443

CHAPTER 14

DECENTRALIZED OPERATIONS

CLASS DISCUSSION QUESTIONS

1. In a cost center, the department manager is

responsible for and has authority over costs

only. In a profit center, the manager’s re-

sponsibility and authority extend to costs

and revenues.

3. The difference in budget performance re-

ports prepared for department supervisors

and plant managers is the amount of detail

provided to each. The departmental supervi-

sors require considerable detail to control

costs. The report for the plant managers

would contain more summarized cost data

for the various departments.

Database administration: Number of reports.

6. The major shortcoming of using operating

income as a measure of investment center

performance is that it ignores the amount of

investment committed to each center. Since

7. Revenues and expenses are considered in

computing the return on investment because

they directly impact the determination of

operating income. Invested assets are con-

sidered in computing the return on invest-

is the lowest. In this situation, the division

would be considered the least profitable per

dollar invested in the division.

9. By dividing operating income by the amount

of invested assets, each division is placed on

a comparable basis of operating income per

dollar invested.

10. North Division. The North Division will return

444

E14–1

a. (a) $148,975 (g) $758,875

(b) $137,500 (h) $750,000

(c) $11,475 (i) $8,875

Schedules of supporting calculations (answers in italics; the solution requires

working from the department level, up to the plant level, then to the vice president

of production level):

EZ BREEZY COMPANY

Budget Performance Report—Vice President, Production

For the Month Ended April 30

EZ BREEZY COMPANY

Budget Performance Report—Plant Manager, Chula Vista Plant

For the Month Ended April 30

Department Actual Budget Over Budget (Under) Budget

Condenser Assembly $148,975 (a) $137,500 (b) $11,475 (c)

445

E14–1, Concluded

EZ BREEZY COMPANY

Budget Performance Report—Supervisor, Condenser Assembly

For the Month Ended April 30

Cost Actual Budget Over Budget (Under) Budget

Factory wages $ 47,750 $ 41,000 $ 6,750

b. MEMO

To: Bop Higgins, Vice President of Production

The Chula Vista plant has experienced a budget overrun, while the San Diego

and Anaheim plants have experienced a budget surplus. The budget of the

E14–2

VINTAGE CONSTRUCTION COMPANY

Divisional Income Statements

For the Year Ended October 31, 20Y3

Commercial Residential

Division Division

Sales ……………………………………………………………………….. $ 6,250,000 $ 1,875,000

Cost of goods sold …………………………………………………… (3,800,000) (1,300,000)

