1. Two distinct obligations are incurred by a corporation when issuing bonds: (1) To pay the face

(maturity) amount of the bonds at a specified date. (2) To pay periodic interest at a specified

p

ercentage of the face amount.

2. a. Convertible bonds are bonds that may be exchanged for shares of stock under specifie

d

conditions.

b. Callable bonds give the issuing corporation the right to redeem the bonds before the

the maturity date.

5. Greater than the contract rate

6. a. Premium

b. $125,000 Premium

c. Premium on Bonds Payable

7. A loss of $50,000 [($5,000,000 × 0.98) – ($5,000,000 – $150,000)]

8. A mortgage note is an installment note that is secured by a pledge of the borrower’s assets.

If the borrower fails to pay the note, the lender has the right to take possession of the pledge

d

asset and sell it to pay off the debt.

p

p

10. a. As a current liability on the balance shee

t

b. As a long-term liability on the balance shee

t

CHAPTER 14

LONG-TERM LIABILITIES: BONDS AND NOTES

DISCUSSION QUESTIONS

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

PE 14-1A

Earnings before bond interest and income tax………

…

$ 400,000 $ 400,000

Interest on bonds……………………………………………

(150,000) (50,000)

Income before income tax…………………………………

$ 250,000 $ 350,000

Income tax……………………………………………………

(100,000) (140,000)

Net income……………………………………………………

$ 150,000 $ 210,000

1

$3,000,000 × 5%

2

$250,000 × 40%

3

$1,000,000 × 5%

PE 14-1B

Earnings before bond interest and income tax………

…

$3,000,000 $ 3,000,000

Interest on bonds……………………………………………

(600,000) (375,000)

Income before income tax…………………………………

$2,400,000 $ 2,625,000

Income tax……………………………………………………

(960,000) (1,050,000)

Net income……………………………………………………

$1,440,000 $ 1,575,000

…

1

$6,000,000 × 10%

2

$2,400,000 × 40%

3

$3,750,000 × 10%

4

$2,625,000 × 40%

PRACTICE EXERCISES

Plan 1 Plan 2

Plan 1 Plan 2

1

2

3

4

1

2

3

4

…

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

PE 14-2A

a.

Cash 3,500,000

Bonds Payable 3,500,000

b.

c.

Bonds Payable 3,500,000

Cash 3,500,000

PE 14-2B

b.

Interest Expense 21,000

Cash 21,000

c.

