Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

14

Business Unit Performance Measurement

Solutions to Review Questions

14-1.

Divisional income is relatively easy to compute because the data exist for financial

14-2.

The basic computations are the same. Because divisional income is not reported, the

14-3.

ROI = (After-tax income ÷ Divisional assets).

14-4.

14-5.

There are two common situations. First, managers might choose not to invest in

14-6.

14-7.

EVA® makes adjustments to income and investment to correct accounting calculations

14-8.

14-9.

The danger is that you will ignore the interdependence of the business units. No

Solutions to Critical Analysis and Discussion Questions

14-10.

14-11.

14-12.

Two problems usually arise here:

(a) The division might be encouraged to produce in volumes in excess of sales. In this

14-13.

There are two common situations. First, managers might choose not to invest in

14-14.

Residual income measures depend upon the rate chosen for charging a division for its

14-15.

The reason the division manager has been delegated the authority to make investment

14-16.

• Residual Income (RI) is defined as follows:

Investment center operating profits—(Capital charge × Investment center assets)

14-17.

The problem with using the same measure of performance for managers at all levels in

14-18.

If the division can rent and the rent does not have to be capitalized for inclusion in the

14-19.

ROI does not take the time value of money into account; it is computed based on

14-20.

Residual income divided by divisional assets is just ROI minus the cost of capital (see

14-21.

Solutions to Exercises

14-22. (10 min.) Compute Divisional Income: Arlington Clothing, Inc.

Operating Income

(thousands)

Lake Region

Coastal Region

Sales revenue ....................................................

$4,080.0

$12,920.0

Cost of sales ......................................................

2,616.3

6,460.0

14-23. (10 min.) Compute Divisional Income: Arlington Clothing, Inc.

Operating Income

(thousands)

Lake

Region

Coastal

Region

Sales revenue ....................................................

$4,080.0

$9,520.0

Comments:

In addition to the comments for exercise 14-22, nothing changed in Lake Region.

