e.

PROBLEM 14.2A

DONELSON, INC. (concluded)

Favorable and unfavorable trends:

Favorable trends. One favorable trend is the $360,000 increase in net sales, which represented

an increase of about 14% over the prior year. A second favorable trend is the decrease in

15 Minutes, Easy

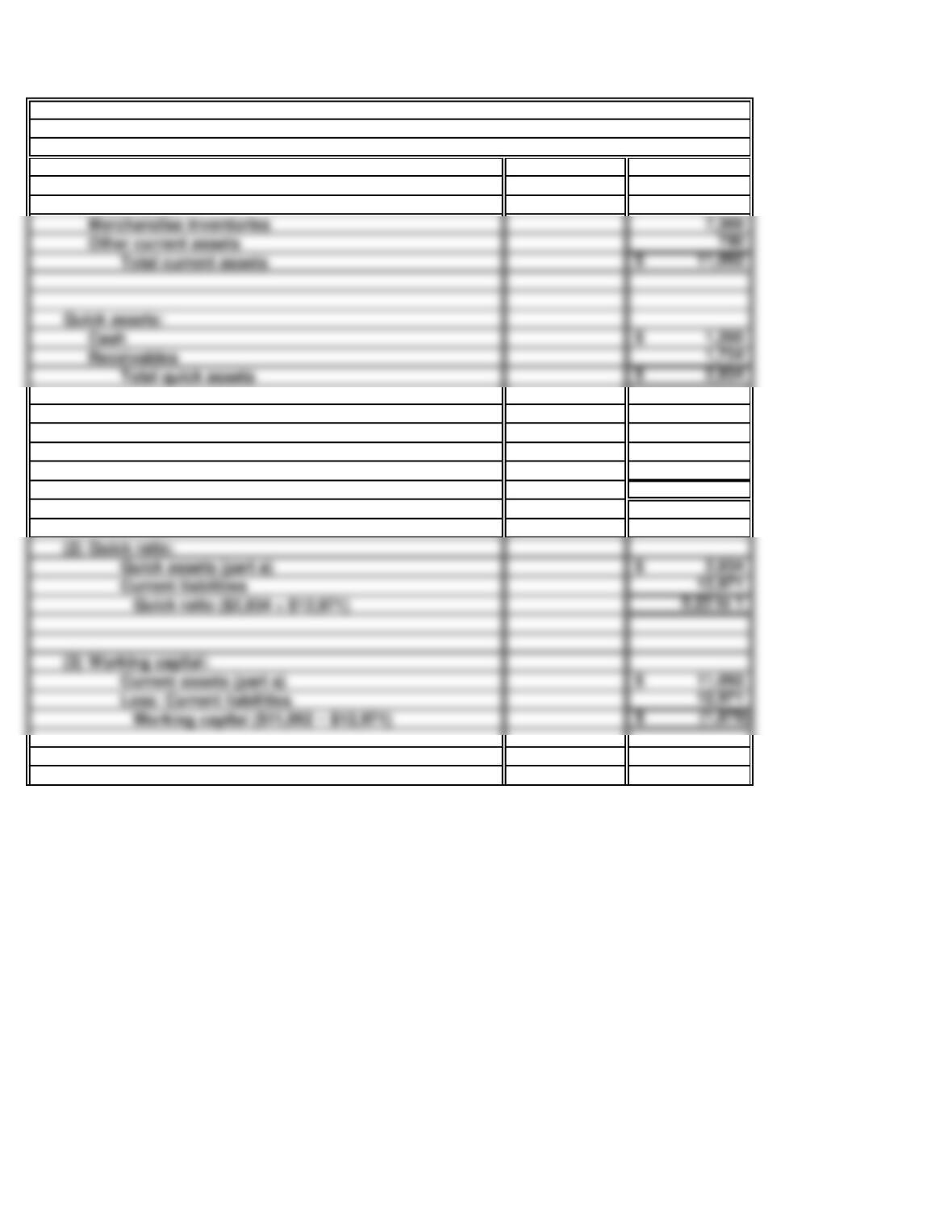

a. Current assets:

Cash 69,400$

Marketable securities 175,040

Accounts receivable 230,540

Inventory 179,600

b.

