CHAPTER 14

SOLUTIONS TO PROBLEMS: SET B

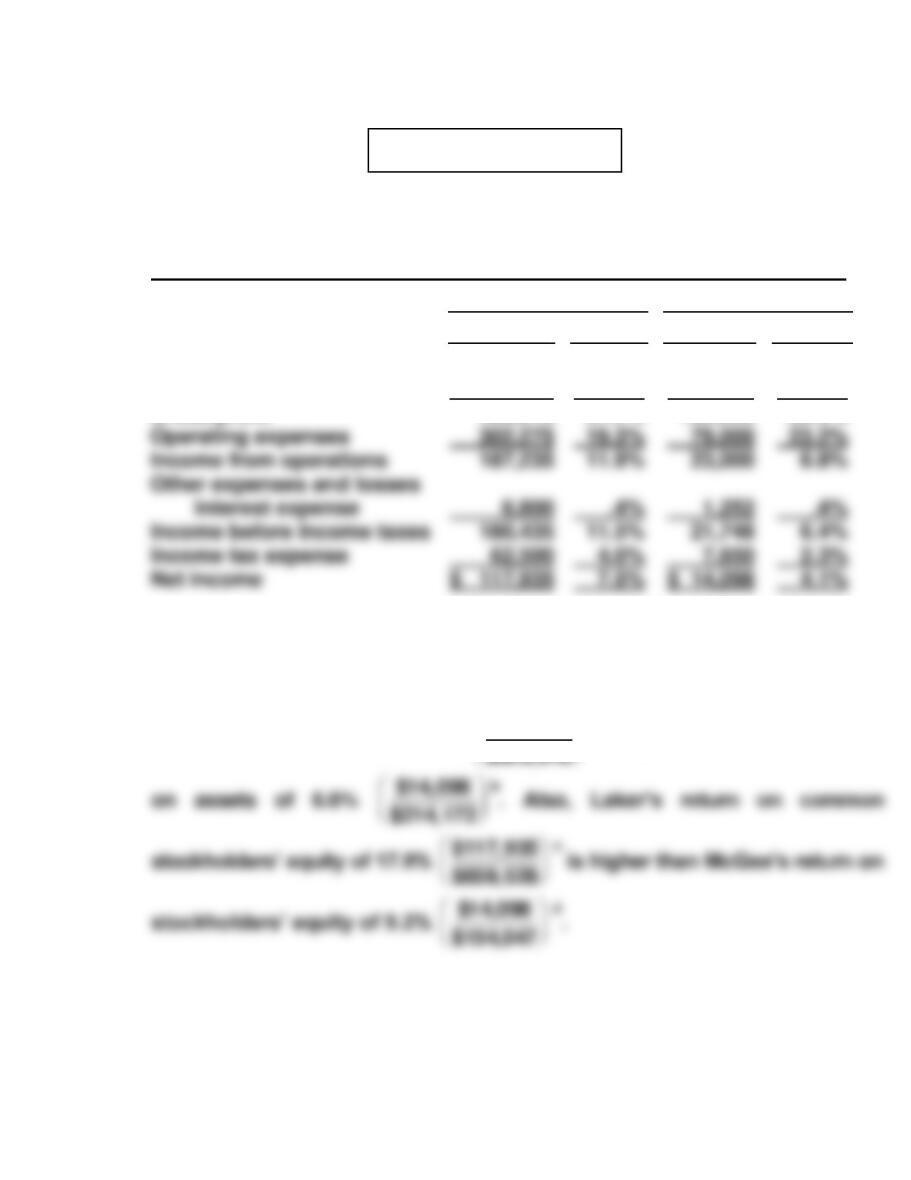

PROBLEM 14-1B

(a) Condensed Income Statement

For the Year Ended December 31, 2017

Laker Company

McGee Company

Dollars

Percent

Dollars

Percent

Net sales

Cost of goods sold

Gross profit

$1,570,000

1,080,490

489,510

100.0%

68.8%

31.2%

$340,000

238,000

102,000

100.0%

70.0%

30.0%

(b) Laker Company appears to be more profitable. It has higher relative

gross profit, income from operations, income before taxes, and net income.