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

PE 14-3A

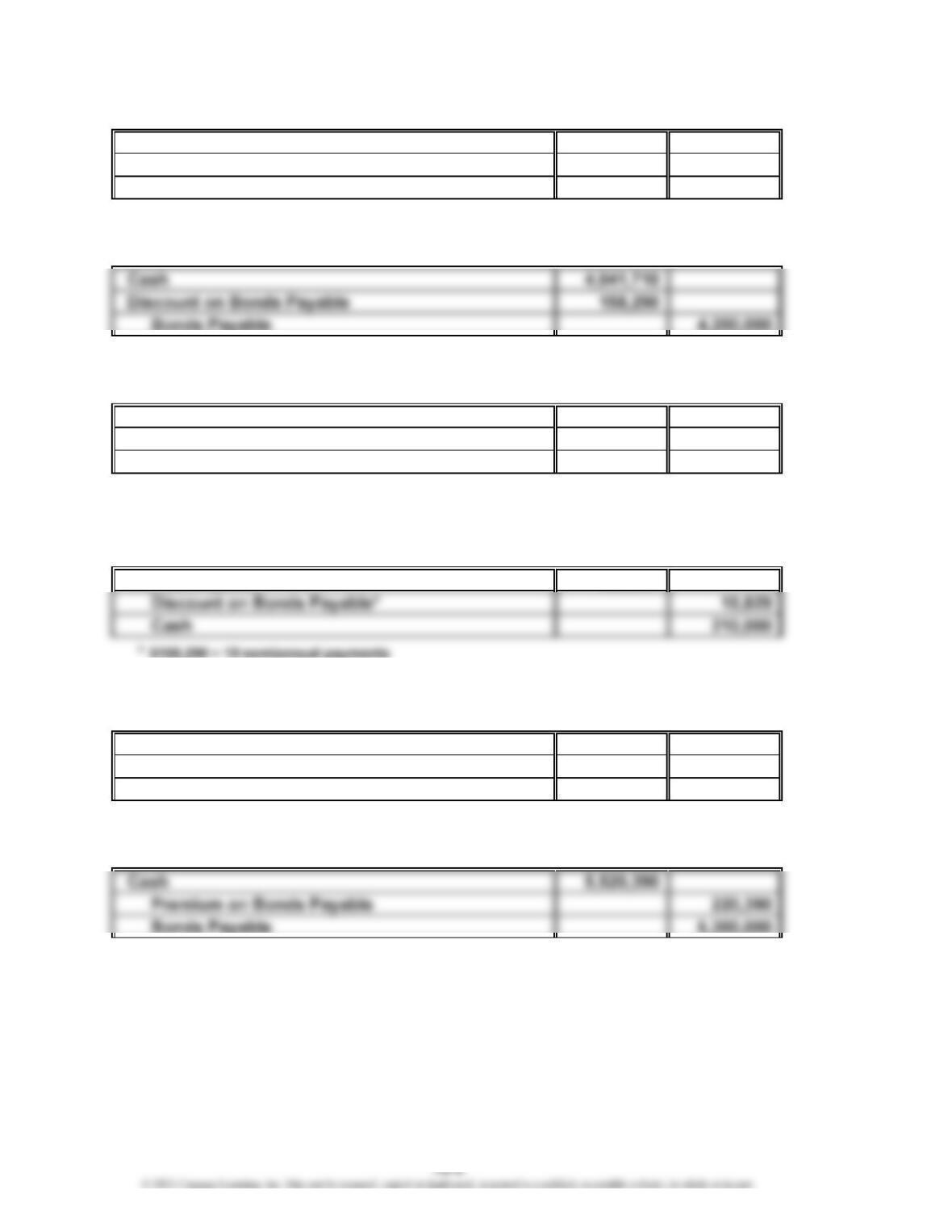

Cash 1,725,151

Discount on Bonds Payable 74,849

Bonds Payable 1,800,000

PE 14-3B

PE 14-4A

Interest Expense 61,485

Discount on Bonds Payable* 7,485

Cash 54,000

*$74,849 ÷ 10 semiannual payments

PE 14-4B

Interest Expense 225,829

PE 14-5A

Cash 8,932,035

Premium on Bonds Payable 332,035

Bonds Payable 8,600,000

PE 14-5B

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

PE 14-6A

