Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 14 - Decision Making: Relevant Costs and Benefits

14-21

Remaining machine hours .................................................................................

30,000

PROBLEM 14-46 (CONTINUED)

2. If the company’s management team is able to reduce the direct material cost per

food processor to $18 ($15 less than previously assumed), then the cost savings

from manufacturing a food processor are $33 per unit ($18 savings computed in

requirement (1) plus $15 reduction in material cost):

Blender

Food

Processor

New unit cost savings if manufactured .........................................

$12.00

$33.00

PROBLEM 14-47 (25 MINUTES)

1.

Incremental unit cost if purchased:

Purchase price .........................................................................................

$ 45,000

Chapter 14 - Decision Making: Relevant Costs and Benefits

14-22

2.

Increase in monthly cost of acquiring part RM67 if purchased

Chapter 14 - Decision Making: Relevant Costs and Benefits

14-23

PROBLEM 14-47 (CONTINUED)

3.

Contribution forgone by not manufacturing alternative product .............

$156,000

PROBLEM 14-48 (20 MINUTES)

The analysis prepared by the engineering, manufacturing, and accounting departments of

Cincinnati Flow Technology (CFT) was not correct. However, their recommendation was

correct, provided that potential labor-cost improvements are ignored. An incremental cost

analysis similar to the following table should have been prepared to determine whether the

Chapter 14 - Decision Making: Relevant Costs and Benefits

14-24

PROBLEM 14-49 (25 MINUTES)

1. Per-unit contribution margins:

Standard

Enhanced

Selling price…………………………………..

$375.00

$495.00

2. The following costs are not relevant to the decision:

• Development costs—sunk

3. Martinez, Inc. expects to sell 10,000 Standard units (40,000 units x 25%) or 8,000

4. The quantitative difference between the profitability of Standard and Enhanced is

relatively small, which may prompt the firm to look at other factors before a final

decision is made. These factors include:

Chapter 14 - Decision Making: Relevant Costs and Benefits

14-25

PROBLEM 14-50 (20 MINUTES)

1. When there is no limit on production capacity the Pro model should be manufactured

since it has the highest contribution margin per unit.

Basic

Deluxe

Pro

2. When labor is in short supply the Basic model should be manufactured, since it has

the highest contribution margin per direct-labor hour.

Basic

Model

Deluxe

Model

Pro

Model

Chapter 14 - Decision Making: Relevant Costs and Benefits

14-26

PROBLEM 14-51 (25 MINUTES)

1. Yes, the order should be accepted because it generates a profit of $68,100 for the

firm. Note: The fixed administrative cost is irrelevant to the decision, because this

cost will be incurred regardless of whether Mercury accepts or rejects the order.

Selling price…………………………………………………

$31.50

Less: Direct material ($16.40 - $4.20)…………………...

$12.20

Direct labor…………………………………………..

4.50

2. No, Mercury lacks adequate machine capacity to manufacture the entire order.

Planned machine hours (5,000 hours x 3 months)……

15,000

3. Options include the following:

• Sacrificing some current business in the hope that a long-term relationship with

14-27

PROBLEM 14-52 (40 MINUTES)

1. The costs that will be relevant in Peters’ analysis of the special order being

considered by Treasure Island Beach Equipment, Inc. are those expected future

costs that are applicable to a particular decision (the costs that will differ between

2. Management should accept the offer. Although the combined average unit cost of

Chapter 14 - Decision Making: Relevant Costs and Benefits

14-28

PROBLEM 14-52 (CONTINUED)

Current Monthly

Production

Special

Order

Combined

Production

Units produced ................................................................

1,875

625

2,500

Sales ................................................................

$ 984,375

a

$187,500

b

$1,171,875

Variable costs: ................................................................

a$525 1,875 units = $984,375

b$300 625 units = $187,500

14-29

PROBLEM 14-52 (CONTINUED)

3. Other considerations that Samantha Peters should include in her analysis of the

special order include the following:

4. Samantha Peters could try to resolve the ethical conflict arising out of the

controller’s insistence that the company avoid competitive bidding by taking the

following steps:

• She should follow the company’s established policies on such matters.

Chapter 14 - Decision Making: Relevant Costs and Benefits

14-30

PROBLEM 14-53 (40 MINUTES)

1. a. An analysis of the relevant costs that shows whether the Midwest Division of

Palisades Corporation should make JY-65 or purchase it from Marley Company is

as follows:

Amount

Per Unit

Total for

32,000

Units

Cost to purchase JY-65 from Marley:

Bid price from Marley .............................................................

$8.65

276,800

Chapter 14 - Decision Making: Relevant Costs and Benefits

14-31

PROBLEM 14-53 (CONTINUED)

2. The qualitative factors that the Midwest Division and Palisades Corporation should

consider before agreeing to purchase JY-65 from Marley Company include the

following:

3. Lynn Hardt would consider the request of John Porter to be unethical for the

following reasons, which are based on the Standards of Ethical Conduct for

Management Accountants.

