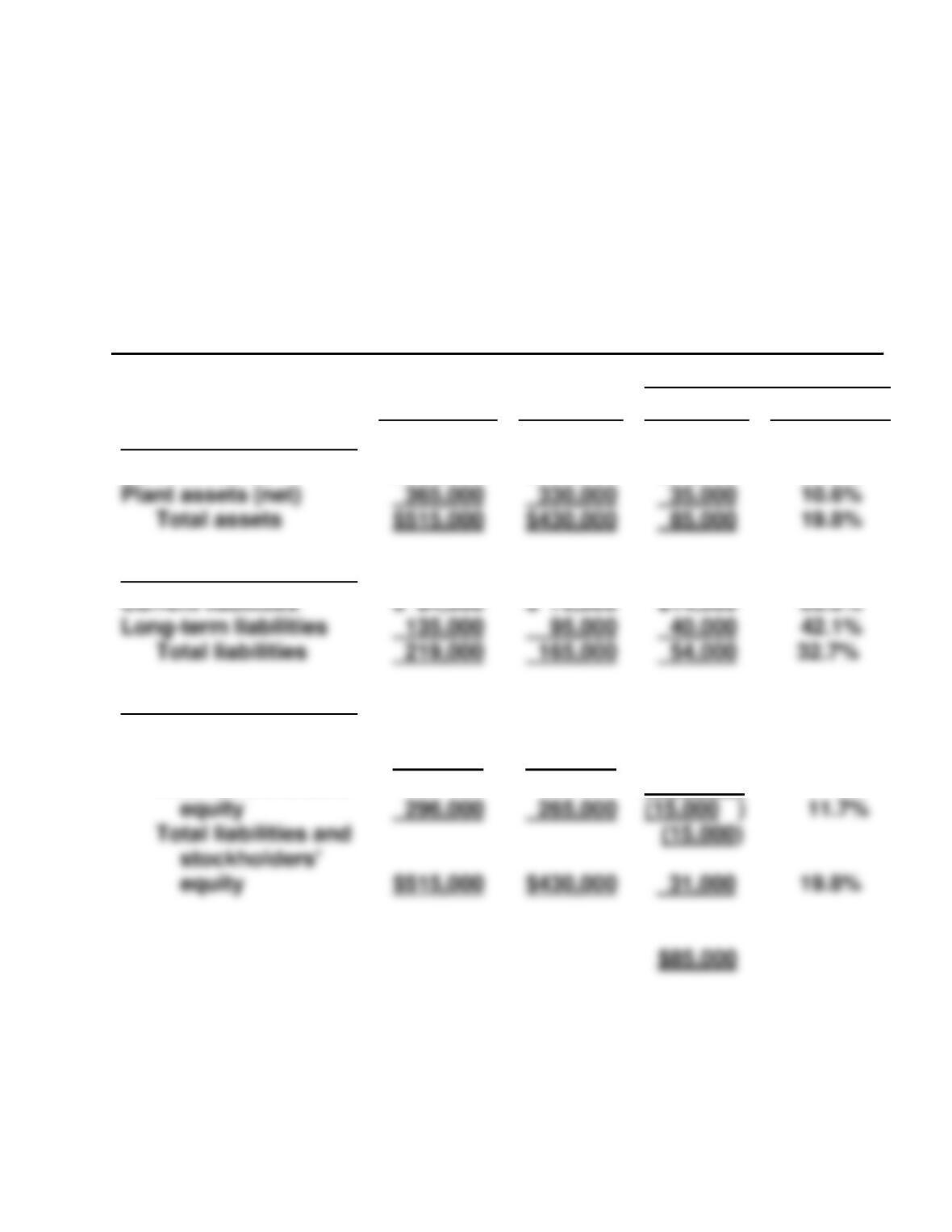

(a) DALLE CORPORATION

Condensed Balance Sheets

December 31

2017

2016

Increase

(Decrease)

