CHAPTER 14

THE PRODUCTION CYCLE

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

14.1. When activity-based cost reports indicate that excess capacity exists, management

should either find alternative revenue-enhancing uses for that capacity or eliminate

it through downsizing. What factors influence management’s decision? What are

the likely behavioral side effects of each choice? What implications do those side

effects have for the long-run usefulness of activity-based cost systems?

It will often be easier to identify opportunities to downsize and eliminate jobs than to find

creative value-adding activities for excess capacity. Thus, management may be more

Ch. 14: The Production Cycle

14.2. Why should accountants participate in product design? What insights about costs

can accountants contribute that differ from the perspectives of purchasing

managers and engineers?

Product design is concerned with designing a product that meets customer requirements

in terms of quality, durability, and functionality while also minimizing costs.

14.3. Some companies have eliminated the collection and reporting of detailed analyses on

direct labor costs broken down by various activities. Instead, first-line supervisors

are responsible for controlling the total costs of direct labor. The justification for

this argument is that labor costs represent only a small fraction of the total costs of

producing a product and are not worth the time and effort to trace to individual

activities. Do you agree or disagree with this argument? Why?

This question should create some debate. The important issues to keep in mind are:

• How will management use detailed labor data?

Production Cycle

14.4. Typically, McDonald’s produces menu items in advance of customer orders based

on anticipated demand. In contrast, Burger King produces menu items only in

response to customer orders. Which system (MRP-II or lean manufacturing) does

each company use? What are the relative advantages and disadvantages of each

system?

McDonald’s uses MRP-II; Burger King uses JIT.

14.5 Some companies have switched from a “management by exception” philosophy to a

“continuous improvement” viewpoint. The change is subtle, but significant.

Continuous improvement focuses on comparing actual performance to the ideal

(i.e., perfection). Consequently, all variances are negative (how can you do better

than perfect?). The largest variances indicate the areas with the greatest amount of

“waste,” and, correspondingly, the greatest opportunity for improving the bottom

line. What are the advantages and disadvantages of this practice?

An advantage of continuous improvement reports is that they combat the tendency for

complacency.

Ch. 14: The Production Cycle

SUGGESTED ANSWERS TO THE PROBLEMS

14.1. Match the terms in the left column with their definitions from the right column:

1. _c__ Bill of materials

a. A factor that causes costs to change.

3. _l__ Master Production

Schedule

c. A list of the raw materials used to create a finished

product.

4. _m_ Lean manufacturing

d. A document used to authorize removal of raw

materials from inventory.

5. _j__ Production order

e. A cost-accounting method that assigns costs to

products based on specific processes performed.

6. _d__ Materials requisition

specific batches or production runs and is used

when the product or service consists of uniquely

identifiable items.

f. A cost accounting method that assigns costs to

7. _i__ Move ticket

g. A cost accounting method that assigns costs to

each step or work center and then calculates the

average cost for all products that passed through

that step or work center.

8. _h__ Job-time ticket

h. A document that records labor costs associated

with manufacturing a product.

9. _f__ Job-order costing

i. A document that tracks the transfer of inventory

from one work center to another.

10. _a_ Cost driver

j. A document that authorizes the manufacture of a

finished good.

11. _b_ Throughput

k. A document that lists the steps required to

manufacture a finished good.

12. _o_ Computer-integrated

manufacturing

l. A document that specifies how much of a finished

good is to be produced during a specific time

period.

m. A production planning technique that is an

extension of the just-in-time inventory control

method.

n. A production planning technique that is an

extension of the Materials Requirement Planning

inventory control method.

o. A term used to refer to the use of robots and other

IT techniques as part of the production process.

2. _k__ Operations list

b. A measure of the number of good units produced

Production Cycle

14.2 What internal control procedure(s) would best prevent or detect the following

problems?

a. A production order was initiated for a product that was already overstocked in

the company’s warehouse.

Base the master production schedule on

Current data on product sales

b. A production employee stole items of work-in-process inventory.