Competence

Chapter 14 - Decision Making: Relevant Costs and Benefits

14-32

PROBLEM 14-53 (CONTINUED)

• Refrain from engaging in or supporting any activity that would discredit the

profession. Falsifying the analysis would discredit Hardt and the profession.

PROBLEM 14-54 (40 MINUTES)

1. The incremental cost of producing one unit of component B81 is computed as

follows:

Direct material ..............................................................................................

$11.25

14-33

PROBLEM 14-54 (CONTINUED)

2.

T79

B81

Purchase price quoted ...............................................................................

$33.75

$40.50

Direct material .............................................................................................

$ 6.75

$11.25

Required quantity of component B81 ................................................

11,000 units

3.

Variable cost per unit of component B81 ..................................................

$31.50

Traceable, avoidable, fixed cost per unit of

14-34

PROBLEM 14-55 (45 MINUTES)

RNA-1 is converted into Fastkil. RNA-2 can be sold as is or converted into two new

products.

a. Management’s analysis is incorrect because it incorporates allocated portions of

the joint-processing costs of VDB. The weekly cost of VDB ($393,600) will be

b.

Revenue from further processing of RNA-2:

DMZ-3 (400,000 $92/100) ................................................................

$368,000

14-35

PROBLEM 14-56 (30 MINUTES)

1. Costs to be avoided by purchasing (conventional analysis):

Direct material ..............................................................................................

$288,000

2. Costs to be avoided by purchasing (ABC analysis):

Direct material ..............................................................................................

$288,000

Direct labor ...................................................................................................

192,000

Overhead:

Product development ..........................................

$600a 10b

6,000

14-36

PROBLEM 14-56 (CONTINUED)

3. Make-or-buy analysis using ABC data:

Cost savings if canisters are purchased

(ABC analysis) ...........................................................................................

$810,750

4. The relevant costing approach remains valid when ABC data are used. The objective

is to determine what costs will be avoided if the canisters are purchased. The ABC