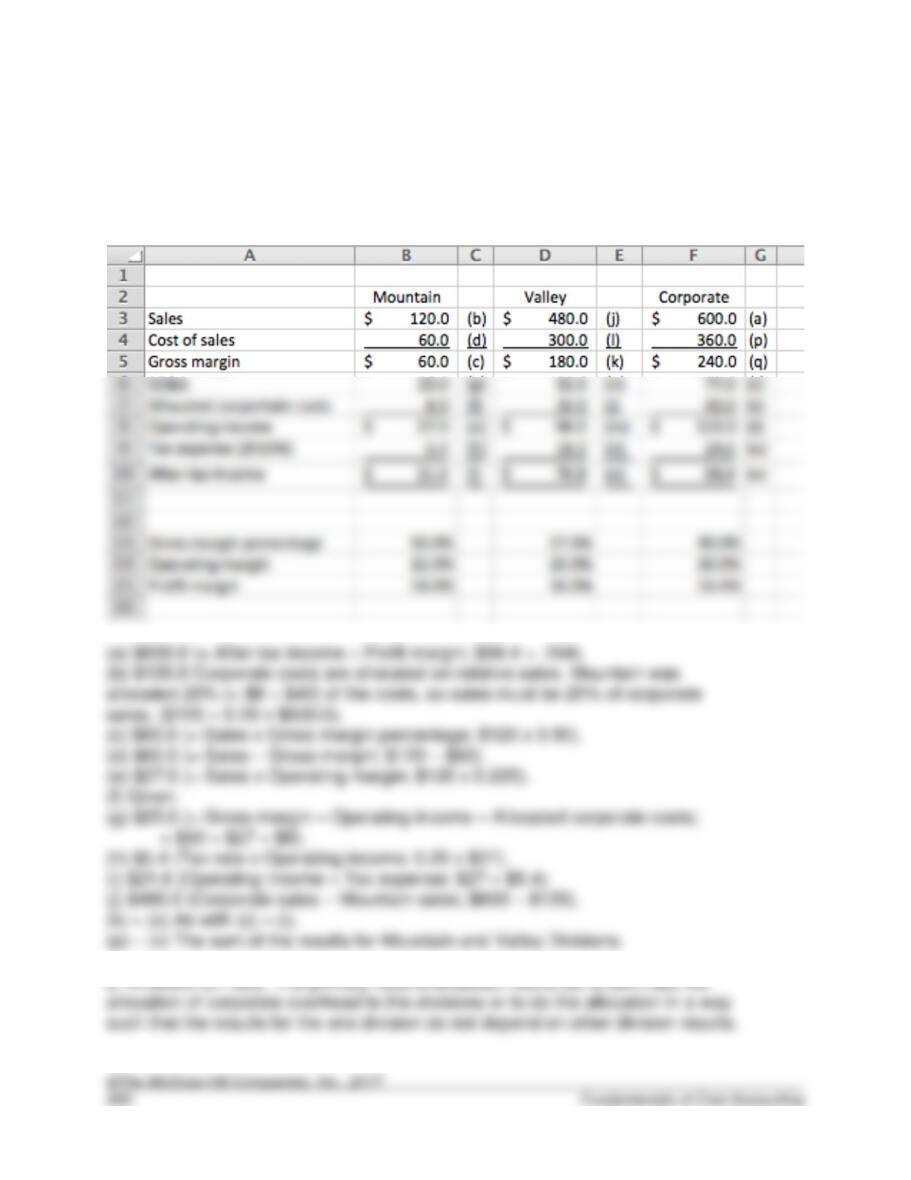

14-24. (10 min.) Compute Divisional Income: Incomplete Information and Financial

Ratios: Sneaky Pete’s.

a. There are many approaches to solving this problem (although it is likely that the first

step will be to calculate total corporate sales). One approach follows.

14-25. (10 min.) Compute RI and ROI: All-States Bank.