• Ensure good supervision by factory supervisors.

c. The “rush–order” tag on a partially completed production job became detached

from the materials and lost, resulting in a costly delay.

Use rush order tags

d. A production employee entered a materials requisition form into the system in

order to steal $300 worth of parts from the raw materials storeroom.

Limit authority to prepare or authorize materials requisitions to production

planning personnel and perhaps factory supervisors.

Ch. 14: The Production Cycle

e. A production worker entering job-time data on an online terminal mistakenly

entered 3,000 instead of 300 in the “quantity–completed” field.

Validate input by comparing the quantity entered with the quantity scheduled

f. A production worker entering job-time data on an online terminal mistakenly

posted the completion of operation 562 to production order 7569 instead of

production order 7596.

g. A parts storeroom clerk issued parts in quantities 10% lower than those

indicated on several materials requisitions and stole the excess quantities.

The discrepancy should show up in an unfavorable materials usage variance, since

the shortage will necessitate requesting additional goods. To deter this type of

problem:

h. A production manager stole several expensive machines and covered up the loss

by submitting a form to the accounting department indicating that the missing

machines were obsolete and should be written off as worthless.

Limit authority to write off expensive machines to management

Production Cycle

i. The quantity-on-hand balance for a key component shows a negative balance.

Use sign checks on master file balances after every file update

j. A factory supervisor accessed the operations list file and inflated the standards

for work completed in his department. Consequently, future performance

reports show favorable budget variances for that department.

Restrict update access to operations list to a limited number of authorized

usage and investigate any material differences

k. A factory supervisor wrote off a robotic assembly machine as being sold for

salvage, but actually sold the machine and pocketed the proceeds.

• Limit authority to write off machines to management

equipment.

l. Overproduction of a slow-moving product resulted in excessive inventory that

had to eventually be marked down and sold at a loss.

• Create a Master Production Schedule based on information from sales forecasts

and customer orders, taking into account inventory on hand.

Ch. 14: The Production Cycle

14.3 Use Table 14-1 to create a questionnaire checklist that can be used to evaluate

controls for each of the basic activities in the production cycle (product design,

planning and scheduling, production operations, and cost accounting).

a. For each control issue, write a Yes/No question such that a “No” answer

represents a control weakness.

A wide variety of questions is possible. Below is a sample list:

Question

Yes

No

1. Is access to production master data (production orders, inventory,

master production schedule, etc.) restricted?

2. Is the production master data regularly reviewed and all changes

6. Are appropriate data entry edit controls used?

7. Is a perpetual inventory of raw materials components maintained?

8. Are physical counts of raw materials inventory taken regularly and used

to adjust the perpetual inventory records?

9. Are competitive bids used when ordering fixed assets?

10. Are reports prepared showing the number of unique components for

each finished product?

11. Are warranty and repair costs tracked for each finished product?

12. Is a Master Production Schedule (MPS) created and followed?

13. Are materials requisitions used to authorize and document removal of

raw materials from inventory?

14. Are move tickets used to document transfers of raw materials and

15. Are the disposals of fixed assets documented?

16. Is there insurance against losses due to fire, flood, or other disaster?

investigated?

3. Is production data encrypted while stored in the database?

4. Does a backup and disaster recovery plan exist?

5. Have backup procedures been tested within the past year?

Production Cycle

b. For each Yes/No question, write a brief explanation of why a “No” answer

represents a control weakness.

Question

Reason a “No” answer represents a weakness

1

2

Failure to investigate all changes to production master data may allow errors

to remain undetected that result in over- or under-production of finished

goods.

3

Failure to encrypt production data can result in the unauthorized disclosure

of sensitive information.

Unrestricted access to the production master data could result in disclosure

4

If a backup and disaster recovery plan does not exist, the organization may

lose important data.

5

If the backup plan is not regularly tested, it may not work.