Percentage

Change

from 2016

Assets

Current assets

Property, plant &

equipment (net)

$ 76,000

99,000

$ 80,000

90,000

$ (4,000)

( 9,000)

(5.0%)

(10.0%)

Selling expenses

Administrative expenses

Income before income taxes

100,000

60,000

140,000

84,000

54,000

62,000

EXERCISE 14-3B (Continued)

DALLE CORPORATION

Condensed Balance Sheets (Continued)

December 31

2017

2016

Increase

(Decrease)

Percentage

Change

from 2016

Liabilities and stock-

holders’ equity

Current liabilities

Long-term

$ 42,000

$ 48,000

$(6,000)

(12.5%)

(b) DALLE CORPORATION

Condensed Balance Sheet

December 31, 2017

Amount

Percent

Long-term liabilities

$205,000

Assets

Current assets

Property, plant, and equipment (net)

Intangibles

Total assets

$ 76,000

99,000

30,000

$205,000

37.1%

48.3%

14.6%

100.0%

Total liabilities and

$205,000

$210,000

EXERCISE 14-4B

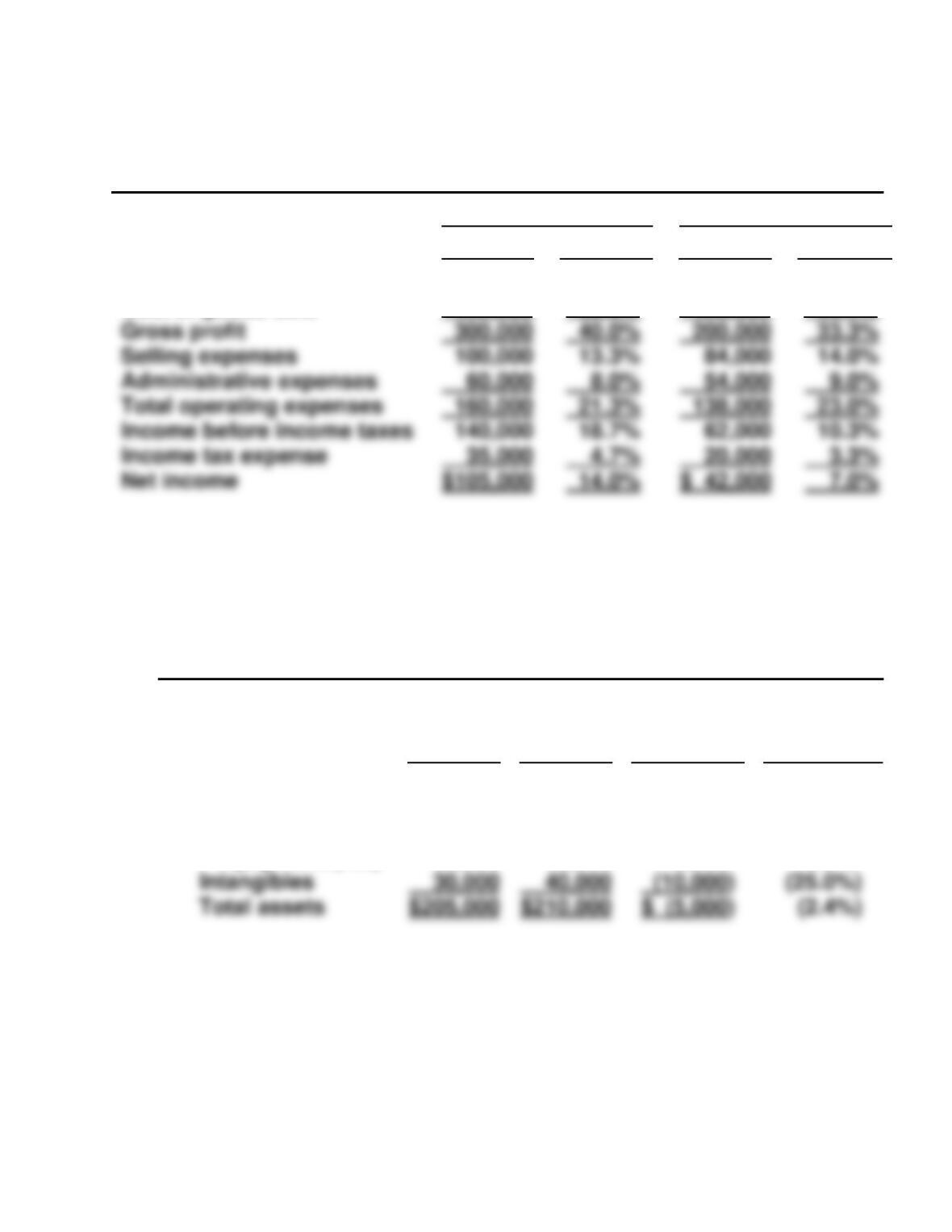

(a) FORREST CORPORATION

Condensed Income Statements

For the Year Ended December 31

Increase or (Decrease)