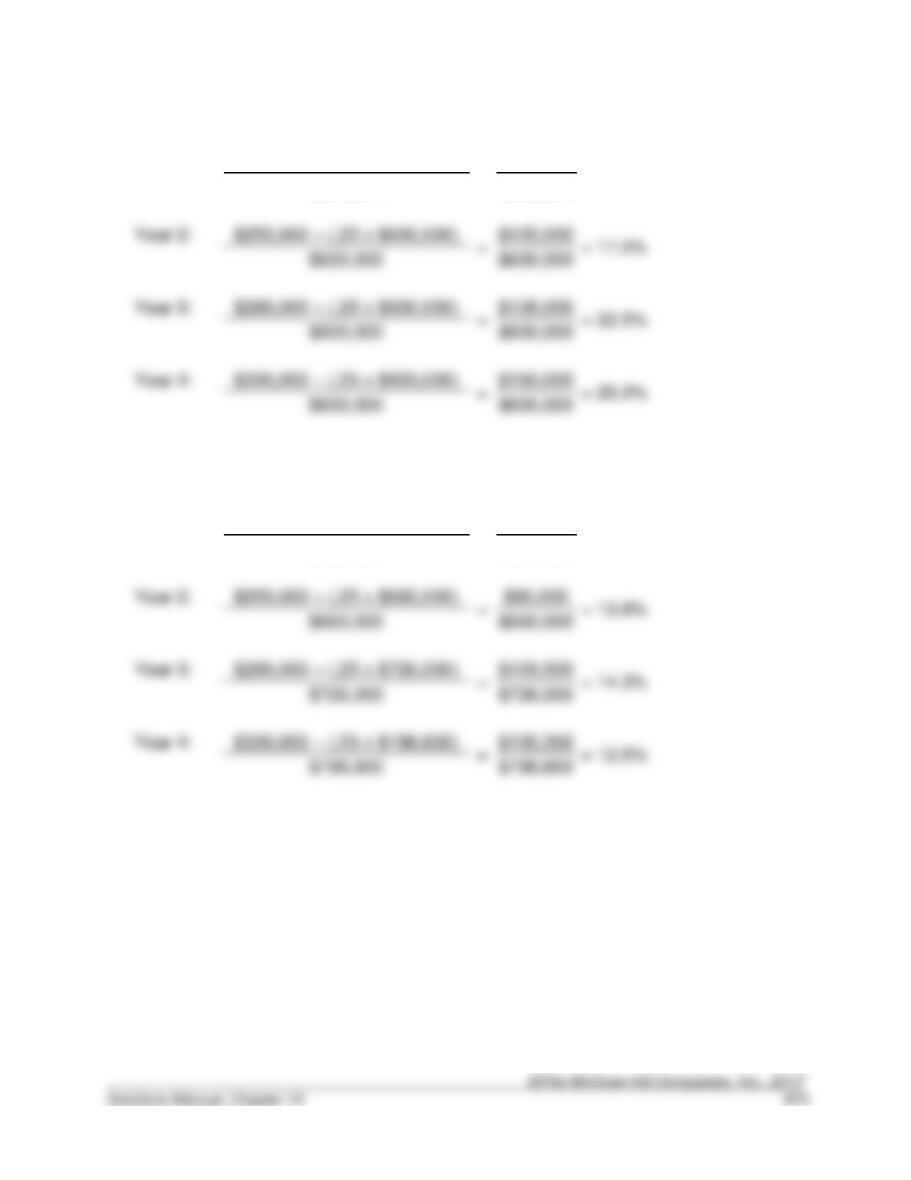

14-26. (25 min.) ROI Versus RI.

Annual income = $700,000 – ($2,520,000 ÷ 4 years) = $70,000

Year

Investment

Base

(a)

ROI

$70,000 ÷ Base

(b)

Residual Income

$70,000 – (8% x Base)

14-27. (10 min.) Compare Alternative Measures of Division Performance:

Solomons Company.

a. Using return on investment measures:

*North:

$6,000,000

= 20%

14-28. (10 min.) Comparing Business Units Using ROI: BMI.

East

West

14-29. (10 min.) Comparing Business Units Using Residual Income: BMI.

East

West

Income

$200

$390

14-30. (10 min.) Comparing Business Units Using Economic Value Added: BMI.

In computing EVAs, we need to adjust both income and investment (assets). The

income adjustment is for R&D and the investment adjustment is for R&D and

current liabilities. Because R&D is assumed to benefit two periods, we only

expense 50% of R&D (it is assumed spent at the beginning of the year) each

year.

14-31. (10 min.) Impact of New Asset on Performance Measures: Patio

Enterprises.

14-32. (10 min.) Impact Of Leasing On Performance Measures: Patio

Enterprises.

With the lease, the incremental income is the operating cash flow minus the lease

The new ROI is:

14-33. (15 min.) Residual Income Measures And New Project Consideration:

Patio Enterprises.

14-34. (20 min.) Impact of an Asset Disposal on Performance Measures: Harbor

Division.

a. ROI before disposal:

14-35. (20 min.) Impact of an Asset Disposal on Performance Measures: Harbor

Division.

14-36. (25 min.) Compare Historical Cost, Net Book Value To Gross Book Value:

Ste. Marie Division.

a. Net Book Value

b. Gross Book Value

Year 1

($20,000,000 – $9,000,000)

($20,000,000 – $9,000,000)

($90,000,000 – $9,000,000)

$90,000,000

14-37. (25 min.) Compare ROI Using Net Book And Gross Book Values: Ste.

Marie Division.

a. Net Book Value

b. Gross Book Value

Year 1

($20,000,000 – $9,000,000)

($20,000,000 – $9,000,000)

$90,000,000

$90,000,000

c. Of course, there is no change under the gross book value method. With the net

14-38.

(30 min.) Compare Current Cost To Historical Cost: St. Marie Division.

Parts c and d can be solved easier if one first sets up a table showing the change in value of the depreciable assets.

(1)

Gross Depreciable

Asset Valuea

(2)

Yearly

Depreciation

[col. (1) x 25%]

(3)

Total Depreciation

(1) (Years of life ÷ 4 years)

Year 1

$36,000,000 x 1.1 = $39,600,000

$9,900,000

$39,600,000 x 1/4 = $9,900,000

14-38. (continued)

a.