6

Without proper data entry edit controls, errors may occur in recording

production operations, which may result in inventory valuation errors, over-

or under-production, or poor pricing decisions.

7

Without a perpetual inventory system, shortages and excess inventory is

more likely.

8

Without periodic physical counts and any necessary inventory records

adjustments, the perpetual inventory records are likely to be incorrect.

9

Without competitive bids, purchases may be at higher than necessary prices.

result in poor product design or excessive costs of production and inventory.

11

Failure to trace warranty and repair costs to specific finished products

precludes correcting poor product designs.

12

Without a Master Production Schedule, unauthorized production orders

could result in over-production of finished goods. There could also be

underproduction of finished goods.

13

Failure to document transfer of raw materials from inventory stores can lead

to theft.

14

Not documenting the transfer of raw materials and work-in-process can

prevent discovery of theft and make it difficult to identify the perpetrator.

15

Not documenting the disposal of fixed assets can cover up theft and make it

difficult to identify the perpetrator.

16

Lack of adequate insurance exposes the organization to the risk of

substantial monetary loss in the event of an insurable incident.

Ch. 14: The Production Cycle

14.4 You have recently been hired as the controller for a small manufacturing firm that

makes high-definition televisions. One of your first tasks is to develop a report

measuring throughput.

Describe the data required to measure throughput and the most efficient and

accurate method of collecting that data.

Throughput = A x B x C where

A = total production (units) / processing time

B = processing time / total elapsed real time

Total time spent in operations (processing time) can be collected by measuring the time

spent on each operation. This can be most accurately done with badge or card readers at

each station.

Total production can be recorded by counting (with bar-code scanners or using RFID tags

, if possible) all units produced at each step of the manufacturing process.

Subtracting defective units from total production yields good production.