Gross profit ……………………………………………………………… $ 2,450,000 $ 575,000

446

E14–3

Expense Activity Bases

a. Accounts Receivable Number of invoices, number of customers

b. Central Purchasing Number of requisitions, number of purchase

orders

E14–4

a. 6 e. 8

447

E14–5

a. Government

Residential Commercial Contract Total

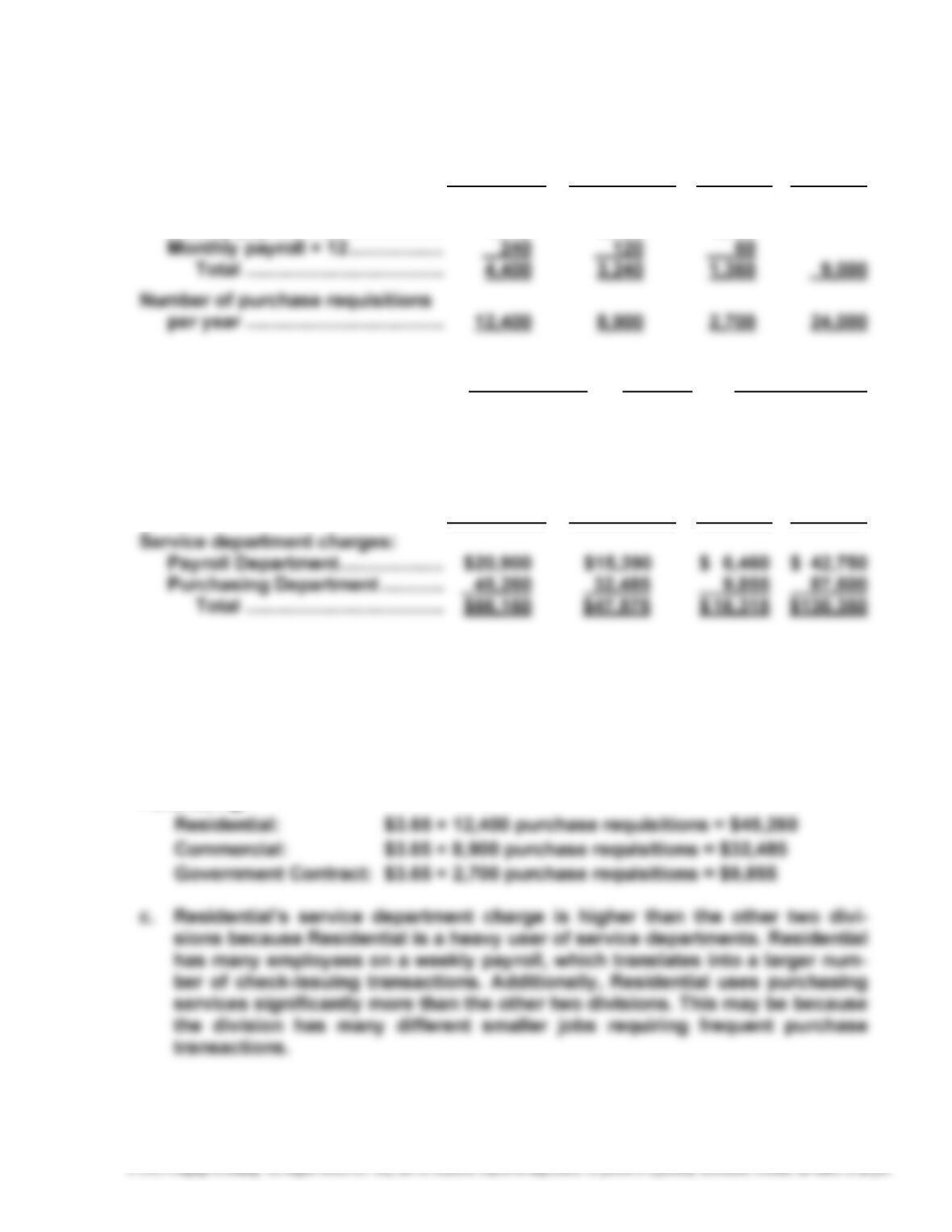

Number of payroll checks:

Weekly payroll × 52 ………………. 4,160 3,120 1,300

b. Service Dept. Activity Charge

Cost ÷ Base = Rate

Service department charge rates:

Payroll Department ……………….. $42,750 ÷ 9,000 = $4.75 per check

Purchasing Department ………… $87,600 ÷ 24,000 = $3.65 per req.

Government

Residential Commercial Contract Total

The service department charges are determined by multiplying the service

department charge rate by the activity base for each division as shown next.

Payroll:

Residential: $4.75 × 4,400 checks = $20,900

Commercial: $4.75 × 3,240 checks = $15,390

Government Contract: $4.75 × 1,360 checks = $6,460

Purchasing:

448

E14–6

a. Help desk: calls 5,000

$135,000 = $27.00 per call

b. February charges to the Electronics sector:

Help desk: (2,000 employees × 60% × 100% × 0.45) × $27.00 per call = $14,580

Network center: [(2,000 employees × 60% × 100%) + 80] × $48.40 per device =

$61,952

449

E14–7

POWER SPORTS COMPANY

Divisional Income Statements

For the Year Ended December 31, 20Y7

Wholesale Division Retail Division

Revenues ………………………………… $24,600,000 $13,750,000

Cost of goods sold ………………….. (14,500,000) (8,000,000)

Gross profit …………………………….. $ 10,100,000 $ 5,750,000

Operating expenses …………………. (1,500,000) (400,000)

Operating income before

450

E14–8

a. The reported operating income does not accurately measure performance

because the service department charges are based on revenues. Revenues are

not associated with the profit center manager’s use of the service department

b.

PANDA AIRLINES INC.

Divisional Income Statements

For the Year Ended April 30, 20Y9

Passenger Division Cargo Division

Revenues ………………………………… $7,500,000 $5,000,000

Operating expenses ………………… (4,500,000) (2,700,000)

Operating income before

service department charges … $3,000,000 $2,300,000

Note 1: Passenger Division, ($500,000 ÷ 800 personnel trained) × 600

Cargo Division, ($500,000 ÷ 800 personnel trained) × 200

Note 2: Passenger Division, ($350,000 ÷ 5,000 flights) × 4,000

Cargo Division, ($350,000 ÷ 5,000 flights) × 1,000

451

E14–9

HUTCHINSON SPORTS CO.