Historical Cost

Net Book Value

b.

Historical Cost

Gross Book Value

Year 1

($22,000,000 – $9,000,000)

($22,000,000 – $9,000,000)

($90,000,000 – $9,000,000)

$90,000,000

14-38. (continued)

c.

Current Cost

Net Book Value

d.

Current Cost

Gross Book Value

Year 1

($22,000,000 – $9,900,000)

($22,000,000 – $9,900,000)

($99,000,000 – $9,900,000)

$99,000,000

14-39. (25 min.) Effects Of Current Cost On Performance Measurements: Upper

Division.

a.

ROI

Year 1:

$225,000 – (.25 x $600,000)

=

$75,000

= 12.5%

$600,000

$600,000

b.

ROI

Year 1:

$225,000 – (.25 x $600,000)

=

$75,000

= 12.5%

$600,000

$600,000

Solutions to Problems

14-40. (30 min.) Comparing Business Units Using Divisional Income, ROI, and

Residual Income: Colonial Pharmaceuticals.

a. – d. Note that because we ignore income taxes, operating income is the same as net

income.

14-41. (20 min.) Comparing Business Units Using EVA: Colonial Pharmaceuticals.

a.

In computing EVAs, we need to adjust both income and investment (assets). The income

and investment adjustments are for R&D. For AC Division, R&D is assumed to benefit two

periods, we only expense 50% of R&D (it is assumed spent at the beginning of the year)

each year. For SO Division, we only expense (1/9), because it is assumed that R&D

benefits nine years.

AC Division

Adjusted profit ...................

[$1,500 + (50% x $2,000)] = $2,500

b. Based on EVA, SO performed better than AC. The difference between the EVA result

14-42. (20 min.) Comparing Business Units Using EVA: Colonial Pharmaceuticals.

a.

In solving this problem, we need to recognize that the same proportion of the R&D

investment is added to net (or in this case operating) income and divisional investment.

b. Answers will vary. From the discussion in the problem, it appears that the two divisions

make different products, sell in different markets, perhaps are subject to different

14-43. (30 min.) Equipment Replacement And Performance Measures: Pitt, Inc.

ROI

a.

$3,750,000

c.

$5,025,000b

14-44. (20 min.) Evaluate Trade-Offs In Return Measurement: Pitt, Inc.

b. For the manager, the relevant cost is the lost bonus this year if the machine is

purchased this year versus the effect on the manager’s bonus that would arise from the

increased depreciation charge. If the manager waits until next year, then the return on

investment for this year would be the 60% as indicated in Problem 14-43, part a. For the

coming year, the ROI would be:

$4,700,000a – $3,500,000b

=

$1,200,000

= 18.0%

$4,000,000 – (2 x $1,250,000) + $7,475,000c – $2,325,000d

$6,650,000

assuming that the new equipment is bought at the beginning of the year.

a

$4,700,000 =

$5,025,000 + $2,000,000 – $2,325,000.

14-45. (30 min.) Economic Value Added: Pitt, Inc.

(In thousands of dollars)

a.

Residual Income

$3,750 – 0.12 x ($4,000 + $5,000 – $1,500 – $1,250)

= $3,000

c.

$5,025b – 0.12 x ($4,000 – (2 x $1,250) + $6,500 – $2,000)

= $4,305

14-46. (20 min.) Evaluate Trade-Offs In Performance Measurement and Decisions:

Pitt, Inc.

b. For the manager, the relevant cost is the lost bonus this year if the machine is

purchased this year versus the effect on the manager’s bonus that would arise from the

increased depreciation charge. If the manager waits until next year, then the residual

income for this year would be the $3 million as indicated in Problem 14-45, part a. For the

coming year, the residual income would be (in thousands of dollars):

assuming that the new equipment is bought at the beginning of the year.