During 2017

2017

2016

Amount

Percentage

Net sales

Cost of goods sold

$550,000

440,000

$500,000

430,000

$50,000

10,000

10.0%

2.3%

(b) FORREST CORPORATION

Condensed Income Statements

For the Year Ended December 31

2017

2016

Amount

Percent

Amount

Percent

$ 60,000

9.1%

$ 35,000

Net sales

Cost of goods sold

$550,000

440,000

100.0%

80.0%

$500,000

430,000

100.0%

86.0%

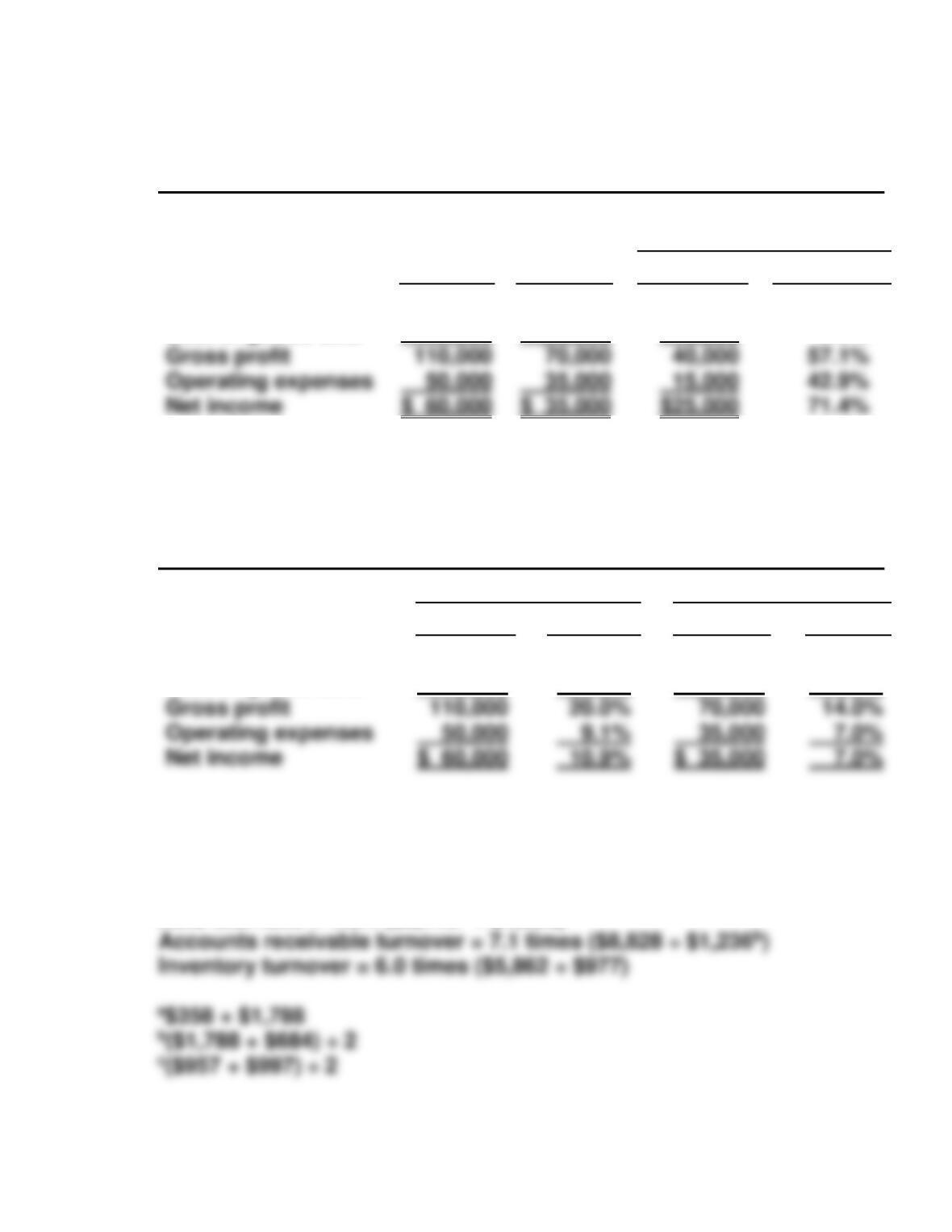

EXERCISE 14-5B

(a) Current ratio = 2.5:1 ($3,362 ÷ $1,350)

Acid-test ratio = 1.6:1 ($2,146a ÷ $1,350)

Net income

EXERCISE 14-5B (Continued)

(b)

Ratio

Nordstrom

J.C. Penney

Industry

Current

Acid-test

Accounts receivable

turnover

Inventory turnover

2.5:1

1.6:1

7.1

6.0

2.02:1

0.87:1

57.0

3.5

1.06:1

0.29:1

28.2

7.0

EXERCISE 14-6B

(a) Current ratio as of February 1, 2016 = 2.5:1 ($125,000 ÷ $50,000).

Feb. 3 2.5:1 No change in total current assets or liabilities.

7 1.9:1 ($97,000 ÷ $50,000).

(b) Acid-test ratio as of February 1, 2016 = 2.2:1 ($110,000* ÷ $50,000).

*$125,000 – $13,000 – $2,000

EXERCISE 14-7B

(a)

$20,000 + $80,000 + $60,000

$50,000

= 3.2:1.

(b)

$20,000 + $80,000

$50,000

= 2.0:1.