Divisional Income Statements

For the Year Ended November 30, 20Y1

Action Team

Sports Sports

Division Division

Sales ………………………………………………………………… $ 9,250,000 $15,300,000

$(1,375,000) $ (1,775,000)

Operating income before service

department charges …………………………………….. $ 2,525,000 $ 3,925,000

Less service department charges:

Supporting Schedule:

Service Department Charges

Action Team

Sports Sports

Division Division Total

Advertising expense ………………………………… $600,000 $900,000 $1,500,000

Transportation rate per bill of lading ………… $ 18.50 $ 18.50

Number of bills of lading ………………………….. × 7,000 × 10,700

Transportation expense …………………………… $129,500 $197,950 $ 327,450

452

E14–10

a. Retail Division: 20% ($4,000,000 ÷ $20,000,000)

Commercial Division: 17% ($6,375,000 ÷ $37,500,000)

E14–11

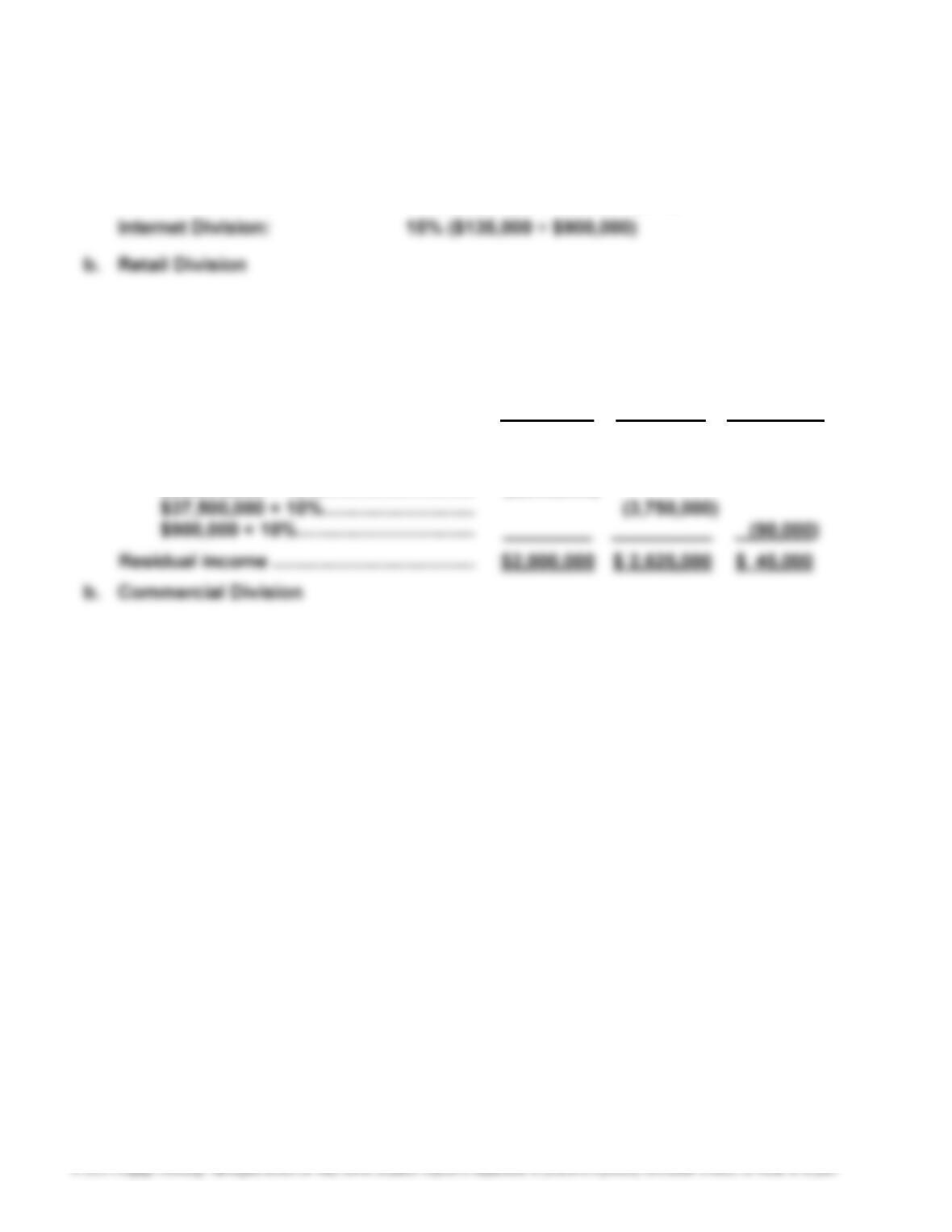

a.