14-47. (40 min.) ROI and Management Behavior—Ethical Issues: Asher Company.

a. Most of the specific actions that division managers can take that would result in

b. Asher’s corporate goals and goals for its divisions are not congruent. Improving the

division ROI does not automatically lead to improved corporate ROI. Certain actions

c. The changes should be two-fold in character. The emphasis on a single measure for

performance evaluation should be eliminated. Additional factors important to division

and corporate goals should be included.

One approach would be to establish a target ROI, which would include allowances for

start-up costs of long-term projects. The company could consider the residual profits

14-47. (continued)

d. Answers will vary. Clearly, manipulating numbers at the division level is unethical (and

CMA adapted

14-48. (30 min.) Impact of Decisions to Capitalize or Expense on Performance

Measurement—Ethical Issues: Pharm-It.

a.

ROI

Base Year

This Year

If R&D is expensed:

c. The board should reject the request for a bonus. The purpose of the bonus is to

14-49. (30 min.) Evaluate Performance Evaluation System—Behavioral issues:

Seville Products.

a. An answer that assumed that managers should only be held responsible for what they

control would make the following arguments:

The financial reporting and performance evaluation program of Seville Products is

inappropriate as a measure of the responsibilities of the Salvador Division. Salvador is

b. Following the notion that managers should be held responsible only for what they

control, the answer to requirement b would be:

The following revisions should be made to Seville Products’s financial reporting and

performance evaluation system.

CMA adapted.

14-50. (35 min.) ROI, EVA, Different Asset Bases: Hy’s.

a. and b.

Income statements to summarize the alternatives are as follows:

Regular

Merchandise

Appliances

Total

Sales revenue ....................................................

$4,680,000

$1,350,000

$6,030,000

Cost of sales ......................................................

2,934,000

1,026,000

3,960,000

c. If the floor plan is used, the investment base will be $3,375,000. Total operating profits

14-50. (continued)

e.

Income statements to summarize the alternatives are as follows: ($ in thousands)

Regular

Merchandise

Appliances

Total

Sales revenue ....................................................

