EXERCISE 14-11

HORNER INC.

Balance Sheet (Partial)

December 31, 20XX

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $5 par value,

40,000 shares authorized,

30,000 shares issued ……………… $ 150,000

Common stock, no par, $1 stated

Total capital stock………………. 480,000

Additional paid-in capital

In excess of par—

preferred stock ……………………… 344,000

In excess of stated value—

Retained earnings (see Note R) ……………….. 800,000

Total paid-in capital and

EXERCISE 14-12

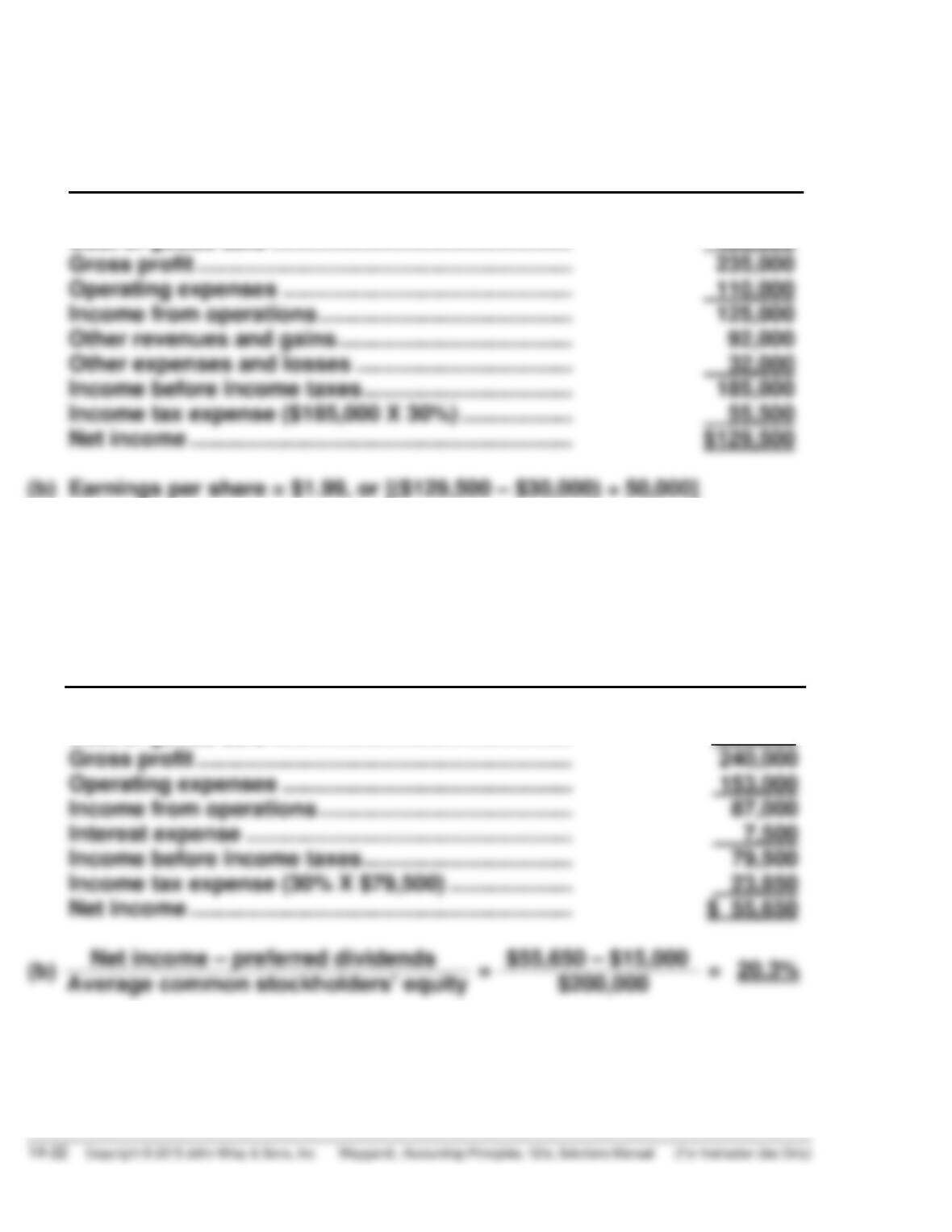

(a) NORMAN CORPORATION

Income Statement

For the Year Ended December 31, 2017

____________________________________________________________

Sales revenue ………………………………………………… $700,000

Cost of goods sold …………………………………………. 465,000

Gross profit ……………………………………………………. 235,000

Operating expenses ……………………………………….. 110,000

Income from operations ………………………………….. 125,000

EXERCISE 14-13

(a) PENNINGTON CORPORATION

Income Statement

For the Year Ended December 31, 2017

____________________________________________________________

Net sales ………………………………………………………… $600,000

Cost of goods sold …………………………………………. 360,000

Gross profit ……………………………………………………. 240,000

EXERCISE 14-14

Net income: $2,000,000 – $1,300,000 = $700,000;

$700,000 – (30% X $700,000) = $490,000

Preferred dividends: (50,000 X $20) X 6% = $60,000

EXERCISE 14-15

2017

2016

Earnings per share

$290,000– $20,000

100,000

= $2.70

$200,000– $20,000

80,000

= $2.25

$290,000– $20,000

$200,000– $20,000

EXERCISE 14-16

2017

2016

Earnings per share

$200,000– $20,000

150,000

= $1.20

$191,000– $20,000

180,000

= $0.95

= 10.0%

= 9.0%

EXERCISE 14-17

(a)