The current ratio is 2.86 to 1. It is computed by dividing the current assets of $659,080 by the

PROBLEM 14.3A

ROGAND GROCERY, INC.

Notes payable 70,000$

Income tax payable 14,600

25 Minutes, Easy

THE KROGER COMPANY, INC.

(Dollars in

Millions)

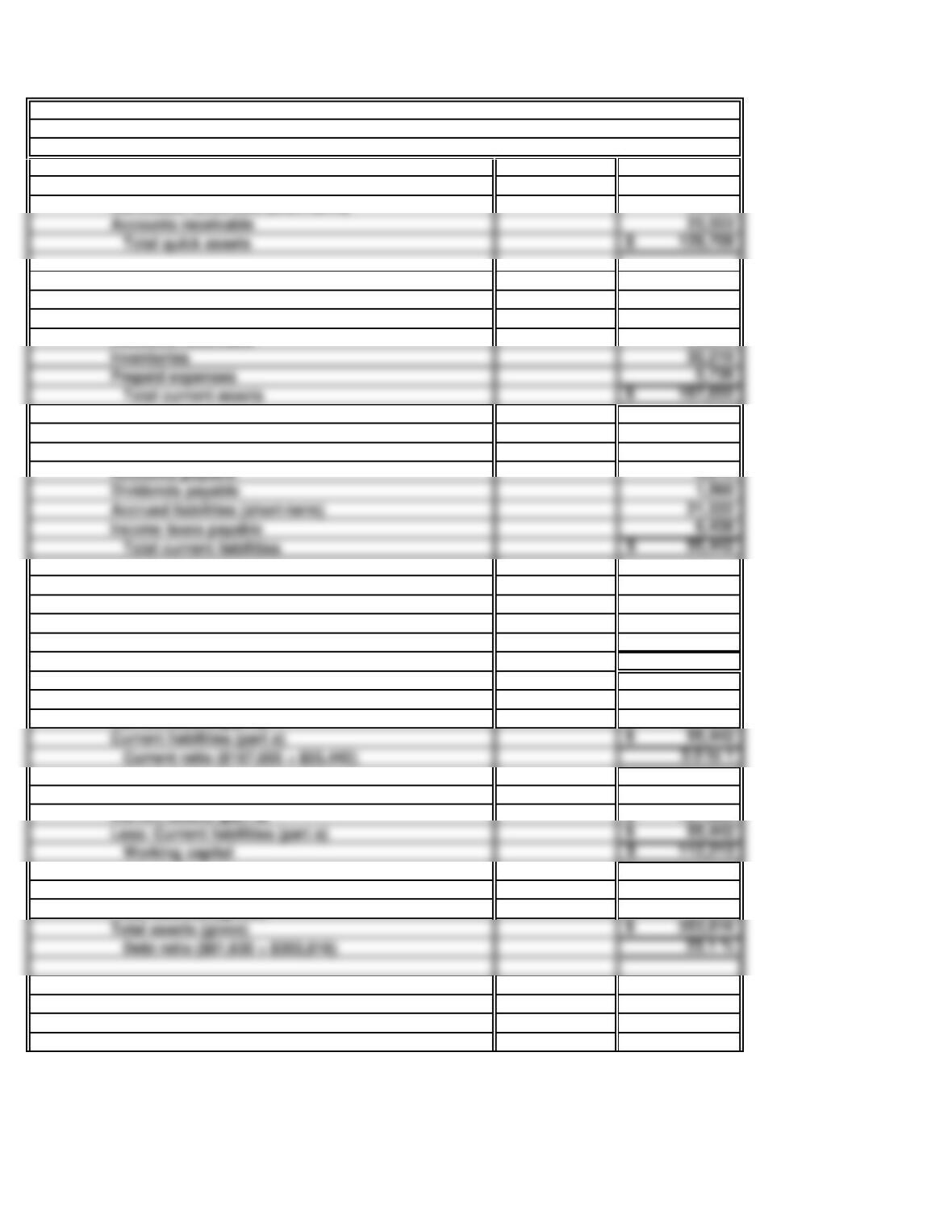

a. Current assets:

(

Cash 1,200$

Receivables 1,734

b. (1) Current ratio:

(

(

Current assets (part a) 11,092$

Current liabilities 12,971

Current ratio ($11,092 ÷ $12,971) 0.86 to 1

(2) Quick ratio:

(

(

Quick assets (part a) 2,934$

(3) Working capital:

(

(

Current assets (part a) 11,092$

PROBLEM 14.4A

(

Cash 1,200$

Receivables 1,734

d.

e.