$4,680,000

$1,350,000

$6,030,000

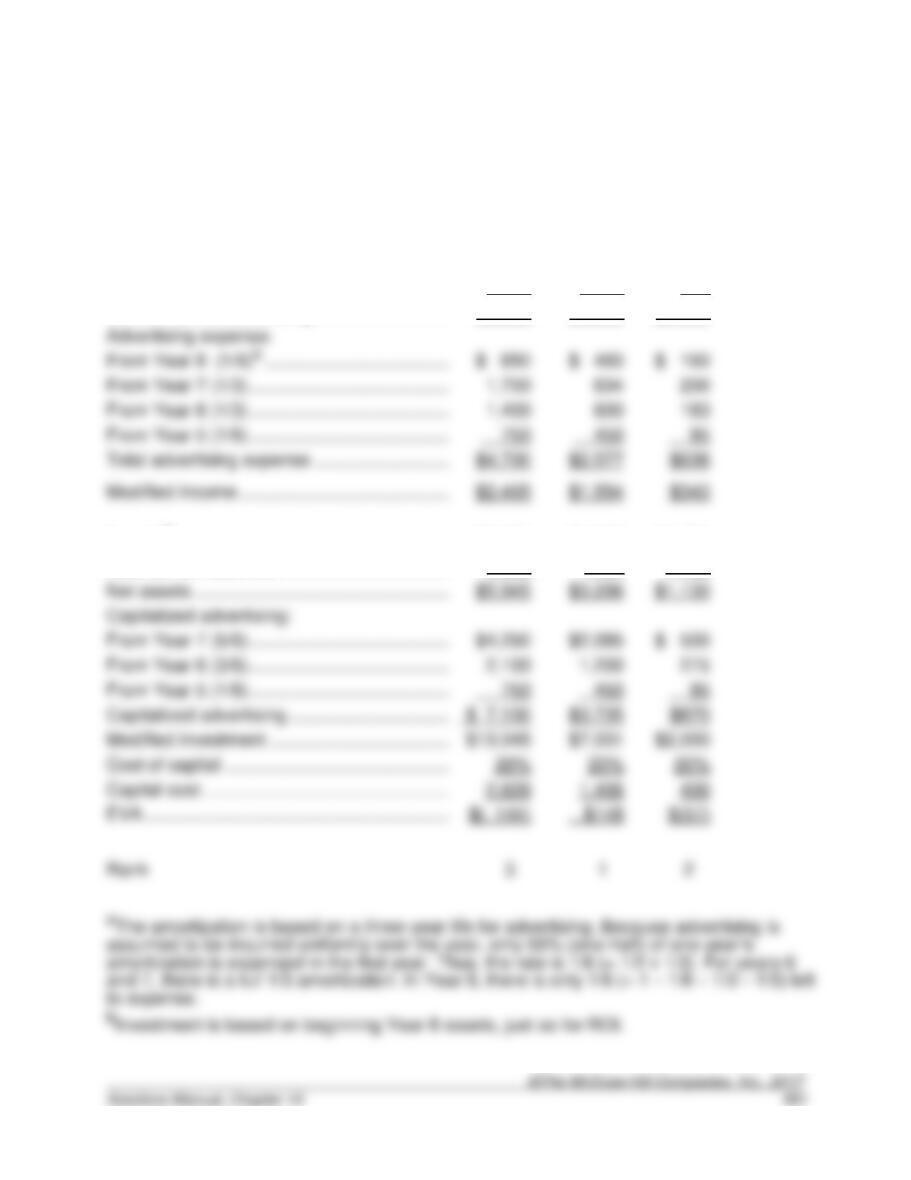

14-51. (35 min.) Economic Value Added: Bisbee Health Products.

After-tax income ...............................................................

$7,500,000

Add back R&D expense for year 2 ...................................

4,800,000

$12,300,000

14-52. (35 min.) Economic Value Added: Biddle Company.

After-tax income ...............................................................

$600,000

Add back advertising expense for year 3 .........................

360,000

$960,000

Less amortization of advertising:

Year 1 advertising: 10% x $150,000 .............................

$15,000

Solutions to Integrative Cases

14-53. (60 – 90 min.) Barrows Consumer Products (A).

a.

There are many possible problems in identifying the “best” performer, but some of the

most commonly cited by students are:

• Different measures can be used in the sector. Different performance measures lead

to different conclusions about the best performer. If different managers use different

14-53. (continued)

b.

(1) Income is given in the case:

County

Indonesia

The Philippines

Vietnam

(2) ROI is computed at Barrows as Operating income ÷ Beginning assets. Notice that

Barrows does not use after-tax income in computing this ratio. This might be a good

time to discuss with students the fact that different companies and different analysts

14-53. (continued)

(3) EVA can be computed in many ways. This is one, in which advertising is amortized

over three years and advertising expenditures are assumed to be incurred uniformly

over the year.

($000)

Indonesia

Philippines

Vietnam

Income ...............................................................

$2,065

$1,176

$ 21

Advertising .........................................................

5,100

2,955

960

Income before advertising ..................................

$7,165

$4,131

$ 981

Assets b ..............................................................

$7,200

$4,000

$1,880

Less current liabilities .........................................

1,255

704

750

14-53. (continued)

c.

Answers will vary. Some common suggestions include dividing by population or by

d.

The following items should be included:

(1). The measure you recommend and why. It is important that the measure be one

that the company can actually collect data for use in calculations.