$241,000– $16,000

100,000

= $2.25

SOLUTIONS TO PROBLEMS

PROBLEM 14-1A

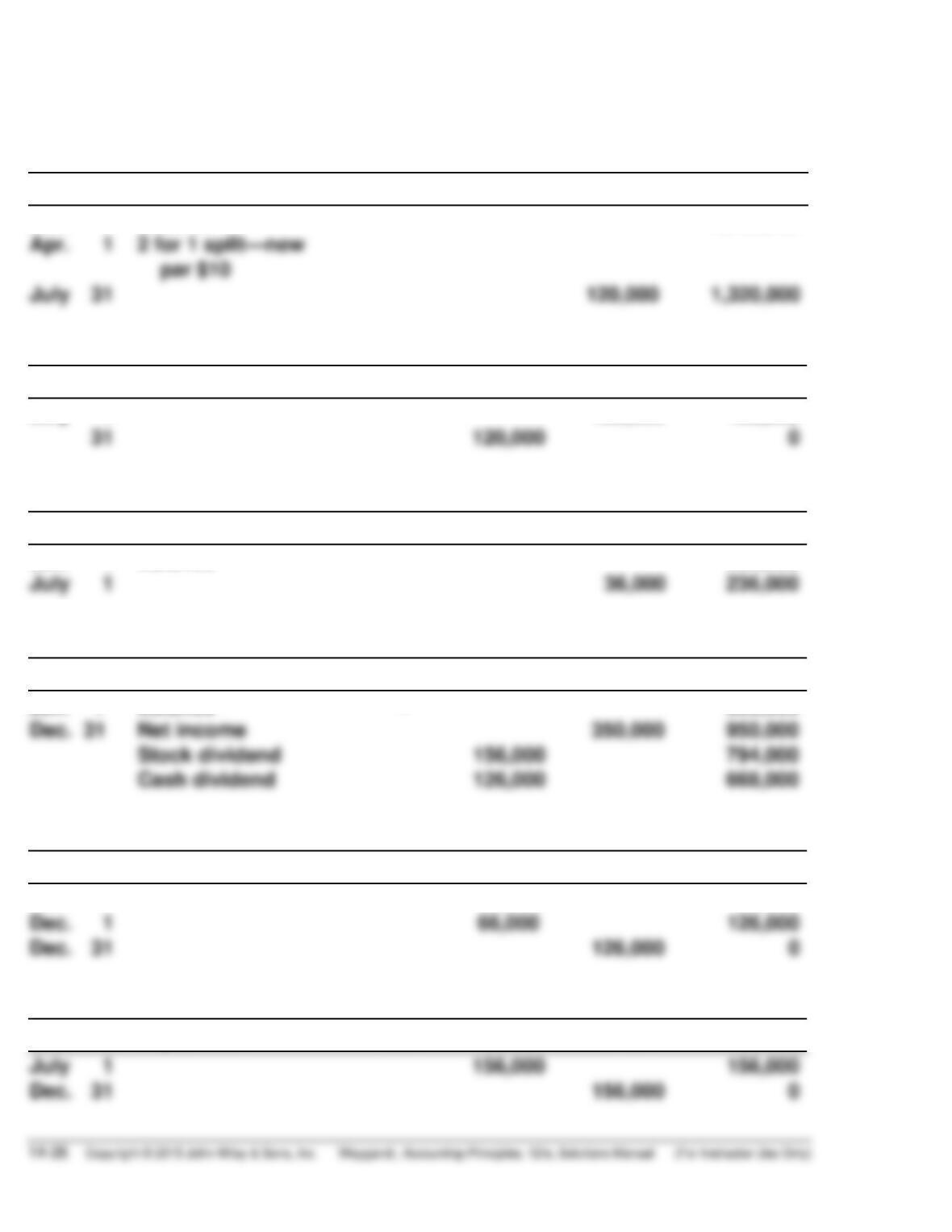

(a) Feb. 1 Cash Dividends (60,000 X $1) …………… 60,000

Dividends Payable ……………………. 60,000

Mar. 1 Dividends Payable …………………………... 60,000

Cash ………………………………………… 60,000

July 1 Stock Dividends (12,000 X $13) ………… 156,000

Common Stock Dividends

Distributable (12,000 X $10) …… 120,000

Paid-in Capital in Excess of

Par—Common Stock

(12,000 X $3) …………………………. 36,000

31 Common Stock Dividends

Distributable ……………………………….. 120,000

Common Stock ………………………… 120,000

PROBLEM 14-1A (Continued)

(b)

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 1

Jan. 1

Balance

1,200,000

Common Stock Dividends Distributable

Date

Explanation

Ref.

Debit

Credit

Balance

July 1

120,000

120,000

Paid-in Capital in Excess of Par—Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

200,000

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Dec. 31

Balance

Net income

350,000

600,000

950,000

Cash Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

Feb. 1

60,000

60,000

Stock Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 14-1A (Continued)

(c) GEFFREY CORPORATION

Balance Sheet (Partial)

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

Common stock, $10 par value, 132,000

PROBLEM 14-2A

(a) July 1 Cash Dividends

[($800,000 ÷ $5) X $.60] ………………… 96,000

Dividends Payable …………………… 96,000

Aug. 1 Retained Earnings ………………………….. 25,000

Accumulated Depreciation ……….. 25,000

15 Cash Dividends

[12,000 X ($50 X 6%)] …………………… 36,000

Dividends Payable …………………… 36,000

(b)

Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

600,000

PROBLEM 14-2A (Continued)

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

Common Stock Dividends Distributable

Date

Explanation

Ref.