PROBLEM 14.4A

THE KROGER COMPANY, INC. (concluded)

Due to characteristics of the industry, supermarkets tend to have smaller amounts of current

assets and quick assets than other types of merchandising companies. An inventory of food

In evaluating Kroger’s liquidity, it would be useful to review the company’s financial position

35 Minutes, Medium

(Dollars in

Thousands)

a. (1) Quick assets:

(

(

Cash 50,230$

Marketable securities (short-term) 55,926

(2) Current assets:

(

(

Cash 50,230$

Marketable securities (short-term) 55,926

Accounts receivable 23,553

(3) Current liabilities:

(

(

Notes payable to banks (due within one year) 20,000$

Accounts payable 5,912

Dividends payable 1,560

Accrued liabilities (short-term) 21,532

b. (1) Quick ratio:

(

Quick assets (part a) 129,709$

Current liabilities 55,442

Quick ratio: ($129,709 ÷ $55,442) 2.3 to 1

(2) Current ratio:

Current assets (part a) 167,655$

(3) Working capital:

(

(

Current assets (part a) 167,655$

(4) Debt ratio:

Total liabilities (given) 81,630$

PROBLEM 14.5A

SWEET TOOTH, INC.

Accounts receivable 23,553

c. (1)

(2)

(3)

From the viewpoint of stockholders, Sweet Tooth, Inc. appears overly liquid. Current

PROBLEM 14.5A

SWEET TOOTH, INC. (concluded)

From the viewpoint of short-term creditors, Sweet Tooth appears highly liquid. Its quick

Long-term creditors should feel relatively secure. Not only is the company highly liquid,

45 Minutes, Strong

b. (1) Current ratio:

(

(

Current assets:

Cash 30,000$

Accounts receivable 150,000

Inventory 200,000

(2) Quick ratio:

(

(

Quick assets:

Cash 30,000$

Accounts receivable 150,000

Total quick assets 180,000$

Current liabilities 150,000$

Quick ratio ($180,000 ÷ $150,000) 1.2 to 1

(3) Working capital:

(

(

Current assets [part b (1)] 380,000$

Less: Current liabilities 150,000

Working capital 230,000$

(4) Debt ratio:

(

Total liabilities

Total assets 1,000,000$

Total liabilities 700,000$

Total assets 1,000,000$

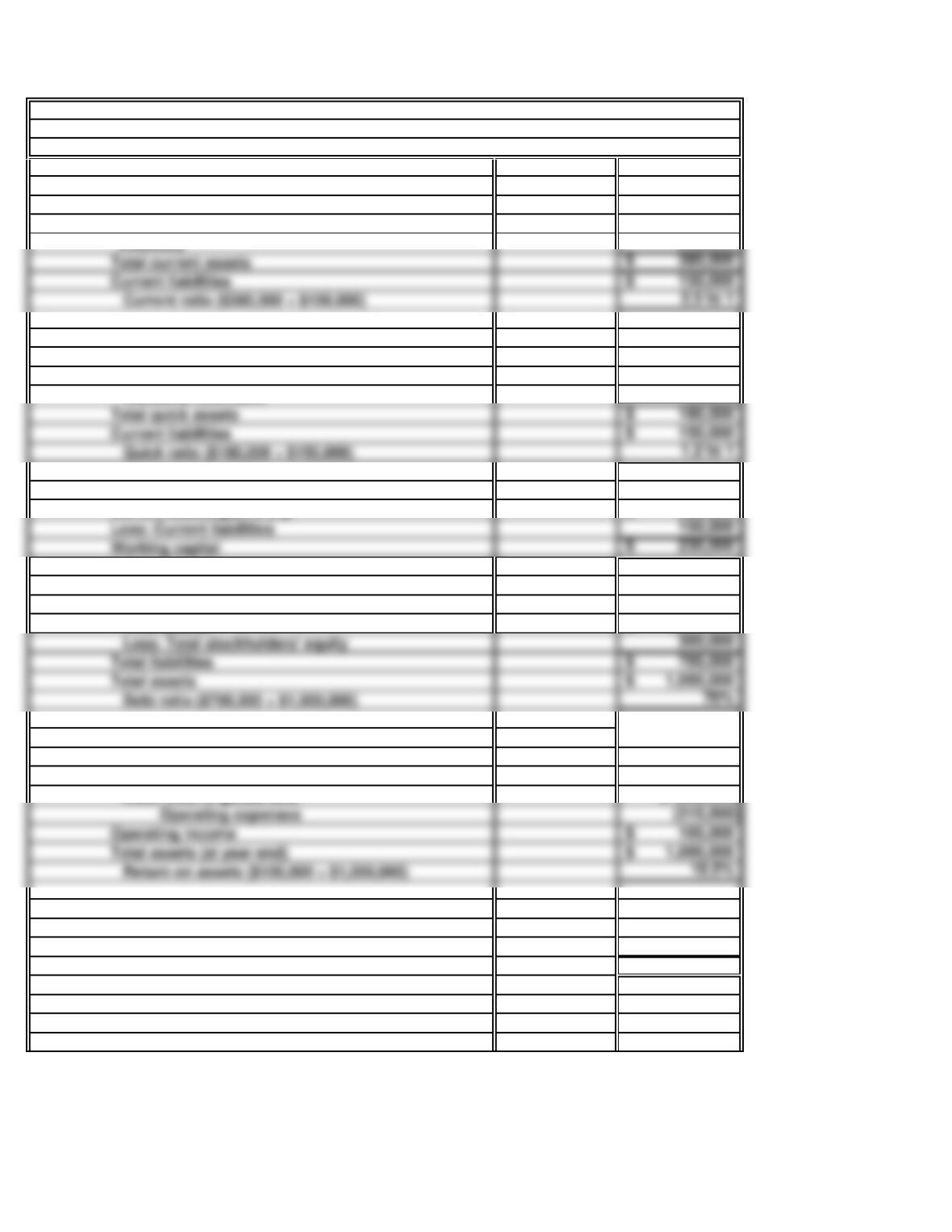

d. (1) Return on assets:

Operating income:

Net sales 1,500,000$

Less: Cost of goods sold (1,080,000)

Operating income 105,000$

(

(

Total assets (at year-end) 1,000,000$

(2) Return on equity:

Net income 15,000$

Total stockholders’ equity (at year-end) 300,000$

Return on equity ($15,000 ÷ $300,000) 5%

PROBLEM 14.6A

DICKSON, INC

Parts a, c, e, and f appear on the following page.

Total current assets 380,000$

Current liabilities 150,000$

Current ratio ($380,000 ÷ $150,000) 2.5 to 1

a.

c.

f. (1)

(2)

PROBLEM 14.6A

DICKSON, INC. (concluded)

Long-term creditors do not appear to have a high margin of safety. The debt ratio of

If the current year is typical, it is doubtful that Dickson, Inc. can continue its $20,000

annual dividend. In the current year, investing activities consumed more than the net

In the statement of cash flows, amounts are reported on a cash basis, whereas in the income

By traditional measures, the company’s current ratio (2.5 to 1) and quick ratio (1.2 to 1)

e.