Retail Commercial Internet

Division Division Division

Operating income ………………………………. $4,000,000 $ 6,375,000 $135,000

Minimum amount of operating income:

$20,000,000 × 10% ……………………….. (2,000,000)

453

E14–12

a. 1.50 = 12% ÷ 8%

b. 20% = 16% × 1.25

E14–13

a. Return on Investment = Profit Margin × Investment Turnover

b. The profit margin would increase from 16% to 17%, the investment turnover

would remain unchanged, and the return on investment would increase from

19.2% to 20.4%, as shown next.

Return on Investment = Profit Margin × Investment Turnover

454

E14–14

Parks and Resorts: $3,031

$16,162 × $16,162

$25,510

= 18.8% × 0.63

= 11.8% (rounded)

Studio Entertainment: $1,973

$6,838 × $6,838

$15,334

= 28.9% × 0.45

= 13.0% (rounded)

b. The four sectors are different from each other. Media Networks combines a

good profit margin with an average investment turnover. Media Networks is

sensitive to advertising revenue, while the Studio Entertainment sector is

455

E14–15

a. 16% ($400,000 ÷ $2,500,000)

e. 14% ($840,000 ÷ $6,000,000)

f. 10% ($600,000 ÷ $6,000,000)

g. $1,500,000 ($7,500,000 × 20%)

h. 12% ($900,000 ÷ $7,500,000)

i. $600,000 ($1,500,000 – $900,000)

456

E14–16

a. (a) $1,200,000 ($6,000,000 × 20%)

(b) $7,500,000 ($1,200,000 ÷ 16%)

(f) 16.8% (12% × 1.4) or ($1,512,000 ÷ $9,000,000)

(g) $1,925,000 ($11,000,000 × 17.5%)

(h) 14% ($1,925,000 ÷ $13,750,000)

(i) 1.25 ($13,750,000 ÷ $11,000,000) or (17.5% ÷ 14%)

b. California Division: $450,000 [$1,200,000 – ($7,500,000 × 10%)]

Midwest Division: $612,000 [$1,512,000 – ($9,000,000 × 10%)]

Northwest Division: $825,000 [$1,925,000 – ($11,000,000 × 10%)]

Texas Division: $490,000 [$840,000 – ($3,500,000 × 10%)]