Production Cycle

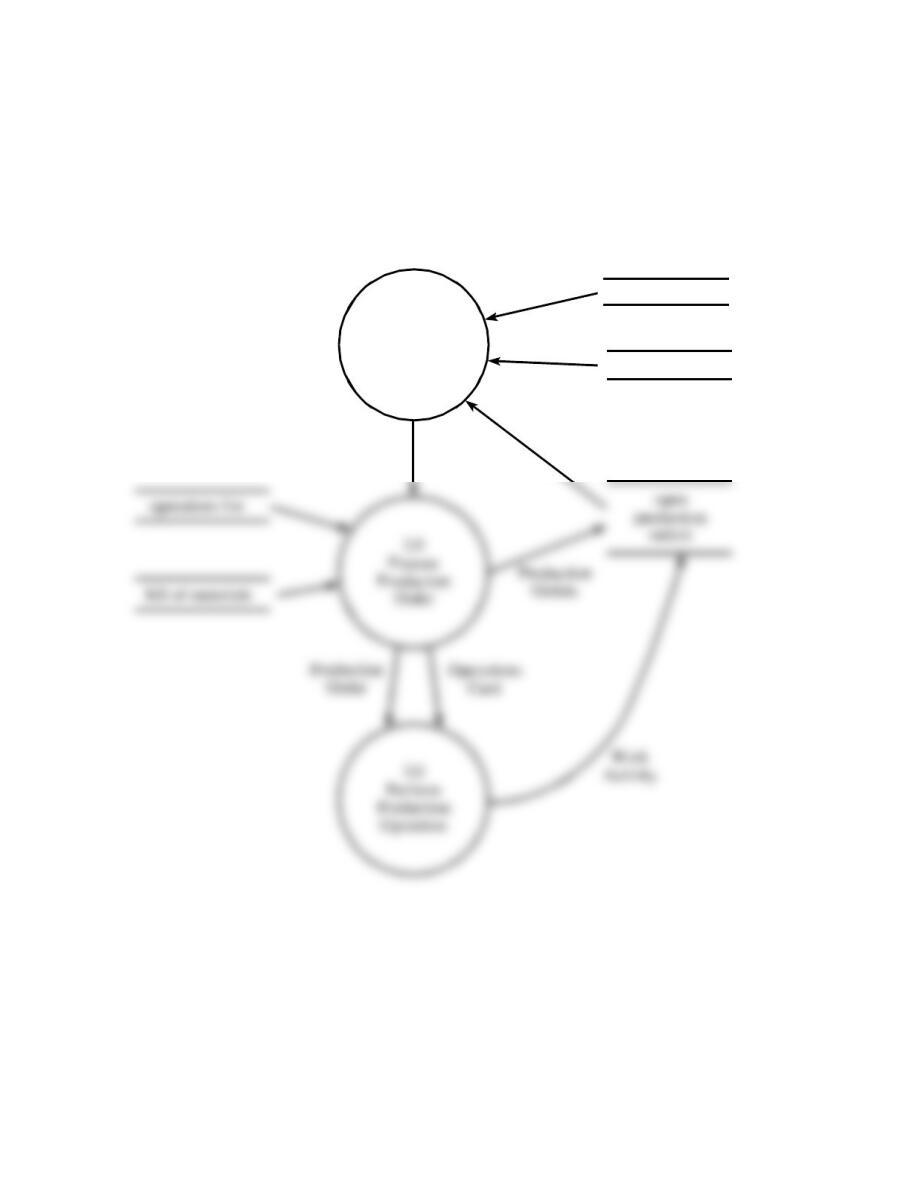

14.5 The Joseph Brant Manufacturing Company makes athletic footwear. Processing of

production orders is as follows: At the end of each week, the production planning

department prepares a master production schedule (MPS) that lists which shoe

styles and quantities are to be produced during the next week. A production order

preparation program accesses the MPS and the operations list (stored on a

permanent disk file) to prepare a production order for each shoe style that is to be

manufactured. Each new production order is added to the open production order

master file stored on disk.

Ch. 14: The Production Cycle

a. Prepare a data flow diagram of all operations described.

inventory

sales forecasts

Scheduled

Production

MPS

1.0

Plan

Production

QOH

Production Cycle

b. What control procedures should be included in the system?

A large number of controls are possible, including the following:

• Access Control – User ID and Password

• Compatibility Test – Password

• Preformatting or Prompting -All Data Entered

• Record Count – # of Transactions

Ch. 14: The Production Cycle

14.6 The XYZ company’s current production processes have a scrap rate of 15% and a

return rate of 3%. Scrap costs (wasted materials) are $12 per unit; warranty/repair

costs average $60 per unit returned. The company is considering the following

alternatives to improve its production processes:

• Option A: Invest $400,000 in new equipment. The new process will also require

an additional $1.50 of raw materials per unit produced. This option is predicted

to reduce both scrap rates return rates by 40% from current levels.

a. Assume that current production levels of 1,000,000 units will continue. Which

option do you recommend? Why?

At current production levels of 1,000,000 units, none of the options reduce total costs, but

option B results in the smallest increase in total costs.

Option A:

Investment = $400,000 + $1.5 x 1,000,000 units = $1,900,000.

Option B:

Investment = $50,000 + $3.2 x 1,000,000 units = $3,250,000

Option C:

Investment = $2,000,000

Production Cycle

b. Assume that because all of the proposed changes will increase product quality,

that production will jump to 1,500,000 units. Which option do you recommend?

Why?

At production levels of 1,500,000 units, options B and C both reduce total costs. Option

C, however, reduces them the most.

Option A:

Investment = $400,000 + $1.5 x 1,500,000 units = $2,650,000.