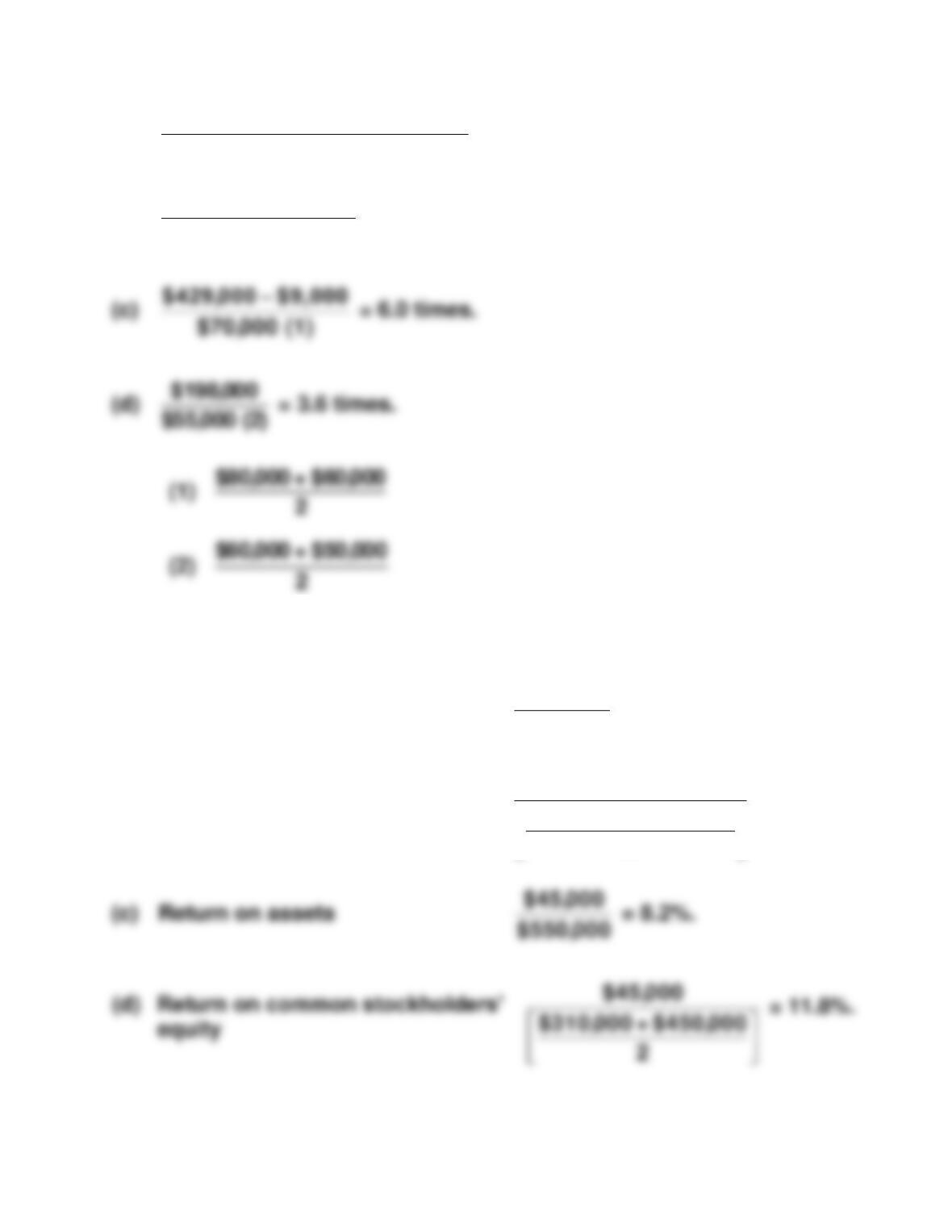

EXERCISE 14-8B

(a) Profit margin

$45,000

$800,000

= 5.6%.

(b) Asset turnover

$800,000

$500,000+$600,000

2

$45,000

$550,000

= 1.5 times.

EXERCISE 14-9B

(a) = $2.10.

EXERCISE 14-10B

(a) Inventory turnover = 4.0 =

Cost of goods sold

$220,000+$180,000

2

4.0 X $200,000 = Cost of goods sold

Cost of goods sold = $800,000.

$70,000 –$7,000

30,000 shares

EXERCISE 14-10B (Continued)