25 Minutes, Medium

($ in Millions)

a. Current ratio:

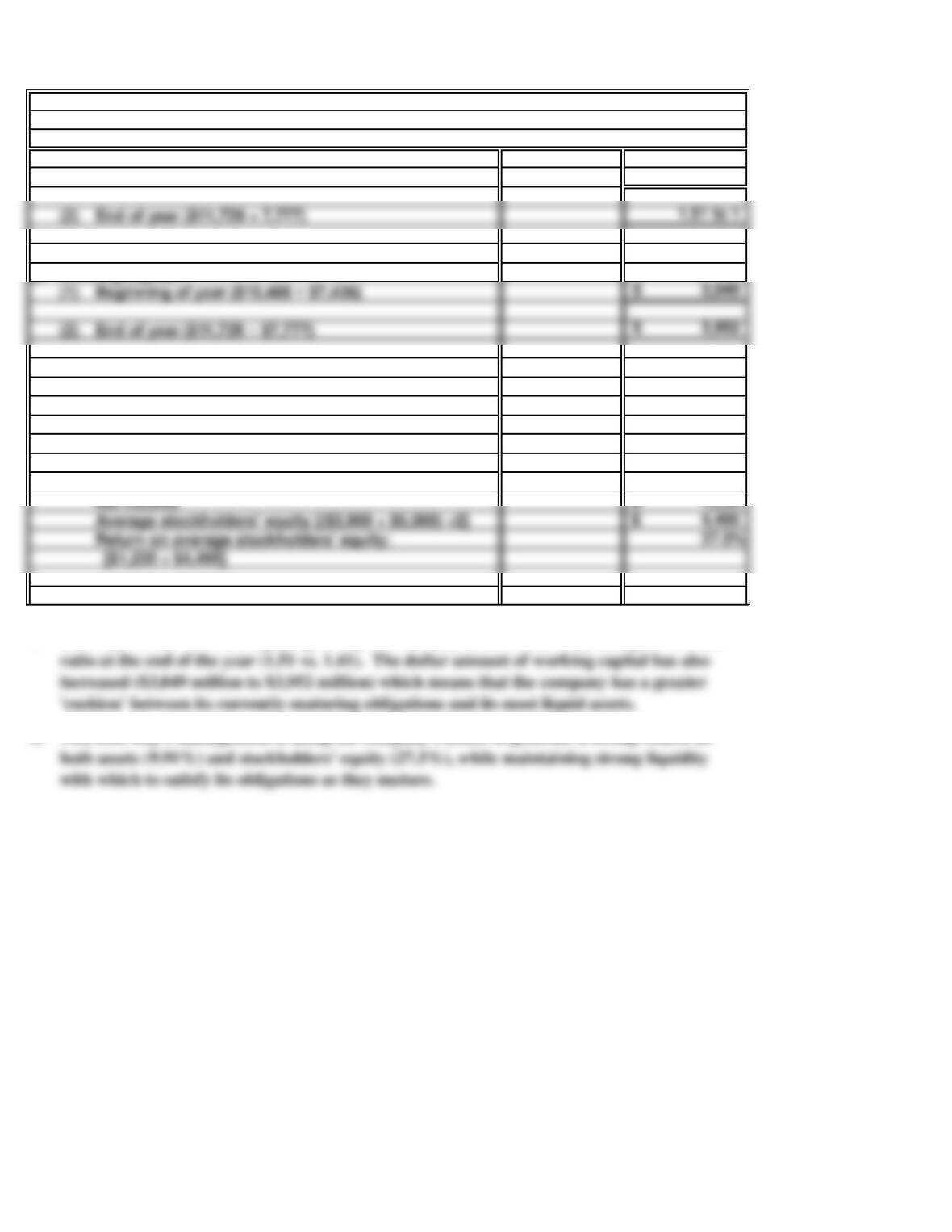

(1) Beginning of year ($10,485 ÷ $7,436) 1.41 to 1

b. Working capital:

d. (1) Return on average total assets:

Operating income 1,450$

Average total assets [($14,013 + $15,256) ÷ 2] 14,635$

Return on average total assets [$1,450 ÷ $14,635] 9.91%

(2) Return on average stockholders’ equity:

Net income 1,235$

Average stockholders’ equity [($3,989 + $5,000) ÷2] 4,495$

Return on average stockholders’ equity: 27.5%

c.

e.