Laker’s return on assets of 14.2%

$117,935

$117,935

a is higher than McGee’s return

PROBLEM 14-1B (Continued)

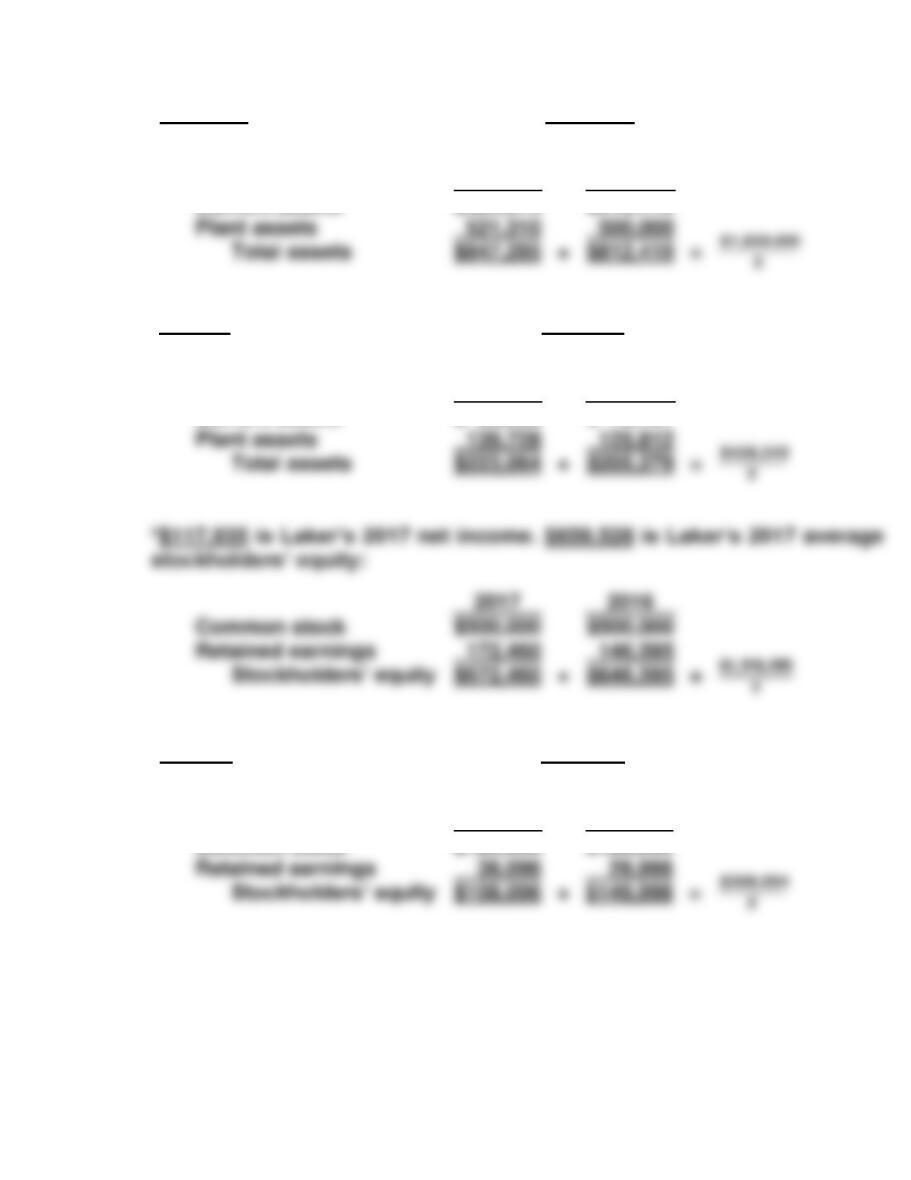

a$117,935 is Laker’s 2017 net income. $829,848 is Laker’s 2017 average

assets:

2017

2016

Current assets

$325,975

$312,410

b$14,098 is McGee’s 2017 net income. $214,172 is McGee’s 2017 average

assets:

2017

2016

2017

2016

Current assets

$ 83,336

$ 79,467

d$14,098 is McGee’s 2017 net income. $154,047 is McGee’s 2017 average

stockholders’ equity:

2017

2016

PROBLEM 14-2B

(a) Earnings per share =

$210,000

62,500

= $3.36.