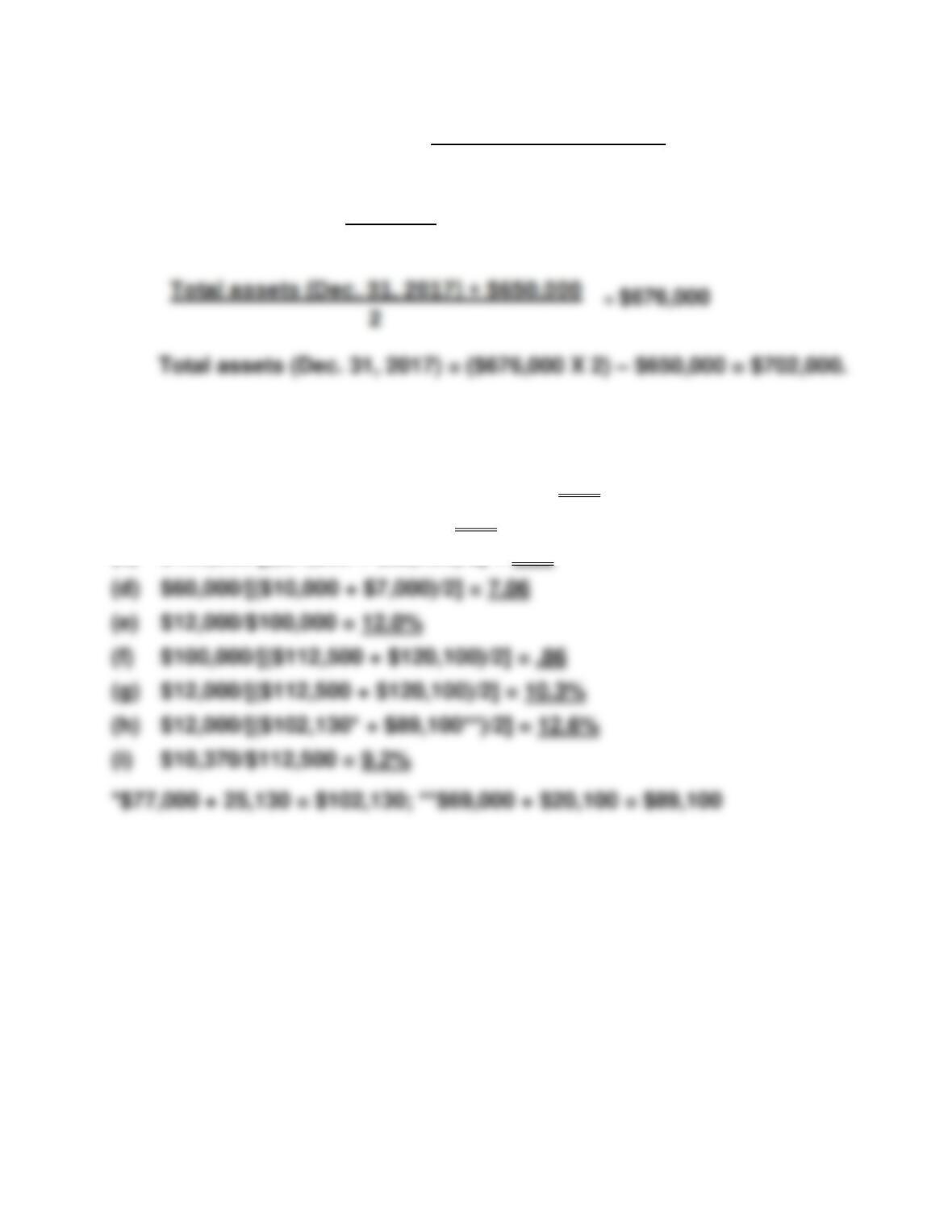

(d) Return on assets = 15% =

Average assets = = $676,000

EXERCISE 14-11B

(a) ($6,300 + $21,200 + $10,000)/$10,370 = 3.62

(b) ($6,300 + $21,200)/$10,370 = 2.65

(c) $100,000/[($21,200 + $22,400)/2] = 4.59

EXERCISE 14-12B

$101,400 [see (c) above]

Average assets

$101,400

.15

(a) SIMONE CORPORATION

Partial Income Statement

For the Year Ended October 31, 2017

Income before income taxes ………………………………………….. $650,000

Income tax expense ($650,000 X 30%) …………………………….. 195,000

Income from continuing operations ……………………………….. 455,000

EXERCISE 14-12B (Continued)

(b) To: Chief Accountant

From: Your name, Independent Auditor

After reviewing your income statement for the year ended 10/31/17, we

believe it is misleading for the following reasons:

EXERCISE 14-13B

FRANK CORPORATION

Partial Statement of Comprehensive Income

For the Year Ended December 31, 2017

Income from continuing operations ……………………………….. $350,000

Discontinued operations

Loss from operations of discontinued division, net

of $1,500income tax savings ……………………. ($3,500)