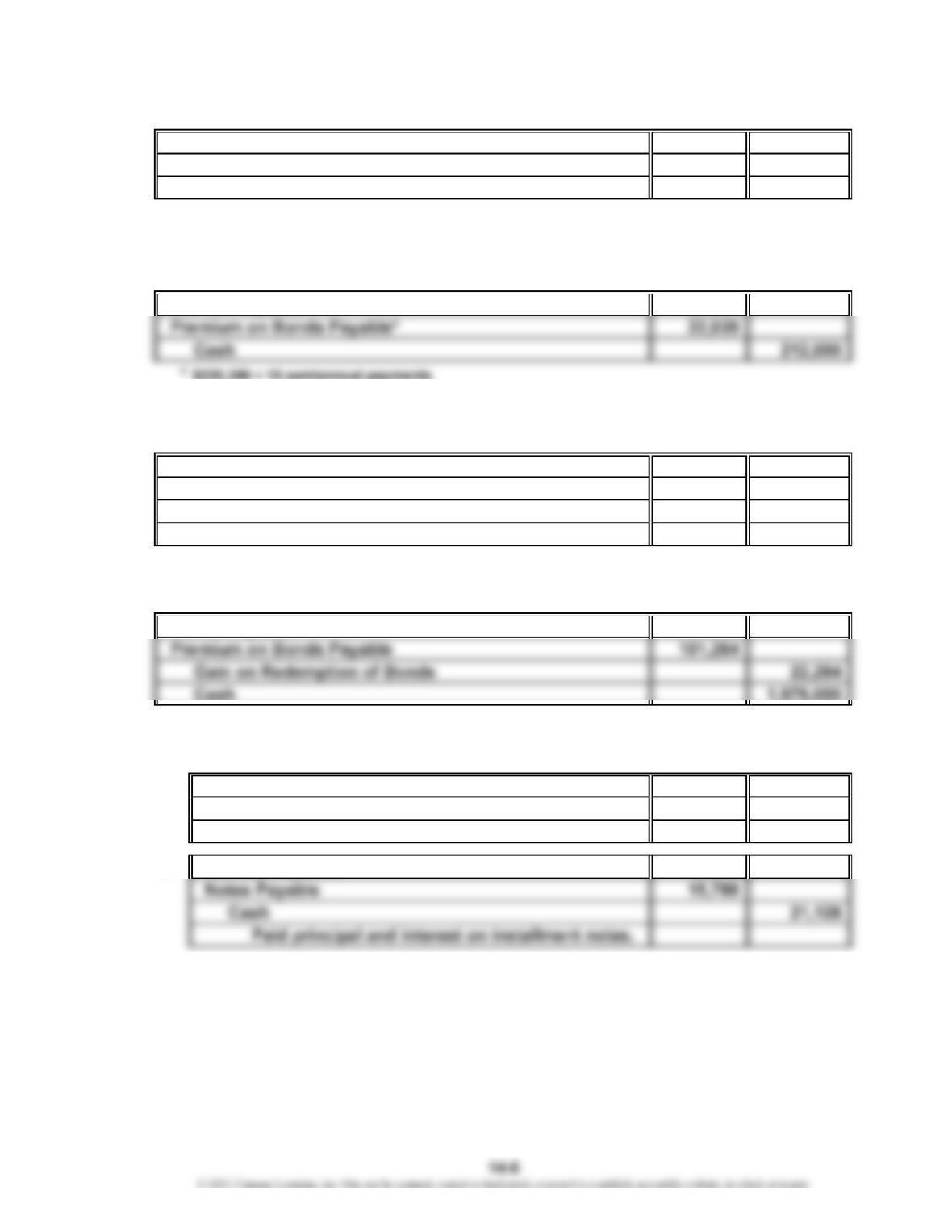

Interest Expense 439,796

Premium on Bonds Payable* 33,204

Cash 473,000

*$332,035 ÷ 10 semiannual payments

PE 14-6B

Interest Expense 189,961

PE 14-7A

Bonds Payable 2,300,000

Loss on Redemption of Bonds 38,500

Discount on Bonds Payable 107,500

Cash 2,231,000

PE 14-7B

Bonds Payable 1,900,000

PE 14-8A

a. Cash 89,000

Notes Payable 89,000

Issued installment notes for cash.

b. Interest Expense 5,340

PE 14-8B

a. Cash 35,000

Notes Payable 35,000

Issued installment notes for cash.