(c) Return on assets =

$210,000

$852,800+$970,200

2

=

$210,000

$911,500

= 23.0%.

(f) Accounts receivable turnover =

$1,828,500

($102,800+ $122,800 )

2

$210,000

$465,400+$556,700

2

$210,000

$511,050

PROBLEM 14-2B (Continued)

(g) Inventory turnover =

$1,010,500

$115,500 + $118,000

2

=

$1,010,500

$116,750

= 8.7 times.

PROBLEM 14-3B

(a)

2016

2017

(1)

Profit margin.

(2)

Asset turnover.

$650,000

$533,000+ $600,000

2

= 1.1 times

$700,000

$600,000+ $640,000

2

= 1.1 times

(3)

Earnings per share.

(5)

Payout ratio.

$18,000

$30,000

*

= 60.0%

*($113,000 + $30,000 – $125,000)

$25,000

$45,000

**

= 55.6%

**($125,000 + $45,000 – $145,000)

(6)

PROBLEM 14-3B (Continued)

(b) The underlying profitability of the corporation appears to have improved. For

example, profit margin and earnings per share have both increased. In

PROBLEM 14-4B

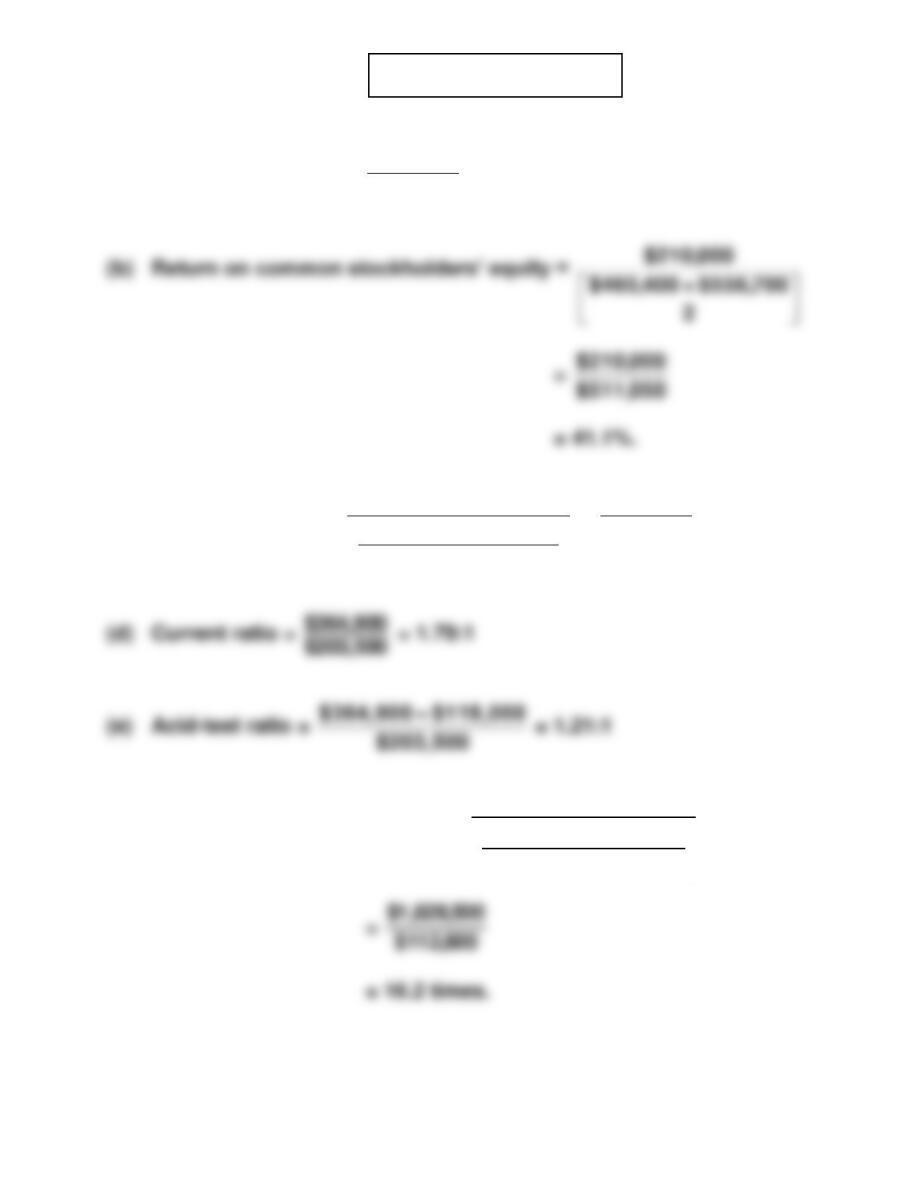

(a) LIQUIDITY

2016

2017

Change

Current

$65,000 + $40,000 + $90,000 + $125,000 + $20,000 = 1.9:1

$100,000 + $42,000 + $40,000

$364,000 = 2.0:1

$185,000

Increase

$209,000 = 1.1:1

$185,000

Inventory

turnover

$570,000 = 4.7 times

$122,500*

Increase

*($120,000 + $125,000) ÷ 2 **($125,000 + $130,000) ÷ 2

An overall increase in short-term liquidity has occurred.