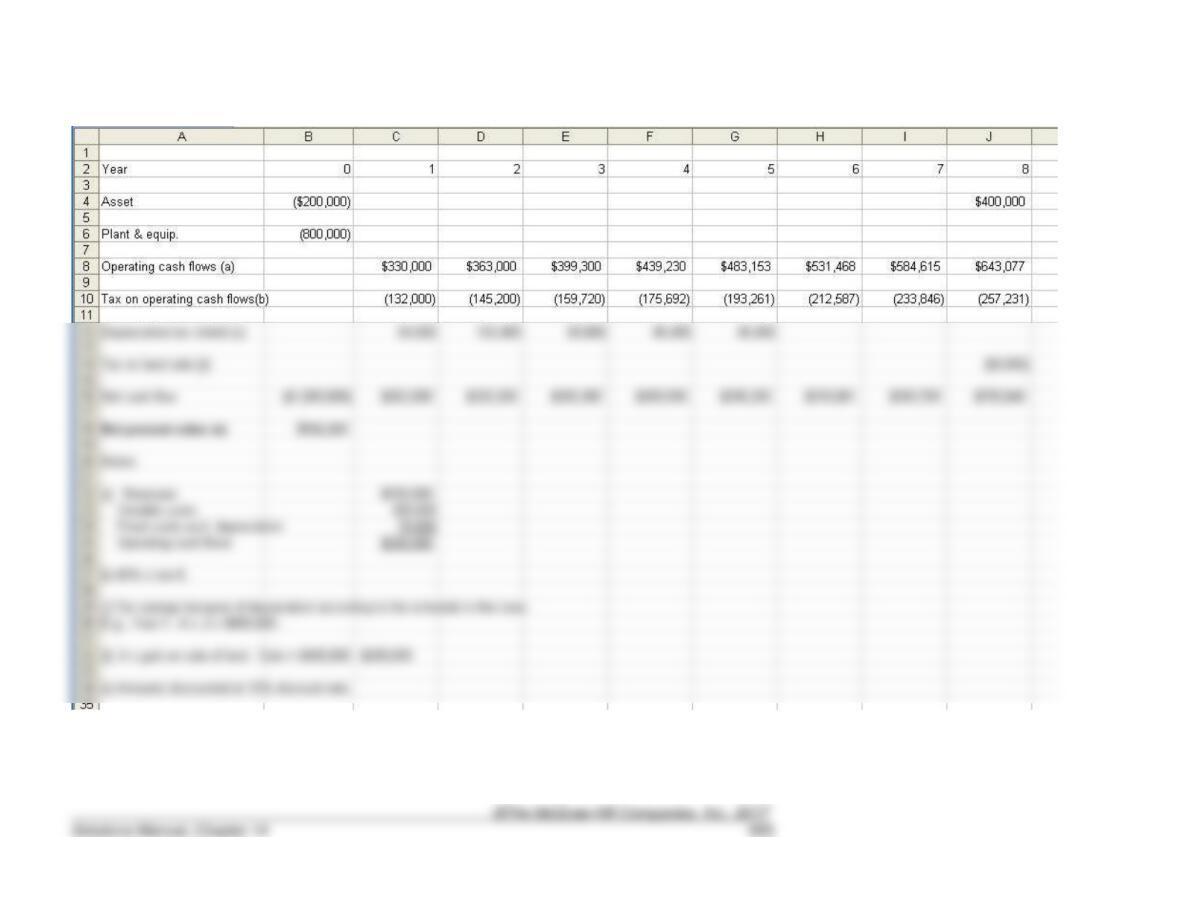

14-54. (60 – 90 min.) Capital Investment Analysis and Decentralized Performance

Measurement: Diversified Electronics.

a. David Parker's new product proposal was rejected because its ROI was less than 15

percent after tax.

The decision was not correct because it is inappropriate to use a short-term measure

like ROI to evaluate a long-term decision, ignoring completely the project's cash flows.

b. It appears that Diversified Electronics' management wanted the focus of division

managers to be on the profitability of their assets, which is why company management

used the investment center concept for performance evaluation. Therefore, Diversified

Electronics' choice of ROI makes sense because it is a measure of profitability of

assets used. (The company could also have used EVA.) By focusing on ROI,

company management delegates decision rights regarding sales (e.g., product pricing)

and costs to division managers. The benefits of delegation include reduction in cost of

corporate administration, improvement in operational decision making, increased

motivation at division level, and freeing corporate management up for more effective

utilization. However, some unexpected ROI-related pitfalls that the company’s

management apparently did not anticipate are:

1. It may not be appropriate to use one ROI performance standard for all divisions,

14-54. (continued)

14-54. (continued)

Possible Modification to the Present System

1. Within a division there could be a corporate ROI for evaluating the division and