PE 14-9A

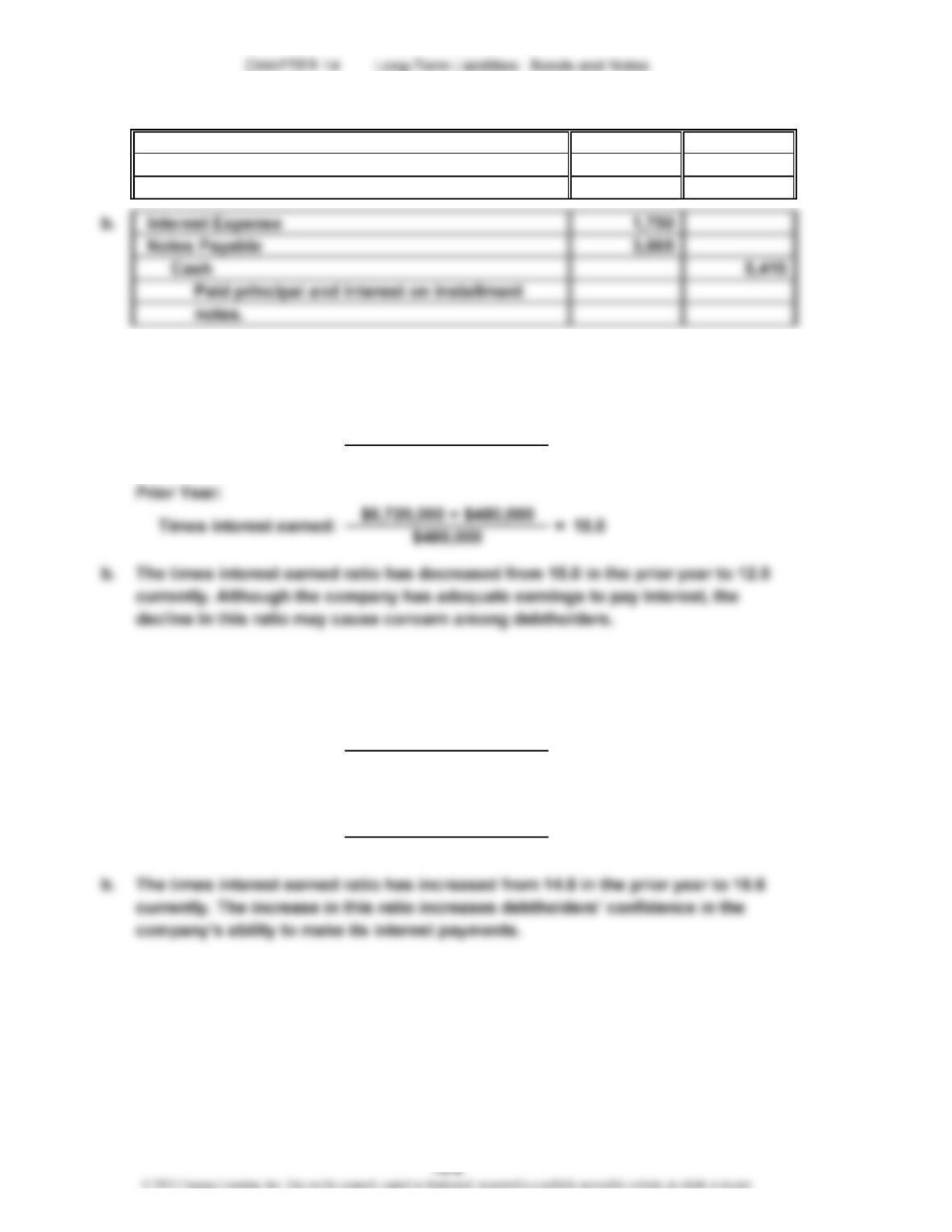

a. Current Year:

PE 14-9B

a. Current Year:

Prior Year:

=

12.0

Times interest earned: =

Times interest earned: =

16.6

14.8

$4,212,000 + $270,000

$3,450,000 + $250,000

$270,000

$250,000

Times interest earned: $5,610,000 + $510,000

$510,000

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Ex. 14-1

Domanico

Co.

a. Earnings before bond interest and income tax………………………

…

$ 900,000

Bond interest………………………………………………………………

…

(300,000)

Balance………………………………………………………………………

…

$ 600,000

Income tax…………………………………………………………………… (240,000)

b. Earnings before bond interest and income tax………………………

…

$1,100,000

Bond interest………………………………………………………………

…

(300,000)

Balance………………………………………………………………………

…

$ 800,000

Income tax…………………………………………………………………… (320,000)