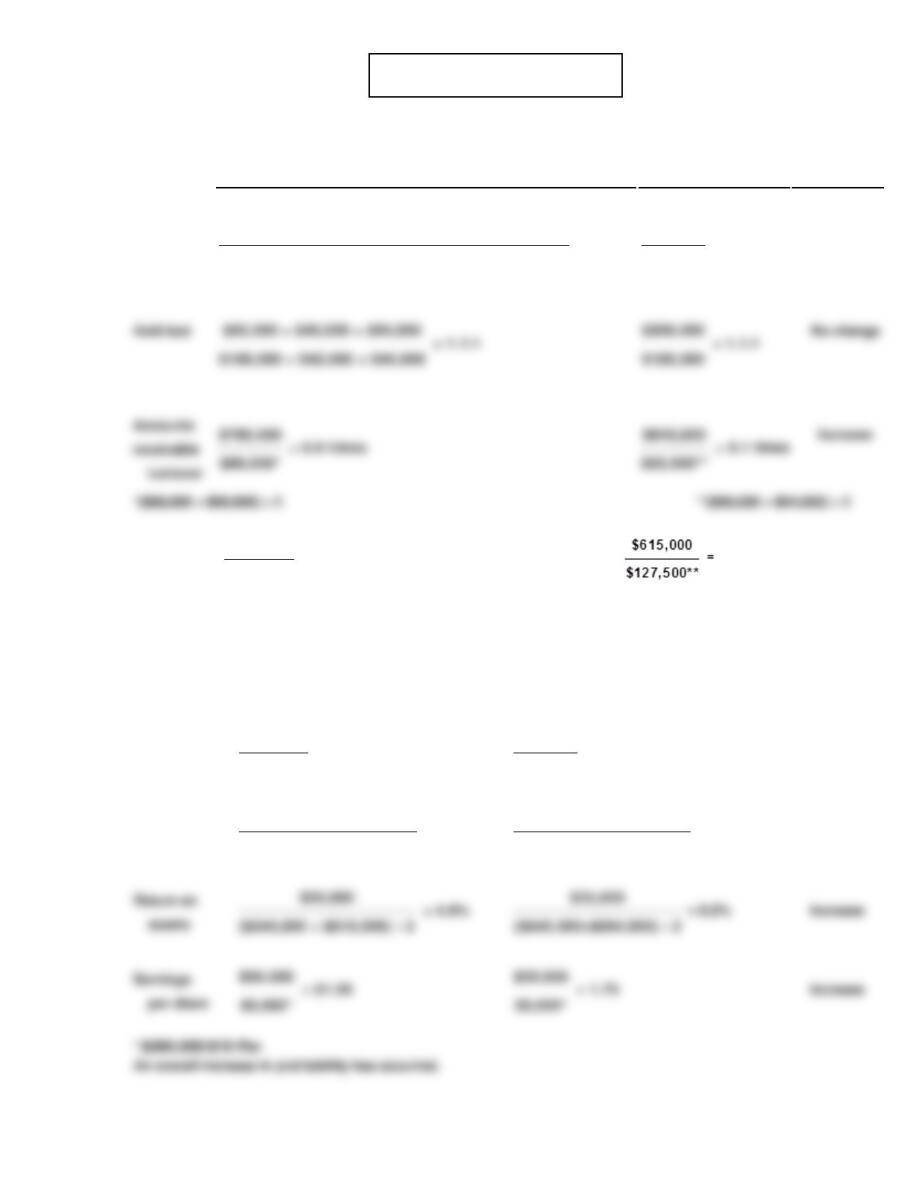

PROFITABILITY

Profit

margin

$30,000 = 3.8%

$780,000*

$35,000 = 4.2%

$840,000

Increase

Asset

turnover

$780,000 = 1.2 times

($645,000 + $615,000) 2

$840,000 = 1.3 times

($645,000 + $694,000) 2

Increase

4. 8 times

assets

Increase

Earnings

per share

Increase

PROBLEM 14-4B (Continued)

(b)

2017

2018

Change

1.

Return on

common

stockholders’

equity

$35,000 = 10.4%

$336,000 (a)

$40,000 = 8.5%

$469,000 (b)

Decrease

PROBLEM 14-5B

(a)

Ratio

Target

Wal-Mart

(All Dollars Are in Millions)

Times interest earned

5.1 ($4,402g ÷ $866)

11.5 ($21,502h÷ $1,863)

(1)

(2)

(3)

(4)

Current

Accounts receivable turnover

Average collection

period

Inventory turnover

1.7:1 ($17,488 ÷ $10,512)

7.8 ($62,884 ÷ $8,069)

46.8 (365 ÷ 7.8)

7.1 ($44,157 ÷ $6,243)

.8:1 ($47,585 ÷ $58,454)

115.3 ($374,526 ÷ $3,247)

3.2 (365 ÷ 115.3)

8.3 ($286,515 ÷ $34,433)

(b) The comparison of the two companies shows the following:

Liquidity—Target’s current ratio of 1.7:1 is significantly better than Wal-

Mart’s .8:1. However, Wal-Mart has a better inventory turnover ratio than

Target and its account receivable turnover is substantially better than

Target’s.

PROBLEM 14-6B

(a) Current ratio =

$235,000

$145,000

= 1.6:1.

(d) Inventory turnover =

$410,000

$86,000 +$69,000

2

= 5.3 times.

(e) Profit margin ratio =

$54,500

$640,000