Best Buy’s short-term debt-paying ability has increased, as evidenced by its higher current

Yes, Best Buy’s management is using the company’s assets to generate a strong return on

PROBLEM 14.7A

BEST BUY

(2) End of year ($11,729 ÷ 7,777) 1.51 to 1

25 Minutes, Medium

a. (1) Inventory turnover:

(3) Total operating expenses:

Sales 2,750,000$

Less: Cost of goods sold 1,781,000

Gross profit 969,000$

(6) Return on average assets:

Operating income:

Sales 2,750,000$

Cost of goods sold 1,781,000

Gross profit 969,000$

PROBLEM 14.8A

HARRISON ELECTRONICS, INC.

b.

PROBLEM 14.8A

HARRISON ELECTRONICS, INC. (concluded)

Obtaining the loan will be desirable to stockholders because the return on average assets

35 Minutes, Medium

a.

Another Imports

World Inc.

(2) Current ratio:

($53,000 + $75,000 + $84,000) ÷ $105,000 2 to 1

($22,000 + $70,000 + $160,000) ÷ $100,000 2.5 to 1

($53,000 + $75,000) ÷ $105,000 1.2 to 1

($22,000 + $70,000) ÷ $100,000 .9 to 1

(4) Number of times inventory turned over during the year:

($504,000 cost of goods sold ÷ $84,000 inventory) 6 times

($480,000 cost of goods sold ÷ $160,000 inventory) 3 times

Average number of days required to turn over inventory:

(365 ÷ 6 times) 61 days

(365 ÷ 3 times) 122 days

(5) Number of times accounts receivable turned over:

($675,000 credit sales ÷ $75,000 accounts receivable) 9 times

Average number of days required to collect accounts rec.:

(365 ÷ 9 times) 41 days

(365 ÷ 8 times) 46 days

(6) Operating cycle:

(61 days + 41 days) 102 days

PROBLEM 14.9A

ANOTHER WORLD AND

IMPORTS, INC.

(1) Working capital:

($53,000 + $75,000 + $84,000 – $105,000) 107,000$

b.

PROBLEM 14.9A

ANOTHER WORLD AND IMPORTS, INC. (concluded)

Although Imports, Inc., has a larger dollar amount of working capital and a higher current

ratio, Another World has the higher-quality working capital. The quality of working capital

is determined by the nature of the current assets comprising the working capital and the

20 Minutes, Easy

a. Common size income statement:

Décor Industry

Inc. Average

Sales (net) 100% 100%

Cost of goods sold 61 69

b.

SOLUTIONS TO PROBLEM SET B

Decor, Inc.’s operating results are significantly better than the average performance within

the industry. As a percentage of sales revenue, operating income is over two times the

industry average and net income almost three times the average for the industry.

PROBLEM 14.1B

DECOR, INC.

25 Minutes, Medium

2018 2017

a. Net sales: ($150,000 ÷ .08) 1,875,000$

($170,000 ÷ .10) 1,700,000$

b. Cost of goods sold in dollars:

($1,875,000 net sales – $720,000 gross profit) 1,155,000$

c. Operating expenses in dollars:

($720,000 gross profit – $200,000 income before tax) 520,000$

($800,000 gross profit – $220,000 income before tax) 580,000$

($520,000 ÷ $1,875,000) 27.7%

d.

2018 2017

Net sales 1,875,000$ 1,700,000$

For the Year Ended December 31, 2018 and December 31, 2017

PROBLEM 14.2B

FREE TIME, INC.

SLOW TIME, INC.

Condensed Comparative Income Statement

($1,155,000 ÷ $1,875,000) 61.6%

e.

PROBLEM 14.2B

Favorable and unfavorable trends:

Favorable trends. One favorable trend is the $175,000 increase in net sales, which represented

an increase of about 10% over the prior year. A second favorable trend is the decrease in

FREE TIME, INC. (concluded)

15 Minutes, Easy

a. Current assets:

Cash 61,000$

Marketable securities 175,000

The company appears to be in a strong position as to short-run debt-paying ability. It has

almost three dollars of current assets for each dollar of current liabilities. Even if some losses

PROBLEM 14.3B

GLAVEN, INC.

Accounts receivable 217,000

Income taxes payable 14,400