Net income…………………………………………………………………

…

$ 480,000

Dividends on preferred stock……………………………………………

…

(60,000)

…

…

c. Earnings before bond interest and income tax………………………

…

$1,500,000

Bond interest………………………………………………………………

…

(300,000)

Balance………………………………………………………………………

…

$1,200,000

Income tax…………………………………………………………………… (480,000)

…

…

…

Earnings per share on common stock…………………………………

…

$ 3.30

*

** ($3,000,000 preferred stock ÷ $100 par value) × $2 preferred dividend per share

***

Ex. 14-2

Factors other than earnings per share that should be considered in evaluating

financing plans include: bonds represent a fixed annual interest requirement, while

EXERCISES

$6,000,000 bonds payable × 5% interest

$5,000,000 common stock ÷ $25 par value

*

*

**

*

…

…

…

…

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Ex. 14-3

Nike’s major source of financing is common stock. Nike has long-term debt; however,

the amount is less than 40% of stockholders’ equity.

Ex. 14-4

The bonds were selling at a discount. This is indicated by the selling price of 77.00,

Ex. 14-5

1 Cash 700,000

Bonds Payable 700,000

Ex. 14-6

a. 1. Cash 6,194,985

Discount on Bonds Payable 305,015

Bonds Payable 6,500,000

2. Interest Expense 252,918

Discount on Bonds Payable* 25,418

Cash** 227,500

May

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Ex. 14-6 (Concluded)

b. Annual interest paid ($6,500,000 × 7%)……………………………

…

$455,000

Discount amortized ($25,418 × 2)……………………………………

…

50,836

Interest expense for first year………………………………………… $505,836

Ex. 14-7

a. Apr. 1 Cash 36,492,785

Premium on Bonds Payable 1,492,785

Bonds Payable 35,000,000

Ex. 14-8

20Y1

1 Cash 11,000,000

Bonds Payable 11,000,000

1 Interest Expense* 495,000

Cash 495,000

Mar.

Sept.