= 8.5%.

(h) Return on common stockholders’ equity =

$54,500

$403,000+$350,000

2

= 14.5%.

PROBLEM 14-6B (Continued)

(i) Earnings per share =

$54,500

30,000 (1)

= $1.82.

(1) $150,000 ÷ $5.00

(l) Debt to assets =

$235,000

$638,000

= 36.8%.

PROBLEM 14-7B

Accounts receivable turnover = 10 =

$11,000,000

Average receivables

Average accounts receivable =

$11,000,000

10

= $1,100,000

Profit margin = 15% = .15 =

Netincome

$11,000,000

Net income = $11,000,000 X .15 = $1,650,000

Income before income taxes = $1,650,000 + $580,000 = $2,230,000

Return on assets = 24% = .24 =

$1,650,000

Average assets

= $6,875,000

= $1,100,000

PROBLEM 14-7B (Continued)

Current ratio = 2.5 =

$2,200,000

Currentliabilities

Current liabilities = $2,200,000 ÷ 2.5 = $880,000

Long-term notes payable = $3,350,000 – $880,000 = $2,470,000

PROBLEM 14-8B

LARAMIE CORPORATION

Statement of Comprehensive Income

For the Year Ended December 31, 2017

Operating revenues

($12,700,000 – $3,000,000) …………………… $9,700,000

Operating expenses

($8,700,000 – $4,000,000) …………………….. 4,700,000

PROBLEM 14-9B

STARSHIP CORPORATION

Statement of Comprehensive Income

For the Year Ended December 31, 2017

Net sales …………………………………………………… $1,700,000

Cost of goods sold …………………………………….. 900,000

Gross profit……………………………………………….. 800,000

Selling and administrative expenses

($100,000 + $200,000) …………………………….. 300,000