Savings = $2,160,000:

Reduced scrap costs = 40% x 15% x $12 x 1,500,000 units = $1,080,000

Reduced warranty/repair costs = 40% x 3% x $60 x 1,500,000 units =

$1,0800,000

Option B:

Option C:

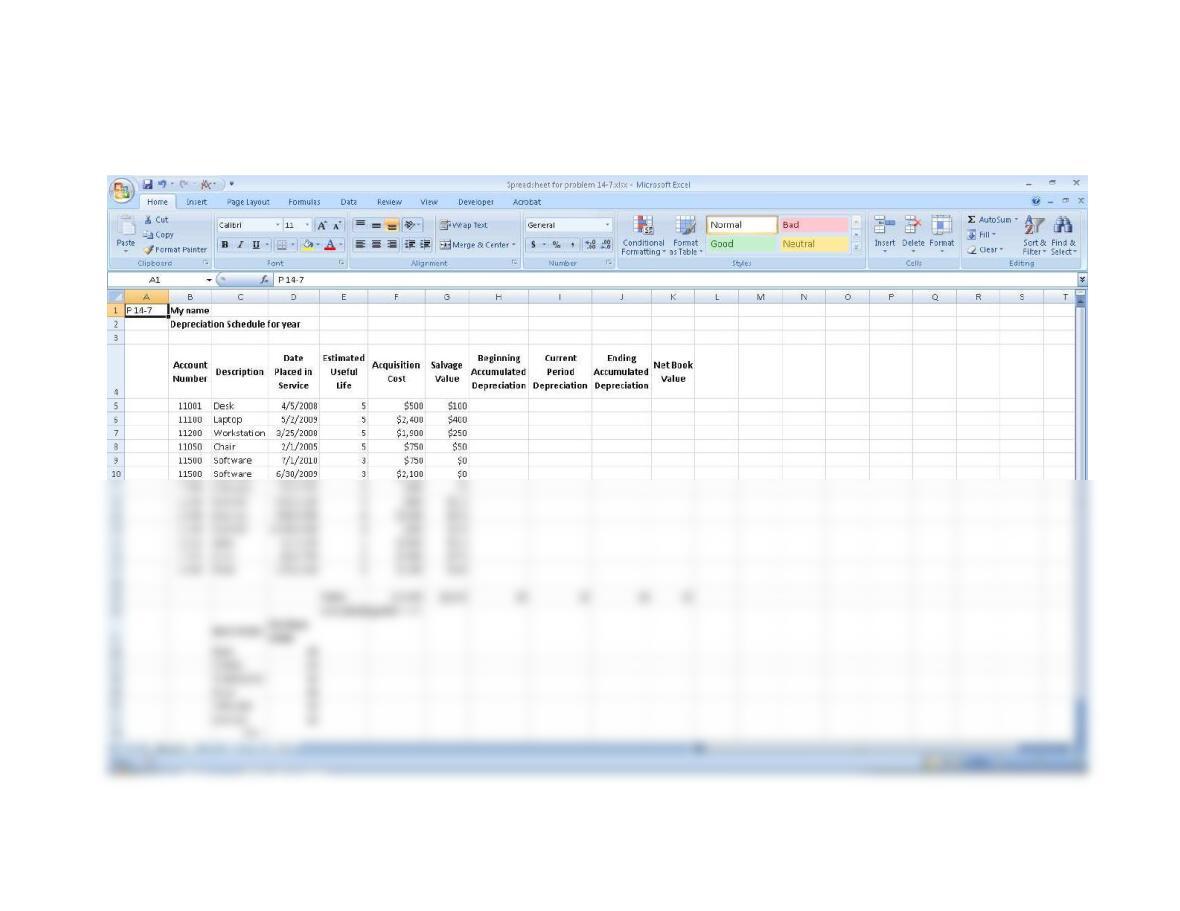

14.7 EXCEL PROBLEM

a. Create the following spreadsheet

Production Cycle

b. Create formulas to calculate

• Accumulated depreciation (all assets use the straight line method; all assets acquired any time during the year get

a full year’s initial depreciation)

• Current year’s depreciation (straight-line method, full amount for initial year in which asset acquired)

c. Create a table at the bottom of your worksheet that consists of two columns:

• Asset name (values should be chair, desk, laptop, monitor, software, and workstation)

d. Enter your name in row 1 in the cell to the right of the text “Name”