20Y5

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Ex. 14-9

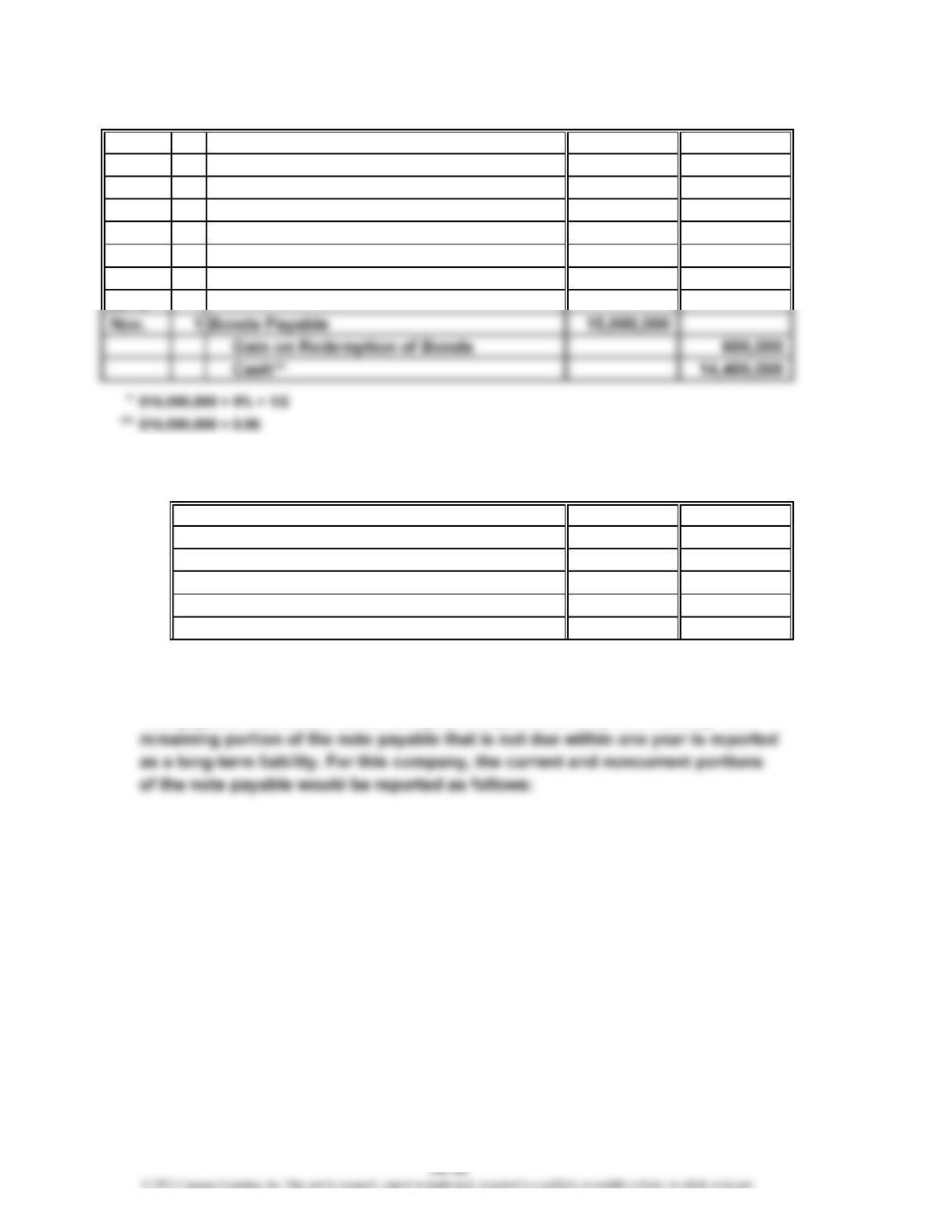

1 Cash 15,000,000

Bonds Payable 15,000,000

1 Interest Expense* 675,000

Cash 675,000

Ex. 14-10

a. 1. Cash 85,000

Notes Payable 85,000

2. Interest Expense* 5,950

Notes Payable 9,822

Cash 15,772

*$85,000 × 7%

b. Notes payable are reported as liabilities on the balance sheet. The portion of the

note payable that is due within one year is reported as a current liability. The

20Y1

Nov.

May

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Ex. 14-10 (Concluded)

Current liabilities:

Notes payable*…………………………………………………………………………

…

$10,510

* The principal repayment portion of the next installment payment. See computation below.

Noncurrent liabilities:

Notes payable**………………………………………………………………………… $64,668

** Original note payable…………………………………………………………………

…

$85,000

Principal repayment from Year 1……………………………………………………

…

9,822

Note payable balance at the end of Year 1………………………………………… $75,178

Ex. 14-11

1 Cash 170,000

Notes Payable 170,000

31 Interest Expense 13,600

Notes Payable 28,978

Cash 42,578

Year 1

Jan.

Dec.

…

…

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Ex. 14-12

a.

AB DE

Decrease Dec. 31

January 1 Note in Notes Carrying

Carrying Payment Payable Amount

Amount (Cash Paid) (B – C) (A – D)

$147,750 $ 43,620 $10,343 (7% of $147,750) $ 33,277 $114,473

114,473 43,620 8,013 (7% of $114,473) 35,607 78,866

b. Year 1

Jan. 1 Cash 147,750

Notes Payable 147,750

Year 2

Dec. 31 Interest Expense 8,013

Notes Payable 35,607

Cash 43,620

Year 3

Dec. 31 Interest Expense 5,521

Notes Payable 38,099

Cash 43,620

c. Interest expense of $10,343 would be reported on the income statement.

Amortization of Installment Notes

Year

Ending

C

Interest Expense

December 31 Note Carrying Amount)

(7% of January 1

Year 1

Year 2

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Ex. 14-13

1. The significant loss on redemption of the Simmons Industries bonds should be

reported in the Other Income and Expense section of the income statement,

rather than as cost of merchandise sold.