457

E14–17 Appendix

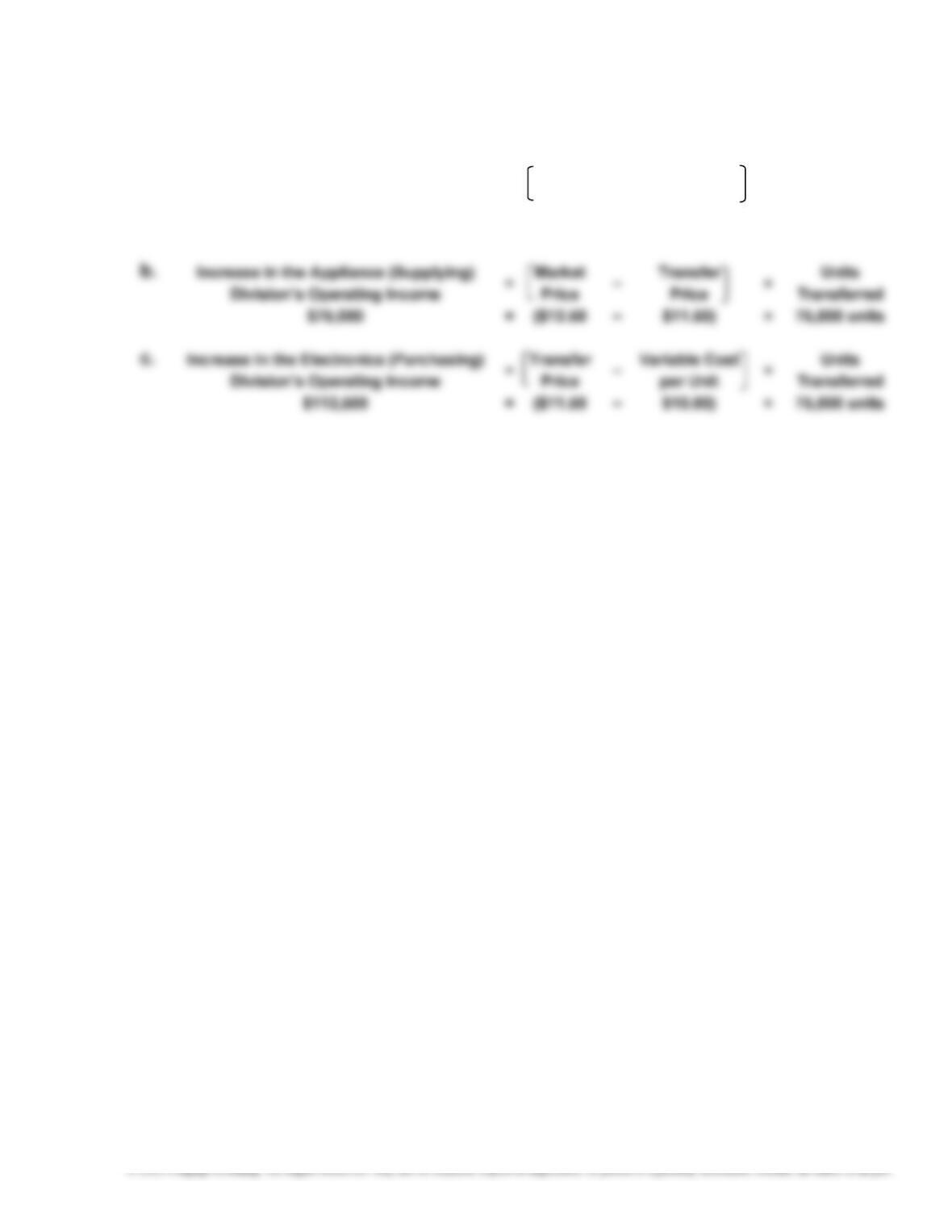

a. Increase in Childs Manufacturing’s

Operatin

g

Income = Market

Price – Variable Cost

per Unit × Units

Transferred

$187,500 = ($12.50 – $10.00) × 75,000 units

g

g

458

E14–18 Appendix

a. Increase in Childs Manufacturing’s

Operatin

g

Income = Market

Price – Variable Cost

per Unit × Units

Transferred

$187,500 = ($12.50 – $10.00) × 75,000 units

g

This is the amount the Appliance Division saves by purchasing from the Electronics Division

at an internal price that is lower than the market price.

c. Increase in the Electronics (Supplying)

Division’s Operatin

g

Income = Transfer

Price – Variable Cost

per Unit × Units

Transferred

$75,000 = ($11.00 – $10.00) × 75,000 units

This is the amount the Appliance Division earns by using available excess

capacity to produce and sell products above variable cost to the Electronics

Division.

d. Any transfer price will cause the total income of the company to increase, as

long as the supplier division’s capacity is used toward making materials for

products that are ultimately sold to the outside. However, transfer prices

459

PROBLEMS

P14–1

1. RAPTOR COMPANY

Budget Performance Report—Director, Bulldozer Division

For the Month Ended August 31, 20Y6

Over (Under)

Budget Actual Budget Budget

Customer service salaries ……. $ 125,000 $ 184,000 $59,000 $ —

Insurance and property taxes 25,000 24,550 — (450)

Distribution salaries …………….. 237,500 234,750 — (2,750)

2. The customer service and marketing salaries are significantly over budget.

The director should investigate the cause of these results. One possibility is

that the company is having an increase in sales, requiring greater marketing

460

P14–2

1.

CARRY ON FREIGHT INC.

Divisional Income Statements

For the Quarter Ended December 31, 20Y3

Air Rail Truck

Revenues ……………………………………………….. $ 2,500,000 $ 3,000,000 $ 4,500,000

Operating expenses ……………………………….. (2,050,000) (2,450,000) (3,777,500)

Operating income before service

Supporting schedules:

Service department charge rates for the two service departments, Customer

Support and Legal, are determined as follows:

Air Rail Truck Total

Number of customer contacts …… 750 2,250 8,000 11,000

Number of hours billed ……………… 450 1,200 3,350 5,000

Service

461

P14–2, Concluded

2. The CEO evaluates the three divisions using operating income as a percent of

revenues (profit margin). This measure is calculated for the three divisions as

follows:

Air Division: 15.1% ($376,650 ÷ $2,500,000)

3. To: CEO

The method used to evaluate the performance of the divisions should be

reevaluated. The present method identifies the amount of operating income

per dollar of earned revenue. However, this company requires a significant in-

vestment in fixed assets and distribution facilities. In addition, the amount of

assets may not be related to the revenue earned. For example, some divisions