14-37

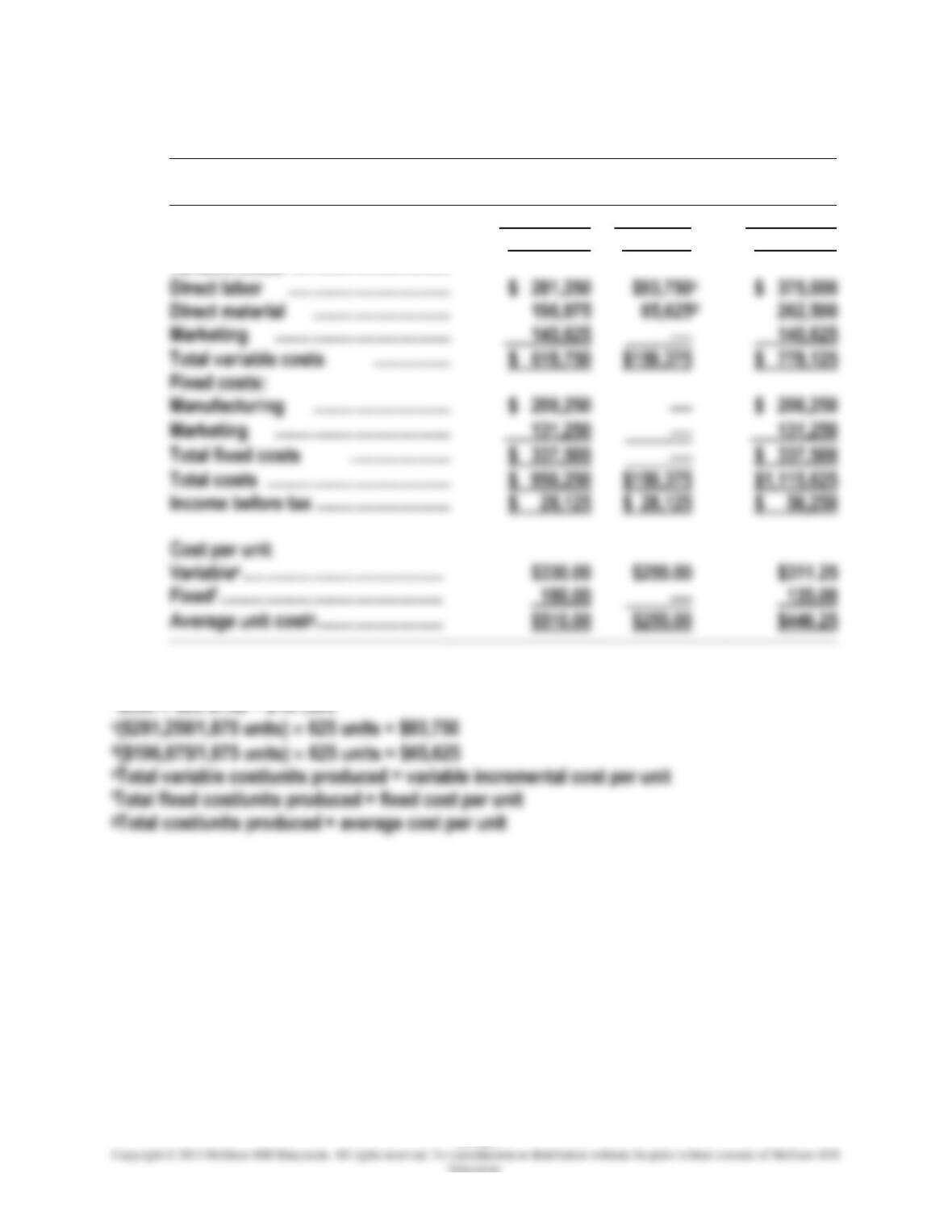

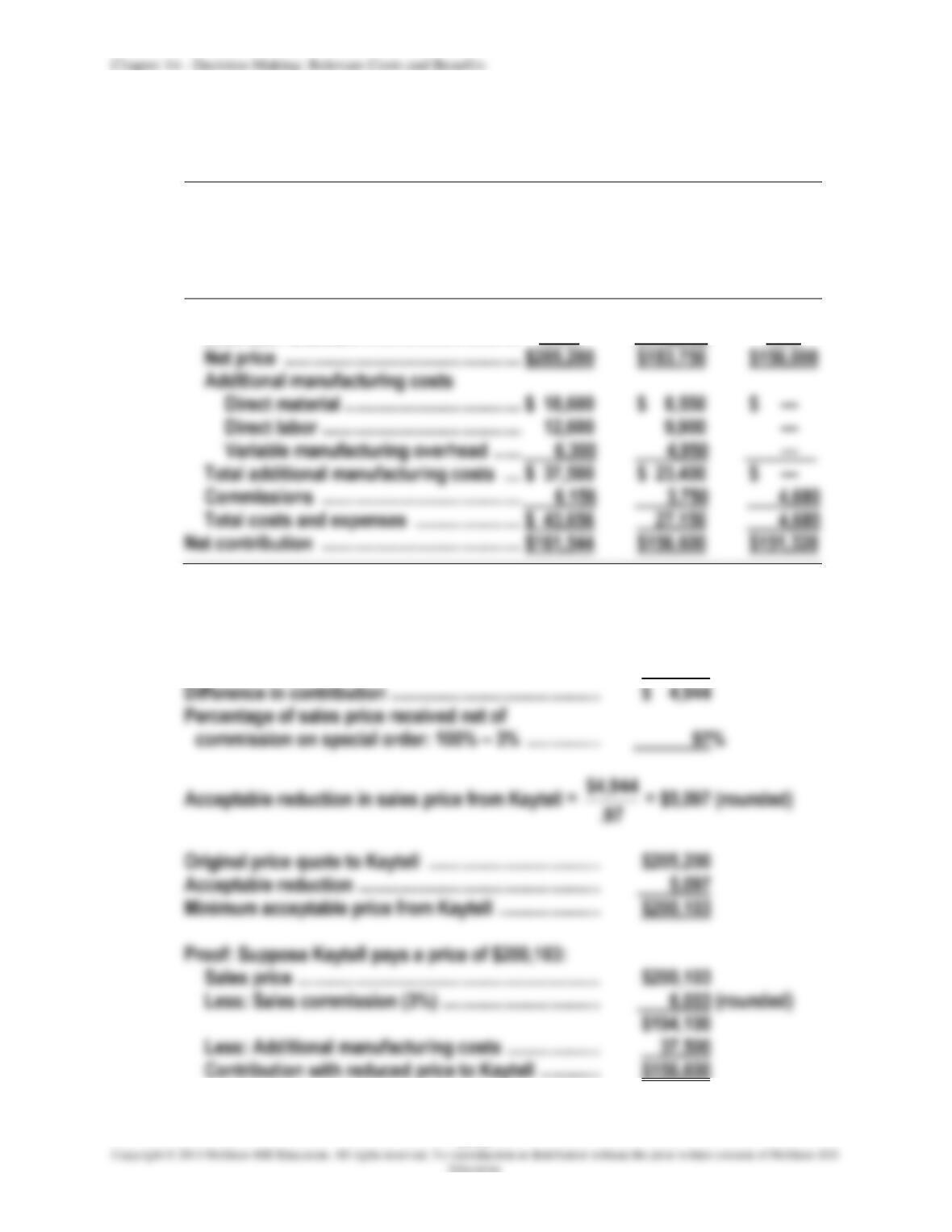

PROBLEM 14-57 (45 MINUTES)

1.

Sell to

Kaytell

as

Special

Order

Convert

to

Standard

Model

Sell as

Special

Order

as Is

Sales price ................................................................

$205,200

$187,500

$156,000

Less cash discount .........................................................

-—

3,750

—

2.

Contribution from sale to Kaytell .......................................

$161,544

Contribution from next best alternative:

sell as standard model .....................................................

156,600

14-38

PROBLEM 14-57 (CONTINUED)

Therefore, at a price of $200,103 to Kaytell, Excalibur’s management would be

3. Fixed manufacturing overhead should have no influence on the sales price quoted

by Excalibur, Inc. for special orders. Management should accept special orders

whenever the firm is operating substantially below capacity, including below the