Ex. 14-14

a. Current Year:

b. The times interest earned ratio has decreased from 29.6 in the prior year to 25.2 in

the current year. Although Southwest Airlines had enough earnings to pay interest

in both years, the decline in this ratio in the current year may cause some concern

for debtholders.

Ex. 14-15

a. Current Year:

$310,500,000 + $13,500,000

$13,500,000

Times interest earned: = 25.2

$3,164,000,000 + $131,000,000

$131,000,000

Times interest earned: = 24.0

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Ex. 14-16

a. Current Year:

Appendix 1 Ex. 14-17

a. $1,000,000 × 0.75131 = $751,310

b. Cash on hand today can be invested to earn interest income. If $751,310 is invested

at 10%, it will be worth $1,000,000 at the end of three years.

Appendix 1 Ex. 14-18

a. First Year: =

Second Year: =

Third Year: =

Fourth Year: =

Total present value

Appendix 1 Ex. 14-19

$6,000,000 × 7.36009 = $44,160,540

163,260

152,580

$3,500,000 + $5,000,000

$5,000,000

$200,000 × 0.87344

$677,444

Times interest earned ratio: = 1.7

$200,000 × 0.93458

$200,000 × 0.81630

$200,000 × 0.76290

$186,916

174,688

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Appendix 1 Ex. 14-20

No. The present value of your winnings using an interest rate of 10% is $36,867,420

($6,000,000 × 6.14457), which is less than the present value of your winnings using

an interest rate of 6% ($44,160,540; see Ex. 14-19). This is because the winnings are

affected by the higher interest rate.