Debit

Credit

Balance

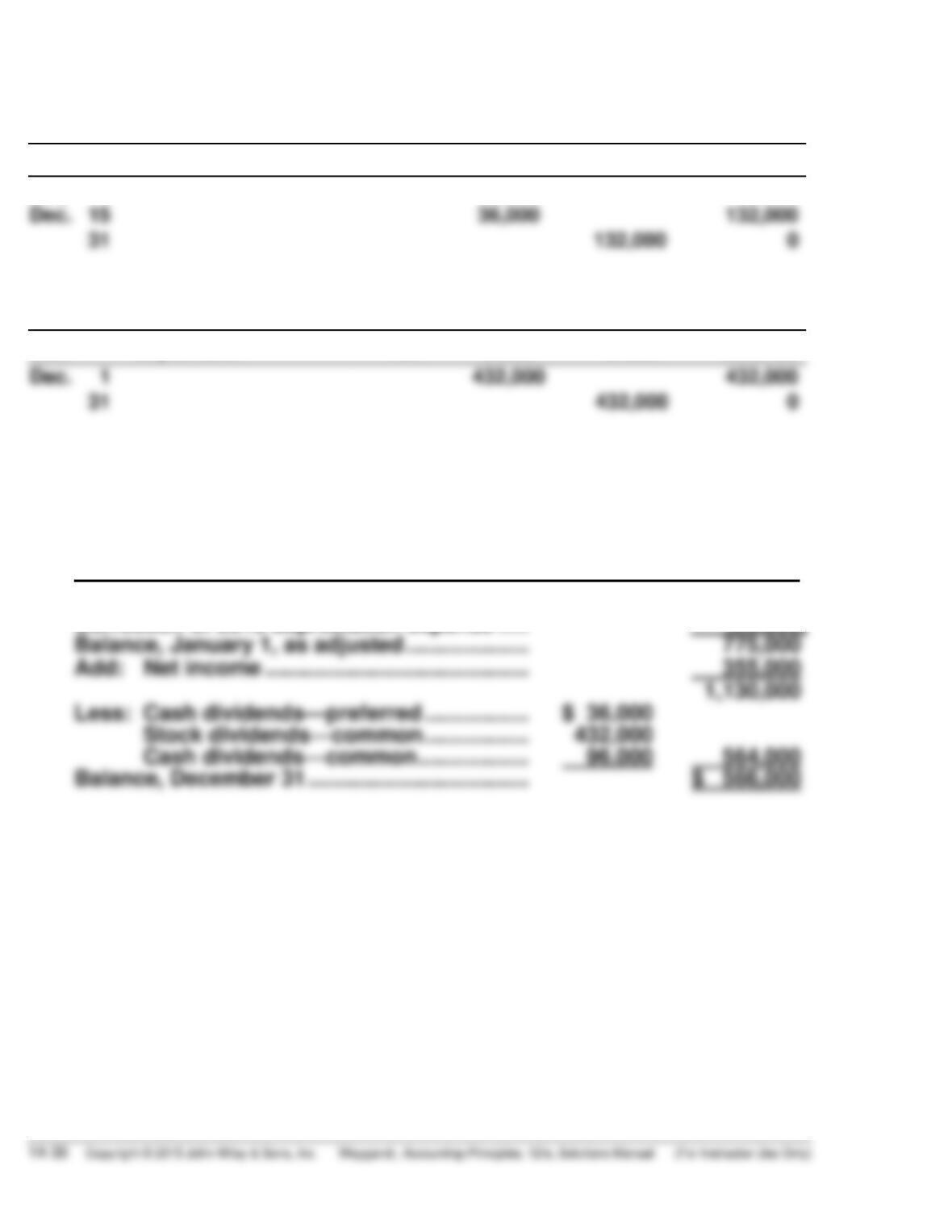

Dec. 1

120,000

120,000

Paid-in Capital in Excess of Par—Preferred Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Balance

200,000

Paid-in Capital in Excess of Par—Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Aug. 1

Balance

Prior period

adjustment—

depreciation

800,000

PROBLEM 14-2A (Continued)

Cash Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

July 1

96,000

96,000

Stock Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

(c) KARP COMPANY

Retained Earnings Statement

For the Year Ended December 31, 2017

Balance, January 1, as reported ……………….. $ 800,000

Correction of 2016 depreciation expense ….. (25,000)

PROBLEM 14-2A (Continued)

(d) KARP COMPANY

Balance Sheet (Partial)

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

6% Preferred stock, $50 par

value, 12,000 shares issued … $ 600,000

Additional paid-in capital

In excess of par—

preferred stock …………………… 200,000

In excess of par—

common stock……………………. 612,000

Total additional paid-in

PROBLEM 14-3A

(a)

Retained Earnings

Dec. 31 Balance 1,042,000

Sept. 1 Prior Per. Adj. 63,000

Jan. 1 Balance 1,170,000

(b) STOREY CORPORATION

Retained Earnings Statement

For the Year Ended December 31, 2017

Balance, January 1, as reported ……………… $1,170,000

Correction of overstatement of 2016 net

income because of understatement of

(c) STOREY CORPORATION

Partial Balance Sheet

December 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

6% Preferred stock,

PROBLEM 14-3A (Continued)

STOREY CORPORATION (Continued)

Common stock, $10 par value,

500,000 shares authorized,

250,000 shares issued and

outstanding ……………………… $2,500,000

Common stock dividends

distributable …………………….. 250,000 2,750,000

Note X: Retained earnings is restricted for plant expansion, $200,000.

(d) Total cash dividend ………………………………… $250,000

Allocated to preferred stock

PROBLEM 14-4A

(a) VEN CORPORATION

Partial Balance Sheet

March 31, 2017

Stockholders’ equity

Paid-in capital

Capital stock

Common stock, no-par value,

(b) VEN CORPORATION

Partial Balance Sheet

June 30, 2017

Stockholders’ equity

Paid-in capital

Capital stock

Common stock, no-par value,

(c) VEN CORPORATION

Partial Balance Sheet

September 30, 2017

Stockholders’ equity

Paid-in capital

Capital stock

Common stock, no-par value,