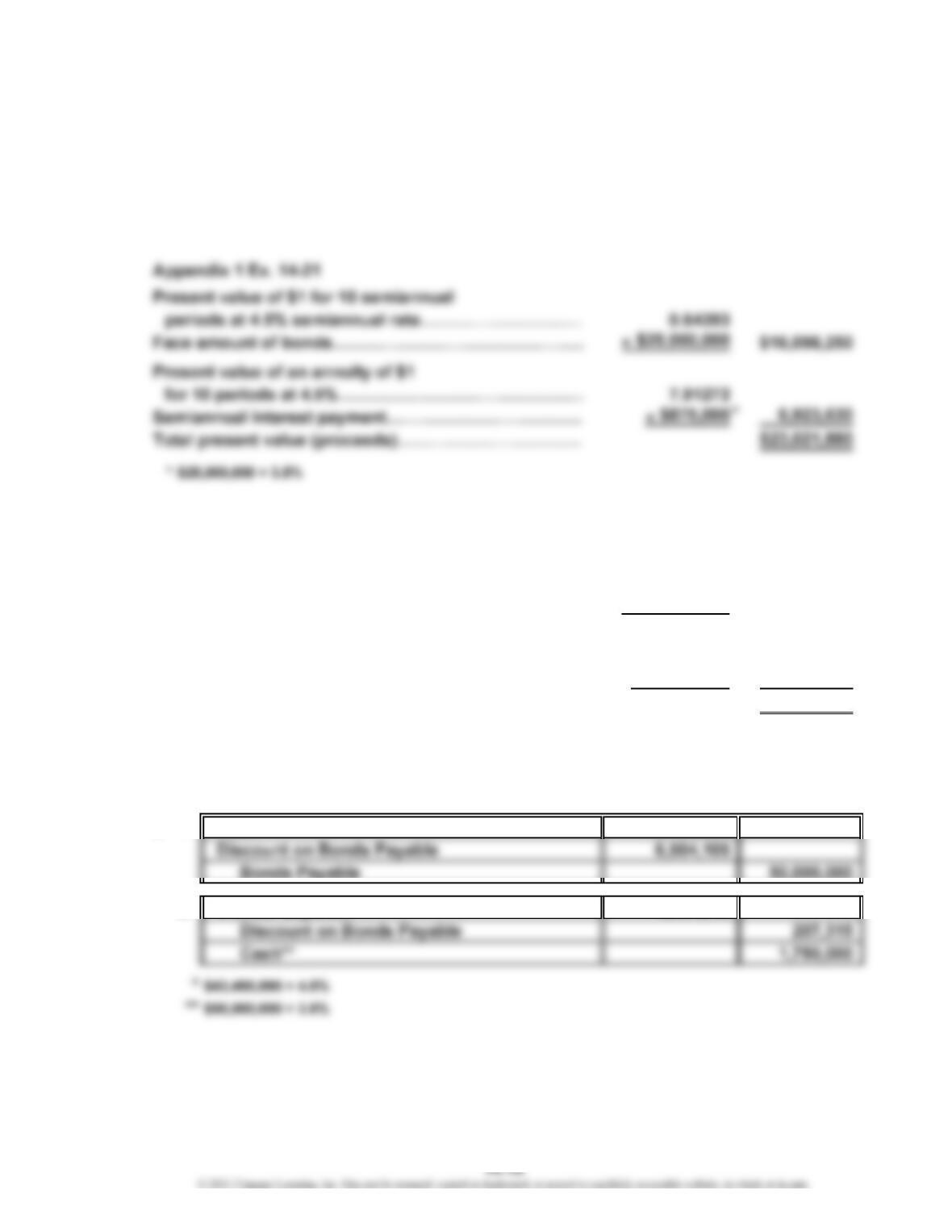

Appendix 1 Ex. 14-22

Present value of $1 for 10 semiannual

periods at 4.5% semiannual rate………………………

…

0.64393

Face amount of bonds……………………………………

…

$42,000,000 $27,045,060

Present value of an annuity of $1

for 10 semiannual periods at 4.5% semiannual rate

…

7.91272

Semiannual interest payment……………………………

…

$2,310,000 18,278,383

Total present value (proceeds)…………………………… $45,323,443

*

$42,000,000 × 5.5%

Appendix 2 Ex. 14-23

a. 1. Cash 43,495,895

2. Interest Expense* 1,957,315

×

×

*

…

…

…

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Appendix 2 Ex. 14-23 (Concluded)

3. Interest Expense* 1,966,644

Discount on Bonds Payable

Cash

*

($43,495,895 + $207,315) × 4.5%

Note: The following data in support of the proceeds of the bond issue stated in

the exercise are presented for the instructor’s information. Students are not

required to make the computations.

*

$50,000,000 × 3.5%

b. Annual interest paid…………………………………………………………

…

$3,500,000

Discount amortized*…………………………………………………………

…

423,959

Interest expense for first year……………………………………………… $3,923,959

*

$207,315 + $216,644

3. Interest Expense* 828,580

Premium on Bonds Payable 161,420

Cash

*

($23,829,684 – $155,961) × 3.5%

216,644

1,750,000

990,000

CHAPTER 14 Long-Term Liabilities: Bonds and Notes

Appendix 2 Ex. 14-24 (Concluded)

b. Annual interest paid……………………………………………………………

…

$1,980,000

Premium amortized*……………………………………………………………

…

(317,381)

Interest expense for first year………………………………………………

…

$1,662,619

*

$155,961 + $161,420

Appendix 1 and Appendix 2 Ex. 14-25

a. Present value of $1 for 10 semiannual

periods at 5% semiannual rate……………………… 0.61391

Face amount of bonds…………………………………

…

$35,000,000 $21,486,850

Present value of an annuity of $1 for 10

semiannual periods at 5% semiannual rate………

…

7.72173

Semiannual interest payment…………………………

…

$2,100,000 16,215,633

Proceeds of bond sale…………………………………………………………

…

$37,702,483

…

…

c. Second semiannual interest payment………………………………………

…

$ 2,100,000

5% of carrying amount of $37,487,607*……………………………………

…

(1,874,380)

Premium amortized……………………………………………………………

…

$ 225,620

*

$37,702,483 – $214,876

…

…

…

×

×